Natural Gas Filter Market Overview:

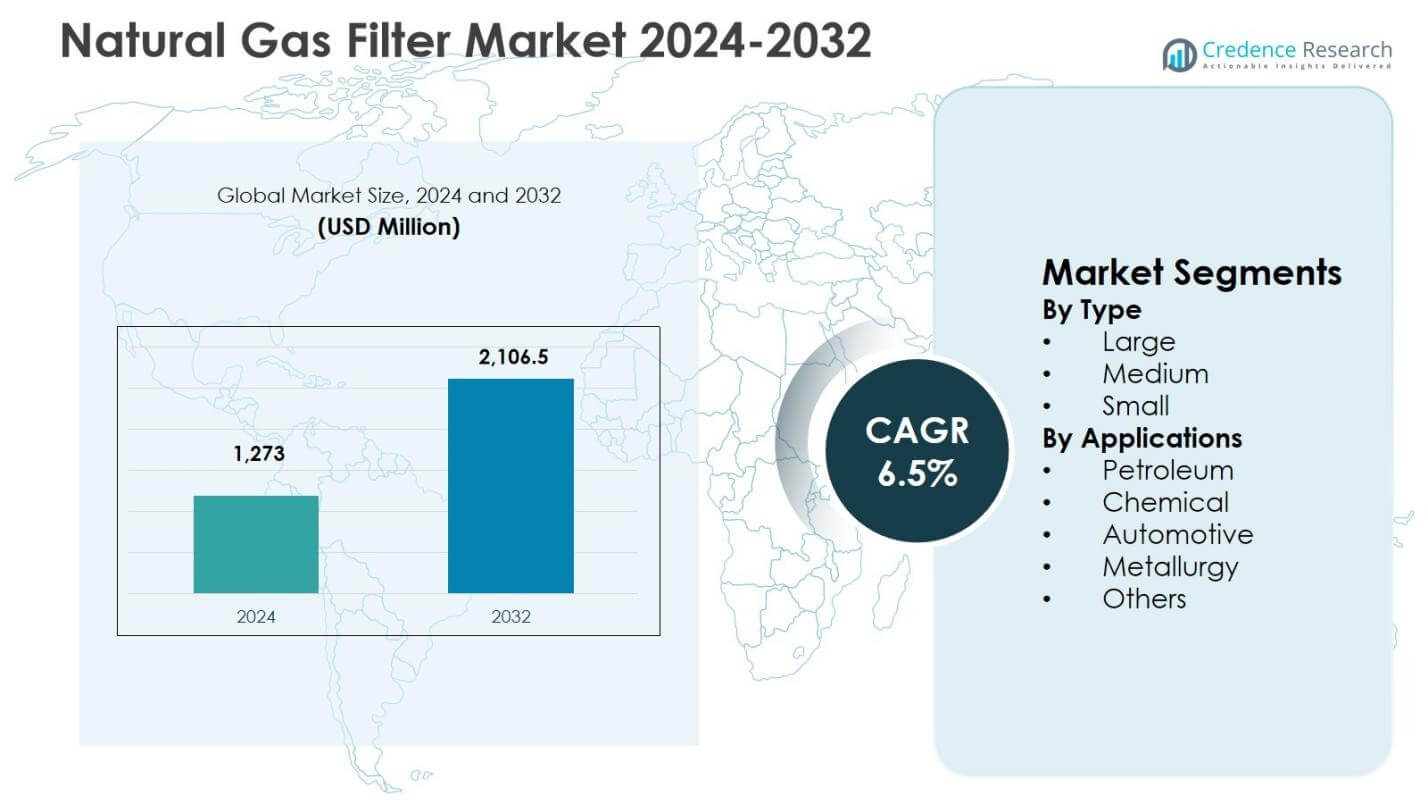

Natural Gas Filter Market size was valued at USD 1,273 million in 2024 and is anticipated to reach USD 2,106.5 million by 2032, registering a CAGR of 6.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Natural Gas Filter Market Size 2024 |

USD 1,273 million |

| Natural Gas Filter Market, CAGR |

6.5% |

| Natural Gas Filter Market Size 2032 |

USD 2,106.5 million |

Natural Gas Filter Market Insights

- Market growth is driven by expansion of natural gas pipelines, LNG terminals, and city gas distribution networks, increasing demand for filtration systems to protect compressors, turbines, and metering equipment and ensure gas quality compliance.

- Large filters dominated the market with a 2% segment share in 2024, followed by medium filters at 34.5% and small filters at 19.3%, reflecting higher adoption of high-capacity filtration systems in gas processing and transmission applications.

- Leading manufacturers focus on advanced filter media, coalescing technologies, and high-pressure systems, while cost pressures and customization complexity remain key restraints affecting adoption among small and mid-scale operators.

- North America led with 6% regional share in 2024, followed by Europe at 26.1%, Asia Pacific at 24.8%, Latin America at 8.7%, and Middle East & Africa at 5.8%, driven by infrastructure development and industrial gas usage.

Natural Gas Filter Market Segmentation Analysis:

By Type:

The Natural Gas Filter Market by type is led by Large filters, which accounted for 46.2% market share in 2024, driven by their extensive deployment in gas processing plants, transmission pipelines, and large-scale industrial facilities requiring high-capacity filtration and contaminant removal. Large filters support higher flow rates and longer service intervals, making them cost-effective for continuous operations. Medium filters held 34.5% share, supported by rising adoption across midstream infrastructure and regional distribution networks. Small filters captured 19.3% share, primarily used in localized applications and compact systems where space constraints and lower throughput requirements dominate.

- For instance, Donaldson Company provides medium pressure spin-on filters like Duramax®, rated up to 2,000 psi for in-line cartridge applications in gas processing systems, ensuring reliable performance in midstream operations with flows up to 30 gpm.

By Applications:

By application, the Petroleum segment dominated with a 38.7% market share in 2024, supported by stringent gas quality requirements across upstream, midstream, and downstream operations to protect compressors, turbines, and metering equipment. The Chemical segment followed with 24.9% share, driven by growing use of natural gas as a feedstock and fuel in process industries. Automotive applications accounted for 16.8%, supported by expanding natural gas vehicle infrastructure. Metallurgy held 11.2% share, while Others contributed 8.4%, reflecting diversified industrial usage.

- For instance, Axens supplies TEG absorption and molecular sieve solutions for chemical plants processing sweet and sour natural gases onshore and offshore. These systems handle varying CO2/H2S levels to ensure dry gas quality for reactions without corrosion risks.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Key Growth Drivers

Expansion of Natural Gas Infrastructure

The rapid expansion of global natural gas infrastructure strongly drives demand in the Natural Gas Filter Market. Rising investments in gas transmission pipelines, LNG terminals, gas storage facilities, and city gas distribution networks increase the need for high-efficiency filtration systems to remove particulates, liquids, and contaminants. Filters play a critical role in protecting compressors, turbines, meters, and valves, ensuring uninterrupted operations and reducing equipment failure. Emerging economies are accelerating pipeline development and gas grid expansion to support energy security and cleaner fuel adoption, directly stimulating sustained demand for advanced natural gas filtration solutions.

- For instance, Enbridge is expanding its Aitken Creek gas storage facility in British Columbia with a C$0.3-billion investment, adding 40 billion cubic feet of capacity to aid LNG exports like Cedar LNG.

Stringent Quality and Safety Regulations

Strict regulatory frameworks governing natural gas quality and industrial safety significantly boost market growth. Regulatory bodies mandate precise filtration standards to control moisture, solid particles, and corrosive elements before gas enters processing units or end-use systems. Compliance requirements across petroleum refining, chemical processing, power generation, and gas distribution compel operators to deploy reliable filtration systems. Increasing enforcement of safety norms and operational efficiency standards encourages upgrades from conventional filters to high-performance designs, supporting consistent replacement demand and long-term adoption across regulated industrial environments.

- For instance, Alto Garda Power upgraded their LM6000 gas turbine filtration to a 2-stage static system to meet environmental and operational regulations.

Rising Industrial Consumption of Natural Gas

Growing industrial reliance on natural gas as a primary fuel and feedstock drives the Natural Gas Filter Market. Industries such as chemicals, metallurgy, automotive manufacturing, and power generation favor natural gas due to its lower emissions, cost efficiency, and stable supply. Increased usage heightens the need for effective filtration to prevent equipment damage and maintain process efficiency. As industrial plants expand capacity and modernize systems, demand for durable and high-capacity filters rises, reinforcing steady market growth across both developed and developing industrial regions.

Key Trends & Opportunities

Technological Advancements in Filtration Systems

Continuous innovation in filtration technologies creates significant growth opportunities in the Natural Gas Filter Market. Manufacturers increasingly develop high-efficiency coalescing filters, advanced media materials, and multi-stage filtration systems capable of handling higher pressures and flow rates. Smart monitoring features integrated with sensors and predictive maintenance tools enhance operational reliability and reduce downtime. These advancements allow end users to optimize performance, extend filter life, and lower maintenance costs, making technologically advanced filtration solutions increasingly attractive across large-scale and midstream applications.

- For instance, Parker Hannifin’s P3X and Finite series filters utilize advanced microfiber coalescing elements that achieve up to 99.99% removal efficiency for oil aerosols and particulates, even in demanding gas processing environments.

Growth of LNG and Clean Energy Transition

The expanding liquefied natural gas sector and the global shift toward cleaner energy sources present strong opportunities for market expansion. LNG processing and transportation require stringent filtration to maintain gas purity and protect sensitive cryogenic equipment. Simultaneously, government initiatives promoting natural gas as a transition fuel accelerate investments in gas-based power plants and distribution networks. This trend increases demand for specialized filtration systems, positioning the Natural Gas Filter Market to benefit from long-term clean energy and decarbonization strategies.

- For instance, Filtration Group supplied PuraGrid carbon filters and Drop Safe moisture barrier prefilters to CYDSA’s co-generation power plant, eliminating over 90% of contaminants and raising uptime to 92-94% from prior failures.

Key Challenges

High Installation and Maintenance Costs

High initial installation and ongoing maintenance costs pose a notable challenge for the Natural Gas Filter Market. Advanced filtration systems require specialized materials, precision engineering, and regular replacement of filter elements, increasing total ownership costs. Small and mid-scale operators often face budget constraints, limiting adoption of high-performance filters. Additionally, maintenance downtime during filter replacement can impact operational efficiency, prompting end users to delay upgrades or opt for lower-cost alternatives, which may restrict market penetration in cost-sensitive regions.

Operational Complexity and Customization Requirements

The need for application-specific customization creates operational challenges for filter manufacturers and end users. Natural gas composition varies significantly across sources and regions, requiring tailored filtration solutions to address specific contaminants. Designing and deploying customized systems increases engineering complexity and lead times. Improper filter selection or integration can result in performance inefficiencies and equipment damage. These challenges demand strong technical expertise and collaboration, which can slow decision-making and adoption, particularly among operators lacking in-house technical capabilities.

Regional Analysis

North America

North America held 34.6% market share in 2024, supported by extensive natural gas production, mature pipeline networks, and high adoption of advanced filtration technologies. Strong shale gas activities across the United States and Canada drive consistent demand for natural gas filters to protect compressors, turbines, and metering systems. Stringent safety and gas quality regulations further reinforce filter replacement and upgrade cycles. The region also benefits from high investments in LNG export terminals and gas-fired power plants, sustaining demand for large-capacity and high-efficiency filtration systems across upstream, midstream, and downstream operations.

Europe

Europe accounted for 26.1% market share in 2024, driven by strict environmental regulations and growing focus on energy security. Countries across Western and Northern Europe emphasize gas quality compliance to support industrial processes, power generation, and residential distribution networks. Expansion of LNG import infrastructure and cross-border pipeline interconnections increases filtration demand across transmission systems. Industrial sectors such as chemicals, metallurgy, and manufacturing further contribute to steady adoption. Continuous modernization of aging gas infrastructure and strong regulatory enforcement support sustained demand for reliable and high-performance natural gas filtration solutions across the region.

Asia Pacific

Asia Pacific captured 24.8% market share in 2024, reflecting rapid industrialization, urban expansion, and increasing natural gas consumption. Countries such as China, India, Japan, and South Korea are expanding gas distribution networks and LNG import capacity to meet rising energy demand. Industrial growth across chemicals, automotive manufacturing, and metallurgy increases the need for effective filtration to ensure operational efficiency. Government initiatives promoting cleaner fuels accelerate gas-based power generation and city gas projects, strengthening demand for natural gas filters across large, medium, and small-scale installations throughout the region.

Latin America

Latin America represented 8.7% market share in 2024, supported by expanding gas exploration and infrastructure development in countries such as Brazil, Argentina, and Mexico. Growth in offshore gas production and pipeline expansion projects drives demand for filtration systems to maintain gas quality and equipment reliability. Industrial applications across petroleum refining and chemicals further support market growth. Increasing investments in gas-fired power plants and regional energy diversification strategies enhance adoption. However, market expansion remains influenced by investment cycles and regulatory stability across individual countries within the region.

Middle East & Africa

The Middle East & Africa held 5.8% market share in 2024, driven by large-scale natural gas production and processing activities. Countries across the Middle East focus on gas processing, LNG exports, and industrial diversification, creating strong demand for high-capacity filtration systems. Filtration plays a critical role in protecting processing equipment under harsh operating conditions. In Africa, gradual expansion of gas infrastructure and power generation projects supports steady growth. Ongoing investments in upstream and midstream developments continue to drive long-term demand across the region.

Natural Gas Filter Market Segmentations:

By Type

By Applications

- Petroleum

- Chemical

- Automotive

- Metallurgy

- Others

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

Competitive landscape of the Natural Gas Filter Market is characterized by the presence of Parker Hannifin Corporation, Donaldson Company, Inc., MANN+HUMMEL Group, Camfil AB, Filtration Group Corporation, Eaton Corporation plc, Honeywell International Inc., AAF International, Pall Corporation, and 3M Company. The market remains moderately consolidated, with leading players focusing on product reliability, filtration efficiency, and lifecycle performance to strengthen their positions. Companies invest heavily in advanced filter media, coalescing technologies, and high-pressure filtration systems to address evolving gas quality standards across upstream, midstream, and downstream operations. Strategic initiatives such as capacity expansion, product customization, and long-term supply contracts with gas processors and pipeline operators enhance competitive strength. Regional players compete through cost-effective solutions and localized service support, while global manufacturers leverage strong distribution networks and technical expertise. Continuous innovation, compliance with safety regulations, and aftermarket service capabilities remain critical factors shaping competition in the global market.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Recent Developments

- In October 2025, Cleanova launched its new PFAS-Free Media Coalescing Filters, offering high-efficiency gas and compressed air filtration with an environmentally friendly PFAS-free construction, marking a notable sustainable product introduction in gas filtration technology.

- In October 2025, Desco Infratech Limited signed an MoU with KPI Green Hydrogen and Ammonia Pvt. Ltd. and Naveriya Gas Pvt. Ltd. to launch India’s first Hydrogen-Natural Gas Blending Projects in the city gas distribution sector, indicating a strategic partnership toward cleaner gas applications.

- In January 2025, Rensa Filtration acquired Air Filtration Co., Inc., expanding its operations in California and Iowa with a focus on air filter products for industrial markets including those relevant to natural gas applications.

- In July 2024, Cleanova acquired Sidco Filter Company and Shawndra Products Inc., strengthening its position in clean tech filtration for air and gas markets, including natural gas wellheads and pipelines.

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will benefit from continued expansion of natural gas pipelines and transmission infrastructure across developed and emerging regions.

- Rising investments in LNG processing, storage, and export facilities will support sustained demand for high-efficiency filtration systems.

- Stricter gas quality and safety regulations will accelerate replacement and upgrade cycles for existing filtration installations.

- Industrial shift toward cleaner fuels will increase natural gas usage across chemicals, metallurgy, and manufacturing sectors.

- Technological advancements will improve filter media efficiency, durability, and performance under high-pressure conditions.

- Adoption of smart filtration systems with monitoring and predictive maintenance capabilities will increase across large-scale operations.

- Growth in city gas distribution networks will expand demand for medium and small-capacity filters.

- Increasing focus on equipment protection and reduced downtime will drive preference for premium filtration solutions.

- Emerging economies will witness faster adoption due to industrialization and energy infrastructure development.

- Strategic collaborations and product customization will strengthen supplier relationships with gas operators and utilities.