Boil Off Gas (BOG) Compressor Market Overview:

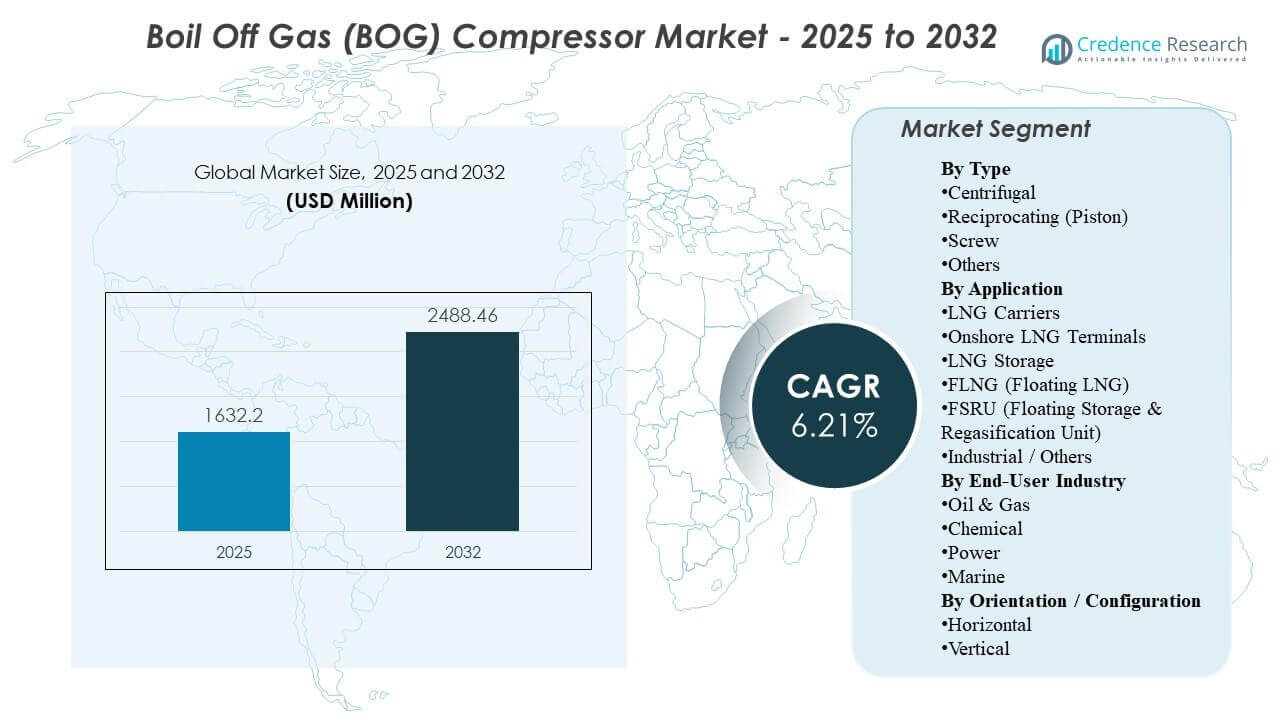

The global Boil Off Gas (BOG) Compressor Market size was estimated at USD 1632.2 million in 2025 and is expected to reach USD 2488.46 million by 2032, growing at a CAGR of 6.21% from 2025 to 2032. Growth is primarily supported by rising LNG throughput across the value chain, where operators prioritize reliable boil-off handling to reduce product loss, maintain tank pressure stability, and improve operational efficiency at terminals and storage sites. Demand is also supported by continued investments in LNG infrastructure and the need to integrate BOG management with fuel gas, reliquefaction, and emissions-control strategies across onshore and floating assets.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Boil Off Gas (BOG) Compressor Market Size 2025 |

USD 1632.2 million |

| Boil Off Gas (BOG) Compressor Market, CAGR |

6.21% |

| Boil Off Gas (BOG) Compressor Market Size 2032 |

USD 2488.46 million |

Key Market Trends & Insights

- Reciprocating (Piston) compressors accounted for the largest share of 46% in 2025, reflecting strong adoption in duty cycles requiring robust high-pressure performance.

- Onshore LNG Terminals represented 61% in 2025, indicating that terminal-based boil-off handling remains the core installation base for BOG compression systems.

- The Power end-user segment held 52% in 2025, supported by LNG-to-power linkages and steady demand for secure gas supply and pressure management.

- North America captured 35% share in 2025, supported by mature gas infrastructure, LNG ecosystem investments, and emphasis on operational reliability.

- Europe held 24% share in 2025, driven by LNG import infrastructure utilization and system optimization priorities across terminals and regasification assets.

Segment Analysis

BOG compressors are deployed to capture, condition, and route boil-off gas generated during LNG storage, loading/unloading, and regasification. Buyer requirements typically center on reliability, stable performance across variable flow rates, and fit-for-purpose integration with terminal and storage process trains. Equipment selection also reflects practical constraints such as available plot space, maintainability, vibration control, and lifecycle serviceability, especially for assets designed for continuous operation.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Across the market, procurement decisions increasingly emphasize total cost of ownership and uptime rather than only initial capex. This supports demand for proven designs, standardized skids, and strong aftermarket support for spares, overhaul, and field service. Application dominance at onshore terminals also raises the importance of seamless tie-ins with fuel gas systems and operational controls, enabling operators to minimize venting and improve overall LNG handling efficiency.

By Type Insights

Reciprocating (Piston) accounted for the largest share of 46% in 2025. This leadership is supported by suitability for demanding operating conditions where pressure ratios and stable compression performance are critical across varying boil-off rates. Reciprocating platforms are also widely adopted due to familiarity in LNG operations, established maintenance practices, and availability of service capabilities. For many operators, these factors reduce operational risk and support predictable lifecycle planning for critical BOG handling duties.

By Application Insights

Onshore LNG Terminals accounted for the largest share of 61% in 2025. Terminals face continuous boil-off generation across storage and transfer activities, making reliable compression a core requirement for safe and efficient operations. Terminal projects also increasingly prioritize modular integration and smooth control-system interfacing to align BOG handling with broader plant performance. Additionally, terminal operators commonly pursue solutions that reduce product losses and support stable tank management under fluctuating send-out and ship-loading cycles.

By End-User Industry Insights

Power accounted for the largest share of 52% in 2025. LNG-to-power demand links regasification reliability to electricity supply stability, increasing the importance of robust boil-off management. BOG compression supports fuel utilization strategies by enabling controlled routing of boil-off into fuel systems or downstream processing where appropriate. The segment also benefits from operational priorities such as high availability and predictable maintenance windows, particularly for facilities supporting baseload and peak power generation requirements.

By Orientation / Configuration Insights

Horizontal and Vertical configurations are selected primarily based on footprint constraints, maintainability preferences, and integration requirements within LNG layouts. Space-limited settings such as modular terminals, marine-linked infrastructure, and certain offshore contexts can favor compact configurations and simplified access planning. Configuration choice is also influenced by vibration management, skid layout, and ease of service for critical components. As project designs increasingly optimize plot space and installation schedules, fit-for-layout becomes a more prominent differentiator during equipment selection.

Market Drivers

Expansion and optimization of LNG infrastructure

Continued investments in LNG terminals, storage, and regasification assets increase the installed base for boil-off handling systems. As throughput rises, operators require dependable compression to manage continuous boil-off generation and stabilize tank pressure. Terminal optimization programs also drive upgrades and retrofits that improve operational efficiency and reduce avoidable losses. These factors collectively support sustained demand for BOG compressors across new-build and brownfield projects.

- For instance, in the German LNG onshore regasification terminal project at Brunsbüttel, Sener notes a design basis of up to 8 BCMA send-out (expandable to at least 10 BCMA) and two 165,000 m³ storage tanks—scale that directly increases the installed base needing boil-off handling and compression hardware.

Operational reliability and uptime requirements in critical LNG operations

BOG compression is a mission-critical function where downtime can disrupt storage stability and downstream operations. Buyers therefore prioritize proven equipment designs, robust control integration, and reliable service support. High availability requirements reinforce demand for equipment configurations that simplify maintenance and reduce unplanned outages. This reliability focus also encourages investment in monitoring, spares planning, and long-term service agreements.

- For instance, Burckhardt Compression positions its Laby‑GI BOG solution with documented product availability “above 98%” and “more than 2 million operating hours at sea,” quantifying reliability in continuous LNG operations.

Economics of product loss reduction and gas utilization

Capturing and compressing boil-off reduces LNG losses and enables controlled routing of gas for fuel use or processing. In high-throughput environments, incremental efficiency improvements can translate into meaningful operational value. BOG compression also supports stable operating conditions and reduces the need for operational workarounds. As operators emphasize efficiency and cost discipline, solutions that improve gas utilization become more attractive.

Growth of LNG-to-power linkages and flexible gas supply chains

The expansion of LNG as a fuel source for power generation increases the importance of reliable LNG handling and stable supply. Facilities supporting power demand prioritize continuity, predictable performance, and robust integration across the LNG chain. BOG compressors support these requirements by maintaining storage stability and enabling controlled management of boil-off gas. This strengthens demand where LNG infrastructure is closely tied to power generation needs.

Market Challenges

BOG compressor projects face complexity related to engineering integration, especially where assets require tight coupling with fuel gas systems, reliquefaction, and control architectures. Equipment sizing must accommodate variable flow regimes, shifting duty cycles, and evolving operating conditions across terminals and storage sites. These factors increase engineering effort and can extend commissioning timelines if interfaces are not standardized early. In addition, procurement teams often balance capex constraints against reliability requirements, which can delay decisions for mission-critical installations.

- For instance, in the Cedar LNG project award booked in Q1 2024, Baker Hughes’ scope included two electric-driven boil-off gas compressors an equipment choice that typically increases electrical, controls, and protection-system interface work versus conventional driver arrangements.

Operational challenges also include maintenance planning, spares availability, and service access, particularly for installations where footprint and layout constraints limit ease of intervention. Compressor performance can be sensitive to suction conditions and process variability, placing importance on robust controls and protective systems. Long lead times for specialized components and tight project schedules can further elevate delivery risk. Collectively, these issues push buyers toward vendors with strong execution capability and mature service ecosystems.

Market Trends and Opportunities

A key trend is the increasing preference for modular and skid-based solutions that reduce site work, simplify integration, and support faster project execution. Buyers are also emphasizing higher reliability and predictable lifecycle service through condition monitoring and structured maintenance programs. These priorities align with the broader shift toward performance-based procurement where uptime and total cost of ownership carry more weight. As LNG assets diversify across onshore and floating infrastructure, flexibility and integration readiness become stronger differentiators.

Opportunities also exist in retrofits and upgrades at existing terminals and storage facilities where operators aim to improve efficiency and boil-off handling performance. Integration improvements with digital monitoring and control systems can support better operational visibility and reduced unplanned downtime. The expanding LNG-to-power ecosystem creates demand for dependable boil-off handling aligned to dispatch variability and fuel management strategies. Vendors that provide application engineering depth and responsive aftermarket coverage are positioned to benefit from these shifts.

- For instance, Howden’s packaged process gas screw compressor systems are specified up to 26,000 m3/hr flow, up to 15 bar(a) pressure, and up to 4,000 kW power, and its turbo blower range indicates turndown to 45% volume flow capabilities that map directly to variable-duty boil-off and LNG-to-power operating profiles.

Regional Insights

North America

North America held 35% of global revenue in 2025, supported by a mature gas value chain and strong operational focus on reliability and efficiency. Demand is driven by LNG ecosystem investments, terminal utilization, and ongoing performance optimization in established assets. Buyers typically prioritize proven compressor performance, service coverage, and lifecycle support for critical operations.

Europe

Europe accounted for 24% revenue share in 2025, reflecting substantial demand tied to LNG import infrastructure utilization and optimization. Regional buyers often prioritize dependable boil-off handling integrated with regasification operations and terminal controls. The market also benefits from continued investment in LNG import and storage capabilities and a strong emphasis on operational efficiency across facilities.

Asia Pacific

Asia Pacific represented 26% share in 2025, supported by high LNG import intensity and sustained terminal and storage usage. Demand is anchored by the need for stable, reliable boil-off management across diverse operating profiles. Buyers often value equipment flexibility and integration readiness to fit varied terminal configurations and utilization patterns.

Latin America

Latin America held 6% share in 2025, reflecting a smaller LNG infrastructure base relative to major regions. Growth is supported by gradual additions in LNG-to-power and industrial LNG usage, where reliable boil-off handling improves operational stability. Procurement tends to emphasize cost-effective lifecycle performance and service accessibility.

Middle East & Africa

Middle East & Africa accounted for 9% share in 2025, supported by LNG infrastructure development and export-linked ecosystems. Demand is shaped by large-scale project nodes and the need for robust, high-reliability solutions in critical LNG operations. Buyers often prioritize equipment resilience and strong service capability due to the operational importance of boil-off handling.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Competitive Landscape

Competition is shaped by equipment reliability, application engineering capability, energy efficiency, footprint optimization, and aftermarket service depth. Vendors differentiate through proven compressor platforms, modular skid offerings, and integration support across LNG terminal, storage, and marine-linked applications. Service responsiveness, spares availability, and long-term maintenance programs are also key decision factors for operators focused on uptime. As projects diversify across onshore and floating infrastructure, flexibility and execution capability increasingly influence vendor selection.

Atlas Copco’s positioning typically centers on engineered compression solutions with an emphasis on operational reliability, system integration, and lifecycle support. The company’s approach aligns with buyer priorities in LNG environments where availability and maintainability are critical procurement criteria. Its competitive strength is supported by global service reach and experience in industrial compression applications that translate into LNG boil-off handling requirements. This makes it relevant for projects prioritizing predictable performance and dependable aftermarket coverage.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlas Copco

- Burckhardt Compression

- Siemens Energy

- Baker Hughes

- Elliott Group

- SIAD Macchine Impianti

- Hanwha Power Systems

- MAN Energy Solutions

- NEUMAN & ESSER Group

- Howden Group

- Mitsubishi Heavy Industries

- Kobe Steel Ltd.

- Cryostar

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In June 2025, Atlas Copco announced that Spanish compressor manufacturer ABC Compressors would become part of Atlas Copco Group, with Atlas Copco explicitly framing the deal as enhancing its offering within gas and air compression (closing expected in Q3 2025).

- In June 2025, Jier New Energy Equipment published a “newest BOG compressor” release describing its BOG compressor engineered for cryogenic applications (LNG logistics/vapor management) to compress evaporated LNG vapors for reinjection or energy recovery.

- In March 2025, Honeywell announced it had agreed to acquire Sundyne (a maker of highly engineered pumps and gas compressors) from Warburg Pincus for $2.16 billion in an all-cash transaction, expanding Honeywell’s equipment and services footprint in process-industry compression.

- In November 2024, Burckhardt Compression was selected to supply boil-off gas (BOG) and pipeline injection compressors for the Brunsbüttel LNG regasification terminal in Germany, positioning its equipment as part of the terminal’s LNG handling and grid-injection setup (with regular operations expected to start in 2027).

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1632.2 million |

| Revenue forecast in 2032 |

USD 2488.46 million |

| Growth rate (CAGR) |

6.21% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Type Outlook: Centrifugal, Reciprocating (Piston), Screw, Others; By Application Outlook: LNG Carriers, Onshore LNG Terminals, LNG Storage, FLNG (Floating LNG), FSRU (Floating Storage & Regasification Unit), Industrial / Others; By End-User Industry Outlook: Oil & Gas, Chemical, Power, Marine; By Orientation / Configuration Outlook: Horizontal, Vertical |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Atlas Copco; Burckhardt Compression; Siemens Energy; Baker Hughes; Elliott Group; SIAD Macchine Impianti; Hanwha Power Systems; MAN Energy Solutions; NEUMAN & ESSER Group; Howden Group; Mitsubishi Heavy Industries; Kobe Steel Ltd.; Cryostar |

| No.of Pages |

335 |

Segmentation

By Type

- Centrifugal

- Reciprocating (Piston)

- Screw

- Axial

By Application

- LNG Carriers

- Onshore LNG Terminals

- LNG Storage

- FLNG (Floating LNG)

- FSRU (Floating Storage & Regasification Unit)

- Industrial / Others

By End-User Industry

- Oil & Gas

- Chemical

- Power

- Marine

By Orientation / Configuration

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa