| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Neurosurgery Devices Market Size 2024 |

USD 12,543.23 Million |

| Neurosurgery Devices Market, CAGR |

10.16% |

| Neurosurgery Devices Market Size 2032 |

USD 27,041.46 Million |

Market Overview:

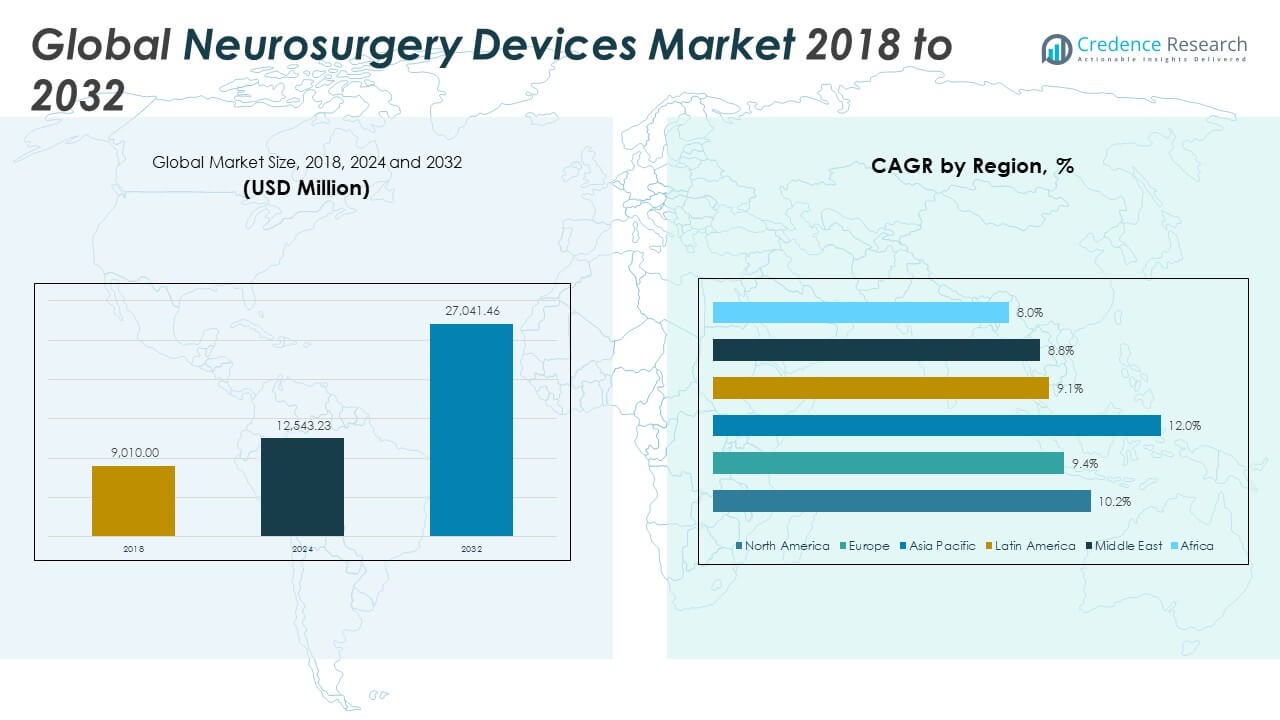

The Global Neurosurgery Devices Market size was valued at USD 9,010.00 million in 2018 to USD 12,543.23 million in 2024 and is anticipated to reach USD 27,041.46 million by 2032, at a CAGR of 10.16% during the forecast period.

Key drivers accelerating growth include the rising prevalence of neurological conditions such as brain tumors, epilepsy, Parkinson’s disease, and spinal cord injuries. As life expectancy increases and the global population ages, the incidence of such disorders continues to rise, prompting higher demand for precise and effective neurosurgical interventions. Technological advancements—particularly in neuroendoscopy, deep brain stimulation (DBS), stereotactic navigation, and robotic-assisted surgery—are transforming neurosurgical care, enhancing precision, and reducing complication rates. The industry is also benefiting from the increasing adoption of minimally invasive procedures that shorten recovery times and improve patient outcomes. Continued regulatory approvals, product innovations, and expanded access to advanced devices are further contributing to the market’s growth trajectory.

Regionally, North America dominates the neurosurgery devices market, accounting for over half of the global revenue. The region benefits from a robust healthcare infrastructure, high incidence of neurological disorders, and strong reimbursement frameworks. The United States remains the largest contributor, driven by advanced surgical capabilities and high investment in R&D. Europe holds the second-largest share, supported by favorable healthcare systems and increased adoption of neuromodulation therapies. Countries like Germany, France, and the UK are at the forefront of neurotechnology integration. Meanwhile, the Asia-Pacific region is experiencing the fastest growth, fueled by expanding healthcare infrastructure, rising patient awareness, and increased government spending in countries like China, India, and Japan. Latin America, the Middle East, and Africa are gradually emerging as potential markets due to improving access to specialized care and growing investments in medical technology.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The market size was valued at USD 9,010.00 million in 2018, reached USD 12,543.23 million in 2024, and is projected to grow to USD 27,041.46 million by 2032, registering a CAGR of 10.16% during 2024–2032.

- The increasing prevalence of neurological conditions such as brain tumors, epilepsy, Parkinson’s disease, and spinal cord injuries is driving global demand for neurosurgical interventions, especially among the aging population.

- Advancements in neuroendoscopy, stereotactic navigation, robotic-assisted surgery, and intraoperative imaging are enabling safer, more precise, and minimally invasive procedures that reduce complication rates and improve recovery times.

- The growing adoption of neuromodulation devices, including deep brain stimulation (DBS) and spinal cord stimulation (SCS), is improving treatment outcomes for chronic and treatment-resistant neurological disorders like essential tremor, Parkinson’s disease, and chronic pain.

- North America accounts for over 50% of global revenue, led by the United States, due to advanced surgical capabilities, high R&D spending, and robust reimbursement frameworks; Europe ranks second, with strong adoption in Germany, France, and the UK.

- The high cost of devices like robotic surgery systems, intraoperative imaging units, and navigation platforms, combined with budget constraints and limited neurosurgical infrastructure, restrict adoption in low- and middle-income countries, especially in Latin America, Africa, and parts of Asia.

- Regulatory approval processes in markets like the U.S., EU, and Japan involve long timelines, high clinical trial costs, and post-market surveillance, increasing the risk of product recalls, financial losses, and delayed commercialization for neurosurgery device manufacturers.

Market Drivers:

Rising Burden of Neurological Disorders is Driving Demand for Advanced Surgical Interventions:

The growing prevalence of neurological conditions, including traumatic brain injuries, brain tumors, epilepsy, Parkinson’s disease, and spinal cord disorders, is a primary driver of the Global Neurosurgery Devices Market. Increasing life expectancy and aging populations are contributing to a higher incidence of these disorders worldwide. Neurological diseases often require precise and complex interventions, which are facilitated by advanced neurosurgical devices. Public health systems and private providers are responding by expanding neurosurgical services to meet demand. The market is also seeing growing procedural volumes in developed and emerging economies. This surge in neurological cases is generating sustained demand for innovative tools and technologies that improve outcomes and reduce surgical risks.

- For instance, according to a 2021 study published by The Lancet Neurology and the World Health Organization, more than 3 billion people globally were living with a neurological condition, representing over one-third of the world’s population.

Technological Advancements in Minimally Invasive and Image-Guided Surgery Are Enhancing Market Value:

Advancements in neurosurgical technology, including robotics, neuroendoscopy, stereotactic navigation, and intraoperative imaging, are significantly improving the precision and safety of neurosurgical procedures. Surgeons are increasingly favoring minimally invasive techniques that allow for smaller incisions, faster recovery, and lower complication rates. The integration of real-time imaging systems with surgical navigation platforms is enabling more accurate localization of lesions and better tissue preservation. It is supporting the shift from traditional open surgeries toward advanced neuromodulation and minimally invasive methods. These innovations are expanding the range of treatable conditions while enhancing patient satisfaction. The Global Neurosurgery Devices Market is benefiting from continuous innovation in both hardware and software systems that improve clinical decision-making and surgical efficiency.

- For instance, Brainlab’s Curve™ Image Guided Surgery platform has been adopted in more than 5,600 hospitals, enabling surgeons to perform precise navigation with sub-millimeter accuracy during cranial and spinal procedures.

Increasing Adoption of Neuromodulation Devices for Chronic Neurological Conditions;

The adoption of neuromodulation technologies, such as deep brain stimulation (DBS) and spinal cord stimulation (SCS), is accelerating due to their effectiveness in managing chronic and treatment-resistant neurological disorders. These devices offer non-pharmacological alternatives for patients with Parkinson’s disease, essential tremor, chronic pain, and certain psychiatric conditions. Growing clinical evidence and favorable regulatory approvals are supporting the expansion of these therapies across new indications. It is also leading to increased investments from both established manufacturers and new entrants focused on developing next-generation stimulation systems. Patients and providers are recognizing the long-term therapeutic benefits and reduced side effect profiles associated with neuromodulation. This trend is significantly contributing to the growth and diversification of the neurosurgery devices market.

Supportive Healthcare Infrastructure and Reimbursement Systems in Developed Markets:

Established healthcare systems in North America and Europe are creating favorable conditions for the adoption of advanced neurosurgery devices. High awareness, strong surgical expertise, and availability of specialized facilities support early uptake of new technologies. Reimbursement policies in countries such as the United States, Germany, and Japan are facilitating patient access to costly procedures like DBS and neuro-navigation-guided surgeries. It enables faster market penetration for high-value devices. Health systems are prioritizing capital equipment that delivers measurable improvements in clinical outcomes. Strategic collaborations between device manufacturers and hospitals are also boosting technology deployment across high-volume surgical centers. These dynamics continue to reinforce the leadership of developed markets in driving global neurosurgery innovation.

Market Trends:

Integration of Artificial Intelligence and Machine Learning into Surgical Workflows:

Artificial intelligence (AI) and machine learning (ML) are transforming neurosurgical planning, intraoperative navigation, and post-operative analysis. These technologies help surgeons predict procedural risks, model brain functions, and identify optimal surgical paths using preoperative imaging data. AI-powered platforms are improving precision in tumor resection and deep brain stimulation targeting. It enables real-time decision support during critical procedures and enhances the safety of complex interventions. The Global Neurosurgery Devices Market is witnessing increasing adoption of AI-integrated software solutions that align with robotic systems and imaging tools. Hospitals are investing in AI-enabled neurosurgical systems to support data-driven clinical decision-making and boost patient outcomes.

- For instance, AI-based diagnostic tools developed by companies like Aidoc have achieved median diagnostic accuracies above 91% in neuro-oncology applications, such as tumor identification.

Expansion of Single-Use and Disposable Neurosurgical Instruments:

Surgeons and hospitals are shifting toward sterile, single-use neurosurgical tools to reduce cross-contamination and lower reprocessing costs. The demand for disposable devices is rising in procedures involving cerebrospinal fluid drainage, stereotactic biopsies, and spinal fusion. These tools offer consistent performance, eliminate the risk of instrument degradation, and support operating room efficiency. It reflects a broader shift toward infection control and cost-effective surgical management in both developed and emerging markets. Manufacturers are developing disposable variants of high-precision instruments such as cranial drills, catheters, and shunts. The Global Neurosurgery Devices Market is gaining from increased preference for single-use solutions in outpatient and ambulatory surgical settings.

- For instance, Xenco Medical’s single-use spinal surgery kits have been shown to reduce postoperative infection rates by nearly eliminating instrument-related contamination, with peer-reviewed studies attributing 15-20% of postoperative infections to sterilization failures in reusable instruments.

Growth of Ambulatory Neurosurgery and Day-Care Surgical Centers:

There is a growing trend toward performing neurosurgical procedures in ambulatory and outpatient environments, particularly for minimally invasive and image-guided interventions. Patients and providers favor these settings for lower costs, faster discharge, and reduced hospital-acquired infection risks. Advances in anesthesia, portable imaging, and compact neurosurgical devices support this migration. It is prompting hospitals to invest in mobile surgical units and lightweight equipment optimized for short-stay use. The Global Neurosurgery Devices Market is adapting to this trend with compact, modular systems that fit ambulatory care requirements. Device manufacturers are redesigning platforms to support rapid setup, mobility, and ease of integration into smaller surgical suites.

Personalization of Neurosurgical Solutions Through Patient-Specific Technologies:

The market is witnessing a rise in demand for patient-specific neurosurgical planning tools and implantable devices. Advances in 3D printing and imaging technologies are enabling the customization of cranial implants, spinal hardware, and surgical guides tailored to each patient’s anatomy. It enhances implant fit, reduces operative time, and improves clinical outcomes in complex procedures. Surgeons are increasingly relying on patient-specific navigation templates for tumor resections and reconstructive surgeries. The Global Neurosurgery Devices Market is responding to this trend with greater investment in personalized device portfolios and digital modeling tools. Customization is becoming a key competitive differentiator among leading neurosurgical technology providers.

Market Challenges Analysis:

High Cost of Devices and Limited Access in Low-Income Regions:

The high capital investment required for neurosurgery devices presents a significant barrier to adoption, particularly in low- and middle-income countries. Advanced systems such as robotic-assisted surgery, intraoperative imaging, and neuronavigation demand substantial upfront costs and ongoing maintenance. Many hospitals in resource-constrained settings lack the financial capacity to procure and maintain such equipment. The Global Neurosurgery Devices Market reflects an uneven distribution of access, with most high-end technologies concentrated in developed economies. This disparity limits the reach of life-saving interventions to underserved populations. Public healthcare systems in developing regions struggle to integrate cutting-edge tools into routine neurosurgical care due to budgetary constraints and limited skilled personnel.

Stringent Regulatory Approval Processes and Product Recall Risks:

Securing regulatory approval for neurosurgery devices involves complex clinical validation and long lead times, particularly in regions like the U.S., EU, and Japan. Companies must conduct extensive trials to meet safety and efficacy benchmarks, delaying product launches and increasing development costs. Regulatory bodies often require post-market surveillance, adding compliance burdens on manufacturers. It also raises the risk of product recalls if safety concerns arise after commercialization. The Global Neurosurgery Devices Market faces reputational and financial setbacks when device failures or adverse events occur. Companies must invest in robust quality management systems to mitigate regulatory risks and maintain long-term credibility in competitive global markets.

Market Opportunities:

Rising Investment in Emerging Markets and Expanding Healthcare Infrastructure:

Emerging economies are creating substantial opportunities for manufacturers to expand their presence and address underserved neurosurgical needs. Countries across Asia-Pacific, Latin America, and the Middle East are investing in healthcare infrastructure and upgrading surgical capabilities. Governments and private hospitals are allocating resources for advanced operating rooms, training programs, and diagnostic technologies. The Global Neurosurgery Devices Market can benefit from this momentum by offering cost-effective, scalable solutions tailored to regional needs. Local manufacturing, distributor partnerships, and technology transfer initiatives can accelerate device penetration. Growth in medical tourism and international collaboration further supports expansion across developing markets.

Innovation in Smart Implants and AI-Enabled Surgical Tools:

The development of smart implants and AI-integrated surgical tools is opening new avenues for personalized and data-driven neurosurgery. Smart neurostimulation systems with adaptive feedback capabilities are gaining attention for improving clinical outcomes. Companies are exploring bioresorbable implants, wireless brain monitoring, and AI-guided planning systems to enhance therapeutic precision. It allows surgeons to optimize treatment strategies in real time while reducing procedural variability. The Global Neurosurgery Devices Market stands to gain from increasing demand for connected devices that integrate seamlessly with hospital IT systems and electronic health records. These innovations create long-term opportunities for differentiation and value-added care.

Market Segmentation Analysis:

By Product Type

Neurostimulation devices dominate the segment due to their clinical success in treating Parkinson’s disease, chronic pain, and tremors. Neurointerventional devices are increasingly used in the treatment of stroke and aneurysms, supported by advancements in catheter-based technologies. Neurosurgical navigation systems improve surgical accuracy and patient safety, making them essential in complex cranial and spinal procedures. Cerebral Spinal Fluid (CSF) management devices remain crucial for hydrocephalus and traumatic brain injury care. The “others” segment includes supportive and emerging tools aiding neurosurgical outcomes.

- For instance, the NeuroPace RNS® System has demonstrated a 75% median reduction in seizure frequency over nine years in adults with focal epilepsy, with a 73% responder rate and 35% of patients experiencing at least a 90% reduction in seizures.

By Application

Spinal cord stimulation holds the largest share, driven by the growing prevalence of chronic pain, failed back surgery syndrome, and ischemia. Deep brain stimulation is widely used in the management of Parkinson’s disease, tremors, depression, and other neurological disorders. Neuroendoscopy procedures—including transnasal, intraventricular, and transcranial techniques—are expanding rapidly due to the shift toward minimally invasive interventions that reduce recovery time and surgical trauma.

- For instance, utilization of spinal cord stimulation trials in the U.S. Medicare population increased by 186% from 2009 to 2018, with the number of pulse generator implants rising from 7,640 to 22,960 over the same period.

By End-user

Hospitals lead the market with their capacity for complex neurosurgical procedures, availability of advanced equipment, and presence of skilled neurosurgeons. Ambulatory surgical centers are experiencing increased adoption due to faster procedural throughput and reduced patient costs. The “others” category includes specialized neurological clinics and research institutes focusing on clinical innovation and academic study.

Segmentation:

By Product Type:

- Neurostimulation Devices

- Neurointerventional Devices

- Neurosurgical Navigation Systems

- Cerebral Spinal Fluid (CSF) Management Devices

- Others

By Application:

- Spinal Cord Stimulation

- Chronic Pain

- Failed Back Surgery Syndrome

- Ischemia

- Deep Brain Stimulation

- Parkinson’s Disease

- Tremor

- Depression

- Others

- Neuroendoscopy

- Transnasal Neuroendoscopy

- Intraventricular Neuroendoscopy

- Transcranial Neuroendoscopy

By End-user:

- Hospitals

- Ambulatory Surgical Centers

- Others

By Region:

- North America (U.S., Canada, Mexico)

- Europe (UK, France, Germany, Italy, Spain, Russia, Rest of Europe)

- Asia Pacific (China, Japan, South Korea, India, Australia, Southeast Asia, Rest of Asia Pacific)

- Latin America (Brazil, Argentina, Rest of Latin America)

- Middle East (GCC Countries, Israel, Turkey, Rest of Middle East)

- Africa (South Africa, Egypt, Rest of Africa)

Regional Analysis:

North America

The North America Neurosurgery Devices Market size was valued at USD 3,838.26 million in 2018 to USD 5,288.15 million in 2024 and is anticipated to reach USD 11,387.21 million by 2032, at a CAGR of 10.2% during the forecast period. North America holds the largest share of the Global Neurosurgery Devices Market, accounting for over 42% of global revenue. It benefits from advanced healthcare infrastructure, high procedural volume, and strong reimbursement systems. The United States leads the region due to rapid adoption of neuromodulation, neuronavigation, and robotic-assisted surgeries. Canada and Mexico are also expanding their neurosurgical capabilities through public-private investments. Hospitals in this region continue to implement cutting-edge technologies across a broad range of neurological disorders. It maintains global leadership in neurosurgical innovation and clinical excellence.

Europe

The Europe Neurosurgery Devices Market size was valued at USD 2,563.35 million in 2018 to USD 3,440.27 million in 2024 and is anticipated to reach USD 7,037.61 million by 2032, at a CAGR of 9.4% during the forecast period. Europe accounts for approximately 27% of the Global Neurosurgery Devices Market. Germany, France, and the UK lead the region with strong clinical infrastructure and widespread technology adoption. The growing aging population is increasing the demand for treatments targeting Parkinson’s disease, spinal disorders, and brain tumors. Hospitals are integrating neuronavigation, endoscopy, and intraoperative imaging systems to enhance surgical outcomes. Government-backed health programs and clinical research initiatives support market growth. It remains a key center for neuromodulation and image-guided surgery adoption.

Asia Pacific

The Asia Pacific Neurosurgery Devices Market size was valued at USD 1,511.88 million in 2018 to USD 2,240.80 million in 2024 and is anticipated to reach USD 5,546.23 million by 2032, at a CAGR of 12.0% during the forecast period. Asia Pacific is the fastest-growing region, representing about 18% of the Global Neurosurgery Devices Market. Rapid urbanization, growing patient awareness, and increasing government healthcare spending drive demand for neurosurgical procedures. China, India, and Japan are key contributors, with rising investments in medical technology and specialized neurology centers. Private hospital chains are expanding high-end neurosurgical services in metro cities. Robotic systems and neuronavigation tools are being deployed in advanced care settings. It presents strong growth potential across both therapeutic and diagnostic neurosurgical segments.

Latin America

The Latin America Neurosurgery Devices Market size was valued at USD 520.78 million in 2018 to USD 717.35 million in 2024 and is anticipated to reach USD 1,424.27 million by 2032, at a CAGR of 9.1% during the forecast period. Latin America accounts for around 6% of the Global Neurosurgery Devices Market. Brazil dominates regional adoption, supported by urban healthcare expansion and large public hospital networks. Argentina, Colombia, and Chile are increasing access to neurosurgical care through national health initiatives. Equipment shortages and limited clinical expertise in rural areas restrict broader market reach. Hospitals in major cities are adopting neuronavigation and endoscopy systems for complex procedures. It is gradually advancing toward improved access and affordability in neurosurgical services.

Middle East

The Middle East Neurosurgery Devices Market size was valued at USD 348.69 million in 2018 to USD 455.24 million in 2024 and is anticipated to reach USD 887.11 million by 2032, at a CAGR of 8.8% during the forecast period. The Middle East contributes about 4% to the Global Neurosurgery Devices Market. GCC countries such as Saudi Arabia and the UAE are building advanced neurological centers with imported high-end systems. Israel leads in medical research and robotic surgery adoption. The demand for spinal and cranial neurosurgical procedures is growing with increased awareness and investment. Some countries still face gaps in equipment access and specialist availability. It is moving toward improved regional coverage and technology integration through strategic healthcare investments.

Africa

The Africa Neurosurgery Devices Market size was valued at USD 227.05 million in 2018 to USD 401.43 million in 2024 and is anticipated to reach USD 759.03 million by 2032, at a CAGR of 8.0% during the forecast period. Africa holds under 3% of the Global Neurosurgery Devices Market. South Africa leads in technology adoption and surgical capabilities. Egypt and Nigeria are expanding neurosurgical units in public hospitals, often supported by international aid and partnerships. Most of the continent lacks neurosurgical infrastructure, trained professionals, and high-end equipment. Market growth is concentrated in urban centers with access to tertiary care. It shows emerging potential for basic to mid-level neurosurgical systems, backed by rising government and non-profit engagement.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Abbott Laboratories

- Ackermann Instrumente GmbH

- Adeor Medical AG

- Braun Melsungen AG

- Biotronik

- Boston Scientific Corporation

- DePuy Synthes Inc.

- Integra LifeSciences Corporation

- Johnson & Johnson Services Inc.

- Medtroic Plc

- Nevro Corporation

- Nihon Kohden Corporation

- Penumbra Inc.

- Stryker Corporation

Competitive Analysis:

The Global Neurosurgery Devices Market features a competitive landscape driven by continuous innovation, strategic partnerships, and a strong focus on precision technologies. Leading players such as Medtronic, Stryker, Boston Scientific, Johnson & Johnson, and B. Braun Melsungen dominate the market through diversified product portfolios, global distribution networks, and ongoing R&D investments. It remains highly competitive, with emerging companies introducing advanced tools in neurostimulation, robotics, and navigation. Companies are actively pursuing regulatory approvals and geographic expansion to strengthen market presence. Mergers, acquisitions, and collaborations with hospitals and research institutions are common strategies to accelerate product development and clinical adoption. The market also sees increasing focus on AI integration and patient-specific solutions to differentiate offerings and capture untapped segments.

Recent Developments:

- In July 2025, Ackermann Instrumente GmbH announced that healthcare investor SHS Capital had acquired a majority stake in the company. This acquisition is part of a strategy to form a leading MedTech group by expanding Ackermann’s core business and pursuing further partnerships and acquisitions. The move is expected to strengthen Ackermann’s global presence in surgical instruments, including those used in neurosurgery.

- In April 2025, Abbott Laboratories launched a next-generation delivery system for its Proclaim™ DRG neurostimulation system. This new system is designed to streamline the implantation process for electrodes in patients suffering from complex regional pain syndrome (CRPS) Type 1 and causalgia (CRPS Type 2) of the lower extremities. The innovation aims to make the procedure more efficient and improve patient outcomes by targeting pain signals at the dorsal root ganglion.

- In April 2025, B. Braun Melsungen AG launched the EZCOVER® Probe Cover Set, designed to improve ultrasound safety in peripheral nerve block procedures. While primarily focused on anesthesia, this product supports safer neurosurgical interventions by enhancing infection control and procedural efficiency in nerve-related surgeries.

- In March 2025, Boston Scientific Corporation announced an agreement to acquire SoniVie Ltd., a medical device company specializing in the TIVUS™ Intravascular Ultrasound System. This acquisition expands Boston Scientific’s interventional portfolio with a minimally invasive therapy for hypertension, which is closely linked to neurological health and stroke risk. The acquisition is valued at an upfront payment of approximately $360 million, plus potential milestone payments.

Market Concentration & Characteristics:

The Global Neurosurgery Devices Market exhibits moderate to high market concentration, with a few multinational companies holding significant shares due to strong brand recognition, regulatory expertise, and expansive distribution networks. It is characterized by rapid technological innovation, high entry barriers, and a strong emphasis on clinical efficacy and safety. Product differentiation through AI integration, robotic assistance, and minimally invasive solutions drives competition. The market favors companies with robust R&D capabilities, strategic partnerships, and access to advanced manufacturing. Demand remains concentrated in developed regions, but emerging markets are gaining traction due to rising investments in healthcare infrastructure. It continues to evolve with a focus on precision, personalization, and real-time surgical guidance.

Report Coverage:

The research report offers an in-depth analysis based on product type, application, and end-user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global incidence of neurological disorders will sustain long-term demand for neurosurgical devices.

- Expansion of AI and machine learning will enhance precision and decision-making in complex procedures.

- Adoption of robotic-assisted surgery is expected to increase across high-volume neurosurgical centers.

- Growing preference for outpatient and ambulatory procedures will drive demand for portable and modular systems.

- Emerging markets will offer growth potential through improved infrastructure and increased healthcare spending.

- Innovation in bioresorbable and smart implants will open new therapeutic possibilities.

- Regulatory approvals for novel neurostimulation devices will broaden clinical indications and user adoption.

- Integration with hospital IT systems will support data-driven, connected surgical environments.

- Strategic partnerships between medtech firms and academic institutions will accelerate R&D pipelines.

- Demand for personalized surgical planning and 3D-printed implants will shape the next wave of product development.