| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Spine Degenerative Disk Disease Treatment Market Size 2024 |

USD 28,140.7 million |

| Spine Degenerative Disk Disease Treatment Market, CAGR |

4.39% |

| Spine Degenerative Disk Disease Treatment Market Size 2032 |

USD 39,589.9 million |

Market Overview

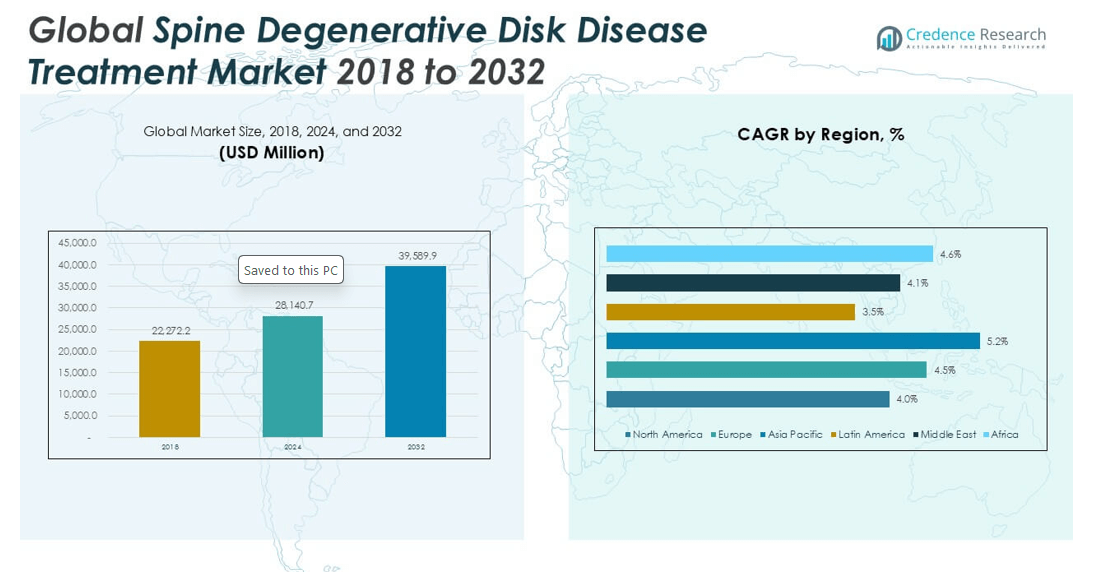

The Global Spine Degenerative Disk Disease Treatment Market is projected to grow from USD 28,140.7 million in 2024 to an estimated USD 39,589.9 million by 2032, with a compound annual growth rate (CAGR) of 4.39% from 2025 to 2032.

Key drivers of the market include the growing geriatric population globally, increasing incidence of obesity and sedentary lifestyles, and a higher awareness of spine-related disorders. Additionally, technological advancements such as image-guided surgery, robot-assisted procedures, and biologics for spinal regeneration are accelerating adoption across healthcare facilities. The trend toward outpatient surgical procedures and minimally invasive techniques continues to reduce recovery times and hospitalization costs, enhancing market acceptance.

Geographically, North America dominates the Global Spine Degenerative Disk Disease Treatment Market due to robust healthcare infrastructure, favorable reimbursement policies, and high diagnosis rates. Europe follows closely, supported by advanced medical facilities and increasing patient awareness. The Asia-Pacific region is projected to witness the fastest growth, driven by a large aging population, rising healthcare investments, and expanding access to advanced spinal treatments. Key players in the market include Medtronic, Johnson & Johnson (DePuy Synthes), Stryker Corporation, Zimmer Biomet, NuVasive, Globus Medical, Aesculap Implant Systems, and Orthofix Medical Inc., who focus on strategic innovation, R&D, and global expansion

Market Insights

- The market is projected to grow from USD 28,140.7 million in 2024 to USD 39,589.9 million by 2032, registering a CAGR of 4.39% from 2025 to 2032.

- Rising geriatric population and sedentary lifestyles are key drivers accelerating the demand for both surgical and non-surgical spine treatments.

- Technological advancements such as robot-assisted surgery, image-guided procedures, and biologics are enhancing treatment outcomes and boosting market adoption.

- High treatment costs and limited insurance coverage in some regions remain significant restraints affecting access and overall market penetration.

- North America holds the largest market share due to robust healthcare infrastructure and high diagnosis rates of spinal disorders.

- Asia-Pacific is the fastest-growing region, driven by aging demographics, improving healthcare investments, and broader access to advanced spinal care.

- The market reflects moderate to high concentration, with key players focusing on innovation, strategic partnerships, and global expansion to maintain competitiveness.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Aging Population and Increased Prevalence of Degenerative Conditions Drive Market Demand

The growing global aging population remains a primary driver of the Global Spine Degenerative Disk Disease Treatment Market. With age, spinal discs naturally deteriorate, making older adults more susceptible to degenerative disk disease. This demographic trend directly contributes to rising case volumes and increased demand for treatment solutions. Healthcare systems worldwide are experiencing higher patient loads related to spine-related ailments. The market responds with expanded services, specialized care units, and targeted therapies for elderly patients. It benefits from the parallel rise in chronic conditions such as arthritis and osteoporosis, which often coexist with degenerative disk disease. These factors sustain consistent market growth and long-term demand.

- For instance, research indicates that approximately 40% of adults aged 40 to 59 experience moderate to severe degeneration of intervertebral discs, and the global share of individuals aged 65 and older is projected to rise from 10.3% in 2024 to over 20% by 2074, resulting in a substantial increase in spine-related healthcare needs

Technological Advancements in Surgical and Non-surgical Interventions Enhance Treatment Outcomes

Advancements in medical technology continue to improve the safety, precision, and efficacy of both surgical and non-surgical treatments for spine disorders. Image-guided navigation, robotic-assisted spine surgery, and next-generation implants help minimize risks and optimize patient recovery. Innovations in biomaterials and regenerative medicine offer new avenues for restoring disk function and reducing pain. The Global Spine Degenerative Disk Disease Treatment Market sees increased adoption of artificial disk replacements and biologics due to their improved outcomes and shorter recovery times. Hospitals and surgical centers invest heavily in modern equipment to meet patient expectations. These innovations help healthcare providers offer more effective and less invasive options.

- For instance, over 4.83 million spinal operations are performed annually worldwide, with more than 1.34 million in the United States alone, and the adoption of robotic-assisted spine surgery is increasing rapidly—driven by the proven benefits of enhanced precision and reduced recovery times.

Rise in Sedentary Lifestyles and Occupational Hazards Increases Disease Incidence

Urban lifestyles, characterized by prolonged sitting, poor posture, and low physical activity, contribute to a rising incidence of spine-related conditions. Desk-based occupations and increased screen time have led to more cases of lower back and neck pain, often progressing to degenerative disk disease. The market responds by expanding treatment offerings for younger demographics who experience early onset symptoms. It also sees growing demand for physical therapy, pain management, and early intervention strategies. Awareness campaigns encourage early diagnosis and proactive treatment. These lifestyle-related factors play a significant role in market expansion across both developed and developing region

Improved Access to Healthcare and Rising Awareness Bolster Market Penetration

Access to advanced spine care is improving globally through better healthcare infrastructure, increased insurance coverage, and growing awareness of spinal health. Emerging economies are witnessing rising investment in neurosurgery and orthopedic specialties. Governments and private entities are funding healthcare modernization programs to meet patient needs. The Global Spine Degenerative Disk Disease Treatment Market benefits from broader acceptance of minimally invasive procedures and outpatient care models. Awareness about symptoms and available treatment options motivates patients to seek earlier medical attention. These shifts collectively enhance treatment uptake and create a favorable environment for sustained market growth.

Market Trends

Rising Adoption of Minimally Invasive and Outpatient Spine Procedures

Healthcare providers increasingly prefer minimally invasive procedures for treating degenerative spine conditions due to reduced recovery times and lower complication risks. Techniques such as microdiscectomy, endoscopic spine surgery, and laser-assisted interventions are gaining traction. These procedures require smaller incisions and allow patients to return to daily activities more quickly. Hospitals and ambulatory surgical centers are expanding outpatient services to meet this demand. The Global Spine Degenerative Disk Disease Treatment Market reflects this shift by supporting advanced training and infrastructure investments. It also encourages the development of devices and tools tailored for minimally invasive use.

- For instance, from 2018 through 2024, nearly 900,000 outpatient spinal procedures were performed in ASCs in the United States, with the annual number of such procedures increasing by nearly 8% each year from 2021 to 2024. Outpatient spine surgery volume rose by 18% in 2023 alone, and the total number of outpatient spine procedures increased by approximately 193% from 2010 to 2021

Integration of Advanced Imaging and Navigation Technologies in Spine Surgery

Technology plays a central role in improving surgical precision and patient outcomes in spine treatments. Surgeons now rely on intraoperative imaging, real-time navigation systems, and robotic assistance to enhance accuracy and reduce complications. These tools support complex procedures while minimizing damage to surrounding tissues. The trend is particularly strong in advanced markets with high patient expectations and reimbursement support. The Global Spine Degenerative Disk Disease Treatment Market continues to evolve with investments in AI-driven diagnostics and augmented reality systems. It promotes seamless integration of digital technologies into spine care workflows.

- For instance, a 2025 global survey found that nearly half (49%) of spine surgeons reported occasional or frequent use of navigation assistance during spinal instrumentation procedures, while 18% reported using robotic assistance. The use of computer-assisted navigation in cervical spine surgeries has increased approximately tenfold between 2015 and 2024, with augmented reality and AI-driven systems emerging as key areas of investment

Growing Emphasis on Regenerative Therapies and Biologic Solutions

Research in stem cell therapies, tissue engineering, and biologic agents is shaping the future of spinal disk regeneration. Regenerative treatments offer alternatives to traditional surgery, particularly in early-stage degeneration. These therapies aim to restore disc function, reduce inflammation, and slow disease progression. Startups and established medical companies are investing in clinical trials to validate the safety and efficacy of these solutions. The Global Spine Degenerative Disk Disease Treatment Market supports innovation by facilitating regulatory pathways and funding collaborations. It sees increasing interest from physicians and patients seeking less invasive and long-lasting solutions.

Expansion of Telehealth and Digital Monitoring in Spine Care Management

Digital health platforms are transforming how patients access diagnosis, treatment planning, and follow-up care. Telehealth services enable virtual consultations, especially useful for chronic pain management and postoperative monitoring. Mobile apps and wearable devices support remote physiotherapy, pain tracking, and medication reminders. These tools increase patient engagement and reduce the burden on healthcare facilities. The Global Spine Degenerative Disk Disease Treatment Market embraces digital innovation to improve continuity of care and outcomes. It aligns with broader trends toward personalized, tech-enabled healthcare delivery.

Market Challenges

High Treatment Costs and Limited Reimbursement Pose Barriers to Access

The high cost of advanced spinal procedures, implants, and biologics creates financial barriers for many patients. Insurance coverage often excludes newer or minimally invasive treatments, leaving patients to bear significant out-of-pocket expenses. These cost constraints limit access, particularly in low- and middle-income regions. Hospitals and providers also face challenges in justifying capital investments without guaranteed returns. The Global Spine Degenerative Disk Disease Treatment Market faces pressure to deliver cost-effective solutions without compromising care quality. It must balance innovation with affordability to ensure broader patient reach.

- For instance, in 2024, an international health technology survey found that more than 3,200 hospitals in Asia and Latin America postponed or canceled purchases of advanced spinal surgery systems due to acquisition costs exceeding $200,000 per unit, while over 1,400 facilities reported patient complaints about out-of-pocket expenses for minimally invasive spinal implants and biologics, according to procurement records and government health agency reports.

Surgical Risks, Postoperative Complications, and Skill Gaps Affect Outcomes

Spine surgeries, though advanced, still carry risks such as infection, nerve damage, and implant failure. Postoperative complications can lead to extended recovery times or additional interventions. Surgeon skill variability further impacts treatment outcomes, especially in resource-constrained settings. Training and standardization remain critical concerns for healthcare systems adopting new techniques. The Global Spine Degenerative Disk Disease Treatment Market must address these clinical risks through improved training, robust clinical protocols, and continuous innovation. It relies on partnerships between device manufacturers and healthcare institutions to ensure safety and consistency in patient care.

Market Opportunities

Expansion into Emerging Markets with Growing Healthcare Infrastructure

The Global Spine Degenerative Disk Disease Treatment Market has significant potential in emerging regions where healthcare infrastructure improves rapidly. It can tap into markets with rising healthcare expenditure and supportive government initiatives. Partnerships with local providers enable tailored offerings for patient populations. Expansion in Asia-Pacific and Latin America offers access to large patient pools and lower procedural cost environments. Manufacturers benefit from joint ventures that navigate regulatory requirements efficiently. Strategic investments in training and education build provider confidence and drive adoption.

Adoption of AI-Driven Diagnostics and Personalized Treatment Protocols

Integration of artificial intelligence and machine learning into diagnostic and treatment planning workflows offers new revenue streams. The Global Spine Degenerative Disk Disease Treatment Market can use AI-driven tools to enhance surgical precision and predict postoperative outcomes. It supports development of personalized treatment protocols based on patient-specific data. Collaboration with technology firms accelerates innovation in smart implants and remote monitoring devices. These solutions reduce complication rates and shorten hospital stays. Companies that pursue digital health platforms and data analytics gain competitive advantages.

Market Segmentation Analysis

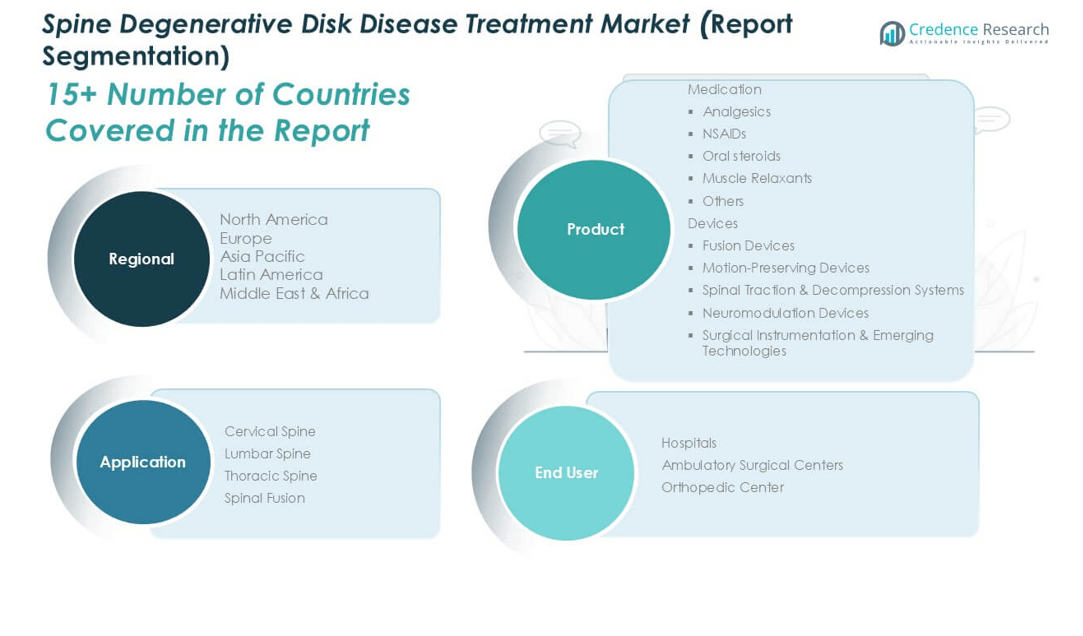

By Product

The Global Spine Degenerative Disk Disease Treatment Market comprises two primary product categories: medications and devices. Medications include analgesics, NSAIDs, oral steroids, muscle relaxants, and other supportive drugs that manage pain and inflammation in early-stage or non-surgical cases. Devices dominate revenue generation, driven by advanced solutions like fusion devices, motion-preserving implants, spinal traction and decompression systems, neuromodulation technologies, and surgical instrumentation. Fusion devices remain the standard in surgical interventions, while motion-preserving devices are gaining popularity due to their ability to maintain spinal flexibility. Neuromodulation and decompression systems are expanding within non-invasive therapeutic frameworks. Surgical instrumentation and emerging technologies support the growing demand for precision-driven, minimally invasive procedures.

- For instance, a 2024 industry survey reported that more than 1,200,000 spinal fusion surgeries were performed globally, with over 2,500,000 spinal implants and devices supplied to hospitals and surgical centers, highlighting the dominance of device-based interventions in the market.

By Application

Application-wise, the market segments into cervical, lumbar, thoracic spine treatment, and spinal fusion procedures. Lumbar spine disorders hold the largest share due to high incidence rates and the weight-bearing nature of this spinal region. Cervical spine treatments are also rising due to postural problems and occupational stress factors. Spinal fusion remains a dominant surgical application, widely adopted to treat severe degeneration. Thoracic spine treatments hold a smaller share but are vital in complex cases. The market continues to support specialized approaches for each region of the spine, ensuring tailored care for varying patient needs.

- For instance, global hospital data from 2024 indicated that more than 800,000 lumbar spine surgeries and over 400,000 cervical spine procedures were performed, underscoring the high clinical demand for region-specific and fusion-based treatments in degenerative disk disease management.

By End User

Hospitals account for the largest end-user share due to their comprehensive surgical capabilities, advanced infrastructure, and access to trained specialists. The Global Spine Degenerative Disk Disease Treatment Market also sees growing contributions from ambulatory surgical centers (ASCs), which offer cost-effective and minimally invasive procedures in outpatient settings. Orthopedic centers serve as specialized hubs, particularly in urban regions, focusing on targeted diagnosis, pain management, and elective surgeries. Each end-user segment contributes uniquely to expanding market accessibility and patient-centered care delivery.

Segments

Based on Product

- Medication

- Analgesics

- NSAIDs

- Oral steroids

- Muscle Relaxants

- Others

- Devices

- Fusion Devices

- Motion-Preserving Devices

- Spinal Traction & Decompression Systems

- Neuromodulation Devices

- Surgical Instrumentation & Emerging Technologies

Based on Application

- Cervical Spine

- Lumbar Spine

- Thoracic Spine

- Spinal Fusion

Based on End User

- Hospitals

- Ambulatory Surgical Centers

- Orthopedic Center

Based on Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Spine Degenerative Disk Disease Treatment Market

North America held the largest share of the global Spine Degenerative Disk Disease Treatment Market in 2024, valued at USD 9,009.85 million, and is expected to reach USD 12,272.87 million by 2032, growing at a CAGR of 4.0%. The region accounted for approximately 32.0% of the global market share in 2024. It leads due to its advanced healthcare infrastructure, high rate of spinal surgeries, and strong presence of key medical device manufacturers. The United States dominates the regional landscape with widespread adoption of minimally invasive surgical techniques and favorable insurance coverage. Canada follows with significant investments in orthopedic care and access to cutting-edge spinal technologies. The region continues to drive innovation and adoption of biologics and AI-powered surgical tools.

Europe Spine Degenerative Disk Disease Treatment Market

Europe captured around 24.8% of the global market in 2024, valued at USD 6,982.11 million, and is projected to grow to USD 9,897.47 million by 2032, at a CAGR of 4.5%. Countries like Germany, France, and the UK lead due to advanced clinical practices, growing geriatric populations, and expanding reimbursement schemes. The region benefits from strong regulatory frameworks that support the development of new spinal implants and regenerative therapies. Public awareness and accessibility to high-quality spine care have further fueled market penetration. Orthopedic centers across Western Europe are increasingly adopting motion-preserving and robotic-assisted procedures. The market maintains steady growth with increasing investments in outpatient surgical centers.

Asia Pacific Spine Degenerative Disk Disease Treatment Market

Asia Pacific is the fastest-growing regional segment, with a projected CAGR of 5.2% from 2025 to 2032. Valued at USD 6,477.19 million in 2024, it is expected to reach USD 9,723.28 million by 2032, contributing 23.0% to the global market share. China, Japan, and India are the primary growth engines, supported by expanding healthcare infrastructure, rising medical tourism, and increased awareness of spine health. The region experiences high demand for affordable, minimally invasive treatments and spinal rehabilitation services. Aging populations and lifestyle changes have raised the incidence of degenerative spinal disorders. Governments and private sectors are investing in advanced diagnostics and surgical facilities. Domestic manufacturers are also playing a growing role in supplying cost-effective treatment options.

Latin America Spine Degenerative Disk Disease Treatment Market

The Latin America market stood at USD 2,714.37 million in 2024 and is forecast to reach USD 3,563.09 million by 2032, growing at a CAGR of 3.5%, holding a 9.6% share in 2024. Brazil and Mexico dominate the regional market due to improving healthcare systems and increasing investments in specialized orthopedic care. Urbanization and changing work environments are contributing to higher diagnosis rates of spine-related disorders. Hospitals are expanding capabilities in spinal fusion and rehabilitation services. However, uneven access to advanced care in rural areas limits broader adoption. The region shows gradual uptake of new treatment modalities supported by public-private healthcare partnerships.

Middle East Spine Degenerative Disk Disease Treatment Market

In the Middle East, the market was valued at USD 1,753.57 million in 2024 and is projected to reach USD 2,414.98 million by 2032, registering a CAGR of 4.1%. It accounted for approximately 6.2% of the global market share in 2024. Countries like Saudi Arabia and the UAE lead with substantial investments in healthcare modernization and specialist training programs. The rise of medical tourism and expanding hospital networks fuel market activity. High-income populations and increasing spinal injury cases support procedural growth. Governments are partnering with global medical device companies to introduce cutting-edge technologies. The market remains on a stable growth path supported by policy-driven healthcare reforms.

Africa Spine Degenerative Disk Disease Treatment Market

Africa held the smallest market share of around 4.3% in 2024, valued at USD 1,203.62 million, and is expected to grow to USD 1,718.20 million by 2032, with a CAGR of 4.6%. South Africa leads in surgical infrastructure and specialist availability, while other countries are gradually developing orthopedic capabilities. Awareness campaigns and outreach programs are improving diagnosis and early treatment. Access to cost-effective treatments and essential medications remains a challenge across rural areas. The region sees growing interest from international medical device firms targeting affordable and scalable solutions. It offers long-term growth opportunities as infrastructure and skilled personnel continue to expand

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key players

- Medtronic

- Johnson and Johnson Services, Inc.

- Stryker

- Zimmer Biomet

- Teva Pharmaceutical Industries

- Endo Pharmaceuticals

- Mallinckrodt Pharmaceuticals

- Pfizer

- Anika Therapeutics

- Mesoblast Ltd

Competitive Analysis

The global Spine Degenerative Disk Disease Treatment Market features a competitive landscape marked by technological innovation, strategic collaborations, and a focus on advanced minimally invasive solutions. Leading players such as Medtronic, Johnson & Johnson Services, Inc., and Stryker dominate with extensive product portfolios and global distribution networks. These companies invest heavily in R\&D to enhance surgical precision, device performance, and regenerative therapies. Pharmaceutical firms like Teva, Pfizer, and Endo focus on analgesics, anti-inflammatory drugs, and muscle relaxants to support non-surgical treatments. Emerging players such as Anika Therapeutics and Mesoblast Ltd contribute with biologic and regenerative innovations. The market rewards firms with strong clinical data, global regulatory approvals, and efficient supply chains. It continues to evolve with a focus on personalized treatment, robotic-assisted surgery, and AI-driven planning tools. Competitive differentiation depends on innovation speed, pricing strategies, and the ability to serve a broad patient base across diverse healthcare settings.

Recent Developments

- At the AAOS 2025 conference in March, J&J MedTech presented the VELYS™ Spine system, alongside new implants and data-driven technologies, emphasizing their commitment to innovation in spine surgery. The VELYS™ Robotic-Assisted Solution, which has seen over 100,000 total knee replacement procedures, was also highlighted as a key innovation for enhancing surgical precision and streamlining workflows in knee surgery.

Market Concentration and Characteristics

The global Spine Degenerative Disk Disease Treatment Market exhibits moderate to high market concentration, with a few dominant players such as Medtronic, Stryker, and Johnson & Johnson controlling a significant share. It features a blend of multinational medical device companies and specialized pharmaceutical firms offering complementary treatment solutions. The market is characterized by continuous innovation, strong regulatory oversight, and growing demand for minimally invasive procedures and biologic therapies. It benefits from advancements in robotics, imaging technologies, and AI-driven diagnostics. Barriers to entry remain high due to capital-intensive R&D, strict approval processes, and theneed for specialized clinical expertise. Strategic partnerships, product differentiation, and global expansion define competitive positioning.

Report Coverage

The research report offers an in-depth analysis based on Product, Application, End User and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will see growing adoption of minimally invasive spine surgeries, driven by patient preference for quicker recovery and lower complication risks.

- AI-enabled planning tools and robotic-assisted systems will improve surgical accuracy, reduce errors, and support complex spinal procedures globally.

- Pharmaceutical and biotech firms will invest in stem cell therapies and biologics aimed at restoring spinal disc health and slowing disease progression.

- The shift from inpatient to outpatient settings will expand, supported by advancements in surgical techniques and reimbursement policy changes.

- Smart spinal implants integrated with sensors will enable post-surgical performance tracking, enhancing patient outcomes and long-term care management.

- Rapid healthcare infrastructure development in Asia Pacific, Latin America, and Africa will open new avenues for treatment expansion and market entry.

- Leading companies will pursue mergers, acquisitions, and joint ventures to expand their product portfolios and accelerate market reach.

- Governments and health organizations will drive spine health awareness campaigns, leading to early diagnosis and timely intervention.

- The market will embrace personalized care, using genetic data and imaging insights to tailor treatments for individual spinal conditions.

- Regulatory bodies will tighten safety standards while supporting faster approval of innovative devices and biologics through streamlined processes.