| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Malignant Ascites Market Size 2024 |

USD 1,122.40 Million |

| Malignant Ascites Market, CAGR |

8.57% |

| Malignant Ascites Market Size 2032 |

USD 2,269.91 Million |

Market Overview:

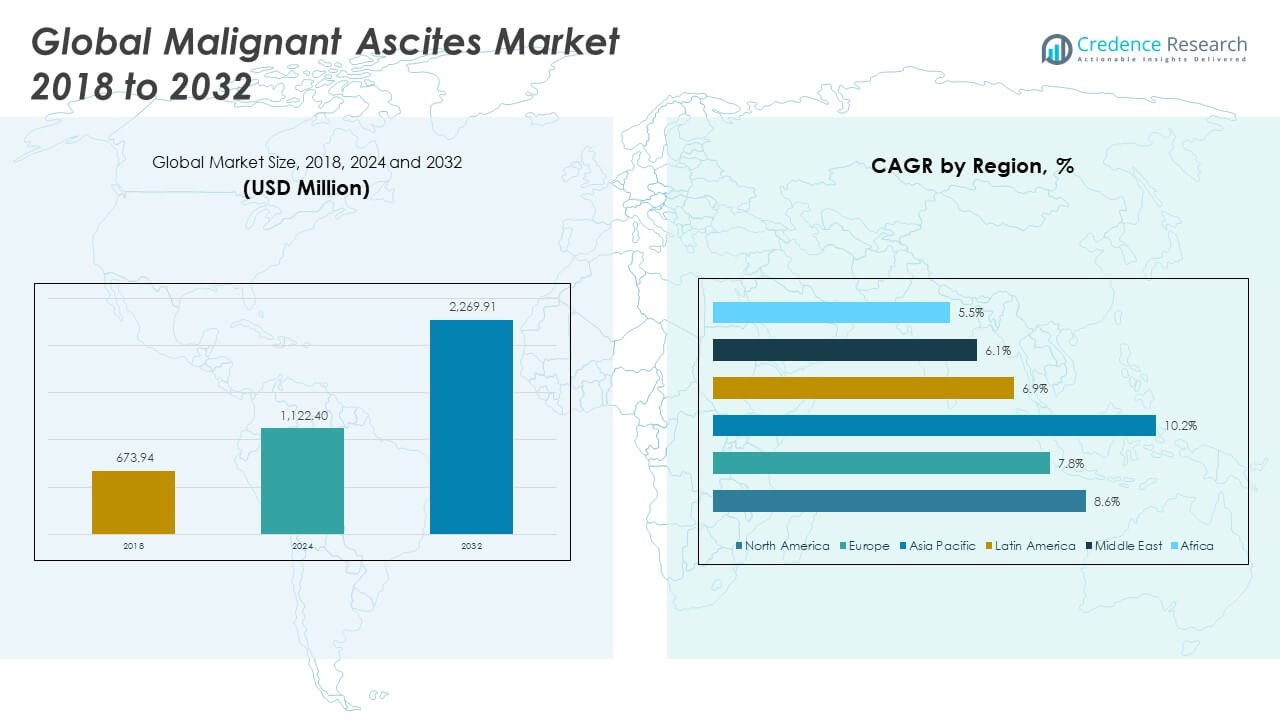

The Global Malignant Ascites Market size was valued at USD 673.94 million in 2018 to USD 1,122.40 million in 2024 and is anticipated to reach USD 2,269.91 million by 2032, at a CAGR of 8.57% during the forecast period.

The global malignant ascites market is primarily driven by the rising prevalence of advanced-stage cancers such as ovarian, pancreatic, gastric, and colorectal cancers, where malignant ascites often presents as a severe complication. Increasing cancer diagnosis rates, particularly among aging populations, are contributing to higher demand for effective palliative care solutions. Therapeutic paracentesis remains the most common treatment, but the market is increasingly embracing advanced options such as intraperitoneal chemotherapy, catheter-based drainage systems, and monoclonal antibody therapies. Continuous advancements in drug delivery technologies and the integration of biologics are expanding the therapeutic landscape. Moreover, the shift toward minimally invasive and home-based treatment approaches has further accelerated market adoption, especially among patients seeking improved quality of life. Healthcare providers and payers are also supporting this transition through reimbursement policies and outpatient care programs.

North America holds the largest share of the global malignant ascites market due to the region’s well-established healthcare infrastructure, higher cancer prevalence, and strong adoption of advanced treatment modalities. The U.S., in particular, accounts for a substantial portion of market revenue, driven by high healthcare spending, favorable reimbursement systems, and the presence of major pharmaceutical and medical device companies. Europe follows closely, with countries like Germany, France, and the U.K. offering robust cancer care networks and early access to intraperitoneal biologics such as catumaxomab. Meanwhile, Asia-Pacific is projected to witness the fastest growth, fueled by an increasing geriatric population, rising cancer incidence, and improving healthcare infrastructure in countries like China, Japan, and India. Governments across the region are ramping up cancer screening programs and expanding public healthcare budgets. Latin America and the Middle East & Africa are also showing steady progress, though market penetration remains limited due to infrastructural and economic constraints.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Global Malignant Ascites Market was valued at USD 1,122.40 million in 2024 and is projected to reach USD 2,269.91 million by 2032, growing at a CAGR of 8.57%.

- Rising cases of ovarian, gastric, pancreatic, and colorectal cancers are driving the demand for malignant ascites management solutions.

- Hospitals and oncology clinics are increasingly adopting catheter-based drainage systems and intraperitoneal therapies for better patient outcomes.

- Advancements in monoclonal antibodies and biologics are expanding the treatment landscape beyond traditional paracentesis.

- Patients and providers are favoring home-based and minimally invasive procedures that reduce hospital visits and improve quality of life.

- North America leads the market share, followed by Europe, while Asia Pacific is the fastest-growing region due to rising cancer prevalence and healthcare investments.

- High treatment costs and limited access in low-resource settings remain key challenges, prompting demand for affordable, scalable solutions.

Market Drivers:

Increasing Global Cancer Burden is Elevating the Need for Malignant Ascites Management

The rising incidence of late-stage cancers is a key driver for the Global Malignant Ascites Market. Malignant ascites frequently occurs in patients with ovarian, pancreatic, gastric, and colorectal cancers, especially during the advanced stages. With cancer rates climbing globally due to aging populations, sedentary lifestyles, and dietary changes, the need for effective palliative treatments has intensified. Many patients experience recurrent fluid buildup that impacts quality of life and requires timely intervention. It is critical for healthcare systems to provide access to reliable drainage and therapeutic solutions. The Global Malignant Ascites Market is expanding as hospitals and oncology clinics seek to address this unmet medical need through symptom-focused treatments and innovative approaches.

Therapeutic Advancements Are Broadening Treatment Capabilities and Market Scope

The market benefits from ongoing progress in drug delivery and supportive care techniques. Therapeutic paracentesis remains a widely used method for fluid removal, but newer options, such as indwelling peritoneal catheters and intraperitoneal chemotherapy, are becoming more available. Targeted therapies, including monoclonal antibodies like catumaxomab, have opened new clinical pathways, especially for refractory cases. These advancements are improving symptom control, reducing hospital stays, and enhancing patient comfort. The Global Malignant Ascites Market is responding to the demand for safer, more effective, and personalized therapeutic options. It continues to evolve as research institutions and pharmaceutical companies invest in innovative solutions.

Shift Toward Minimally Invasive and Outpatient Procedures is Accelerating Adoption

A growing number of patients and providers prefer minimally invasive and outpatient procedures over repeated hospital admissions. Technologies such as tunneled catheters and automated drainage systems allow patients to manage malignant ascites outside of traditional care settings. These tools reduce complications and improve treatment adherence, especially among elderly or terminally ill patients. It supports healthcare cost reduction while maintaining clinical effectiveness. The Global Malignant Ascites Market is adapting to this trend by integrating device-based solutions with home care protocols. It aligns with broader healthcare goals to improve quality of life through patient-centered care models.

- For instance, Becton, Dickinson and Company (BD) expanded its portfolio in 2021 with the PeritX Peritoneal Catheter System, which is the first and only FDA-indicated tunneled catheter for both malignant and non-malignant ascites drainage, allowing patients to manage their condition at home.

Supportive Healthcare Policies and Cancer Care Infrastructure Are Enhancing Market Growth

Stronger national policies focused on cancer care and palliative treatment are reinforcing market momentum. In high-income countries, reimbursement programs help cover advanced treatments, including intraperitoneal drug delivery and catheter-based fluid management. Government-funded screening and oncology programs have led to earlier detection and more consistent monitoring, increasing the need for ascites control. Pharmaceutical companies are leveraging these systems to introduce new products and scale adoption. The Global Malignant Ascites Market benefits from favorable regulatory environments and healthcare modernization in both developed and emerging economies. It is well-positioned to grow alongside expanding oncology care frameworks.

- For instance, the Centers for Medicare & Medicaid Services (CMS) in the United States proposed additional payment for Sequana Medical’s Alfapump system in 2024, following its FDA approval as the first active implantable device for automatic ascites removal.

Market Trends:

Growing Focus on Biomarker-Based Approaches Is Enhancing Diagnostic Precision

The increasing interest in personalized medicine has driven research into biomarker-based identification of malignant ascites. Clinicians are using specific molecular markers in ascitic fluid, such as vascular endothelial growth factor (VEGF) and cancer antigen 125 (CA-125), to distinguish malignant from benign ascites more accurately. It enables faster diagnosis and supports timely treatment decisions, especially in cases where imaging and cytology alone may be inconclusive. Diagnostic advancements help clinicians detect underlying cancer progression and guide therapy more effectively. The Global Malignant Ascites Market is witnessing increased investment in fluid-based molecular diagnostics for enhanced clinical outcomes. It supports a shift toward more targeted, evidence-driven care.

- For example, Bio-Techne’s Ella™ platform enables automated, multiplexed quantification of biomarkers such as vascular endothelial growth factor (VEGF) and cancer antigen 125 (CA-125), delivering results in under 90 minutes. The system typically achieves a coefficient of variation (CV) below 10% for both intra- and inter-assay precision.

Integration of AI and Machine Learning Tools into Oncology Workflow

Artificial intelligence (AI) and machine learning are becoming part of oncology treatment planning, including for complex conditions like malignant ascites. These technologies assist in predictive analytics by evaluating patterns in patient data, recurrence risk, and response to therapy. Software tools help oncologists select optimal interventions, improving patient stratification and follow-up care. It is gaining relevance in large hospital systems where early intervention in fluid accumulation can improve patient outcomes. The Global Malignant Ascites Market is expected to benefit from AI-enabled solutions that enhance monitoring, resource allocation, and decision-making efficiency. It supports more proactive and data-informed clinical pathways.

- For example, Siemens Healthineers has implemented its AI-Rad Companion software, powered by Intel Xeon Scalable processors, to accelerate and improve the accuracy of cancer imaging diagnostics.

Expansion of Clinical Trials Exploring Novel Intraperitoneal Therapies

The pipeline of experimental therapies for malignant ascites is growing, with several clinical trials underway worldwide. Researchers are exploring innovative agents, including cytokine modulators, immunotherapeutics, and gene-based therapies, for intraperitoneal administration. These trials aim to disrupt the tumor microenvironment and limit fluid accumulation through targeted biological mechanisms. It reflects a shift from conventional fluid removal to disease-modifying interventions. The Global Malignant Ascites Market is evolving with these developments, as early-stage results show promising efficacy and safety profiles. It signals the potential for new treatment standards over the coming decade.

Collaborations Between Pharma and Device Firms Are Enabling Hybrid Solutions

Partnerships between pharmaceutical companies and medical device manufacturers are driving the development of integrated treatment platforms. These collaborations are producing hybrid systems that combine drug delivery mechanisms with catheter-based management or implantable devices. It improves convenience and reduces the procedural burden for both patients and healthcare providers. Companies are co-developing closed-loop systems that facilitate real-time monitoring and drug infusion directly into the peritoneal cavity. The Global Malignant Ascites Market is moving toward such combined modalities that offer both therapeutic control and fluid drainage in one solution. It reflects a broader trend of cross-sector innovation in advanced oncology care.

Market Challenges Analysis:

High Treatment Costs and Limited Access in Resource-Constrained Settings

The cost of managing malignant ascites remains a major challenge, especially in low- and middle-income countries. Therapeutic procedures such as paracentesis, tunneled catheter placement, and intraperitoneal chemotherapy involve significant expenditure on equipment, hospitalization, and ongoing care. Reimbursement gaps and limited insurance coverage further restrict access to advanced treatment options. Many healthcare systems struggle to absorb the high costs of biologics and targeted therapies. The Global Malignant Ascites Market faces barriers in reaching underserved populations where oncology infrastructure is still developing. It needs scalable, cost-effective solutions that align with regional healthcare capabilities.

Safety Concerns and Limited Long-Term Efficacy of Current Interventions

Procedures used to manage malignant ascites carry clinical risks, including infection, bowel perforation, electrolyte imbalance, and reduced patient tolerance with repeated drainage. While fluid removal offers short-term relief, it does not address the root cause of ascitic accumulation. Current interventions often fail to deliver sustained efficacy, leading to frequent hospital readmissions and reduced quality of life. Regulatory bodies remain cautious in approving newer treatments due to safety profiles and limited long-term data. The Global Malignant Ascites Market must overcome these clinical limitations by promoting innovation in safer, disease-modifying therapies. It requires a balance between symptom control and long-term oncologic benefit.

Market Opportunities:

Rising Demand for Personalized Oncology Care Is Creating Space for Targeted Therapies

The shift toward personalized medicine presents significant opportunities for more precise and effective treatment of malignant ascites. Oncologists are focusing on tumor-specific markers and molecular profiles to guide therapeutic decisions. This approach supports the use of targeted intraperitoneal therapies and immunotherapies that align with individual patient biology. The Global Malignant Ascites Market can benefit from integrating these innovations into standard care, especially in advanced cancer cases where tailored interventions improve clinical outcomes. It opens the door for biotech firms and pharmaceutical companies to develop niche therapies that address fluid accumulation at its source. New regulatory frameworks are supporting faster approvals of such targeted treatments.

Growing Use of Home-Based Care Models Is Expanding Treatment Accessibility

The healthcare industry is seeing a rising shift toward decentralized care delivery, including home-based treatment for palliative conditions. Malignant ascites management through indwelling catheters and remote monitoring tools supports this trend. Patients prefer the comfort of home settings, reducing hospital visits and enhancing adherence to care plans. The Global Malignant Ascites Market is well-positioned to capture value through portable drainage devices and digital health integrations. It creates new business models around home infusion services, rental equipment, and virtual consultations. Medical device manufacturers and service providers have a growing opportunity to deliver patient-centered, scalable solutions.

Market Segmentation Analysis:

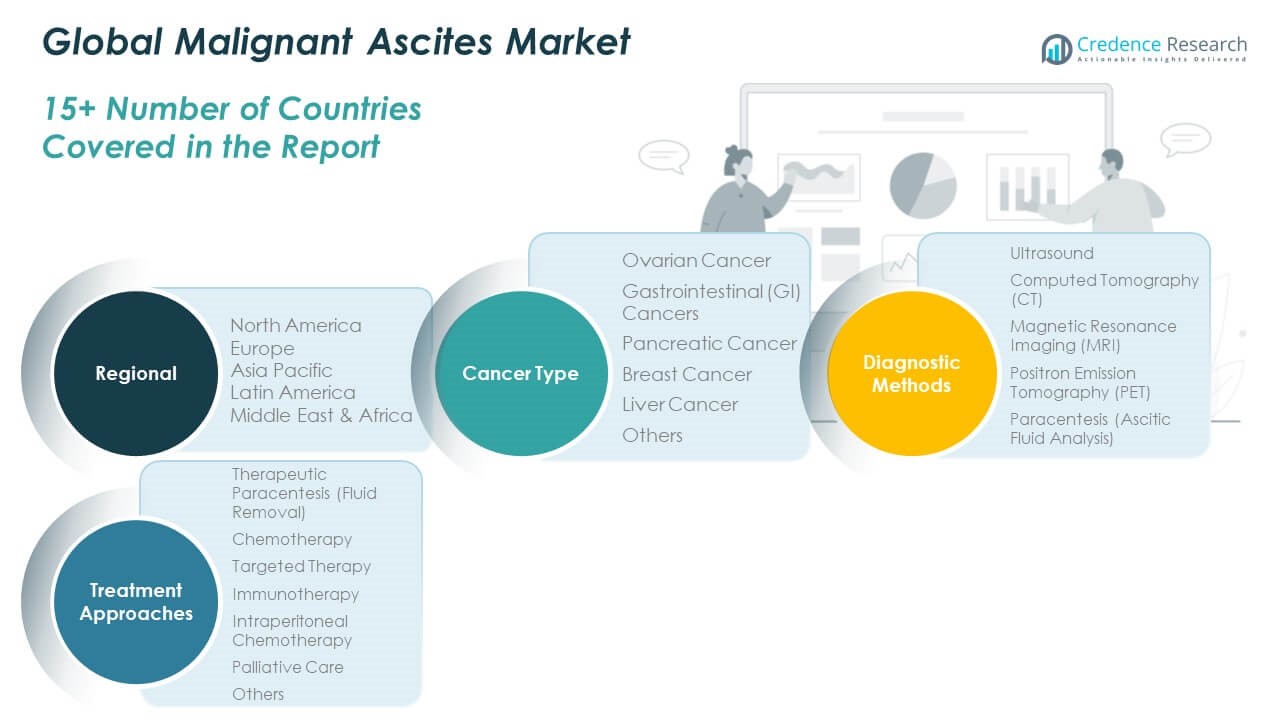

The Global Malignant Ascites Market is segmented

By cancer type, diagnostic methods, and treatment approaches, reflecting the complexity and multi-disciplinary nature of managing this condition. Among cancer types, ovarian cancer holds the largest share due to its strong association with malignant ascites in advanced stages. Gastrointestinal and pancreatic cancers follow closely, while breast and liver cancers contribute steadily to overall case volumes. The “Others” category includes less common malignancies that still lead to peritoneal fluid accumulation.

- For example, in the pivotal GOG-0218 trial, 38% of women with advanced-stage ovarian cancer presented with malignant ascites at diagnosis, and over 60% developed ascites during disease progression.

By diagnostic methods, paracentesis remains the most definitive and widely used technique, enabling both fluid analysis and symptom relief. Ultrasound and CT imaging are frequently used for fluid detection and guiding procedures. MRI and PET are typically reserved for complex cases requiring detailed visualization.

By treatment, therapeutic paracentesis dominates the segment due to its immediate effectiveness in symptom control. The Global Malignant Ascites Market is also expanding across targeted therapy, intraperitoneal chemotherapy, and immunotherapy. These approaches offer potential disease-modifying benefits and align with evolving cancer treatment protocols. Palliative care continues to play a vital role in overall patient management.

- For example, Bevacizumab, an anti-VEGF monoclonal antibody, was shown in the GOG-0218 trial to significantly delay the recurrence of ascites and reduce the need for repeat paracentesis in ovarian cancer patients.

Segmentation:

By Cancer Type

- Ovarian Cancer

- Gastrointestinal (GI) Cancers

- Pancreatic Cancer

- Breast Cancer

- Liver Cancer

- Others

By Diagnostic Methods

- Ultrasound

- Computed Tomography (CT)

- Magnetic Resonance Imaging (MRI)

- Positron Emission Tomography (PET)

- Paracentesis (Ascitic Fluid Analysis)

By Treatment Approaches

- Therapeutic Paracentesis (Fluid Removal)

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Intraperitoneal Chemotherapy

- Palliative Care

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East

- Africa

Regional Analysis:

North America

The North America Malignant Ascites Market size was valued at USD 285.23 million in 2018 to USD 469.95 million in 2024 and is anticipated to reach USD 953.12 million by 2032, at a CAGR of 8.6% during the forecast period. North America holds the highest share in the Global Malignant Ascites Market, accounting for nearly 37% of the global revenue in 2024. Strong healthcare infrastructure, high cancer prevalence, and the presence of leading pharmaceutical and medical device companies contribute to regional dominance. The U.S. leads within the region due to strong adoption of advanced therapies and favorable reimbursement frameworks. It benefits from ongoing clinical trials and the integration of precision medicine into oncology care. Canada also supports market growth through public healthcare systems and early diagnosis programs. The demand for home-based drainage systems is growing, improving patient convenience and reducing hospital burden.

Europe

The Europe Malignant Ascites Market size was valued at USD 195.15 million in 2018 to USD 313.52 million in 2024 and is anticipated to reach USD 597.74 million by 2032, at a CAGR of 7.8% during the forecast period. Europe represents around 25% of the Global Malignant Ascites Market, driven by comprehensive cancer care networks and strong public health systems. Countries such as Germany, France, and the United Kingdom invest in cancer research and provide access to innovative biologics like catumaxomab. The region supports regulatory approvals for intraperitoneal therapies and promotes early intervention strategies. It emphasizes evidence-based care and patient-centered treatment protocols. Hospitals in Western Europe are increasingly adopting minimally invasive tools and personalized approaches. Eastern European countries show growing demand due to improved oncology infrastructure and funding.

Asia Pacific

The Asia Pacific Malignant Ascites Market size was valued at USD 133.07 million in 2018 to USD 239.73 million in 2024 and is anticipated to reach USD 547.56 million by 2032, at a CAGR of 10.2% during the forecast period. Asia Pacific holds nearly 19% share of the Global Malignant Ascites Market and is the fastest-growing regional segment. Rising cancer incidence, especially gastrointestinal and ovarian cancers, is accelerating the need for malignant ascites management. Countries like China, Japan, and India are expanding oncology services and integrating new treatment protocols. It benefits from improving diagnostic capabilities and increased government focus on cancer care. The region sees rising demand for cost-effective, scalable interventions suited to both urban and rural populations. Domestic manufacturers and global players are strengthening regional supply chains and product access.

Latin America

The Latin America Malignant Ascites Market size was valued at USD 32.43 million in 2018 to USD 53.35 million in 2024 and is anticipated to reach USD 95.74 million by 2032, at a CAGR of 6.9% during the forecast period. Latin America accounts for around 4% of the Global Malignant Ascites Market and shows steady growth driven by improving cancer diagnosis and treatment infrastructure. Brazil and Mexico lead regional adoption due to expanding oncology units and access to essential therapies. It faces challenges in affordability and healthcare disparities, particularly in rural and low-income communities. However, public health programs and collaborations with international organizations are supporting progress. Hospitals are increasingly introducing palliative care options, including outpatient fluid drainage. The focus on medical device affordability is likely to support broader access in the coming years.

Middle East

The Middle East Malignant Ascites Market size was valued at USD 17.68 million in 2018 to USD 26.74 million in 2024 and is anticipated to reach USD 45.01 million by 2032, at a CAGR of 6.1% during the forecast period. The Middle East contributes nearly 2% of the Global Malignant Ascites Market, supported by growing investments in cancer care and medical tourism. Gulf countries such as the UAE and Saudi Arabia are enhancing oncology services with modern infrastructure and international partnerships. It benefits from higher awareness, private sector engagement, and early-stage screening programs. However, gaps in skilled workforce and treatment standardization limit uniform adoption across the region. Demand for portable fluid management devices is rising, especially in specialized cancer centers. Government-led healthcare reforms are expected to improve access to innovative therapies.

Africa

The Africa Malignant Ascites Market size was valued at USD 10.38 million in 2018 to USD 19.11 million in 2024 and is anticipated to reach USD 30.74 million by 2032, at a CAGR of 5.5% during the forecast period. Africa holds less than 2% share of the Global Malignant Ascites Market but presents untapped potential. Limited oncology infrastructure and delayed cancer diagnosis remain key barriers to early treatment of malignant ascites. It relies heavily on international aid, non-governmental initiatives, and mobile health services to address care gaps. Major urban centers in South Africa, Nigeria, and Kenya are gradually introducing advanced palliative care tools. The region requires affordable treatment options and training programs to support clinical personnel. Strategic partnerships between global companies and local health agencies may accelerate market development in underserved areas.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Medtronic plc

- Braun Melsungen AG

- GE Healthcare

- Boston Scientific Corporation

- Fresenius SE & Co. KGaA

- BD (Becton, Dickinson and Company)

- Pfizer Inc.

Competitive Analysis:

The Global Malignant Ascites Market features a moderately competitive landscape, with key players focusing on specialized therapies and drainage devices. Companies such as Becton, Dickinson and Company, Medtronic, Fresenius Kabi, and Cardinal Health lead the market by offering advanced paracentesis kits, catheters, and infusion systems. It is witnessing increased activity from biotechnology firms developing monoclonal antibodies and targeted intraperitoneal therapies. Strategic partnerships, product innovations, and clinical trial investments are shaping competitive dynamics. Firms are prioritizing safety, ease of use, and home-care compatibility to meet evolving patient and provider needs. The Global Malignant Ascites Market is also attracting interest from regional device manufacturers in Asia and Latin America, aiming to offer cost-effective solutions. Competition remains centered on expanding distribution, obtaining regulatory approvals, and demonstrating superior clinical outcomes.

Recent Developments:

- In January 2024, B. Braun Melsungen AG completed the sale of its endoscopic vacuum therapy assets, including the Endo-SPONGE® and Eso-SPONGE®, to Boston Scientific Corporation. This transaction enables B. Braun to focus on its core strategic areas, while Boston Scientific expands its portfolio in gastrointestinal treatment technologies.

- In February 2025, Lindis Biotech and Pharmanovia announced the European marketing authorization approval for Catumaxomab, a first-in-class trifunctional bi-specific monoclonal antibody treatment for malignant ascites. This approval marks Catumaxomab as the only approved drug therapy for malignant ascites in Europe, representing a significant advancement in treatment options for this condition.

- In December 2024, the U.S. Food and Drug Administration (FDA) approved the Alfapump® system for the treatment of recurrent or refractory ascites due to liver cirrhosis. This implantable device automatically transfers excess fluid from the abdominal cavity to the bladder, reducing the need for frequent paracentesis and improving patients’ quality of life. This approval highlights the growing innovation in medical devices aimed at managing malignant ascites and related complications.

Market Concentration & Characteristics:

The Global Malignant Ascites Market exhibits moderate concentration, with a mix of multinational corporations and emerging biotechnology firms competing across treatment and device segments. It is characterized by a strong focus on palliative care, limited curative options, and a reliance on hospital and outpatient-based procedures. The market emphasizes symptom management through paracentesis, intraperitoneal drug delivery, and catheter-based fluid control. It is shaped by regulatory oversight, patient safety requirements, and regional disparities in access to oncology care. Technological advancements, home-based care adoption, and targeted therapies are influencing product development and market entry strategies. The Global Malignant Ascites Market remains driven by clinical need, innovation, and expanding cancer care infrastructure.

Report Coverage:

The research report offers an in-depth analysis based on Cancer Type, Diagnostic Methods and Treatment Approaches. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global cancer incidence will continue to drive demand for malignant ascites management solutions.

- Targeted intraperitoneal therapies are expected to gain regulatory approval and expand treatment options.

- Home-based care models will see higher adoption, boosting demand for portable drainage systems.

- Asia Pacific will emerge as a key growth region due to improved oncology infrastructure and rising awareness.

- Integration of AI tools in oncology workflows will enhance early diagnosis and personalized treatment planning.

- Collaborations between pharmaceutical and medical device firms will lead to hybrid therapy-delivery platforms.

- Public and private investments in cancer research will accelerate the development of innovative biologics.

- Reimbursement frameworks will evolve to support outpatient and minimally invasive procedures.

- Market players will prioritize cost-effective solutions to improve access in low-income regions.

- Clinical trials focused on long-term efficacy and disease-modifying therapies will shape future treatment standards.