Arthroscopy Devices Market Overview:

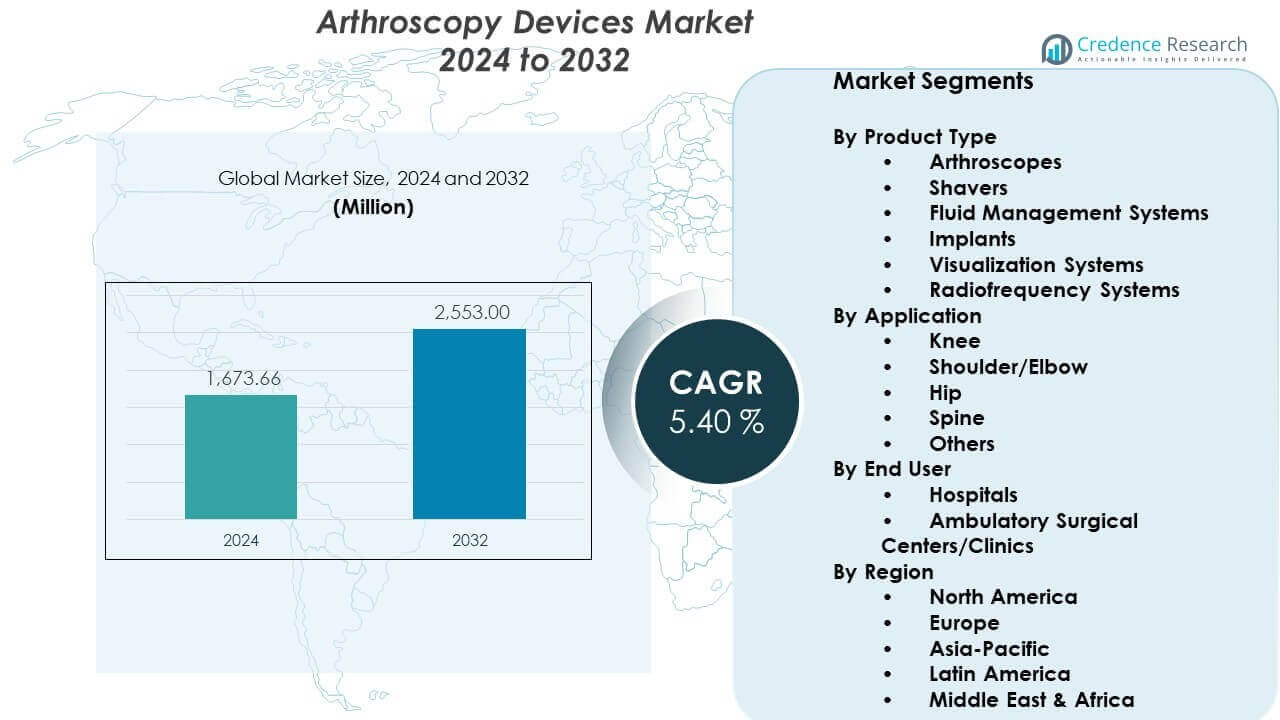

The Arthroscopy Devices Market is projected to grow from USD 1673.66 million in 2024 to an estimated USD 2553 million by 2032, with a compound annual growth rate (CAGR) of 5.40% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Arthroscopy Devices Market Size 2024 |

USD 1673.66 million |

| Arthroscopy Devices Market, CAGR |

5.40% |

| Arthroscopy Devices Market Size 2032 |

USD 2553 million |

Market drivers center on rising cases of sports injuries, osteoarthritis, and trauma-related joint issues, which push healthcare providers to adopt advanced arthroscopic tools. Surgeons prefer minimally invasive methods because these systems reduce surgical complications, increase procedural precision, and support faster patient mobility. Leading companies expand their portfolios with 4K and 3D imaging platforms, flexible scopes, and energy devices to meet the growing need for efficiency in operating rooms. Hospitals also upgrade equipment to improve diagnostic accuracy and treatment reliability.

North America leads the global Arthroscopy Devices Market due to strong orthopedic procedure volumes, an established hospital network, and rapid integration of advanced surgical systems. Europe follows, supported by favorable reimbursement structures and steady demand for minimally invasive orthopedic interventions. Asia Pacific emerges as the fastest-growing region, driven by rising healthcare investments, expanding medical tourism, and growing awareness about early joint treatment. Countries in Latin America and the Middle East show increasing adoption as healthcare infrastructure modernizes and access to specialized orthopedic care improves.

Arthroscopy Devices Market Insights:

- The Arthroscopy Devices Market is projected to grow from USD 1673.66 million in 2024 to USD 2553 million by 2032, advancing at a 5.40% CAGR, driven by rising minimally invasive orthopedic procedures and steady technology adoption.

- North America holds 40% of the market due to high procedure volumes and strong adoption of advanced surgical systems; Europe accounts for 30% supported by established orthopedic networks; Asia-Pacific captures 20% with rapid investment in healthcare modernization.

- Asia-Pacific is the fastest-growing region with a 20% share, supported by expanding orthopedic capacity, higher sports injury incidence, and broader access to advanced visualization systems.

- Knee applications represent about 45% of total procedure usage, supported by high sports-related injury rates and strong demand for ligament repair and reconstruction.

- Hospitals account for nearly 70% of overall device utilization due to broader caseloads, advanced imaging access, and higher adoption of integrated arthroscopy towers.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Arthroscopy Devices Market Drivers:

Rising Procedure Volumes and Expanding Demand for Minimally Invasive Joint Interventions

The Arthroscopy Devices Market grows due to rising joint disorder cases and wider use of minimally invasive procedures. Surgeons prefer these tools because they improve accuracy and reduce recovery periods. Hospitals invest in upgraded scopes to support complex orthopedic needs. Sports injury cases push higher adoption across major care centers. Younger patients seek faster recovery paths, which strengthens demand. It encourages manufacturers to design integrated visualization systems. Clinicians value systems that provide real-time clarity during surgery. Many providers report steady gains in arthroscopy volumes each year.

- For instance, Arthrex’s NanoScope system utilizes a 1.9 mm chip-on-tip camera technology, which has enabled a shift toward needle arthroscopy in physician offices, allowing for diagnostic procedures that take less than 20 minutes and eliminate the need for general anesthesia.

Advancements in Imaging Platforms That Improve Diagnostic and Surgical Precision

High-definition imaging innovations strengthen the Arthroscopy Devices Market by improving joint assessment quality. Surgeons depend on sharper visuals to guide complex procedures. Manufacturers invest in 4K workflows that support precision-driven decisions in operating rooms. It allows clinicians to detect micro-tears with greater accuracy. Compact camera heads give surgeons better maneuverability during fast-paced cases. Integrated light systems offer stable brightness across tight joint spaces. Hospitals report better outcomes with advanced visualization packages. Growing demand for clarity encourages higher adoption across mid-sized care facilities.

- For instance, Stryker’s 1688 AIM 4K Platform features a 32-inch monitor with 4K resolution and fluorescence imaging capabilities, allowing surgeons to visualize blood flow and critical anatomy in real-time with 4 times the pixel density of standard HD systems.

Growing Preference for Day-Care Orthopedic Procedures Across Expanding Hospital Networks

Outpatient orthopedic centers support the Arthroscopy Devices Market by enabling faster scheduling and reduced patient stays. Care providers shift procedures to ambulatory settings to improve efficiency. It supports wider device procurement across independent surgical centers. Surgeons gain flexibility through standardized device trays and portable towers. Patient demand for shorter stays pushes more hospitals to upgrade systems. New workflow designs reduce bottlenecks in crowded orthopedic units. Expansion of outpatient facilities increases device turnover rates. Health systems continue to integrate arthroscopy suites into new buildings.

R&D Expansion and Technology Integration That Enhances Procedure Outcomes and Surgical Efficiency

Manufacturers strengthen the Arthroscopy Devices Market through investments in next-generation handheld tools and energy systems. Engineers design platforms that improve tissue handling and safety. It drives strong interest in multifunctional systems that reduce instrument changes. New ergonomic handles improve surgeon comfort during long procedures. Electromechanical tools support controlled movements in delicate joint regions. Robotics-assisted modules enter development pipelines across major players. Hybrid solutions pair imaging and navigation features for better alignment. Hospitals seek integrated stacks that unify imaging, insufflation, and recording.

Arthroscopy Devices Market Trends:

Rapid Shift Toward Fully Integrated Surgical Towers With Unified Control Systems

The Arthroscopy Devices Market sees a rising trend toward integrated towers that streamline workflows. Hospitals seek systems that combine imaging, recording, and power controls. It reduces clutter in tight operating rooms and enhances staff efficiency. Standardized towers also improve training for new surgeons. Networks purchase compatible components to simplify procurement. Many facilities aim to unify arthroscopy, laparoscopy, and ENT platforms. This trend helps reduce maintenance complexity across departments. Surgeons report improved coordination when all devices operate under a single interface.

Growing Adoption of Disposable Visualization and Instrumentation Lines Across High-Volume Centers

High-volume surgical units expand disposable arthroscopy tool usage to improve sterility assurance. Many hospitals shift to single-use scopes to limit contamination risks. It reduces downtime linked to reprocessing delays. Procedural consistency improves through standardized disposable sets. Centers handling sports injuries adopt these products for quick turnover. Manufacturers respond by designing premium disposable visualization chips. Cost-management teams evaluate lifecycle savings from reduced repairs. Demand grows in regions with strict infection-control policies.

- For instance, Trice Medical’s mi-eye 2 is a fully disposable, single-use in-office arthroscopy system that provides real-time visualization through an integrated camera and light source. It removes the need for reprocessing reusable scopes and supports rapid diagnostic assessments within orthopedic clinics.

Increased Use of Digital Workflow Platforms That Support Data Capture and Remote Collaboration

Digital platforms gain traction in the Arthroscopy Devices Market due to rising interest in connected surgery. Hospitals deploy solutions that capture intraoperative data for training and auditing. It improves communication between surgeons and support teams. Remote viewing functions help specialists guide procedures across locations. Recorded footage supports skill development for young clinicians. AI-supported software offers automated tagging of key surgical events. Clinical teams store case data for comparative planning. Adoption grows in advanced centers with strong digital infrastructures.

Wider Movement Toward Energy-Efficient Devices and Environmentally Conscious Surgical Technologies

Sustainability trends shape procurement decisions across orthopedic departments. Many hospitals evaluate devices with lower energy footprints. It supports long-term cost reduction goals across large facilities. Manufacturers redesign pumps and shavers for improved efficiency. Packaging reductions become a priority across supply chains. Hospitals also pursue reusable components with longer life cycles. Environmental audits push for low-waste device models. Sustainable procurement standards influence contract terms in several regions. This trend encourages innovation across arthroscopy developers.

- For instance, Smith & Nephew’s LENS Surgical Imaging System uses a high-performance LED light source with a verified 30,000-hour lifespan, offering a durable and energy-efficient alternative to traditional xenon lamps. The system supports 4K UHD imaging within a compact 3-in-1 control unit and reduces downtime by eliminating frequent bulb replacements.

Arthroscopy Devices Market Challenges Analysis:

High Capital Costs, Complex Training Needs, and Technology Gaps Across Expanding Healthcare Systems

The Arthroscopy Devices Market faces challenges linked to high upfront costs for imaging stacks and powered instruments. Smaller facilities struggle with procurement budgets. It limits access to advanced platforms in many regions. Surgeons need extensive training to achieve mastery with new tools. Operating room teams require time to adjust to upgraded workflows. Limited staff availability slows training cycles in crowded hospitals. Technology gaps remain between high-income and emerging regions. Some providers delay upgrades due to budget cycles and procurement hurdles.

Regulatory Constraints, Sterility Concerns, and Limited Device Standardization Across Diverse Surgical Environments

Regulatory variations impose hurdles on global device launches. The Arthroscopy Devices Market encounters delays due to approval timelines in several countries. It creates inconsistencies in technology availability across regions. Sterility assurance remains difficult in centers with limited reprocessing capacity. Variation in device tray designs complicates standard operating protocols. Surgeons often face compatibility issues between legacy and upgraded systems. Procurement teams struggle to balance cost and performance needs. Environmental concerns also push hospitals to reconsider high-waste devices.

Arthroscopy Devices Market Opportunities:

Growing Demand for Early Joint Preservation, Outpatient Expansion, and Digital Integration Across Orthopedic Programs

The Arthroscopy Devices Market benefits from rising demand for early joint care pathways. Patients seek faster interventions that prevent joint deterioration. It supports growth across outpatient orthopedic networks. Hospitals adopt digital platforms to guide post-operative care. Developers introduce software that improves alignment planning. Surgeons pursue tools that handle complex tasks with greater control. Sports medicine units expand capacity to treat younger populations. New procurement cycles open opportunities for bundled imaging and instrumentation upgrades.

Rising Innovation in Disposable Systems, Robotics-Assisted Modules, and Smart Visualization Tools

Manufacturers gain opportunities by advancing disposable product lines and robotics modules. The Arthroscopy Devices Market gains momentum from interest in smart visualization systems. It drives demand for devices that offer automated clarity control. Hospitals evaluate hybrid reusable-disposable mixes for cost balance. AI-supported imaging upgrades enhance precision during difficult procedures. Robotics development pipelines attract investor attention. Providers consider these technologies to improve consistency across surgeons. Growth potential strengthens across technologically progressive regions.

Arthroscopy Devices Market Segmentation Analysis:

By Product Type

The Arthroscopy Devices Market expands through strong demand across key product categories that support precision-driven orthopedic procedures. Arthroscopes lead usage due to their central role in diagnosis and treatment, supported by steady upgrades in optical quality. Shavers gain traction in high-volume centers that require efficient tissue resection tools. Fluid management systems hold vital importance because they maintain joint visibility and stable pressure control. Implants see rising adoption with complex ligament repair cases. Visualization systems benefit from growing interest in 4K and 3D clarity. Radiofrequency systems secure steady demand for controlled tissue sculpting during surgical repair.

- For instance, the Smith & Nephew WEREWOLF Coblation System uses plasma-based radiofrequency technology designed to remove soft tissue with controlled thermal spread, helping protect surrounding structures during arthroscopy. The CrossFlow Integrated Arthroscopy Pump complements this by delivering automated fluid management that maintains consistent intra-articular pressure for clear joint visualization.

By Application

Knee procedures drive high utilization across the Arthroscopy Devices Market because they represent the largest share of sports injuries and degenerative conditions. Shoulder and elbow interventions grow due to expanding athletic treatment volumes. It supports consistent procurement of tools that handle delicate soft-tissue repair. Hip arthroscopy adoption rises as surgeons broaden indications for early joint preservation. Spine applications gain attention in specialized centers that integrate minimally invasive workflows. The others segment includes ankle and wrist procedures that gain adoption in orthopedic and trauma care settings.

By End User

Hospitals dominate usage due to higher patient inflow, wider case complexity, and broader access to advanced imaging systems. Large orthopedic departments procure integrated towers to support heavy procedural loads. Ambulatory surgical centers and clinics record faster growth through rising preference for outpatient orthopedic procedures. It encourages investment in compact, portable, and standardized arthroscopy systems that support efficient scheduling and shorter recovery timelines. These centers strengthen market expansion through steady procedure turnover and streamlined workflows.

- For instance, the Arthrex SynergyUHD4 4K imaging system is engineered for the ASC environment through a 4-in-1 console that combines a 4K camera, LED light source, image management platform, and connectivity functions in a single compact unit. Its integrated design reduces equipment footprint and streamlines setup in smaller outpatient operating suites. The system supports efficient workflows by consolidating multiple imaging components into one platform.

Segmentation:

By Product Type

- Arthroscopes

- Shavers

- Fluid Management Systems

- Implants

- Visualization Systems

- Radiofrequency Systems

By Application

- Knee

- Shoulder/Elbow

- Hip

- Spine

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers/Clinics

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The Arthroscopy Devices Market secures its largest share in North America, holding around 40% of global revenue. High procedure volumes, strong reimbursement frameworks, and broad adoption of minimally invasive orthopedic techniques support steady growth. Hospitals invest in advanced visualization platforms that improve diagnostic clarity and surgical precision. It benefits from a mature provider network and strong presence of leading manufacturers. Sports injury rates remain high, pushing continuous demand for arthroscopy tools across major centers. Ambulatory surgical facilities expand their arthroscopy capabilities, strengthening market penetration across the United States and Canada.

Europe

Europe accounts for about 30% of the global Arthroscopy Devices Market and records consistent adoption across established orthopedic systems. Hospitals prioritize technology upgrades that support efficient workflows and improved patient outcomes. It sees rising demand from countries with aging populations that experience higher joint degeneration rates. Sports medicine programs expand across Germany, France, and the UK, pushing wider use of visualization and fluid management systems. Procurement teams evaluate integrated towers that meet regional safety and sterility standards. Clinics and day-care centers gain traction, contributing to broader market access across Western and Northern Europe.

Asia-Pacific, Latin America, and Middle East & Africa

Asia-Pacific holds roughly 20% of the market and grows at the fastest pace due to expanding healthcare infrastructure and increasing investments in orthopedic services. Rising sports participation and growing awareness of early joint treatment support higher adoption. Latin America represents around 6% of the Arthroscopy Devices Market, driven by modernization efforts in Brazil, Mexico, and Argentina. It gains momentum through rising private hospital expansions and improved insurance coverage. The Middle East & Africa contributes about 4%, supported by rising demand in Gulf countries and gradual upgrades across public hospitals. Investments in training and modern equipment strengthen long-term potential across emerging economies.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Arthrex, Inc.

- Smith & Nephew Plc

- Stryker Corporation

- Johnson & Johnson (DePuy Synthes)

- CONMED Corporation

- KARL STORZ GmbH & Co. KG

- Medtronic Plc

- Zimmer Biomet Holdings

- Olympus Corporation

Competitive Analysis:

The Arthroscopy Devices Market remains highly competitive, with major companies expanding portfolios through innovation, strategic partnerships, and product enhancements. Leading players focus on advanced visualization platforms, ergonomic handheld tools, and disposable systems that support faster workflows. It benefits from strong R&D pipelines across established brands that aim to improve clinical precision and safety. Companies strengthen market positions by integrating imaging, energy devices, and fluid management into unified surgical systems. Rising adoption of outpatient procedures pushes firms to design compact and portable platforms. Competitive intensity increases as global manufacturers target growth in Asia-Pacific and Latin America. Continuous innovation shapes product differentiation across core segments.

Recent Developments:

- In January 2026, Smith & Nephew Plc completed the $450 million acquisition of Integrity Orthopaedics, integrating the innovative Tendon Seam™ system into its portfolio. This disruptive rotator cuff repair technology is designed to reduce re-tear rates and improve patient outcomes compared to the current standard of care, further strengthening the company’s leading position in the sports medicine market.

- In December 2025, Medtronic Plc collaborated with Symbiosis to launch “The TechKnow Verse,” a next-generation cadaveric training and surgical simulation hub. This initiative is designed to advance surgeon proficiency in minimally invasive techniques, supporting the broader adoption of Medtronic’s arthroscopic and orthopedic diagnostic technologies.

- In September 2025, Arthrex, Inc. announced the successful completion of the first surgical case using its NanoNeedle™ Scope 2.0, a next-generation visualization system for minimally invasive procedures. This follows the July 2025 FDA clearance of the NanoScope™ System for pediatric use in orthopedic and laparoscopic procedures and the June 2025 launch of the Synergy Power™ system, a versatile battery-powered instrument for sports medicine and trauma.

- In January 2025, Stryker Corporation entered into a definitive agreement to acquire Inari Medical, Inc. for approximately $4.9 billion, a deal that closed in February 2025 to significantly expand its vascular and neurotechnology offerings. Additionally, in September 2025, Stryker launched its next-generation 1788 advanced surgical camera in new global markets, providing vibrant 4K high-resolution imaging and enhanced fluorescence capabilities for detailed anatomical visualization.

Report Coverage:

The research report offers an in-depth analysis based on Product Type, Application, and End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising adoption of minimally invasive orthopedic surgery strengthens long-term growth, supported by higher patient preference for faster recovery and improved joint preservation outcomes across diverse clinical settings.

- Advancements in HD, 3D, and chip-on-tip visualization systems improve surgical precision, guiding wider use of enhanced optics in complex procedures performed in high-volume orthopedic centers.

- Outpatient and ambulatory care facilities expand their role in arthroscopy delivery, driven by shorter procedure times, reduced hospital stays, and strong investments in portable surgical platforms.

- Disposable arthroscopy instruments gain broader acceptance due to improved sterility control, predictable performance, and reduced reprocessing constraints in busy clinical environments.

- Robotics-enabled arthroscopy and navigation modules move closer to mainstream adoption, offering enhanced accuracy in joint repair and greater consistency in technique across surgical teams.

- Rising global sports participation and increased injury incidence push steady demand for joint reconstruction and soft-tissue repair tools across both developed and emerging regions.

- AI-supported imaging, automated tissue recognition, and digital case-planning platforms integrate into orthopedic practices, shaping a new phase of data-driven arthroscopy workflows.

- Hospitals invest in unified surgical towers and integrated control systems that streamline operating room functions, strengthen efficiency, and reduce equipment redundancy.

- Emerging economies accelerate procurement of advanced arthroscopy systems due to expanding orthopedic training programs, growing private hospital investments, and rising medical tourism.

- Sustainability-driven design improvements influence device selection, with providers prioritizing energy-efficient consoles, optimized packaging, and extended-life reusable components.