Big Data in Oil & Gas Exploration & Production Market Overview:

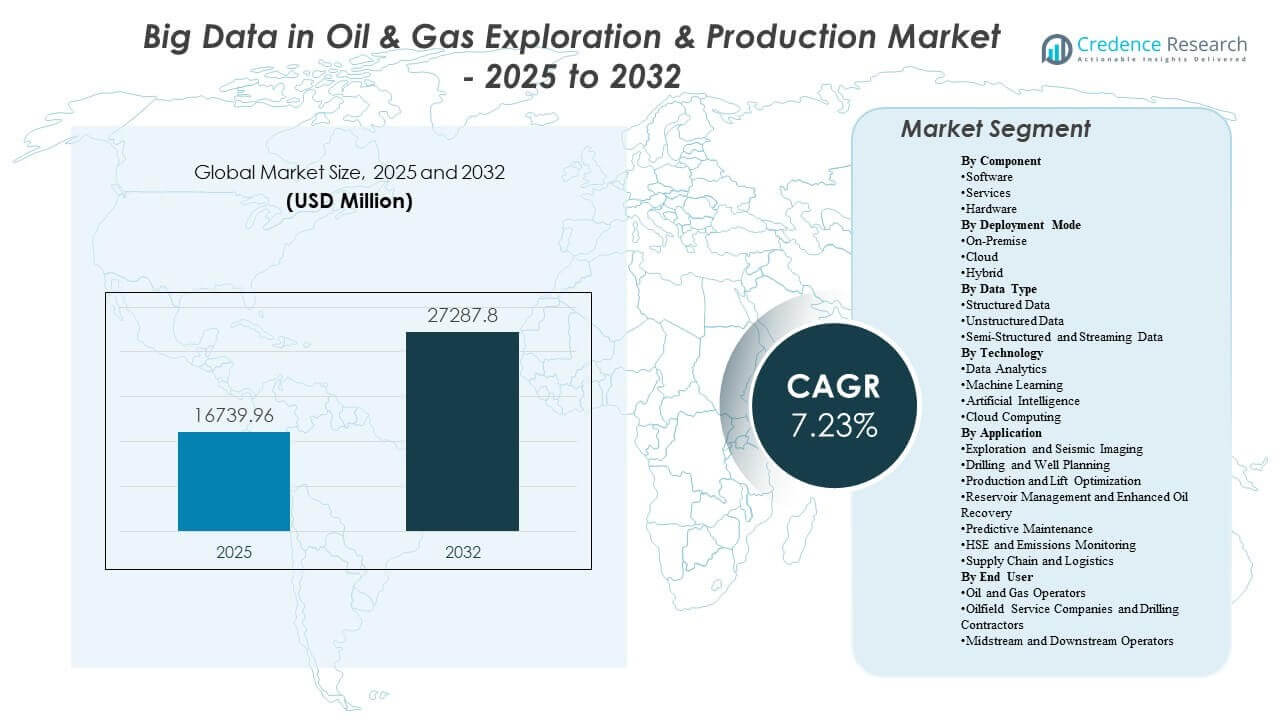

The global Big Data in Oil & Gas Exploration & Production Market size was estimated at USD 16,739.96 million in 2025 and is expected to reach USD 27,287.8 million by 2032, growing at a CAGR of 7.23% from 2025 to 2032. The strongest growth driver is the rising operational need to convert high-frequency subsurface and production data into faster, higher-confidence decisions that improve drilling outcomes, stabilize production performance, and reduce non-productive time across complex assets. Adoption is also supported by expanding digital programs across major basins and offshore projects, where modern analytics stacks increasingly integrate engineering workflows with reliability and emissions monitoring requirements.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Big Data in Oil & Gas Exploration & Production Market Size 2025 |

USD 16,739.96 million |

| Big Data in Oil & Gas Exploration & Production Market, CAGR |

7.23% |

| Big Data in Oil & Gas Exploration & Production Market Size 2032 |

USD 27,287.8 million |

Key Market Trends & Insights

- Software accounted for the largest share of 62% in 2025, reflecting platform-led adoption across interpretation, optimization, and reliability workflows.

- On-premise deployments held 41.27% share in 2025, supported by data sovereignty priorities and latency-sensitive operational environments.

- Structured data represented 38.74% share in 2025, anchored by production histories, maintenance records, and enterprise reporting requirements.

- Reservoir Management and Enhanced Oil Recovery accounted for 34% share in 2025, driven by recovery-factor improvement and injection optimization priorities.

- The market is expanding at 23% CAGR (2025–2032), supported by broader integration of analytics into core upstream planning and operations cycles.

Segment Analysis

Adoption of big data and advanced analytics in upstream environments is increasingly tied to the scale and complexity of datasets generated across exploration, drilling, production, and asset maintenance workflows. Higher sensor density, expanding SCADA coverage, and multi-disciplinary subsurface models are increasing demand for governed data pipelines that can support near-real-time decisions and repeatable optimization cycles. Organizations are prioritizing architectures that can handle mixed data formats while enforcing security and access controls across teams and sites. As a result, value creation is increasingly linked to the ability to operationalize insights in engineering workflows rather than only generating reports.

Deployment strategies are evolving around governance, performance, and total cost of ownership considerations. Operators commonly pursue staged modernization that strengthens data quality, standardization, and interoperability across applications used for interpretation, planning, and operations. Hybrid approaches are increasingly used to balance high-performance processing needs with enterprise governance, keeping sensitive datasets controlled while enabling scalable compute when workloads spike. Over time, workflow automation and model reuse are becoming more important procurement criteria as organizations look to reduce manual analysis effort and improve decision speed at the asset level.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Component Insights

Software accounted for the largest share of 38.62% in 2025. Platform capabilities lead because they standardize ingestion, cataloging, modeling, and workflow execution across subsurface and operations teams. Software-led adoption also accelerates integration across interpretation, planning, production optimization, and reliability functions, improving repeatability and governance. As compute becomes more elastic and infrastructure refresh cycles lengthen, differentiation increasingly shifts toward analytics depth, workflow automation, and interoperability across vendor ecosystems.

By Deployment Mode Insights

On-Premise accounted for the largest share of 41.27% in 2025. On-premise environments remain preferred where data sovereignty, IP protection, and low-latency control are central to operational continuity and risk management. Many upstream sites require predictable performance for monitoring and control workflows that depend on stable connectivity and tightly managed access permissions. Hybrid deployment is increasingly used to retain sensitive datasets locally while enabling scalable processing when simulation, interpretation, or analytics workloads intensify.

By Data Type Insights

Structured Data accounted for the largest share of 38.74% in 2025. Structured datasets remain foundational because production histories, maintenance records, and operational logs are central inputs for optimization, planning, and performance benchmarking. Standardized formats also support enterprise reporting and facilitate integration across multiple applications and business units. At the same time, growth in streaming and semi-structured feeds is increasing the need for architectures that can unify telemetry, event data, and operational context into decision-ready pipelines.

By Technology Insights

Technology adoption in the market is shaped by the need to move from descriptive analytics to predictive and prescriptive decision support across upstream workflows. Data analytics remains a baseline capability for performance visibility, root-cause analysis, and continuous improvement programs. Machine learning and artificial intelligence are increasingly used to improve drilling risk prediction, automate interpretation tasks, and enhance asset reliability through early-warning signals. Cloud computing plays a critical role in scaling compute-intensive workloads and enabling centralized governance across distributed assets, especially when combined with secure hybrid operating models.

By Application Insights

Reservoir Management and Enhanced Oil Recovery accounted for the largest share of 21.34% in 2025. These workflows lead because they directly influence field economics through recovery-factor improvement, injection strategy optimization, and tighter reservoir surveillance. Analytics-driven reservoir modeling supports faster scenario evaluation and improves alignment between subsurface understanding and operational execution. As pressure to maximize output from mature assets rises, EOR analytics and continuous reservoir monitoring become higher-priority investment areas alongside production optimization and reliability analytics.

By End User Insights

End-user adoption is led by organizations with the largest operational datasets and the strongest incentives to convert data into faster, repeatable decisions. Oil and gas operators typically drive demand through enterprise-wide digital programs aimed at improving drilling outcomes, stabilizing production performance, and strengthening reliability and safety practices. Oilfield service companies and drilling contractors contribute by embedding analytics into service delivery and offering standardized digital workflows across clients and basins. Midstream and downstream operators adopt similar capabilities where integrity monitoring, reliability analytics, and logistics optimization create measurable operational value, often supported by integrated data governance initiatives.

Big Data in Oil & Gas Exploration & Production Market Drivers

Rising operational complexity and data intensity in upstream assets

Upstream operations generate increasingly dense datasets from drilling instrumentation, production telemetry, and reservoir surveillance systems. As asset complexity increases, manual interpretation becomes less efficient and more error-prone across engineering workflows. Big data platforms improve the ability to consolidate, clean, and contextualize multi-source inputs into actionable intelligence. This strengthens decision speed in planning and execution cycles and improves repeatability across assets and teams.

- For instance, Shell’s integrated data-driven drilling program in the Deep Sleep well in the Gulf of Mexico used high-frequency drilling data and advanced analytics to increase on-bottom rate of penetration (ROP) to 275 ft/h, a 52% improvement over the best offset well, while drilling 4,230 ft in a single day more than twice the previous average daily footage.

Need to reduce non-productive time and improve drilling and production performance

Operators prioritize analytics investments that reduce downtime, optimize drilling parameters, and stabilize production systems. Predictive models and decision support tools can identify abnormal patterns earlier and enable faster interventions. Improved workflow integration helps align subsurface interpretation with drilling execution and production targets. This performance focus sustains investment even during periods of cost discipline because value is tied to measurable operational improvements.

- For instance, one field application of machine-learning-based ROP optimization reported time savings of about 30 hours on a single well, equivalent to roughly 12.5% of the total drilling time, by continuously tuning weight-on-bit, RPM, and flow rate based on predictive models.

Expansion of reliability programs and predictive maintenance across critical equipment

Rotating equipment, pumps, compressors, and other critical assets require consistent monitoring to avoid unplanned outages. Advanced analytics enable early-warning detection using pressure, vibration, temperature, and flow signatures. Reliability programs increasingly connect maintenance planning with operational data to prioritize interventions and reduce life-cycle costs. This expands demand for scalable data pipelines and model management capabilities across distributed sites.

Increasing emphasis on HSE, compliance, and emissions monitoring integration

Regulatory expectations and corporate commitments are increasing the need for integrated monitoring and reporting. Data platforms help unify sensor feeds, operational logs, and inspection records into auditable datasets. Analytics supports anomaly detection, incident prevention, and performance tracking across safety and environmental objectives. This expands adoption beyond subsurface and production use cases into broader operational governance and reporting workflows.

Big Data in Oil & Gas Exploration & Production Market Challenges

Data quality, fragmentation, and interoperability remain persistent barriers to scaling analytics across large upstream organizations. Legacy systems often store critical data in inconsistent formats, and integration across multiple vendor applications can be complex and costly. Inconsistent tagging, incomplete metadata, and limited standardization can reduce model performance and slow adoption in operational workflows. These constraints increase dependence on specialized integration expertise and can delay time-to-value for enterprise rollouts.

- For instance, OMV’s AI workflows in DELFI only reached full efficiency after standardized model realizations allowed the subsurface team to automatically generate and simulate 200 reservoir models in one sixth of the usual time, indicating how harmonized inputs directly improve model throughput and reliability.

Cybersecurity, IP protection, and governance constraints also limit the pace of modernization, particularly when datasets contain sensitive subsurface information and operational configurations. Organizations must balance accessibility for multi-disciplinary teams with strict controls on usage, sharing, and retention. In remote environments, connectivity limitations can restrict cloud-first approaches and require resilient architectures with local processing. As a result, many deployments progress in phased steps that prioritize governance, reliability, and compliance over rapid scale.

Market Trends and Opportunities

Hybrid architectures are becoming a preferred pathway for organizations modernizing upstream data estates, enabling localized control for sensitive datasets while providing scalability for compute-intensive workloads. This creates opportunities for vendors that support consistent governance across environments and simplify workload orchestration across distributed sites. Increased standardization efforts and open data practices further improve portability across applications, which strengthens long-term platform adoption. Over time, these approaches reduce integration friction and enable broader analytics reuse across asset classes.

- For instance, bp standardized upstream operational data in the AVEVA PI System and PI Vision across its North Sea assets, which supported analytics that lifted production by more than 20,000 barrels per day on one asset through improved access to contextualized time‑series data.

Workflow automation and AI-enabled interpretation are expanding beyond experimentation into operational deployment, particularly where decision cycles are frequent and outcomes are measurable. Opportunities are strongest in drilling risk prediction, automated log interpretation, production optimization, and reliability analytics where model outputs can be embedded into routine operating procedures. Vendors that provide domain-specific templates, model governance, and explainable outputs are positioned to gain share as adoption matures. This trend also supports growth in services tied to change management, data governance, and operationalization of analytics workflows.

Regional Insights

North America

North America accounted for 36.68% share in 2025, supported by data-intensive unconventional operations, mature digital workflows, and strong platform adoption across large operators and service providers. The region benefits from deep ecosystems of technology vendors, analytics specialists, and oilfield digital service capabilities that accelerate deployment cycles. Operational priorities commonly focus on drilling efficiency, production optimization, and reliability programs that can be scaled across multiple assets. As organizations continue modernizing data estates, hybrid deployment models remain common to balance performance needs and governance requirements.

Europe

Europe accounted for 21.87% share in 2025, reflecting strong adoption across complex offshore operations and established upstream organizations with mature engineering workflows. Emissions monitoring and safety-led analytics are frequently integrated into broader digital transformation roadmaps, supporting multi-use platform investments. The region’s emphasis on governance and standardization supports structured data management and repeatable analytics at scale. Continued modernization focuses on interoperability, workflow automation, and higher-quality decision support across subsurface and operations teams.

Asia Pacific

Asia Pacific accounted for 20.43% share in 2025, supported by expanding upstream activity and accelerating digital investment agendas across major markets. Organizations are increasingly focused on improving exploration success rates, optimizing drilling programs, and strengthening operational reliability through analytics. Adoption is reinforced by large-scale projects that benefit from centralized data platforms and standardized workflows. The region’s growth trajectory is supported by continued infrastructure development, increasing digital maturity, and broader use of advanced analytics in operational decision cycles.

Latin America

Latin America accounted for 7.11% share in 2025, with adoption concentrated in selective operators and projects where offshore complexity and asset reliability priorities justify platform investments. The region’s deployments often emphasize practical use cases tied to production performance, integrity monitoring, and maintenance optimization. Implementation can be uneven due to differences in organizational maturity, integration readiness, and investment cycles across markets. As modernization progresses, opportunities expand for scalable analytics offerings that reduce integration burden and improve time-to-value.

Middle East & Africa

Middle East & Africa accounted for 13.91% share in 2025, supported by large-field operations, extensive production datasets, and growing digital programs led by major upstream organizations. Analytics adoption is frequently tied to reservoir surveillance, production optimization, and operational governance requirements across high-volume assets. Procurement cycles and phased modernization approaches can shape deployment speed, but platform investments remain strategic where efficiency and reliability gains are measurable. Increasing integration of safety and emissions monitoring also strengthens demand for governed data pipelines and advanced analytics capabilities.

Competitive Landscape

Competition is shaped by the ability to deliver scalable data platforms that integrate subsurface interpretation, drilling decision support, production optimization, and asset reliability workflows under strong governance. Vendors differentiate through domain-specific analytics accelerators, interoperability across multi-vendor ecosystems, and deployment flexibility across on-premise, cloud, and hybrid environments. Platform depth in workflow orchestration, model governance, and operationalization capabilities is increasingly important as organizations scale beyond pilots. Service capability in integration, change management, and security assurance remains a key enabler of large enterprise deployments.

IBM’s approach is typically positioned around enterprise data management, analytics platforms, and AI capabilities that support governed workflows across large, complex organizations. The company’s strength is often linked to integrating diverse data sources, enabling policy-driven governance, and supporting scalable analytics across business units. Such capabilities align with upstream needs for secure access control, standardized pipelines, and repeatable decision support across distributed assets. This positioning can be relevant where operators prioritize enterprise integration and long-term platform extensibility across multiple workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- IBM

- Microsoft

- Amazon Web Services (AWS)

- Google Cloud

- Oracle

- SAP SE

- Schlumberger

- Halliburton

- Baker Hughes

- Weatherford

- Siemens

- Honeywell

- Accenture

- AspenTech

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In November 2025, ADNOC and SLB launched the AI-powered Production System Optimization solution, which uses millions of real-time data points along with SLB’s Lumi data and AI platform and Cognite Data Fusion to improve upstream productivity and decision-making across operations.

- In September 2025, SLB announced its acquisition of RESMAN Energy Technology, saying the deal would add reservoir tracer technologies and combine them with SLB’s advanced digital workflows to deliver faster insights and smarter data-driven production decisions.

- In July 2025, SLB launched the OnWave autonomous logging platform, a new product designed to streamline well logging and accelerate data-driven exploration and production workflows.

- In November 2024, PETRONAS, through Malaysia Petroleum Management, partnered with Earth Science Analytics and Amazon Web Services to expand the use of AI and machine learning in Malaysia’s oil and gas sector, with the work focused on improving exploration in the Malay Basin and strengthening the myPROdata platform’s data capabilities for better upstream decision-making.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 16,739.96 million |

| Revenue forecast in 2032 |

USD 27,287.8 million |

| Growth rate (CAGR) |

7.23% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Component Outlook: Software, Services, Hardware;

By Deployment Mode Outlook: On-Premise, Cloud, Hybrid;

By Data Type Outlook: Structured Data, Unstructured Data, Semi-Structured and Streaming Data;

By Technology Outlook: Data Analytics, Machine Learning, Artificial Intelligence, Cloud Computing;

By Application Outlook: Exploration and Seismic Imaging, Drilling and Well Planning, Production and Lift Optimization, Reservoir Management and Enhanced Oil Recovery, Predictive Maintenance, HSE and Emissions Monitoring, Supply Chain and Logistics;

By End User Outlook: Oil and Gas Operators, Oilfield Service Companies and Drilling Contractors, Midstream and Downstream Operators |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

IBM, Microsoft, Amazon Web Services (AWS), Google Cloud, Oracle, SAP SE, Schlumberger, Halliburton, Baker Hughes, Weatherford, Siemens, Honeywell, Accenture, AspenTech |

| No. of Pages |

338 |

Segmentation

By Component

- Software

- Services

- Hardware

By Deployment Mode

By Data Type

- Structured Data

- Unstructured Data

- Semi-Structured and Streaming Data

By Technology

- Data Analytics

- Machine Learning

- Artificial Intelligence

- Cloud Computing

By Application

- Exploration and Seismic Imaging

- Drilling and Well Planning

- Production and Lift Optimization

- Reservoir Management and Enhanced Oil Recovery

- Predictive Maintenance

- HSE and Emissions Monitoring

- Supply Chain and Logistics

By End User

- Oil and Gas Operators

- Oilfield Service Companies and Drilling Contractors

- Midstream and Downstream Operators

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa