Market Overview:

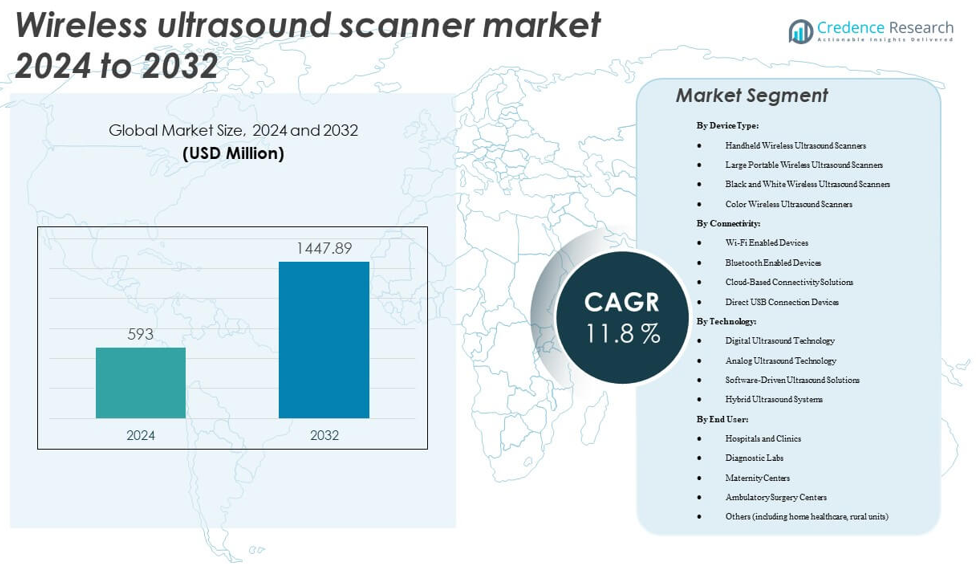

The Wireless ultrasound scanner market is projected to grow from USD 593 million in 2024 to an estimated USD 1,447.89 million by 2032, with a compound annual growth rate (CAGR) of 11.8% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Wireless ultrasound scanner market Size 2024 |

USD 593 million |

| Wireless ultrasound scanner market, CAGR |

11.8% |

| Wireless ultrasound scanner market Size 2032 |

USD 1,447.89 million |

The growth of the wireless ultrasound scanner market is driven by increasing demand for portable, real-time diagnostic tools that can be used in a variety of healthcare settings. Wireless ultrasound scanners enable healthcare providers to deliver more efficient and accessible care, especially in remote or rural areas. Technological advancements in imaging quality, mobility, and connectivity further enhance their adoption. These devices are becoming essential in point-of-care diagnostics, reducing equipment costs while improving patient care and outcomes.

Regionally, North America leads the Wireless ultrasound scanner market due to its advanced healthcare infrastructure and early adoption of digital medical technologies. Europe follows closely, with countries like the UK and Germany investing in telemedicine and home healthcare solutions. Emerging markets in Asia Pacific, such as China and India, are seeing rapid growth due to rising healthcare access, expanding hospital infrastructure, and increasing awareness of portable diagnostic solutions. Latin America and the Middle East also offer opportunities for growth as healthcare systems continue to modernize and seek cost-effective solutions.

Market Insights:

- The Wireless ultrasound scanner market is projected to grow from USD 593 million in 2024 to USD 1,447.89 million by 2032, with a CAGR of 11.8%.

- Rising demand for portable, real-time diagnostic tools is driving the market, especially in remote and rural healthcare settings.

- Technological advancements in imaging quality, mobility, and cloud-based connectivity solutions are enhancing product appeal and market adoption.

- Cost-effectiveness of wireless ultrasound scanners makes them increasingly popular in point-of-care diagnostics and home healthcare.

- The market faces challenges related to regulatory compliance and data security, especially with cloud-based storage solutions.

- North America holds the largest market share due to its advanced healthcare infrastructure and high adoption rates of digital technologies.

- The Asia Pacific region is witnessing rapid growth, driven by expanding healthcare access and infrastructure improvements in countries like China and India.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Demand for Portable Medical Devices

The growing preference for portable, real-time diagnostic tools fuels the demand for wireless ultrasound scanners. These devices offer flexibility, enabling medical professionals to perform diagnostic imaging in remote or underserved locations. Their ability to provide quick results at the point of care is a significant factor driving adoption, particularly in rural areas and emergency settings. Wireless ultrasound scanners help healthcare providers streamline workflows and reduce the need for centralized imaging facilities, thus expanding their use across various clinical environments.

- For instance, the University of Rochester Medical Center (URMC) deployed 862 Butterfly Network’s point-of-care ultrasound devices across 64 departments by September 2024, leading to a 116% increase in ultrasound charge capture and enabling nearly 50,000 scanning sessions, generating over 175,000 images and over 15,000 finalized reports in less than three years.

Technological Advancements in Imaging Quality

Recent innovations in wireless ultrasound technology have significantly improved imaging quality, making these devices more reliable and effective for diagnosing a wide range of conditions. Enhanced resolution, advanced Doppler imaging capabilities, and better connectivity with cloud-based systems are some factors that have increased their market appeal. The improved accuracy and speed of wireless ultrasound scanners make them valuable diagnostic tools in critical care, emergency medicine, and general healthcare applications, further accelerating their adoption.

- For example, Clarius Mobile Health introduced the PAL HD3 in 2023 the world’s first handheld dual-array scanner for whole-body ultrasound offering a frequency range of 1 to 15 MHz and imaging depth up to 40 cm, with more than 25,000 AI-powered handheld ultrasound systems delivered to clinicians in 58 countries as of early 2024.

Cost-Effectiveness and Efficiency

The wireless ultrasound scanner market benefits from the increasing need for cost-effective healthcare solutions. These devices reduce the costs associated with traditional imaging systems, such as installation, maintenance, and infrastructure. Their portability and ease of use also enable healthcare providers to offer more affordable services. Hospitals, clinics, and mobile health providers are increasingly turning to wireless ultrasound scanners to optimize diagnostic efficiency while managing costs effectively.

Increased Adoption in Home Healthcare and Point-of-Care Settings

The growth of home healthcare services and point-of-care (POC) testing drives demand for wireless ultrasound scanners. Patients requiring regular monitoring benefit from the convenience and flexibility these devices offer, enabling healthcare professionals to conduct assessments at the patient’s location. Wireless ultrasound systems can be easily integrated into home health monitoring programs, making it easier to track chronic conditions like cardiovascular diseases and pregnancy. This growing trend of decentralized care presents a significant market opportunity for these portable diagnostic tools.

Market Trends:

Integration with Mobile and Cloud Technologies

The integration of wireless ultrasound scanners with mobile devices and cloud-based platforms has become a notable trend. These devices allow healthcare providers to remotely access and analyze diagnostic images, improving collaboration among medical teams. The ability to store and share patient data securely via the cloud enhances workflow efficiency and supports telemedicine applications. This trend is shaping the future of healthcare by facilitating more comprehensive and accessible care, especially in remote or rural locations where access to specialized medical expertise is limited.

Miniaturization and Enhanced Portability

Miniaturization is a key trend in the wireless ultrasound scanner market, with manufacturers continuously working to reduce the size and weight of these devices. This trend makes the scanners more portable and easier to handle in various healthcare settings. As wireless ultrasound scanners become more compact, they are increasingly being used in both clinical and non-clinical environments, such as field hospitals, ambulances, and home healthcare. The shift toward more compact and lightweight designs contributes to the broader adoption of these devices.

- For example, the Clarius HD3 handheld ultrasound scanner (model L7 HD3) weighs 288 grams and measures 147 × 76 × 32 mm, based on the official technical product sheet released by Clarius. This device is compatible with both Apple and Android devices and offers a wireless, pocket-size form factor that supports high portability in field, EMS, and clinical settings.

Increased Use in Emergency Medical Services (EMS)

The adoption of wireless ultrasound scanners in emergency medical services is on the rise. These devices allow paramedics and emergency responders to perform real-time diagnostics in the field, providing crucial information before patients arrive at the hospital. Wireless ultrasound technology enhances the speed and accuracy of trauma assessments, allowing healthcare providers to make immediate decisions about patient care. As EMS teams continue to seek efficient and effective diagnostic tools, wireless ultrasound scanners are becoming a standard part of emergency response kits.

- For example, Philips Lumify is a handheld ultrasound solution that connects to smart devices, allowing healthcare providers to use it for ultrasound-guided procedures. It has been utilized in ambulances and pre-hospital environments, offering a portable, effective diagnostic tool in emergency medical settings.

Focus on User-Friendly Interfaces and AI Integration

There is an increasing focus on developing wireless ultrasound scanners with intuitive interfaces that are easy for healthcare providers to use. Simplified touch-screen controls, automated image analysis, and artificial intelligence (AI)-driven decision support systems are becoming common features. AI integration helps improve diagnostic accuracy by automatically detecting abnormalities and providing real-time suggestions to clinicians. These advancements make wireless ultrasound scanners more accessible, even to healthcare providers with minimal ultrasound experience, while also improving the overall quality of care.

Market Challenges Analysis:

Regulatory and Compliance Issues

The wireless ultrasound scanner market faces challenges related to regulatory approvals and compliance with medical device standards. Manufacturers must navigate complex regulatory frameworks to ensure their products meet safety and performance standards. This can involve rigorous testing and certification processes, which can delay product launches and increase development costs. Moreover, the market is subject to varying regulations across different regions, making it difficult for companies to maintain compliance and scale globally. The need for standardization and more efficient regulatory processes remains a key challenge.

Data Security and Privacy Concerns

As wireless ultrasound scanners become more integrated with cloud-based systems, data security and patient privacy concerns are emerging as significant challenges. Storing and transmitting sensitive medical data over the internet can expose healthcare providers to cybersecurity risks. Ensuring that these devices meet data protection regulations, such as HIPAA in the U.S. and GDPR in Europe, is crucial for maintaining trust and compliance. Addressing these concerns requires manufacturers to invest in robust encryption methods and secure cloud platforms to protect patient data from unauthorized access and breaches.

Market Opportunities:

Expanding in Emerging Markets

There is a significant growth opportunity for wireless ultrasound scanners in emerging markets, particularly in Asia-Pacific and Africa. As healthcare infrastructure continues to improve in these regions, the demand for cost-effective, portable diagnostic tools is rising. Wireless ultrasound scanners offer an affordable solution to healthcare providers in areas with limited access to traditional imaging equipment. The growing adoption of mobile health initiatives and the increasing availability of wireless connectivity further enhance the potential for market expansion in these regions.

Growth in Home Healthcare and Telemedicine

The rapid growth of home healthcare and telemedicine presents a promising opportunity for the wireless ultrasound scanner market. As more patients prefer receiving care at home, the demand for portable and easy-to-use diagnostic devices increases. Wireless ultrasound scanners enable healthcare providers to conduct remote consultations, allowing them to assess patient conditions and make timely decisions. This trend is expected to continue as healthcare systems shift towards more patient-centric, decentralized models of care, creating new opportunities for the market.

Market Segmentation Analysis:

By Device Type:

The Wireless ultrasound scanner market is segmented into four main device types: handheld, large portable, black and white, and color wireless ultrasound scanners. Handheld wireless ultrasound scanners are compact, lightweight, and ideal for point-of-care applications, offering flexibility in various healthcare settings. Large portable wireless ultrasound scanners combine advanced imaging capabilities with portability, suitable for hospitals and diagnostic centers. Black and white wireless ultrasound scanners provide basic imaging, making them an affordable option for routine diagnostics. Color wireless ultrasound scanners offer advanced imaging features, including color Doppler, and are widely used in fields like obstetrics and cardiology, where high-quality images are crucial for accurate diagnostics.

- For instance, the Butterfly iQ+ from Butterfly Network is a handheld, single-probe, whole-body ultrasound system utilizing patented Ultrasound-on-Chip technology and offering 20+ presets across clinical applications. It is FDA-cleared, CE-marked, and has facilitated space health research in partnership with NASA and the Translational Research Institute for Space Health.

By Connectivity:

The connectivity segment of the Wireless ultrasound scanner market includes Wi-Fi enabled devices, Bluetooth enabled devices, cloud-based connectivity solutions, and direct USB connection devices. Wi-Fi-enabled devices facilitate seamless real-time image sharing and remote consultations, improving workflow efficiency. Bluetooth-enabled devices offer secure and energy-efficient connections for quick image transfer to nearby devices. Cloud-based connectivity solutions allow for secure data storage, retrieval, and sharing across multiple devices, supporting telemedicine and remote diagnostics. Direct USB connection devices provide simple, secure connections for immediate data transfer without the need for internet access, catering to environments with limited connectivity.

By Technology:

The technology segment of the Wireless ultrasound scanner market includes digital ultrasound technology, analog ultrasound technology, software-driven ultrasound solutions, and hybrid ultrasound systems. Digital ultrasound technology provides high-quality imaging and enhanced resolution, making it the most common choice in modern wireless ultrasound systems. Analog ultrasound technology, though less common today, still plays a role in basic, cost-effective ultrasound solutions. Software-driven ultrasound solutions leverage AI and advanced algorithms to improve image quality and diagnostic accuracy, while hybrid ultrasound systems combine multiple technologies to offer versatile imaging capabilities, catering to complex diagnostic needs.

- For example, Samsung Medison continues to offer legacy analog ultrasound models still used in foundational diagnostic workflows in some rural care settings. Their historical 128-channel architecture is described in product manuals, though prevalence decreases as facilities update equipment.

By End User:

The end-user segment of the Wireless ultrasound scanner market includes hospitals and clinics, diagnostic labs, maternity centers, ambulatory surgery centers, and others, such as home healthcare and rural units. Hospitals and clinics are major consumers of wireless ultrasound scanners due to their need for portable, efficient diagnostic tools for a wide range of patient conditions. Diagnostic labs and maternity centers use these devices for routine and specialized testing, while ambulatory surgery centers benefit from the portability and ease of use in outpatient procedures. The growing demand for home healthcare and rural diagnostics is expanding the market as these devices offer cost-effective, reliable solutions for remote care and patient monitoring.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Segmentation:

By Device Type:

- Handheld Wireless Ultrasound Scanners

- Large Portable Wireless Ultrasound Scanners

- Black and White Wireless Ultrasound Scanners

- Color Wireless Ultrasound Scanners

By Connectivity:

- Wi-Fi Enabled Devices

- Bluetooth Enabled Devices

- Cloud-Based Connectivity Solutions

- Direct USB Connection Devices

By Technology:

- Digital Ultrasound Technology

- Analog Ultrasound Technology

- Software-Driven Ultrasound Solutions

- Hybrid Ultrasound Systems

By End User:

- Hospitals and Clinics

- Diagnostic Labs

- Maternity Centers

- Ambulatory Surgery Centers

- Others (including home healthcare, rural units)

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Dominance and Growth

North America holds a leading position in the Wireless ultrasound scanner market, capturing approximately 40% of global revenue. It benefits from advanced healthcare infrastructure, strong reimbursement frameworks, and high adoption of mobile imaging solutions. Leading players conduct substantial R&D in this region, which accelerates product innovation and deployment. Hospitals and outpatient settings drive demand for wireless systems in emergency and point‑of‑care settings. Market growth remains high due to increasing chronic disease prevalence and demand for quick diagnostics. Manufacturers expand partnerships with major health networks, strengthening market penetration and vendor positioning.

Europe Steady Adoption and Market Share

Europe contributes about 20% of the global wireless ultrasound scanner market share. The region sees steady adoption driven by aging populations, high public healthcare spending, and strong digital health initiatives. Key countries such as the UK, Germany and France invest in portable imaging upgrades across hospitals and clinics. The regulatory environment supports wireless diagnostics, although reimbursement varies across countries. Clinics and ambulatory care centers expand the use of wireless scanners to reduce costs and improve patient throughput. Growth remains moderate but sustainable due to stable healthcare budgets and focus on non‑invasive diagnostics.

Asia Pacific and Emerging Markets Acceleration

Asia Pacific commands around 30% of the market share in the wireless ultrasound scanner space, while Latin America and Middle East & Africa together account for near 10%. APAC leads the growth frontier thanks to rising healthcare access, increasing hospital infrastructure, and telemedicine expansion in countries such as China and India. In Latin America and MEA, growth remains smaller but promising because rural diagnostics and portable imaging gain attention. Manufacturers target these emerging regions with cost‑effective wireless systems to capture latent demand. Market entry strategies often feature local partnerships, training programs and tailored solutions for point‑of‑care settings.

Key Player Analysis:

Competitive Analysis:

The competitive landscape of the wireless ultrasound scanner market features several major players who vie for technological leadership and market share. Companies such as GE Healthcare, Philips Healthcare and Siemens Healthineers lead by delivering high‑end systems, strong global sales networks and extensive R&D capabilities. Emerging competitors like Clarius Mobile Health and Butterfly Network focus on portable, app‑enabled wireless scanners and offer innovative business models. The market remains fragmented with room for niche vendors targeting rural diagnostics, veterinary applications and home healthcare. Manufacturers compete on device portability, image quality, connectivity features and cost‑effectiveness. Strategic alliances and acquisitions help firms expand geographic reach and product portfolios. It remains critical for vendors to manage regulatory compliance, interoperability and service networks to maintain competitive advantage.

Recent Developments:

- In September 2025, GE HealthCare introduced its Voluson Performance series of ultrasound systems, which incorporates wireless Vscan Air probes and enhanced AI-driven imaging features. The new systems are designed for improved workflow and integration in point-of-care diagnostics, highlighting advancements in wireless ultrasound scanner technology for clinical settings.

- In January 2025, Clarius Mobile Health unveiled new enterprise software and AI-powered capabilities for its wireless ultrasound scanners, including features for workflow, billing management, and advanced anatomical overlays for learning and practice.

- In April 2024, GE HealthCare introduced the Vscan Air SL wireless ultrasound scanner enhanced with Caption AI, advancing their solutions for cardiac imaging and early disease detection. This integration followed GE’s strategic acquisition of Caption Health in 2023, solidifying their leadership in AI-powered ultrasound technology.

Report Coverage:

The research report offers an in-depth analysis based on Device Type, Connectivity, Technology and End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The wireless ultrasound scanner market will see rapid growth driven by increasing demand for portable, real-time diagnostic tools.

- Technological advancements in image quality and AI-driven features will enhance diagnostic capabilities and accuracy.

- Expansion of telemedicine and remote care services will significantly boost market adoption across healthcare settings.

- Increased adoption in emergency medical services (EMS) will open new opportunities for wireless ultrasound devices.

- Regulatory support for mobile healthcare solutions will pave the way for greater acceptance of wireless ultrasound scanners.

- As healthcare systems in emerging markets modernize, the wireless ultrasound scanner market will see accelerated growth.

- Continued advancements in connectivity features, such as cloud integration and mobile app compatibility, will drive further adoption.

- The increasing need for cost-effective diagnostic tools in rural and remote areas will further expand the market.

- Growing investments in healthcare infrastructure, particularly in Asia-Pacific and Latin America, will contribute to market expansion.

- Integration with wearable medical devices and personalized healthcare applications will enhance the use of wireless ultrasound scanners.