Market Overview

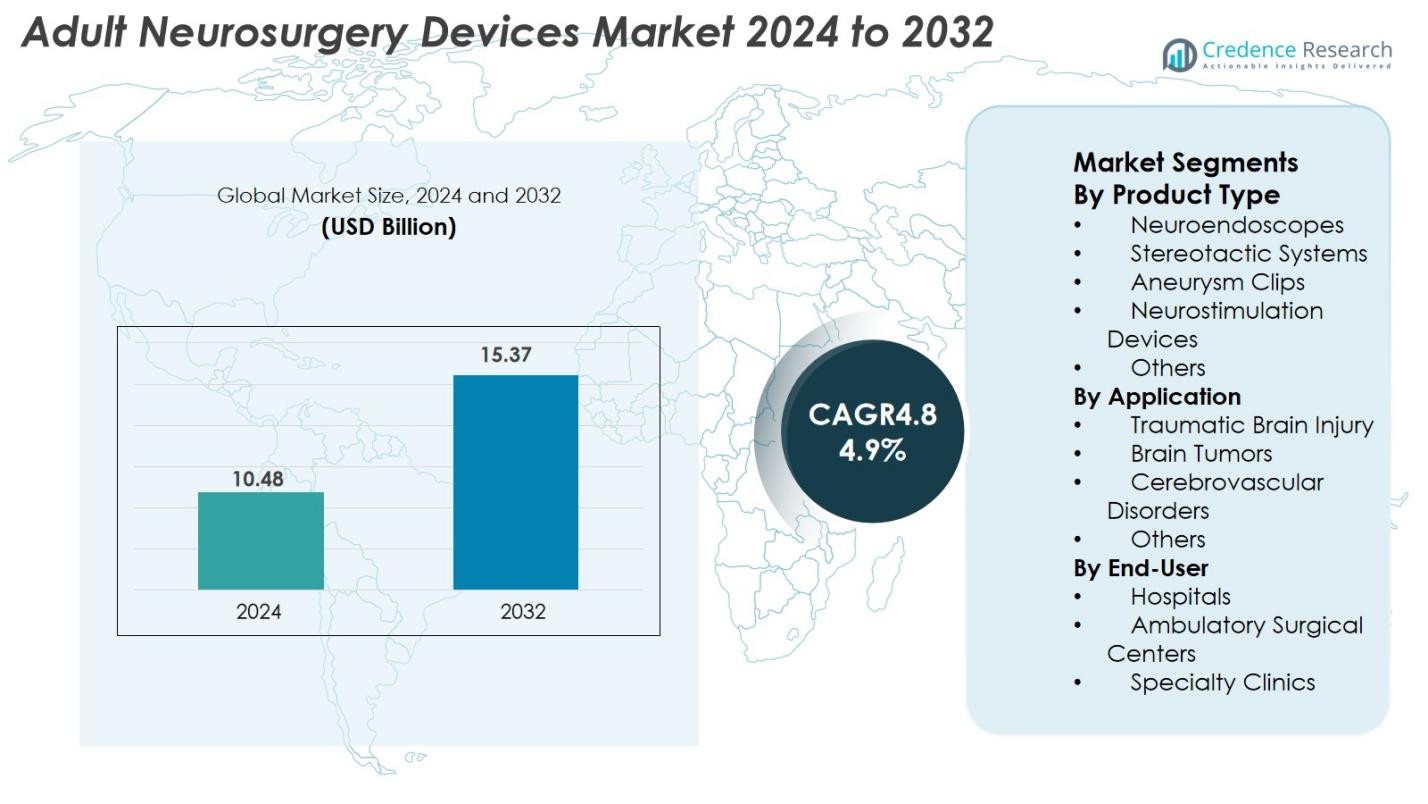

Adult Neurosurgery Devices Market size was valued at USD 10.48 Billion in 2024 and is anticipated to reach USD 15.37 Billion by 2032, growing at a CAGR of 4.9% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Adult Neurosurgery Devices Market Size 2024 |

USD 10.48 Billion |

| Adult Neurosurgery Devices Market, CAGR |

4.9% |

| Adult Neurosurgery Devices Market Size 2032 |

USD 15.37 Billion |

Adult Neurosurgery Devices Market is driven by leading manufacturers such as Medtronic, Stryker Corporation, Johnson & Johnson, Boston Scientific, B. Braun Melsungen AG, Abbott Laboratories, Zimmer Biomet, Smith & Nephew, Integra LifeSciences, and Terumo Corporation, each expanding portfolios with advanced neurostimulation, stereotactic, and minimally invasive devices. North America leads the market with 38.4% share in 2024 due to strong neurosurgical infrastructure and high adoption of innovative technologies, followed by Europe with 27.1% share supported by robust clinical expertise and regulatory frameworks. Asia Pacific, holding 23.6% share, emerges as the fastest-growing region driven by healthcare expansion and rising neurological disease prevalence.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- Adult Neurosurgery Devices Market reached USD 10.48 Billion in 2024 and will grow at a CAGR of 4.9% through 2032, reaching USD 15.37 billion.

- Market growth is driven by increasing neurological disorders, expanding aging population, and higher adoption of minimally invasive neurosurgery technologies across hospitals and specialty centers.

- Advancements in neurostimulation, stereotactic systems, and AI-integrated surgical platforms shape key trends, with neurostimulation devices holding the largest product share at 34.6% in 2024.

- Leading players such as Medtronic, Stryker, Johnson & Johnson, Boston Scientific, Abbott, and Zimmer Biomet strengthen their positions through product innovation, clinical partnerships, and expansion in emerging markets.

- North America leads with 38.4% share, followed by Europe at 27.1%, while Asia Pacific holds 23.6% and remains the fastest-growing region due to healthcare modernization and increasing access to neurosurgical care.

Market Segmentation Analysis

By Product Type

The Adult Neurosurgery Devices Market by product type is led by neurostimulation devices, accounting for 34.6% share in 2024 due to their expanding use in managing chronic pain, movement disorders, and epilepsy. Increasing adoption of minimally invasive neuromodulation therapies and advancements such as closed-loop stimulation systems strengthen their dominance. Neuroendoscopes and stereotactic systems gain traction with rising demand for precision-guided interventions, while aneurysm clips remain essential in cerebrovascular surgeries. The segment grows as healthcare providers prioritize accuracy, safety, and reduced postoperative complications through technology-driven neurosurgical tools.

- For instance, ElectroCore’s non-invasive vagus nerve stimulation devices like gammaCore are FDA-cleared for migraine and cluster headache treatment, expanding options for neurostimulation therapies.

By Application

Traumatic brain injury (TBI) dominated the application segment with 39.2% share in 2024, driven by the high global incidence of accidents, sports injuries, and falls requiring advanced neurosurgical interventions. Increasing adoption of neuroendoscopic and stereotactic technologies for rapid assessment and minimally invasive management further reinforces this segment’s leadership. Brain tumor surgeries also contribute significantly due to rising diagnostic rates and improved survival outcomes supported by precision devices. Growing use of neuromodulation for cerebrovascular disorders and neurological rehabilitation expands the application scope across diverse clinical needs.

- For instance, the use of neuroendoscopic technology by companies like Karl Storz enables minimally invasive procedures that allow rapid assessment and treatment, reducing patient recovery time.

By End-User

Hospitals held the largest end-user share at 56.8% in 2024, driven by the presence of advanced neurosurgical infrastructure, multidisciplinary expertise, and higher patient inflow for complex neurological procedures. Investment in hybrid operating rooms, neuronavigation systems, and robotic assistance strengthens their dominance. Ambulatory surgical centers show rapid growth as minimally invasive neurosurgery enables shorter recovery and outpatient interventions. Specialty clinics increasingly adopt neurostimulation and diagnostic support tools for chronic neurological conditions, expanding care accessibility and supporting market penetration across advanced and developing healthcare settings.

Key Growth Drivers

Rising Burden of Neurological Disorders and Aging Population

The Adult Neurosurgery Devices Market is significantly driven by the escalating prevalence of neurological disorders, including brain tumors, cerebrovascular diseases, epilepsy, Parkinson’s disease, and traumatic brain injuries. An aging global population further accelerates device adoption, as older adults face higher risks of degenerative and vascular neurological conditions requiring surgical intervention. Increasing diagnostic accuracy through advanced imaging modalities leads to earlier detection and greater surgical volume. Moreover, higher survival rates for chronic neurological diseases expand the need for long-term neuromodulation and reconstructive procedures. Healthcare systems worldwide are investing in modern neurosurgical infrastructure, including robotic-assisted systems, enhanced neuronavigation platforms, and minimally invasive surgical tools to manage rising caseloads. These demographic and epidemiological trends collectively reinforce the sustained demand for advanced neurosurgery devices.

- For instance, Medtronic’s Deep Brain Stimulation system has been utilized in over 200,000 patients worldwide to treat Parkinson’s disease and essential tremor, demonstrating growing clinical adoption of neuromodulation devices.

Growing Adoption of Minimally Invasive Neurosurgical Procedures

The shift toward minimally invasive neurosurgery is one of the strongest growth drivers for the market, as both clinicians and patients prioritize reduced surgical trauma, faster recovery, and lower complication risks. Technologies such as neuroendoscopy, stereotactic systems, robotic neurosurgery, and laser ablation enable precise interventions with smaller incisions and enhanced accuracy. Rising awareness of the benefits of minimally invasive neurosurgery has increased procedure volumes across hospitals and ambulatory surgical centers. Manufacturers are integrating real-time imaging, augmented reality, and AI-assisted planning into device platforms, improving surgical precision and patient outcomes. Additionally, minimally invasive approaches lower hospital stays and procedural costs, making them increasingly preferred in cost-sensitive healthcare environments. These advantages collectively strengthen market growth and foster continuous technological expansion.

- For instance, the Neuroendoscopy systems by Karl Storz allow surgeons to perform brain surgeries through small openings, significantly reducing patient recovery time.

Technological Advancements in Neurostimulation and Image-Guided Systems

Rapid technological innovation in neuromodulation, neuronavigation, and image-guided surgery is transforming neurosurgical capabilities, fueling strong market growth. Next-generation neurostimulation devices now feature closed-loop feedback, improved battery life, wireless programmability, and targeted stimulation for conditions such as chronic pain, epilepsy, and movement disorders. Advanced intraoperative imaging, including 3D navigation, MRI-guided systems, and augmented reality overlays, enhances surgical accuracy and reduces intraoperative errors. Robotics-assisted neurosurgery is gaining traction by offering high stability and precision in delicate procedures. Continuous R&D investments by manufacturers and increasing regulatory approvals for innovative devices support faster adoption in clinical practice. These advancements elevate procedural safety, expand treatment options, and strengthen the global demand for technologically advanced neurosurgery devices.

Key Trends & Opportunities

Integration of AI, Robotics, and Digital Neurosurgery Platforms

The Adult Neurosurgery Devices Market is witnessing a major shift toward digital neurosurgery, where AI-driven analytics, robotics, and data-integrated systems optimize surgical workflows and enhance precision. AI tools assist in preoperative planning, predictive analytics, and personalized treatment mapping, while robotic-assisted systems deliver exceptional accuracy during microsurgical tasks. Digital platforms enable surgeons to visualize anatomical structures with greater clarity through AR/VR-based simulation and intraoperative imaging. The rise of smart operating rooms equipped with sensor-based devices and automated workflow management creates significant opportunities for companies to innovate connected systems. This integration of digital technologies improves patient outcomes, reduces operational errors, and positions digital neurosurgery as a transformative growth frontier in the coming years.

- For instance, Philips’ AI-powered IntelliSpace platform aids in preoperative planning by analyzing imaging data to personalize surgical approaches.

Expansion of Neurosurgical Care in Emerging Markets

Emerging economies present substantial opportunities as healthcare infrastructure modernizes and access to advanced neurosurgical treatments increases. Countries in Asia Pacific, Latin America, and the Middle East are investing heavily in tertiary hospitals, specialized neurology centers, and trauma care facilities. Rising insurance penetration, government funding for neurological healthcare, and greater private-sector investment accelerate device uptake. Medical tourism further boosts demand as patients seek cost-effective neurosurgical procedures in technologically progressing nations. Manufacturers are expanding distribution networks and offering affordable device models suited for developing markets. Training collaborations with local healthcare providers enhance clinical capabilities, positioning emerging regions as key contributors to future market expansion.

- For instance, Thailand’s growing medical tourism sector attracts patients from neighboring countries seeking affordable neurosurgical care, increasing device demand in the region.

Key Challenges

High Cost of Neurosurgery Devices and Limited Affordability

The high capital cost of advanced neurosurgery devices—including neuronavigation systems, robotic surgery platforms, and neuromodulation implants—remains a major challenge restricting widespread adoption. Budget constraints in public healthcare facilities limit procurement of high-end systems, creating significant disparities in access to modern neurosurgical care. Additionally, recurring expenses related to device maintenance, consumables, and software upgrades increase overall treatment costs. Limited reimbursement coverage for neuromodulation procedures further impacts patient affordability. These financial constraints slow market penetration, particularly in developing regions, highlighting the need for cost-effective solutions and improved reimbursement frameworks to expand access to advanced neurosurgical technologies.

Shortage of Skilled Neurosurgeons and Training Limitations

The global shortage of trained neurosurgeons is a critical challenge affecting the Adult Neurosurgery Devices Market. Neurosurgery requires exceptional precision and extensive training, and many countries—especially in low- and middle-income regions—lack sufficient specialists to meet rising procedural demand. Adoption of complex technologies such as stereotactic platforms, robotic-assisted systems, and neurostimulation implants requires specialized skill sets, yet standardized training programs remain limited. High workload, long learning curves, and inadequate exposure to advanced tools hinder broader uptake. Addressing this issue demands expanded fellowship programs, simulation-based training, and stronger partnerships between device manufacturers and healthcare institutions to improve expertise and scale neurosurgical capabilities globally.

Regional Analysis

North America

North America dominated the Adult Neurosurgery Devices Market with 38.4% share in 2024, driven by advanced healthcare infrastructure, high adoption of minimally invasive neurosurgical technologies, and strong presence of leading manufacturers. The region benefits from robust reimbursement frameworks, high diagnostic rates of neurological disorders, and continuous integration of AI- and robotics-enabled surgical systems. Rising prevalence of traumatic brain injuries and neurodegenerative diseases further fuels procedure demand. Hospitals and specialty centers in the U.S. and Canada increasingly invest in neuronavigation, neurostimulation, and endoscopic platforms, reinforcing North America’s position as the primary hub for neurosurgical innovation and clinical adoption.

Europe

Europe held 27.1% share in 2024, supported by well-established neurosurgical infrastructure, growing geriatric population, and rising burden of cerebrovascular and neurodegenerative diseases. Germany, France, and the U.K. lead regional adoption due to strong clinical expertise and significant investments in image-guided and minimally invasive neurosurgery. Increasing uptake of neurostimulation therapies for epilepsy and movement disorders also strengthens market growth. Public healthcare spending and favorable medical device regulations accelerate the entry of advanced robotic and stereotactic systems. Expanding training programs in neurosurgical technologies further position Europe as a key contributor to global market expansion.

Asia Pacific

Asia Pacific accounted for 23.6% share in 2024, emerging as the fastest-growing region due to rapid healthcare modernization, increasing neurological disease prevalence, and expanding access to advanced neurosurgical procedures. China, India, Japan, and South Korea experience rising demand for neurostimulation, endoscopy, and stereotactic systems as hospitals upgrade surgical capabilities. Government investments in tertiary care facilities and trauma centers support high adoption rates. Increasing medical tourism, particularly in Southeast Asia, promotes market growth through cost-effective neurosurgical care. Rising training initiatives and partnerships with global device manufacturers strengthen Asia Pacific’s long-term growth trajectory.

Latin America

Latin America captured 6.9% share in 2024, driven by improving neurosurgical capabilities in Brazil, Mexico, Argentina, and Chile. Growing investments in modern operating rooms, neuronavigation systems, and neuromodulation therapies contribute to increased device adoption. The region benefits from rising awareness of minimally invasive neurosurgery and expanding private healthcare infrastructure. However, economic disparities and limited reimbursement coverage create access gaps, slowing market penetration in lower-income areas. Collaborative training programs and expansion strategies by global device manufacturers continue to support regional growth, gradually increasing the availability of advanced neurosurgical solutions across Latin America.

Middle East & Africa

The Middle East & Africa region held 4.0% share in 2024, with growth supported by expanding neurology and neurosurgery centers in Saudi Arabia, the UAE, South Africa, and Egypt. Government-led healthcare modernization initiatives, including investment in advanced surgical technologies and specialized neurological institutes, boost adoption of neuromodulation, stereotactic, and endoscopic devices. Medical tourism in the Gulf region further strengthens demand. However, limited access to specialized surgeons and high device costs restrict widespread implementation across low-resource countries. Increasing partnerships, training programs, and technology transfer initiatives are expected to gradually improve neurosurgical capacity in the region.

Market Segmentations

By Product Type

- Neuroendoscopes

- Stereotactic Systems

- Aneurysm Clips

- Neurostimulation Devices

- Others

By Application

- Traumatic Brain Injury

- Brain Tumors

- Cerebrovascular Disorders

- Others

By End-User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The Adult Neurosurgery Devices Market features a strong lineup of global medical technology leaders focusing on innovation, portfolio expansion, and advanced neurosurgical solutions. Key players such as Medtronic, Stryker Corporation, Johnson & Johnson, Integra LifeSciences, B. Braun Melsungen AG, Boston Scientific Corporation, Abbott Laboratories, Zimmer Biomet, Smith & Nephew plc, and Terumo Corporation actively strengthen their market presence through product advancements, regulatory approvals, and strategic acquisitions. Companies increasingly prioritize minimally invasive neurosurgical technologies, including neurostimulation, stereotactic systems, neuronavigation platforms, and endoscopic devices. Investments in AI-enabled surgical planning, robotic-assisted neurosurgery, and connected operating room ecosystems further intensify competition. Additionally, firms are expanding in emerging markets through partnerships, training programs, and cost-effective product lines. This competitive environment drives continuous technological progress and broadens access to high-precision neurosurgery devices globally.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Abbott Laboratories

- Zimmer Biomet Holdings, Inc.

- Medtronic

- Terumo Corporation

- Smith & Nephew plc

- Integra LifeSciences

- B. Braun Melsungen AG

- Boston Scientific Corporation

- Johnson & Johnson

- Stryker Corporation

Recent Developments

- In September 2025, B. Braun SE acquired True Digital Surgery a company specializing in digital robotic-assisted 3D surgical microscopy.

- In August 2025, Rhovica Neuroimaging raised €2.5 million to develop “SoNav”, its bedside navigation system for extraventricular drainage (EVD) catheters for emergency neurosurgery.

- In March 2025, Brain Navi Biotechnology entered a strategic partnership with BenQ Medical Technology to introduce and commercialize the “NaoTrac” neurosurgical navigation robot in China.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will experience steady growth driven by rising neurological disease prevalence and expanding surgical volumes.

- Adoption of minimally invasive neurosurgery will increase as hospitals upgrade to advanced endoscopic and stereotactic systems.

- Neurostimulation devices will gain wider clinical acceptance for chronic pain, epilepsy, and movement disorder management.

- AI-assisted planning and intraoperative imaging will enhance precision and reduce surgical complications.

- Robotic-assisted neurosurgery will move toward broader integration across major healthcare institutions.

- Emerging markets will expand rapidly as neurosurgical infrastructure and specialist availability improve.

- Manufacturers will focus on developing cost-effective devices to address affordability barriers in low-resource regions.

- Training programs and simulation-based learning will strengthen neurosurgeon expertise and technology adoption.

- Partnerships between device makers and hospitals will accelerate innovation and procedural efficiency.

- Digital neurosurgery platforms and connected operating rooms will reshape long-term technology adoption and clinical workflows.