Market Overview

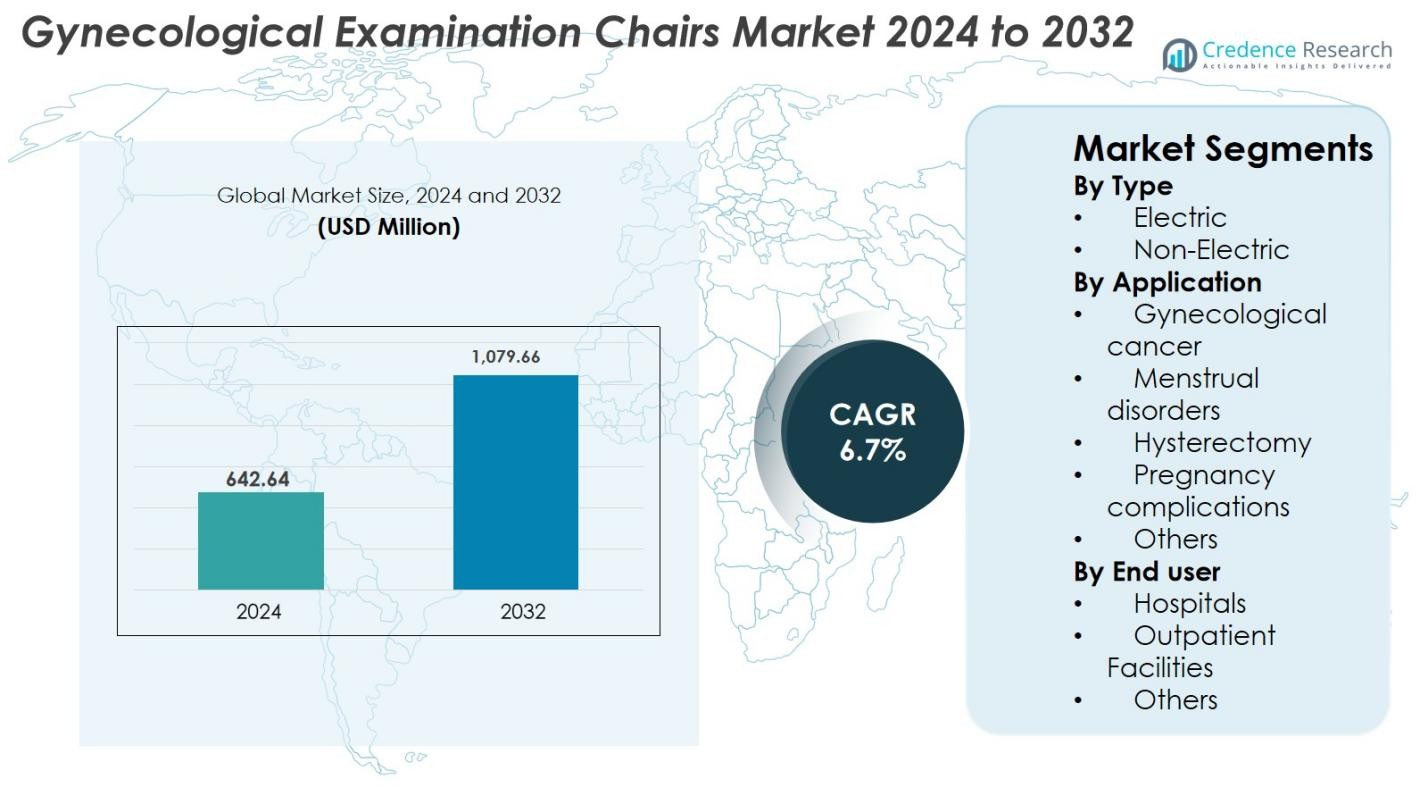

Gynecological Examination Chairs Market size was valued at USD 642.64 Million in 2024 and is anticipated to reach USD 1,079.66 Million by 2032, at a CAGR of 6.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Gynecological Examination Chairs Market Size 2024 |

USD 642.64 Million |

| Gynecological Examination Chairs Market, CAGR |

6.7% |

| Gynecological Examination Chairs Market Size 2032 |

USD 1,079.66 Million |

Gynecological Examination Chairs Market is characterized by strong participation from leading manufacturers such as medifa, SCHMITZ, Favero Health Projects Spa, Novak M., Malvestio Spa, Ocura, Tronwind Industries, AGA SANITÄTSARTIKEL GMBH, Zhangjiagang Medi Medical Equipment Co., Ltd., and Brouwer B.V., all of which focus on ergonomic designs, electric automation, and improved hygiene features. North America led the market in 2024 with a 34.6% share, driven by advanced healthcare infrastructure and high adoption of technologically enhanced chairs, followed by Europe with 29.4%, supported by stringent clinical standards and modernization of women’s health facilities. Asia-Pacific, holding 23.8%, emerged as the fastest-growing region due to expanding healthcare access and rising demand for specialized gynecological equipment.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Gynecological Examination Chairs Market reached USD 642.64 Million in 2024 and will grow at a CAGR of 6.7% to reach USD 1,079.66 Million by 2032.

- Market growth is driven by rising gynecological screenings, increasing prevalence of reproductive health disorders, and strong demand for electric chairs, which held a 63.4% share in 2024.

- Emerging trends include adoption of motorized adjustments, antimicrobial materials, compact outpatient-focused designs, and integration of digital features to improve workflow efficiency.

- Major players such as medifa, SCHMITZ, Favero Health Projects Spa, Malvestio Spa, Novak M., Ocura, Tronwind Industries, and AGA SANITÄTSARTIKEL GMBH focus on innovation, improved ergonomics, and expansion into high-growth markets.

- North America led with 34.6% share in 2024, followed by Europe at 29.4% and Asia-Pacific at 23.8%, while pregnancy complication applications dominated with 31.8% segment share.

Market Segmentation Analysis

Market Segmentation Analysis

By Type

The Gynecological Examination Chairs market is segmented into electric and non-electric models, with electric chairs dominating the segment with a 63.4% share in 2024. Their leadership is driven by increasing adoption of motorized height adjustment, programmable positioning, and enhanced ergonomic support that improves patient comfort and clinician workflow. Hospitals and specialty clinics prefer electric systems for precision during procedures such as biopsies, colposcopy, and minimally invasive interventions. Rising investments in modernizing outpatient facilities and the growing shift toward technologically advanced examination infrastructure further strengthen demand for electric chairs across global markets.

- For Instance, SCHMITZ expanded its updated gynae treatment table ARCO-matic® line, featuring programmable seat elevation and Trendelenburg positioning designed to reduce operator fatigue during prolonged examinations.

By Application

Within the application segment, pregnancy complications accounted for the largest share at 31.8% in 2024, driven by the rising prevalence of high-risk pregnancies, increasing maternal age, and greater emphasis on routine monitoring and diagnostic evaluations. Gynecological chairs supporting ultrasound examinations, pelvic assessments, and emergency evaluations are widely utilized in obstetrics departments. Additionally, demand grows across menstrual disorder management and hysterectomy-related diagnostics as minimally invasive gynecologic procedures expand. Increased cancer screening programs also boost adoption in gynecological oncology settings, though their share remains lower than pregnancy-related applications.

- For Instance, The GE Healthcare “Voluson” line of women’s-health ultrasound systems including products such as the Voluson E6 and S8 is marketed specifically for gynecology and prenatal imaging.

By End User

Among end users, hospitals held the dominant share of 54.7% in 2024, supported by high patient volumes, advanced diagnostic capabilities, and continuous upgrades in women’s health infrastructure. Hospitals increasingly favor adjustable, electro-hydraulic chairs that enhance procedural efficiency in labor wards, oncology units, and general gynecology departments. Outpatient facilities follow as the fastest-growing segment due to rising demand for routine reproductive health checkups and fertility assessments. The expansion of standalone women’s health clinics, combined with improved insurance coverage and increased awareness of preventive gynecological care, continues driving adoption across diversified care settings.

Key Growth Drivers

Ergonomic Advancements and Technology Integration

Ergonomic and technological enhancements represent a major growth driver in the Gynecological Examination Chairs market as healthcare providers prioritize patient comfort, procedural efficiency, and clinician safety. The shift toward motorized, programmable, and electro-hydraulic systems enhances precision during pelvic exams, biopsies, and minimally invasive gynecologic procedures. Features such as memory positioning, antimicrobial upholstery, modular accessories, and improved weight-bearing capacity support broader clinical use cases. Integration of sensors and digital connectivity enables better workflow management and maintenance tracking. As modern women’s health departments standardize advanced equipment to improve clinical outcomes and reduce fatigue among healthcare professionals, demand for technologically superior chairs continues to accelerate across both developed and emerging markets.

- For instance, Midmark’s 631 Procedure Chair offers 8-way powered positioning and lowers to a 17-inch seat height for compliant wheelchair transfers, supporting patients up to 650 pounds with Active Sensing Technology that pauses movement on impact detection.

Rising Gynecological Disease Burden and Screening Programs

The growing prevalence of gynecological disorders—including endometriosis, uterine fibroids, infertility, pelvic inflammatory disease, and high-risk pregnancies—significantly fuels market growth. Increasing government and institutional focus on early diagnosis and preventive care has expanded gynecological screening programs worldwide, driving higher procedural volumes in hospitals and outpatient clinics. National cervical and breast cancer screening initiatives also require frequent pelvic examinations, contributing to rising equipment demand. Aging populations and delayed pregnancies further increase the incidence of complications requiring routine monitoring. The rising availability of insurance coverage for women’s health services and investments in reproductive health infrastructure enhance accessibility, resulting in sustained demand for advanced examination chairs tailored to diverse diagnostic and therapeutic needs.

- For Instance, The World Health Organization reports that endometriosis affects approximately 10% of women of reproductive age, increasing the need for ongoing pelvic evaluations and specialized exam equipment.

Expansion of Outpatient and Ambulatory Care Settings

The rapid growth of outpatient gynecology clinics and ambulatory care centers serves as another key growth driver, supported by a global shift toward cost-effective and patient-centric care delivery models. Outpatient settings increasingly handle routine examinations, fertility assessments, prenatal monitoring, and minimally invasive procedures that require compact, adjustable, and high-functionality examination chairs. Their growth is reinforced by improved reimbursement frameworks, shorter waiting times, and the rising popularity of specialized women’s health centers. Manufacturers address this demand by offering space-efficient designs, integrated storage, and mobile configurations suitable for smaller clinical environments. As decentralized care grows across both developed and emerging regions, adoption of versatile and ergonomically optimized chairs is expected to accelerate significantly.

Key Trends & Opportunities

Adoption of Smart and Connected Examination Systems

A key trend reshaping the Gynecological Examination Chairs market is the adoption of smart, digitally connected systems that enhance operational efficiency and clinical outcomes. Chairs equipped with IoT sensors, remote diagnostics, usage tracking, and automated maintenance alerts help healthcare providers optimize performance and reduce downtime. Integration with electronic health records (EHRs) and imaging devices supports seamless workflows and improves documentation accuracy. Smart features also allow personalized positioning and pressure monitoring, improving patient comfort and reducing examination variability. As hospitals prioritize digital transformation and automation, demand for technologically advanced, connected gynecological chairs continues to rise.

- For instance, in 2023 SCHMITZ introduced updated functionalities for its medi-matic® 115.0 chair, adding programmable positions and hygiene-focused digital controls designed to streamline workflow and reduce manual adjustments.

Growing Focus on Infection Control and Hygiene Compliance

Strengthening infection control regulations and heightened emphasis on patient safety create substantial opportunities for manufacturers. Innovations in antimicrobial upholstery, seamless surfaces, easy-clean designs, and disposable accessories address the need for strict hygiene compliance in gynecology departments. Enhanced sterilization compatibility and low-maintenance materials further support safe repetitive use. Increasing awareness of hospital-acquired infections (HAIs) and regulatory mandates for hygienic equipment drive accelerated replacement cycles across healthcare settings. Manufacturers leveraging advanced materials science, surface coatings, and modular hygiene-focused designs are well positioned to capture growing demand from hospitals and outpatient care providers prioritizing safety and regulatory compliance.

- For instance, Lemi MD a medical-chair supplier builds its gynecology-sector chairs using high-quality, easy-to-clean materials designed for frequent sanitization, which supports strict hospital hygiene protocols.

Key Challenges

High Cost of Advanced Examination Chairs

One of the major challenges in the Gynecological Examination Chairs market is the high cost associated with technologically advanced electric and electro-hydraulic models. Premium features such as programmable controls, integrated sensors, and specialized ergonomic configurations significantly increase purchase and maintenance expenses, limiting adoption in small clinics and low-income regions. Budget constraints in public hospitals further slow replacement cycles. While cost-effective non-electric chairs exist, they lack the efficiency and functionality required for complex diagnostic procedures. This cost disparity creates market imbalance, restricting widespread modernization of women’s health infrastructure in developing economies.

Limited Awareness and Uneven Healthcare Infrastructure

Unequal healthcare access and limited awareness about routine gynecological screening remain significant barriers to market expansion, especially in rural and underserved regions. Inadequate infrastructure, shortage of trained gynecology professionals, and low prioritization of women’s health services reduce demand for specialized equipment. Cultural barriers and low awareness regarding preventive care lead to delayed diagnosis, resulting in fewer routine examinations where such chairs are essential. Many developing nations also face slow adoption of modern equipment due to procurement challenges, lack of funding, and outdated clinical setups. These disparities hinder market penetration despite rising global emphasis on women’s health.

Regional Analysis

North America

North America dominated the Gynecological Examination Chairs market with a 34.6% share in 2024, driven by advanced women’s health infrastructure, high adoption of electric and smart chairs, and strong reimbursement frameworks. The U.S. leads due to rising gynecological procedure volumes, high awareness of preventive screening, and continuous upgrades in hospital equipment. Growth is further supported by technological innovation, integration of digital features, and increasing investments in outpatient and ambulatory care centers. Expanding fertility services and increasing prevalence of gynecological conditions also contribute to sustained regional demand.

Europe

Europe held a 29.4% market share in 2024, supported by well-established healthcare systems, strong emphasis on early gynecological diagnosis, and increasing modernization of women’s health facilities. Countries such as Germany, France, Italy, and the U.K. drive demand through high procedural adoption and stringent hygiene regulations that encourage procurement of advanced, easy-to-clean examination chairs. The region also benefits from growing investments in maternal care infrastructure and expanding geriatric female populations requiring frequent diagnostic assessments. Rising preference for ergonomically designed and electrically operated chairs further strengthens market growth across both Western and Eastern Europe.

Asia-Pacific

Asia-Pacific emerged as the fastest-growing region, accounting for 23.8% of the market share in 2024, fueled by expanding healthcare infrastructure, rising awareness of women’s health, and increasing government focus on maternal and reproductive care. Rapid growth in China, India, Japan, and South Korea is driven by higher rates of gynecological disorders, growing fertility clinics, and modernization of hospitals. The shift toward urban healthcare facilities and rising demand for cost-effective yet advanced examination chairs promote market penetration. Increasing healthcare expenditure and growing adoption of electric chairs in premium clinics further support regional expansion.

Latin America

Latin America captured 7.1% of the market share in 2024, with growth led by Brazil, Mexico, and Argentina. Rising awareness of prenatal screening, increasing investment in maternity wards, and the expansion of private healthcare facilities support market development. Adoption is gradually shifting from non-electric to electric models as clinics modernize their gynecology departments. However, budget constraints and uneven healthcare access across rural regions slow overall penetration. Government programs aimed at improving women’s health services, along with the increasing presence of international medical equipment manufacturers, are contributing to steady regional growth.

Middle East & Africa

The Middle East & Africa region accounted for 5.1% of the market share in 2024, driven by expanding women’s specialty hospitals, rising investments in modern diagnostic facilities, and increasing focus on maternal healthcare. Gulf countries, including Saudi Arabia and the UAE, lead adoption of advanced electric chairs due to higher healthcare spending and rapid infrastructure development. In Africa, market growth remains moderate due to limited awareness and constrained budgets, though improving access to primary healthcare and international aid programs are gradually enhancing women’s health services. Growing private healthcare investments are expected to support future market expansion.

Market Segmentations

By Type

By Application

- Gynecological cancer

- Menstrual disorders

- Hysterectomy

- Pregnancy complications

- Others

By End user

- Hospitals

- Outpatient Facilities

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Gynecological Examination Chairs market features a diverse and expanding competitive landscape, with manufacturers focusing on ergonomic innovation, advanced motorized systems, and enhanced hygiene features to strengthen their market presence. Leading companies such as medifa, Novak M., SCHMITZ, Favero Health Projects Spa, Malvestio Spa, AGA SANITÄTSARTIKEL GMBH, Tronwind Industries, Ocura, Zhangjiagang Medi Medical Equipment Co., Ltd., and Brouwer B.V. compete through continuous product upgrades, modular designs, and customizable configurations tailored for hospitals and outpatient facilities. Many players emphasize digital integration, antimicrobial materials, and compact models suited for modern gynecology departments. Strategic initiatives, including facility expansions, product launches, distributor partnerships, and geographic expansion into high-growth regions such as Asia-Pacific and Latin America, further accelerate competitive intensity. The market also witnesses increasing adoption of premium electric chairs, prompting manufacturers to differentiate through superior durability, automated positioning, and enhanced patient comfort features, positioning themselves to meet the growing demand for technologically advanced women’s health equipment.

Key Player Analysis

- Tronwind Industries Co. Limited

- SCHMITZ

- Favero Health Projects Spa

- Ocura

- Novak M.

- Zhangjiagang Medi Medical Equipment Co., Ltd.

- Malvestio Spa

- AGA SANITÄTSARTIKEL GMBH

- medifa

- Brouwer B.V.

Recent Developments

- In May 2025, Midmark launched the first USAB-compliant 17-inch transfer-height gynecological examination procedure chair, specifically targeting accessibility needs

- In June 2023, Novak M. introduced a new gynecological examination chair with hydraulic adjustments focused on enhancing patient comfort and procedural efficiency in clinical environments.

- In April 2023, Medistar acquired a leading manufacturer of gynecological examination chairs to expand its product portfolio and strengthen its global presence in the Gynecological Examination Chairs Market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for advanced electric and automated gynecological examination chairs will continue to rise across hospitals and outpatient facilities.

- Adoption of smart, sensor-enabled and digitally connected chairs will increase as healthcare providers modernize clinical workflows.

- Infection-control–focused designs with antimicrobial surfaces and seamless upholstery will gain stronger market preference.

- Outpatient gynecology and fertility clinics will drive higher procurement as decentralized care models expand.

- Manufacturers will invest more in ergonomic innovations to improve patient comfort and clinician efficiency.

- Growth in preventive screening programs and rising gynecological disease burden will elevate procedure volumes globally.

- Asia-Pacific will emerge as the fastest-growing regional market supported by healthcare infrastructure expansion.

- Partnerships between medical equipment companies and distributors will strengthen market penetration in developing regions.

- Customizable and modular chair designs will gain traction to meet diverse clinical requirements.

- Replacement demand will rise as healthcare facilities shift from manual to motorized and digitally enhanced examination chairs.