Market Overview

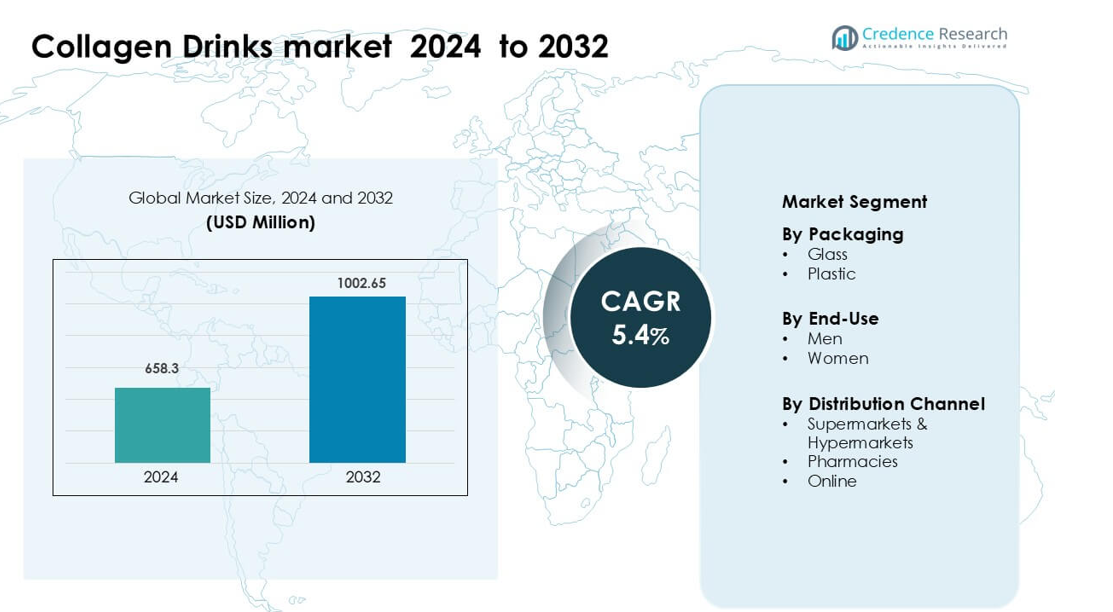

Collagen Drinks market was valued at USD 658.3 million in 2024 and is anticipated to reach USD 1002.65 million by 2032, growing at a CAGR of 5.4 % during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Collagen Drinks Market Size 2024 |

USD 658.3 million |

| Collagen Drinks Market, CAGR |

5.4% |

| Collagen Drinks Market Size 2032 |

USD 1002.65 million |

The Collagen Drinks market is shaped by leading companies such as Revive Collagen, Kinohimitsu, Asertism Healthcare, TCI CO., LTD., Heivy, Shiseido Company Ltd., AmorePacific Corporation, The Collagen Company, Hangzhou Nutrition Biotechnology Co. Ltd., and Vital Protein LLC. These brands compete through clean-label formulations, marine and bovine collagen innovations, and strong digital engagement across global wellness channels. Asia-Pacific remains the leading region with a dominant 36% share in 2024, supported by long-standing collagen consumption habits, rapid product innovation, and strong adoption of beauty-from-within solutions across Japan, South Korea, and China.

Market Insights

- Collagen Drinks market was valued at USD 658.3 million in 2024 and is anticipated to reach USD 1002.65 million by 2032, growing at a CAGR of 5.4 % during the forecast period.

- Strong consumer focus on skin hydration, elasticity, and anti-aging boosts adoption, while women remain the dominant end-use segment with about 68% share due to higher interest in beauty-from-within routines.

- Marine collagen drinks gain traction as a key trend, driven by premium positioning, clean-label demand, and growing preference for fast-absorbing peptide formats in wellness markets.

- Leading companies compete through product innovation, clinical claims, subscription models, and digital marketing strategies, making differentiation essential as new brands enter the category.

- Asia-Pacific leads the global market with 36% share, followed by North America at 32% and Europe at 29%, while glass packaging holds the largest packaging share at around 54%, reflecting demand for premium, stable formulations.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Packaging

Glass packaging leads the Collagen Drinks market with about 54% share in 2024 due to higher consumer trust in glass as a safe, non-reactive container for functional beverages. Brands prefer glass because the material protects active collagen peptides from oxidation and maintains flavor stability. Premium product launches also push demand for glass bottles as companies focus on clean-label positioning and strong shelf appeal. Plastic formats grow at a steady pace as lightweight, low-cost bottles support wider distribution in fitness and convenience channels.

- For instance, Shiseido’s The Collagen Drink comes in 50 ml glass bottles, each delivering 1,000 mg of low-molecular-weight fish collagen peptide per serving.

By End-Use

Women dominate this segment with nearly 68% share in 2024 because most beauty-from-within products target skin health, anti-aging, and hair-nail support. Demand rises as women adopt collagen drinks for daily skincare routines and preventive wellness habits. Marketing campaigns and influencer-driven promotions further strengthen adoption among young and middle-aged users. The men segment grows as brands introduce muscle-support and joint-care formulas, but uptake remains lower compared to women-focused offerings.

- For instance, Herbalife Collagen Skin Booster supplies 2,500 mg of collagen hydrolysate per 5.7 g scoop, formulated with lutein and zinc ingredients often associated with skin health benefits, appealing to beauty-oriented female consumers.

By Distribution Channel

Online channels lead the Collagen Drinks market with about 47% share in 2024 due to rising demand for doorstep delivery, subscription models, and access to wider product ranges. E-commerce platforms help brands promote formulations, flavors, and clinical claims more effectively through targeted ads and user reviews. Supermarkets and hypermarkets also hold strong presence because shoppers value in-store visibility and immediate availability. Pharmacies show steady growth as healthcare-positioned collagen drinks gain acceptance among wellness-driven consumers.

Key Growth Drivers

Rising Demand for Beauty-from-Within Products

Consumers now prioritize internal wellness solutions that support skin elasticity, hydration, and anti-aging results, which drives strong demand for collagen drinks. Many users prefer ingestible collagen because it reaches deeper skin layers that topical creams cannot access, creating steady repeat purchases. Social media plays a major role as influencers share routine-based results, encouraging early adoption among younger age groups. Brands support this rise through clinical claims on wrinkle reduction and improved skin texture, which boosts trust and credibility. Product developers also combine collagen with hyaluronic acid, biotin, and vitamins to deliver multi-benefit drinks that appeal to beauty-conscious buyers.

- For instance, in a randomized, double-blind, placebo-controlled clinical trial, subjects who consumed 1,650 mg/day of low-molecular-weight collagen peptides (containing Gly-Pro and Pro-Hyp) saw significant improvements in skin hydration and elasticity after 12 weeks.

Growing Interest in Joint, Bone, and Muscle Support

Active individuals and aging adults increasingly use collagen drinks to improve joint comfort, bone strength, and muscle recovery. Fitness centers and sports nutrition platforms promote collagen as part of daily workout routines, especially in hydrolyzed or peptide-rich formats that absorb quickly. Clinical studies linking collagen intake with improved cartilage integrity strengthen consumer confidence and encourage long-term use. Urban lifestyles marked by long working hours and limited physical activity further boost demand for joint-support beverages. Manufacturers respond with sugar-free, high-protein, and mobility-focused variants, expanding collagen’s appeal beyond beauty users into overall functional wellness.

- For instance, a study on physically active adults consuming 5 g/day of collagen peptides for 12 weeks reported measurable improvements in joint discomfort and mobility during exercise, based on the Collagen Research Institute’s evaluation of FORTIGEL®.

Premiumization and Demand for Clean-Label Functional Beverages

The market benefits from the rising preference for clean-label drinks featuring transparent, sustainable, and minimally processed ingredients. Consumers choose collagen beverages made from grass-fed, marine, or hormone-free sources and avoid artificial sweeteners, preservatives, and fillers. Brands enhance packaging with eco-friendly bottles, simple labels, and purity certifications to strengthen premium positioning. Improved extraction and hydrolysis technologies increase bioavailability, making premium collagen formats more attractive. As buyers spend more on high-quality functional drinks, collagen beverages gain traction in specialty stores, pharmacies, and online wellness platforms.

Key Trends and Opportunity

Expansion of Marine Collagen Formulations

Marine collagen gains traction due to its high bioavailability, smoother texture, and suitability for pescatarian and flexitarian diets. Brands highlight sustainable fisheries and traceable sourcing to strengthen premium appeal. The growing focus on skin brightness and hydration also aligns well with marine collagen’s peptide profile. Companies launch flavored marine drinks and ready-to-consume shots to attract beauty-focused consumers. This shift creates opportunities for brands to differentiate through ingredient origin, purity, and advanced peptide extraction methods.

- For instance, Vital Proteins’ Marine Collagen provides 12 g of hydrolyzed collagen peptides per serving, derived from the scales of wild-caught cod, and the product is made in a way to maximize digestibility and bioavailability.

Strong Growth of Digital Commerce and Subscription Models

E-commerce drives adoption as consumers explore a wider variety of collagen drinks through reviews, targeted ads, and comparison tools. Subscription plans offering monthly refills boost loyalty and create predictable revenue streams for brands. Digital platforms also support personalized recommendations based on age, lifestyle, and wellness goals. This shift accelerates experimentation with new flavors, functional blends, and travel-size packs, making collagen drinks more accessible to first-time users. The digital environment enables brands to refine messaging and track consumer behavior more effectively.

- For instance, Vital Proteins’ official online store offers a 30-day subscription cycle for its Marine Collagen and Original Collagen Peptides, with each tub containing 284 g (about 28 servings), allowing automated monthly replenishment for regular users.

Rising Demand in Men’s Wellness and Healthy Aging Segments

Men increasingly adopt collagen drinks for joint flexibility, muscle repair, and skin support, creating a new growth zone. Healthy aging populations seek collagen for mobility, bone density, and overall vitality, widening the customer base. Companies offering gender-specific or age-specific formulations can capture these underpenetrated segments. Tailored marketing messages focusing on performance, recovery, and longevity help brands reach new demographics.

Key Challenge

Limited Consumer Education and Conflicting Information

Many buyers remain unclear about collagen’s mechanism, dosage needs, and realistic timelines for visible results. Conflicting online information and exaggerated marketing claims create doubt about effectiveness. Some consumers expect instant changes and discontinue use when results take time, affecting retention. Brands must provide clear, transparent communication supported by clinical studies to build trust and manage expectations. Educating users on consistent intake and ingredient quality becomes essential to sustaining long-term adoption.

Intense Market Competition and Pricing Pressure

Collagen drinks compete with lower-cost powders, capsules, and gummies, which appeal to price-sensitive buyers. Ready-to-drink formats require higher production, packaging, and distribution costs, making premium pricing unavoidable. Smaller brands struggle to stand out as major beauty and nutrition companies dominate shelf space and digital advertising. Intense competition also forces frequent innovation, adding pressure on margins. Balancing premium quality with accessible pricing remains a key challenge for market expansion.

Regional Analysis

North America

North America holds about 32% share of the Collagen Drinks market in 2024, driven by strong consumer focus on beauty-from-within, joint support, and healthy aging. The region benefits from high adoption of premium marine and grass-fed collagen drinks, supported by strong visibility across e-commerce and specialty wellness stores. Influencer-led marketing and clinical positioning further boost demand among women and fitness-driven consumers. The US leads due to advanced product innovation and subscription-based delivery models, while Canada shows steady growth supported by clean-label and sustainable formulations.

Europe

Europe accounts for nearly 29% share in 2024, supported by rising preference for natural beauty supplements and certified clean-label formulations. Consumers in countries such as Germany, the UK, and France adopt collagen drinks for skin elasticity, anti-aging benefits, and joint mobility. Strong regulations around health claims push brands to use clinically backed collagen peptides, which boosts product credibility. The region also sees growing use of marine collagen due to sustainability concerns. Expansion of pharmacy chains and functional beverage aisles further supports category growth across major markets.

Asia-Pacific

Asia-Pacific dominates the Collagen Drinks market with about 36% share in 2024, driven by strong beauty-oriented consumer culture and high acceptance of ingestible skincare. Japan, South Korea, and China lead due to long-standing collagen consumption habits and strong innovation in ready-to-drink formats. Demand rises among younger women who adopt collagen beverages as part of everyday skincare routines. Rising disposable income and extensive online retail penetration accelerate market expansion. The region also benefits from rapid product launches featuring marine collagen, herbal blends, and functional add-ons.

Latin America

Latin America captures around 2% share in 2024, but growth remains steady as awareness of collagen-based beauty and wellness products increases. Brazil and Mexico lead due to rising interest in skincare, fitness, and active aging. Expanding availability in pharmacies and online platforms supports penetration across urban markets. However, price sensitivity limits adoption of premium formulations, encouraging brands to introduce affordable, locally tailored products. Influencer-driven beauty trends and rising wellness culture continue to support market development across major cities.

Middle East & Africa

The Middle East & Africa region holds nearly 1% share in 2024, driven by early-stage adoption of collagen drinks among beauty-conscious consumers in the UAE, Saudi Arabia, and South Africa. Premium collagen beverages gain traction in high-income urban markets where wellness trends spread through social media and expatriate populations. Limited product awareness and high pricing restrain broader penetration, but pharmacy chains and specialty beauty stores expand availability. Growing interest in anti-aging and skin hydration benefits supports gradual growth across developing markets.

Market Segmentations:

By Packaging

By End-Use

By Distribution Channel

- Supermarkets & Hypermarkets

- Pharmacies

- Online

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape of the Collagen Drinks market features a mix of established beauty giants, specialized nutraceutical brands, and emerging wellness companies that compete through formulation quality, clinical credibility, and strong digital engagement. Key players such as Revive Collagen, Kinohimitsu, Asertism Healthcare, TCI CO., LTD., Heivy, Shiseido Company Ltd., AmorePacific Corporation, The Collagen Company, Hangzhou Nutrition Biotechnology Co. Ltd., and Vital Protein LLC focus on expanding product portfolios featuring marine, bovine, and clean-label collagen blends. Companies invest in flavor innovation, premium packaging, and targeted formulations for skin, joints, and active aging to strengthen brand differentiation. E-commerce plays a central role as brands leverage influencer partnerships, subscription programs, and personalized marketing to enhance visibility and retention. Research-backed claims, sustainable sourcing, and transparency in ingredient quality remain critical competitive factors. Manufacturers also expand distribution across pharmacies, supermarkets, and online platforms to reach broader consumer segments and maintain strong market positioning.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Revive Collagen

- Kinohimitsu

- Asertism Healthcare

- TCI CO., LTD.

- Heivy

- Shiseido Company Ltd.

- AmorePacific Corporation

- The Collagen Company

- Hangzhou Nutrition Biotechnology Co. Ltd.

- Vital Protein LLC

Recent Developments

- In August 2025, Revive Collagen Released a blog post titled Collagen for the City: The Daily Upgrade for Busy Londoners.

- In 2024, Pretty Tasty, launched its first ready-to-drink collagen tea line, Pretty Tasty Collagen Tea prepared with high-quality collagen peptides. The product was made available on prettytasty.com and Amazon in two popular flavor varieties, Raspberry Tea and Peach Tea

Report Coverage

The research report offers an in-depth analysis based on Packaging, End-Use, Distribution Channel and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for beauty-from-within products will rise as consumers prioritize skin wellness.

- Marine collagen will gain stronger traction due to clean-label and premium positioning.

- Brands will expand joint, bone, and muscle support formulations for active users.

- Ready-to-drink shots will grow as convenience becomes a major buying factor.

- Digital-first brands will scale faster through influencer marketing and subscription models.

- Gender-specific and age-specific collagen drinks will see wider acceptance.

- Sustainable sourcing and eco-friendly packaging will become key competitive factors.

- Clinical validation of collagen benefits will drive higher trust and repeat purchases.

- Hybrid blends with hyaluronic acid, vitamins, and antioxidants will expand product innovation.

- Pharmacy and specialty wellness channels will become stronger distribution drivers.