Battery Scrap Market Overview:

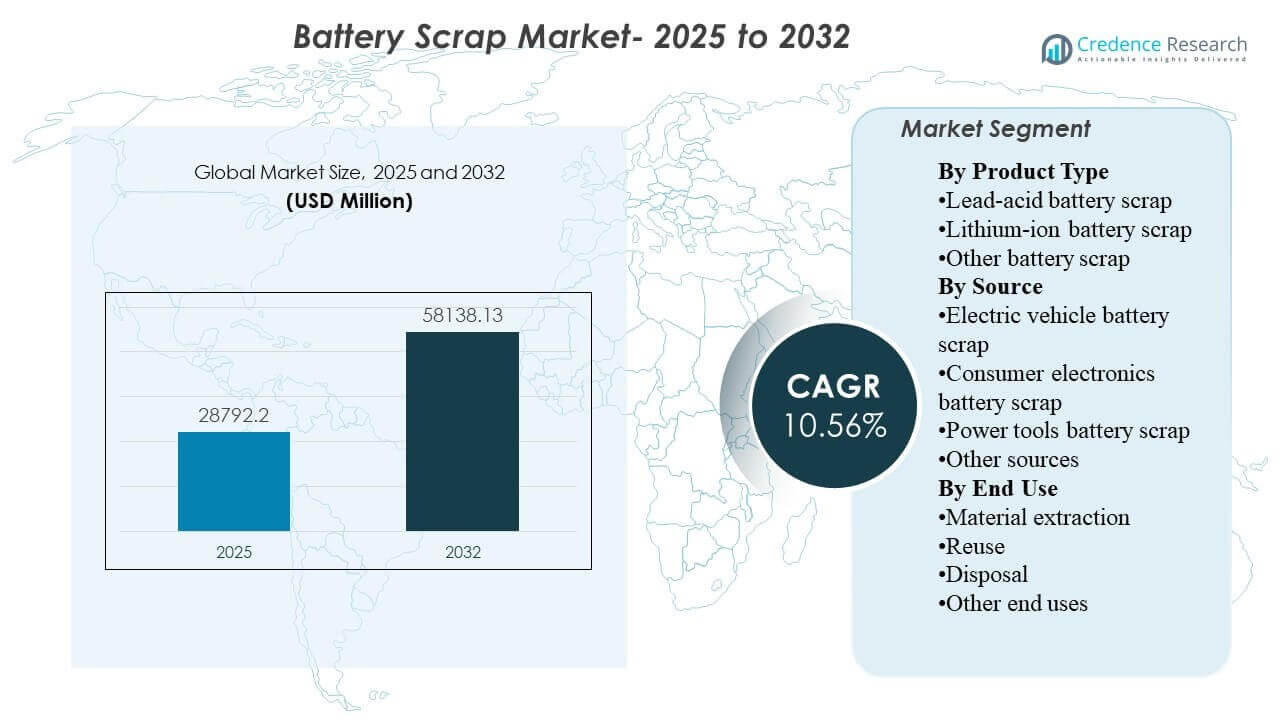

The global Battery Scrap Market size was estimated at USD 28792.2 million in 2025 and is expected to reach USD 58138.13 million by 2032, growing at a CAGR of 10.56% from 2025 to 2032. Expansion is being driven primarily by the rising volume of end-of-life batteries entering formal collection and recycling channels as electric mobility, backup power systems, and consumer electronics installed bases continue to expand. Asia Pacific remains central to market development because the region combines large battery manufacturing capacity with growing recycling infrastructure and strong scrap availability across both lead-acid and lithium-ion streams.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Battery Scrap Market Size 2025 |

USD 28792.2 million |

| Battery Scrap Market, CAGR |

10.56% |

| Battery Scrap Market Size 2032 |

USD 58138.13 million |

Key Market Trends & Insights

- The market is projected to increase from USD 28792.2 million in 2025 to USD 58138.13 million by 2032, reflecting a strong long-term expansion trajectory.

- The Battery Scrap Market is forecast to grow at a CAGR of 10.56% from 2025 to 2032, supported by rising battery replacement cycles and tightening recycling compliance.

- Lead-acid battery scrap accounted for the largest share of 75.8% in 2025, reflecting its mature collection ecosystem and well-established secondary lead recovery chain.

- Electric vehicle battery scrap represented the leading source segment with 43.6% share in 2025, highlighting the growing contribution of EV battery retirement to available scrap volumes.

- Asia Pacific accounted for the largest regional share of 56.4% in 2025, supported by the region’s battery manufacturing concentration and expanding recycling footprint.

Segment Analysis

Battery scrap demand is increasingly shaped by the interplay between battery chemistry, source stream, and downstream recovery economics. Lead-acid scrap continues to anchor market revenues because collection systems are deeply entrenched across automotive, industrial, and backup power applications, creating predictable feedstock flows for recyclers. At the same time, lithium-ion scrap is gaining strategic importance as electric vehicle deployment expands and more high-value battery packs move toward repair, reuse, or recycling channels. Scrap processors are therefore balancing near-term dependence on lead recovery with longer-term investments in lithium, nickel, cobalt, and graphite extraction capabilities.

Commercial positioning in this market depends heavily on access to feedstock, processing efficiency, environmental compliance, and the ability to recover materials that can re-enter battery supply chains. Buyers increasingly prefer organized recyclers that can offer traceability, scale, and safe handling of hazardous battery waste. Reuse pathways are also gaining attention where usable battery capacity can be redirected into lower-intensity stationary applications before final recycling. Across regions, profitability remains closely linked to logistics networks, metal prices, and the extent of formal collection infrastructure.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Lead-acid battery scrap accounted for the largest share of 75.8% in 2025. The segment leads because lead-acid batteries have one of the most established collection and recovery systems in the broader battery value chain. Automotive replacement demand, industrial backup systems, and conventional energy storage applications continue to generate steady volumes of spent lead-acid units. Recyclers also benefit from proven recovery economics, since lead can be efficiently extracted and reintroduced into new battery manufacturing. Lithium-ion battery scrap remains the faster-growth chemistry stream as electric mobility and portable electronics increase end-of-life battery generation.

By Source Insights

Electric vehicle battery scrap accounted for the largest share of 43.6% in 2025. The segment leads because EV batteries contain high-value recoverable materials and are increasingly entering organized take-back, dismantling, and recycling channels. Rising electric vehicle adoption is expanding the installed battery base, which strengthens the long-term pipeline of recyclable scrap. Automakers and battery manufacturers are also supporting formal recovery systems to improve circularity and reduce exposure to raw material volatility. Consumer electronics and power tools remain important source streams, but their average battery size and value recovery potential are generally lower than EV packs.

By End Use Insights

Material extraction accounted for the largest share of 61.2% in 2025. The segment leads because the primary commercial objective of battery scrap processing is the recovery of valuable materials such as lead, lithium, nickel, cobalt, and graphite. Extracted materials can be refined and redirected into battery, metallurgical, and industrial value chains, which supports circular supply strategies. This end use also benefits from stronger economic justification than simple disposal, especially when metal recovery values remain favorable. Reuse is emerging as a growing secondary pathway where battery modules with remaining performance can be redeployed into less demanding storage applications.

Battery Scrap Market Drivers

Rising End-of-Life Battery Volumes from Transport and Electronics

The market is being driven by the rapid increase in the number of batteries reaching end-of-life across electric vehicles, conventional vehicles, power tools, telecom backup systems, and consumer electronics. Every expansion in the installed battery base eventually translates into a larger future scrap pool for collectors and recyclers. This is particularly important for lithium-ion batteries, where EV adoption is creating a new wave of high-value recyclable feedstock. The predictable replacement cycle of lead-acid batteries also supports steady recycling demand. Together, these flows are broadening the revenue base of the battery scrap industry.

Strong Economic Value of Recoverable Metals

Battery scrap recycling is supported by the commercial value of recoverable metals such as lead, lithium, nickel, cobalt, and graphite. Recyclers are not only managing waste streams but also producing secondary raw materials that can offset dependence on virgin mining. This creates stronger economic incentives for collection, dismantling, and treatment activities. As battery manufacturing expands, the importance of stable and diversified material supply is increasing. That dynamic strengthens the role of battery scrap as a strategic feedstock source.

- For instance, Umicore’s proprietary pyro-hydrometallurgical technology delivers recovery yields exceeding 95% for cobalt, copper, and nickel, and over 90% for lithium across a wide variety of battery chemistries outputting these metals in battery-grade purity ready for direct re-entry into cathode production.

Tightening Environmental and Waste Management Regulation

Governments and regulators are increasing scrutiny over hazardous battery disposal, recycling traceability, and producer responsibility frameworks. These rules are pushing more spent batteries into formal recycling systems instead of informal dumping or uncontrolled processing. Compliance requirements are also favoring larger and more organized operators with better safety, emissions control, and documentation systems. This improves market visibility and supports investment in recycling infrastructure. Over time, tighter regulation is expected to further formalize collection networks and improve recovery rates.

- For instance, the EU Battery Regulation (2023/1542), which came into full producer responsibility effect in August 2025, mandates portable battery collection rates of 63% by end-2027 and 73% by end-2030, while from 2027 onward recyclers must achieve material recovery efficiencies of at least 90% for cobalt, nickel, copper, and lead, and 80% for lithium by 2031.

Investment in Advanced Recycling Technologies

The market is also benefiting from continued investment in hydrometallurgical, direct recycling, and integrated refining approaches. These technologies are being adopted to improve recovery efficiency, raise purity levels, and expand the range of materials that can be economically extracted. Technology improvements are especially important for lithium-ion battery scrap, where chemistry complexity is higher than in traditional lead-acid systems. As process performance improves, recycling becomes more commercially viable across a broader set of battery types. This supports both capacity expansion and stronger competitive differentiation.

Battery Scrap Market Challenges

Battery scrap processing remains operationally complex because battery chemistries vary widely in structure, material composition, and handling requirements. Safe transportation, storage, dismantling, and discharging of spent batteries require specialized procedures and trained personnel. Lithium-ion batteries in particular carry fire and thermal risks, which increase logistics and compliance costs. Informal or fragmented collection systems can further reduce feedstock consistency for organized recyclers. These factors make scaling difficult in markets where infrastructure is still developing.

- For instance, Fortum Battery Recycling operates mechanical recycling and dismantling facilities in Kirchardt, Germany, and Ikaalinen, Finland, and states that its Harjavalta hydrometallurgical plant can recover up to 95% of the valuable metals from battery black mass, while about 80% of an entire battery can be recycled when its mechanical and hydrometallurgical stages are combined.

Another major challenge is the uneven economics of recovery across battery types and geographies. Profitability depends heavily on commodity prices, local labor costs, collection efficiency, and the availability of downstream refining capacity. In some regions, recyclers still face weak formal collection systems and competition from low-cost informal channels. The market also remains exposed to technology risk as operators invest in new recycling platforms that may take time to optimize commercially. This creates margin pressure, especially for companies expanding into lithium-ion processing.

Battery Scrap Market Trends and Opportunities

A major market trend is the transition from traditional lead-acid-focused recycling models toward broader multi-chemistry platforms that can process lithium-ion batteries at scale. Companies are expanding capacity to capture rising EV-related scrap volumes and recover critical minerals needed for next-generation battery manufacturing. This is gradually changing the competitive landscape from conventional recycling toward strategic materials recovery. Vertical integration between collection, black mass processing, and refining is becoming more important. These shifts are opening new opportunities for specialized recyclers and technology providers.

- For instance, Redwood Materials has ramped hydrometallurgical operations in Nevada that reclaim 95% of lithium from scrap battery materials, commissioned a reductive calciner that can process more than 40,000 metric tons of battery feed annually, and stated that its campus was already processing 30,000 tons per year with equipment planned to ramp to 60,000 tons, or about 15 GWh, by the end of 2024.

Another important opportunity lies in second-life battery applications and circular supply partnerships. Battery modules that retain usable capacity can be redeployed into stationary storage, backup systems, and lower-load commercial applications before final recycling. This creates an intermediate monetization pathway that can improve asset utilization. At the same time, partnerships between recyclers, automakers, energy storage companies, and material refiners are becoming more common as the industry seeks traceable closed-loop ecosystems. Such arrangements can strengthen feedstock security and improve long-term revenue visibility.

Regional Insights

North America

North America accounted for 18.6% of the Battery Scrap Market in 2025. The region benefits from mature lead-acid battery collection systems, established recycling infrastructure, and increasing investment in lithium-ion recovery capacity. Demand is being reinforced by policy support for domestic battery material supply chains and by the expansion of electric vehicle manufacturing. Formal compliance standards and industrial-scale processing capabilities support the position of organized recyclers. The market is also gaining momentum from efforts to localize battery raw material recovery and reduce import dependence.

Europe

Europe accounted for 16.7% of the Battery Scrap Market in 2025. The region is supported by strong environmental regulation, circular economy targets, and a growing focus on battery traceability and recovery efficiency. Battery recycling demand is reinforced by the region’s automotive manufacturing base and its push to build a more self-sufficient battery ecosystem. Organized collection and regulatory enforcement favor formal recyclers with strong compliance capabilities. Europe remains a strategically important market for closed-loop battery material recovery.

Asia Pacific

Asia Pacific accounted for 56.4% of the Battery Scrap Market in 2025. The region leads due to its large battery manufacturing base, high vehicle and electronics production volumes, and increasing availability of end-of-life battery feedstock. China remains central to regional scale because of its integrated battery supply chain and broad recycling ecosystem. India and other Asian markets are also expanding collection and processing capacity as battery demand rises across transport and backup applications. These factors keep Asia Pacific at the forefront of both scrap generation and material recovery.

Latin America

Latin America accounted for 4.8% of the Battery Scrap Market in 2025. The regional market is supported mainly by lead-acid battery replacement demand in automotive and industrial applications. Growth is gradually improving as waste handling systems become more formalized and awareness of recycling compliance increases. The region still has a smaller industrial recycling footprint than North America, Europe, and Asia Pacific. Even so, developing collection networks and rising battery use create room for further market expansion.

Middle East & Africa

Middle East & Africa accounted for 3.5% of the Battery Scrap Market in 2025. Regional demand is linked to automotive battery replacement, telecom infrastructure, backup power systems, and broader industrial battery usage. Market development is more gradual because formal recycling capacity and collection networks remain uneven across countries. However, the need for compliant hazardous waste management is increasing. This is likely to support gradual expansion of organized battery scrap processing over time.

Competitive Landscape

The Battery Scrap Market is characterized by a mix of established lead recyclers, integrated materials recovery companies, and newer lithium-ion-focused operators. Competition is shaped by access to feedstock, processing scale, recovery efficiency, environmental compliance, and relationships across collection and downstream refining networks. Companies are differentiating themselves through technology platforms, regional expansion, and the ability to recover battery-grade secondary materials. The market is also seeing a stronger push toward closed-loop partnerships tied to electric vehicle and energy storage supply chains. Operators with multi-chemistry capabilities and secure scrap sourcing are better positioned to capture long-term growth.

Li-Cycle has built its market positioning around lithium-ion battery recycling with a focus on recovering critical materials from battery manufacturing scrap and end-of-life batteries. The company’s approach has centered on combining regional collection and pre-processing capabilities with larger-scale downstream recovery infrastructure. This specialization aligns with the market’s shift toward EV-related scrap streams and the need for domestic critical mineral recovery. Strategic restructuring activity has also reflected the capital intensity and operational complexity of scaling lithium-ion recycling. Even so, the company remains relevant as an example of how specialization in high-value battery material recovery is reshaping competitive dynamics.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, Aqua Metals and American Battery Factory (ABF) signed a Memorandum of Understanding (MOU) to collaborate on recycling lithium-ion phosphate (LFP) battery manufacturing scrap generated by ABF’s U.S.-based production facilities. In this proposed collaboration, Aqua Metals would develop a co-located recycling facility capable of processing up to 10,000 metric tons of lithium-ion battery materials annually and returning battery-grade lithium carbonate back into ABF’s supply chain.

- In November 2025, Clarios announced that it is accelerating multiple strategic paths to significantly grow its battery recycling and critical mineral processing capacity in the United States to meet rising demand for battery scrap recovery. In expanding its recycling operations, the company aimed to address increasing volumes of lead-acid and advanced battery scrap being generated across the country.

- In August 2025, Glencore completed its takeover of Li-Cycle’s battery recycling assets after Li-Cycle filed for bankruptcy, with Glencore submitting a bid of approximately $40 million to acquire the assets. In inheriting Li-Cycle’s “spoke and hub” recycling model which breaks down used batteries into black mass before refining them into high-value metals Glencore instantly positioned itself as a leader in the North American battery scrap supply chain.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 28792.2 million |

| Revenue forecast in 2032 |

USD 58138.13 million |

| Growth rate (CAGR) |

10.56% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

Product Type Outlook: Lead-acid battery scrap, Lithium-ion battery scrap, Other battery scrap; Source Outlook: Electric vehicle battery scrap, Consumer electronics battery scrap, Power tools battery scrap, Other sources; End Use Outlook: Material extraction, Reuse, Disposal, Other end uses |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Li-Cycle, Umicore, Husky Battery Solutions, ENGITEC Technologies SpA, Sunlight Group, Aqua Metals, Inc., Ecobat, Exide Industries Ltd., Guangdong Brunp Recycling Technology Co., Ltd., Gravita India Ltd. |

| No. of Pages |

330 |

By Segmentation

By Product Type

- Lead-acid battery scrap

- Lithium-ion battery scrap

- Other battery scrap

By Source

- Electric vehicle battery scrap

- Consumer electronics battery scrap

- Power tools battery scrap

- Other sources

By End Use

- Material extraction

- Reuse

- Disposal

- Other end uses

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa