Market Overview:

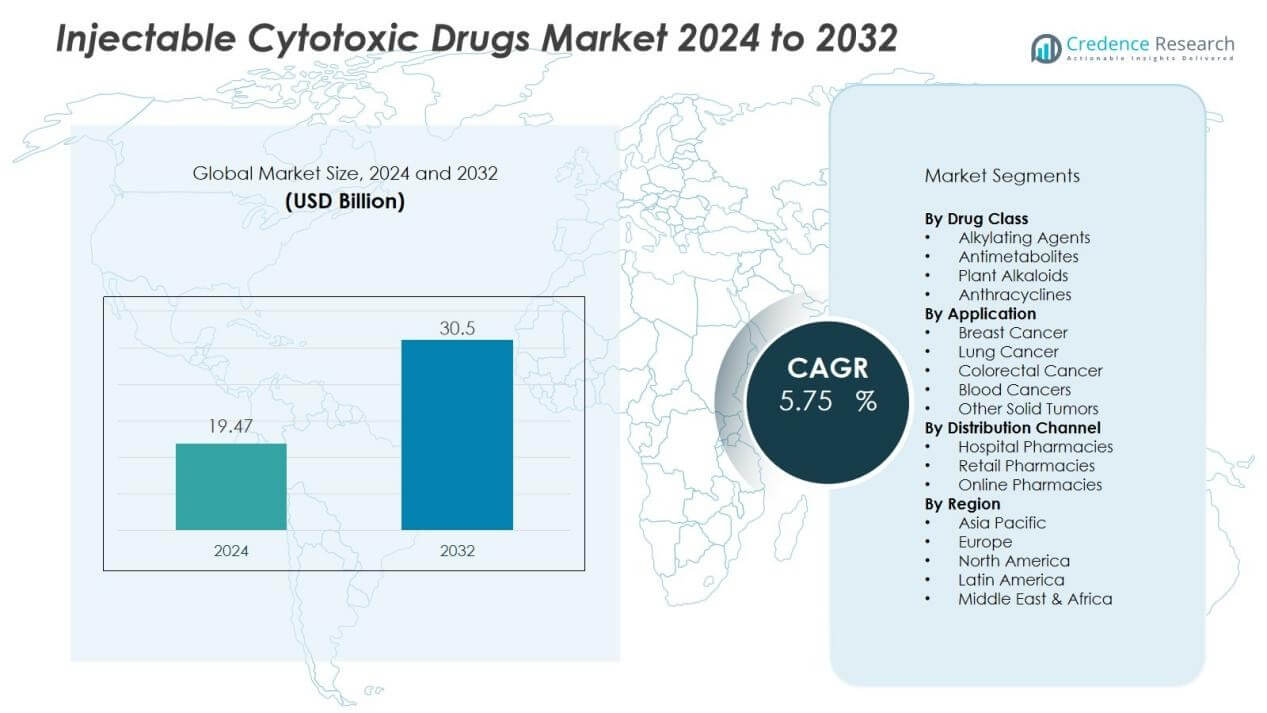

The injectable cytotoxic drugs market size was valued at USD 19.47 billion in 2024 and is anticipated to reach USD 30.5 billion by 2032, at a CAGR of 5.75 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Injectable Cytotoxic Drugs Market Size 2024 |

USD 19.47 Billion |

| Injectable Cytotoxic Drugs Market, CAGR |

5.75% |

| Injectable Cytotoxic Drugs Market Size 2032 |

USD 30.5 Million |

Key drivers include the rising prevalence of cancer worldwide, which sustains a strong need for chemotherapy drugs. Growing geriatric populations and lifestyle-related cancer incidence add to the demand. In addition, the increasing adoption of combination therapies where cytotoxic drugs are paired with newer treatments helps maintain relevance. The market also benefits from expanding healthcare access in low- and middle-income countries, where generic injectable cytotoxic drugs are widely used due to affordability.

Regionally, North America dominates the market, supported by advanced oncology infrastructure, high healthcare spending, and widespread access to branded therapies. Europe follows with strong pharmaceutical pipelines and government-led cancer care initiatives. Asia-Pacific is expected to record the fastest growth, driven by large patient populations, rising cancer screening rates, and the rapid expansion of healthcare infrastructure in countries such as China and India. Latin America and the Middle East & Africa provide emerging opportunities through improved cancer diagnosis and increasing government healthcare investments.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The injectable cytotoxic drugs market was valued at USD 19.47 billion in 2024 and will reach USD 30.5 billion by 2032.

- Rising cancer prevalence across breast, lung, colorectal, and blood cancers drives consistent chemotherapy demand.

- Growing geriatric populations and lifestyle-linked risk factors fuel the need for cytotoxic treatments.

- Combination therapies pairing cytotoxic drugs with targeted or immune-based treatments strengthen market relevance.

- Expanding healthcare infrastructure in Asia-Pacific, Latin America, and Africa supports higher adoption of affordable generics.

- North America held 38% share in 2024, followed by Europe with 29%, backed by advanced oncology systems.

- Asia-Pacific recorded 22% share and remains the fastest-growing region, while Latin America and the Middle East & Africa together accounted for 11% share.

Market Drivers:

Rising Global Cancer Burden:

The injectable cytotoxic drugs market is driven by the growing global cancer burden. Increasing incidence of breast, lung, colorectal, and blood cancers sustains high demand for chemotherapy treatments. It remains a core part of oncology care despite advances in targeted and immuno-oncology therapies. Growing patient pools across both developed and developing regions reinforce the need for these injectable drugs.

- For instance, Novartis replaced two 10 000 L batch reactors with a single 16 L plug flow reactor for continuous manufacturing of imatinib API, boosting overall yield by 50%.

Continued Relevance in Combination Therapies:

The use of cytotoxic drugs in combination with targeted therapies and immunotherapies supports market growth. Oncologists continue to prescribe them to enhance treatment efficacy and reduce resistance. It ensures their relevance in modern cancer care protocols despite new therapeutic options. The injectable cytotoxic drugs market benefits from their adaptability in multi-drug regimens.

- For instance, Roche’s IMpower130 trial showed that adding atezolizumab to carboplatin and nab-paclitaxel extended median overall survival by 4.7 months.

Expanding Healthcare Access in Developing Regions:

Expanding healthcare infrastructure in Asia-Pacific, Latin America, and Africa is a key growth driver. Governments and private players are improving cancer screening and treatment access in these regions. It drives strong uptake of generic injectable cytotoxic drugs due to their affordability and availability. Rising healthcare expenditure and insurance coverage further support market penetration.

Aging Population and Lifestyle Factors:

The rising geriatric population significantly contributes to higher cancer prevalence, fueling drug demand. Older adults are more vulnerable to cancer, making cytotoxic therapies vital in treatment protocols. It also reflects lifestyle-related factors such as smoking, obesity, and sedentary habits that elevate cancer risk. The injectable cytotoxic drugs market continues to expand with these demographic and lifestyle trends.

Market Trends:

Growing Focus on Combination and Multimodal Therapies:

The injectable cytotoxic drugs market is experiencing a shift toward combination and multimodal therapies. Oncologists are increasingly pairing cytotoxic drugs with targeted agents and immunotherapies to maximize treatment outcomes. It helps improve patient survival rates while reducing the chances of drug resistance. Pharmaceutical companies are investing in clinical trials that evaluate cytotoxic agents as part of broader oncology regimens. Hospitals and cancer centers continue to rely on these drugs due to their proven effectiveness in both adjuvant and neoadjuvant settings. The trend highlights the sustained relevance of cytotoxic drugs within modern oncology practices despite the introduction of advanced alternatives.

- For example, in a study of malignant pleural mesothelioma patients, median survival improved to 22.6 months for those receiving surgery, immunotherapy, and chemotherapy combined, compared to 11.7 months with chemotherapy alone.

Rising Demand for Generics and Biosimilars in Emerging Markets:

Demand for generic injectable cytotoxic drugs is expanding rapidly in cost-sensitive regions. Healthcare providers in Asia-Pacific, Latin America, and Africa prioritize affordable generics to increase access to cancer treatments. It creates opportunities for local and regional manufacturers to strengthen their supply chains. Governments are supporting this trend through price regulation and reimbursement programs that encourage widespread adoption. The market is also seeing interest in biosimilars that complement cytotoxic therapies in certain treatment plans. Growing competition among generic producers is shaping a more accessible oncology drug landscape. The injectable cytotoxic drugs market benefits from this transition, reinforcing its role in global cancer care.

- For instance, Sandoz launched the first FDA-approved generic paclitaxel protein-bound injectable suspension containing 100 mg in a single-dose vial in October 2024

Market Challenges Analysis:

High Toxicity and Adverse Effects:

The injectable cytotoxic drugs market faces significant challenges due to toxicity and severe side effects. Patients often experience nausea, immune suppression, hair loss, and fatigue, leading to reduced compliance. Oncologists sometimes limit or delay treatment cycles to protect patient safety, which affects outcomes. It raises concerns about long-term tolerability and quality of life for cancer patients. Pharmaceutical companies continue to explore formulations that may reduce toxicity without compromising efficacy. Despite these efforts, safety concerns remain a major barrier to broader acceptance.

Competition from Targeted and Immuno-Oncology Therapies:

The rise of targeted therapies and immuno-oncology treatments is reshaping the competitive landscape. These advanced options often provide higher precision with fewer side effects compared to cytotoxic drugs. It challenges the positioning of cytotoxic treatments in oncology protocols, especially in developed markets. Healthcare providers prefer modern therapies when affordability and access are not constraints. The injectable cytotoxic drugs market still retains demand in emerging economies, but long-term dominance faces uncertainty. Sustaining relevance will require strategic use in combination regimens and expanded access through affordable generics.

Market Opportunities:

Expansion of Generics and Affordable Therapies:

The injectable cytotoxic drugs market holds strong opportunities through the expansion of generics. Demand for affordable cancer treatments in emerging regions is rising as healthcare systems expand access. It creates space for regional manufacturers to scale production and meet patient needs. Governments support this trend with price control policies, insurance coverage, and procurement programs. Companies focusing on cost-effective supply chains and EN-certified products can secure long-term contracts. Wider adoption of generics ensures sustained relevance of cytotoxic drugs across global oncology care.

Integration in Combination and Adjunct Therapies:

Opportunities also exist in integrating cytotoxic drugs with targeted and immune-based treatments. Oncologists use these drugs to improve outcomes in combination protocols, supporting demand despite competition. It allows pharmaceutical firms to invest in trials that reposition older drugs within modern regimens. Hospitals value these therapies for their proven efficacy in both adjuvant and advanced stages. Expanding clinical applications ensure that injectable cytotoxic drugs remain essential in oncology practice. The injectable cytotoxic drugs market benefits from this adaptability, creating growth avenues in both developed and emerging economies.

Market Segmentation Analysis:

By Drug Class:

The injectable cytotoxic drugs market is segmented into alkylating agents, antimetabolites, plant alkaloids, and anthracyclines. Alkylating agents hold a significant share due to their broad use in multiple cancer types. Antimetabolites remain essential in treating blood cancers and solid tumors, supported by their proven efficacy. Plant alkaloids and anthracyclines continue to see demand, especially in combination regimens. It benefits from the established role of these drug classes in both first-line and second-line treatments.

By Application:

Applications include breast cancer, lung cancer, colorectal cancer, blood cancers, and other solid tumors. Breast and lung cancer dominate due to their high global prevalence and reliance on cytotoxic therapies. Colorectal cancer treatments also represent a strong application segment supported by global screening programs. Blood cancers such as leukemia and lymphoma sustain consistent demand for injectable cytotoxic drugs. It remains vital in oncology care, where newer therapies often serve as adjuncts rather than replacements.

- For instance, the introduction of the FOLFOX regimen (combined oxaliplatin and 5-FU/LV) in metastatic colorectal cancer increased overall survival times to approximately 21.5 months in trials, showcasing substantial improvement in patient outcomes through cytotoxic combinations

By Distribution Channel:

Distribution channels include hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies account for the largest share, reflecting the hospital-based administration of injectable drugs. Retail pharmacies support outpatient access, particularly for maintenance treatments and follow-up cycles. Online pharmacies are emerging in developed and urban markets, offering convenience in procurement. It highlights the growing diversification of distribution methods to improve patient accessibility.

- For instance, Becton, Dickinson and Company’s BD Rowa™ Vmax automated dispensing systems have been installed at over 200 UK&I hospital sites and more than 13,000 sites across Europe, Middle East, and Africa, with a sample of ten new hospital installations achieving actual storage capacities ranging from 17,474 to 41,669 medication packs annually.

Segmentations:

By Drug Class:

- Alkylating Agents

- Antimetabolites

- Plant Alkaloids

- Anthracyclines

By Application:

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Blood Cancers

- Other Solid Tumors

By Distribution Channel:

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Region:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis:

North America and Europe:

North America held 38% market share in 2024, making it the largest regional market. Europe followed with 29% market share during the same year. Advanced oncology infrastructure, high healthcare spending, and access to innovative therapies strengthen adoption in these regions. It benefits from widespread use of both branded and generic injectable cytotoxic drugs across hospital and specialty clinics. Favorable reimbursement systems in the United States, Germany, and France continue to support sustained demand. Regulatory focus on safety and clinical standards further reinforces market strength across these two regions.

Asia-Pacific:

Asia-Pacific accounted for 22% market share in 2024, positioning it as the fastest-growing region. Expanding healthcare infrastructure in China, India, and Japan is driving large-scale adoption of injectable cytotoxic drugs. It is supported by increasing cancer incidence, higher screening rates, and rising government investments in oncology care. Affordable generics dominate usage, enabling broader patient access in low- and middle-income countries. Pharmaceutical firms are expanding production and clinical trials within this region to meet local demand. Rapid urbanization and lifestyle-related cancer cases further strengthen long-term market potential.

Latin America and Middle East & Africa:

Latin America captured 6% market share in 2024, while the Middle East & Africa held 5% market share. Both regions are witnessing improved access to cancer treatment through government funding and private investment. It is supported by infrastructure upgrades, hospital expansions, and better diagnostic facilities. Brazil, Mexico, Saudi Arabia, and South Africa are key countries fueling regional demand. Generic injectable cytotoxic drugs remain central due to affordability and supply availability. Expanding insurance coverage and international partnerships create growth opportunities for manufacturers in these developing markets.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Bristol-Myers Squibb

- Novartis AG

- F. Hoffmann-La Roche Ltd

- Pfizer

- Viatris

- Teva Pharmaceuticals

- Baxter

- Sun Pharmaceutical Industries

- Hikma Pharmaceuticals

- Cipla

Competitive Analysis:

The injectable cytotoxic drugs market is highly competitive with global pharmaceutical leaders driving innovation and supply. Key companies include Bristol-Myers Squibb, Novartis AG, F. Hoffmann-La Roche Ltd, Pfizer, Viatris, Teva Pharmaceuticals, and Baxter. These firms maintain strong portfolios across multiple cancer types, supported by extensive distribution networks and established clinical credibility. It benefits from their focus on combination therapies, reformulations, and generics to address patient needs. Competition is shaped by patent expirations, the rise of cost-effective generics, and ongoing clinical research targeting improved safety profiles. Companies are also strengthening positions through partnerships, regional expansions, and oncology-focused pipelines. It reflects a balanced landscape where multinational firms dominate developed markets while generics producers expand in emerging economies.

Recent Developments:

- In July 2025, Bristol-Myers Squibb’s Supplemental New Drug Application for Sotyktu (deucravacitinib) for the treatment of adults with active psoriatic arthritis was accepted for review across four regions globally (July 20, 2025).

- In October 2024, F. Hoffmann-La Roche Ltd received FDA approval for the first companion diagnostic VENTANA CLDN18 (43-14A) RxDx Assay, to support treatment of gastric and gastroesophageal junction cancers (October 20, 2024).

Report Coverage:

The research report offers an in-depth analysis based on Drug Class, Application, Distribution Channel and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The injectable cytotoxic drugs market will maintain relevance despite competition from advanced oncology therapies.

- Demand will rise in developing regions due to affordability and access to generics.

- Pharmaceutical firms will invest in reformulations aimed at reducing toxicity and side effects.

- Integration with targeted and immune-based treatments will strengthen the role of cytotoxic drugs.

- Expanding geriatric populations will drive consistent demand across global healthcare systems.

- Hospitals and cancer centers will continue to rely on injectable formats for reliable delivery.

- Regional manufacturers will expand production capacity to meet growing demand in Asia-Pacific and Africa.

- Governments will support adoption through procurement programs, reimbursement policies, and cancer care initiatives.

- Research pipelines will focus on enhancing cytotoxic efficacy in combination protocols.

- Long-term opportunities will emerge in personalized oncology where cytotoxic drugs form part of multi-drug regimens.