| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Tracheal Stent Market Size 2024 |

USD 112.7 Million |

| Tracheal Stent Market, CAGR |

7.80% |

| Tracheal Stent Market Size 2032 |

USD 205.5 Million |

Market Overview

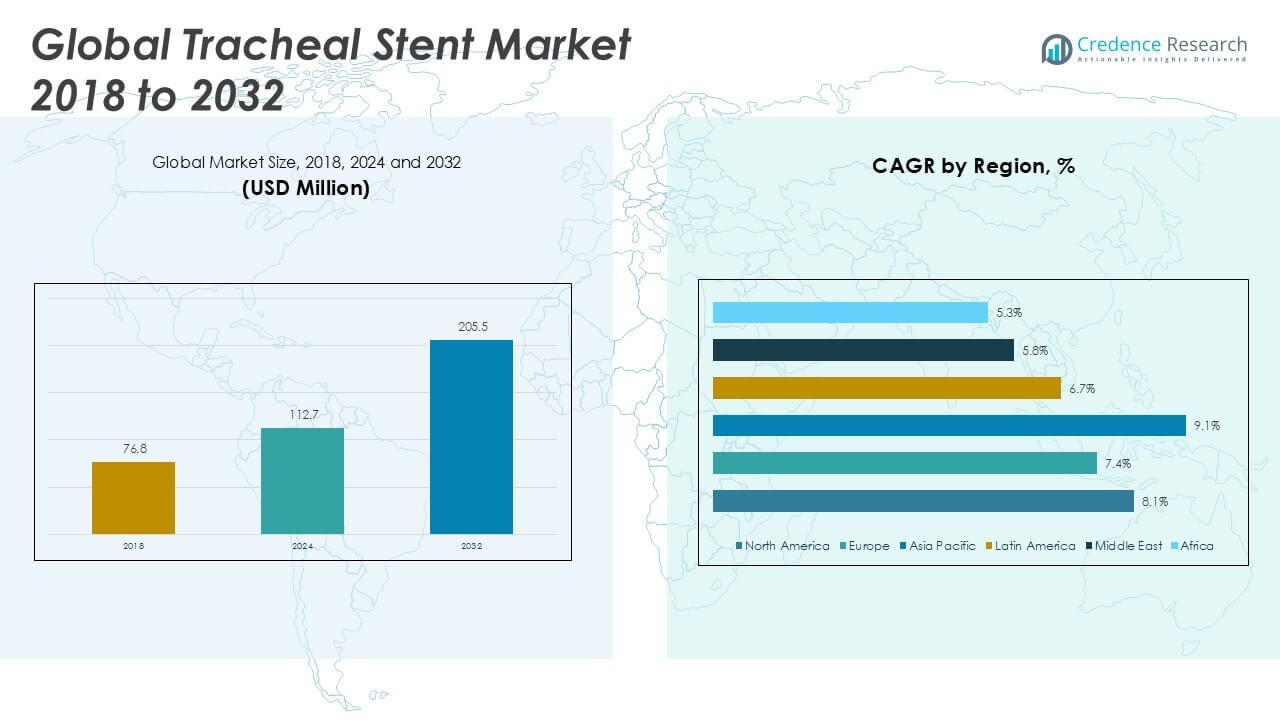

The Global Tracheal Stent Market is projected to grow from USD 112.7 million in 2024 to an estimated USD 205.5 million by 2032, reflecting a compound annual growth rate (CAGR) of 7.80% from 2025 to 2032.

Clinical need drives innovation in tracheal stenting. Manufacturers develop bioresorbable and drug-eluting designs to reduce migration risk and granulation tissue formation. Preference for minimally invasive airway management encourages adoption of self-expanding metallic and silicone stents. Technological advances such as three-dimensional printing enable patient-specific stent geometries, improving deployment accuracy. Meanwhile, strategic collaborations between device makers and contract research organizations accelerate product pipelines and broaden physician training programs.

Regionally, North America commands the largest market share, supported by well-established reimbursement frameworks and high procedural rates. Europe follows, buoyed by growing interventional pulmonology centers across Germany, France, and the UK. Asia Pacific exhibits the fastest growth, led by China and India, where increasing awareness and expanding hospital infrastructure boost demand. Key players compete through product differentiation and global distribution networks; notable companies include Boston Scientific Corporation, Merit Medical Systems Inc., Cook Medical LLC, Johnson & Johnson (Ethicon Division), and Micro-Tech Endoscopy. These organizations leverage R&D investments and strategic alliances to strengthen their market positions across all major regions.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Global Tracheal Stent Market grows from USD 112.7 million in 2024 to USD 205.5 million by 2032 at a 7.8% CAGR, driven by rising procedural volumes.

- Growing incidence of benign and malignant airway obstructions boosts adoption of minimally invasive stenting over surgical alternatives.

- Advances in bioresorbable polymers, drug-eluting coatings and 3D-printed, patient-specific designs improve outcomes and fuel market expansion.

- Stringent approval requirements and variable regional standards extend time-to-market and raise development costs.

- High device and procedural expenses limit uptake in price-sensitive regions and strain hospital budgets.

- It leads with a 38.4% share, underpinned by robust reimbursement and established interventional pulmonology infrastructure.

- Fastest growth at a 9.1% CAGR from 2025 to 2032 reflects expanding hospital networks and rising clinician training programs.

Market Drivers

Clinical Necessity Fuels Adoption and Product Evolution

Tracheal obstructions drive demand for airway support devices. The Global Tracheal Stent Market addresses minimally invasive treatment for benign and malignant lesions. It offers alternative to open surgery, reducing patient recovery time. Clinical trials show improved airway patency and comfort. Physicians adopt metallic and silicone stents for reliable lumen maintenance. Personalized stent designs lower complication rates and enhance outcomes.

- For instance, hospitals are expected to perform the majority of tracheal stenting procedures in 2025, accounting for an estimated 58% of total cases, with ambulatory surgical centers handling about 27%, reflecting the clinical necessity and widespread adoption of these devices in complex airway management

Materials Science and Customization Drive Device Innovation

Innovations in the Global Tracheal Stent Market include materials science breakthroughs. These advances enable development of bioresorbable and drug-eluting stents. It minimizes migration risk and tissue overgrowth. Three-dimensional printing allows custom-fit devices for each patient. Real-time imaging integration improves placement precision. Collaborations between industry and research bodies accelerate product validation.

- For instance, in the near future (2025–2035), the market is expected to see a significant shift with the introduction of individually tailored 3D-printed stents and drug-delivery stents, with hospitals and specialized centers increasingly employing these advanced devices to address patient-specific anatomical needs and reduce complications

Supportive Reimbursement and Infrastructure Boost Market Uptake

Favorable reimbursement frameworks underpin Global Tracheal Stent Market expansion. They lower financial barriers for hospitals and patients. It supports higher procedure volumes in clinical settings. Well-equipped interventional pulmonology centers drive adoption rates. Training programs teach optimal stent selection and placement techniques. Hospital investments in advanced imaging equipment further enable use.

Expansion in Emerging Economies Creates Growth Pathways

Healthcare growth in Asia Pacific and Latin America boosts market potential. It aligns with rising respiratory disease prevalence. Local manufacturing partnerships reduce costs and improve supply chains. Government policies increase access to advanced airway therapies. Clinicians shift toward stenting over invasive surgeries. These factors position the Global Tracheal Stent Market for sustained growth.

Market Trends

Innovative Material Designs Improve Patient Safety Profiles

Material science breakthroughs drive safer device designs. The Global Tracheal Stent Market registered growth in adoption of bioresorbable polymers. It reduces risk of long-term complications following placement. Self-expanding metallic stents incorporate nitinol frameworks to maintain airway patency. Drug-eluting coatings deliver localized therapy to prevent tissue growth. It supports consistent performance under variable physiological conditions. Customized stent surfaces adapt to individual anatomy.

- For instance, a study analyzing silicone airway stents found that a 23 mm stent with a 45° angle demonstrated the best performance against compression and migration in the trachea, highlighting how specific geometric and material innovations can directly improve patient safety outcomes

Patient-Specific Manufacturing Enhances Treatment Precision and Fit

Three-dimensional printing techniques produce exact anatomical replicas. The Global Tracheal Stent Market leverages custom-fit devices for unique airway structures. It reduces procedural time and lowers migration incidents. CT scan data guide tailored designs that match patient curvature. Rapid prototyping shortens development cycles for new stent models. It fosters close collaboration between clinicians and engineers. Precise fit enhances post-placement stability and comfort.

- For instance, a four-year follow-up at the Cleveland Clinic reported the use of nine patient-specific airway stents (five left mainstem and four right mainstem) in a single patient, with CT-based measurements guiding iterative adjustments in stent diameter and fit as the airway anatomy changed over time

Digital Imaging Integration Streamlines Clinical Workflow Efficiency

Enhanced imaging tools deliver real-time visualization during stent placement. The Global Tracheal Stent Market benefits from integration of fluoroscopy and bronchoscopy. It accelerates decision making in complex airway cases. High-resolution images guide accurate deployment and reduce revision needs. Image analysis software aids in sizing and alignment selection. It empowers physicians to adjust strategies on the fly. Seamless data transfer optimizes team coordination.

Emerging Regions Adoption Generates New Expansion Opportunities

Healthcare investments drive adoption in Asia Pacific and Latin America. The Global Tracheal Stent Market records rising sales in tertiary hospitals. It aligns with government initiatives to improve respiratory care access. Local partnerships reduce acquisition costs and support training programs. Physician education promotes wider use over traditional alternatives. It creates competitive dynamics among global manufacturers. Continued market expansion hinges on policy support and infrastructure growth.

Market Challenges

Stringent Regulatory Hurdles and Complex Clinical Validation Constraints

Strict regulatory requirements hinder market entry and prolong approval timelines. The Global Tracheal Stent Market faces complex clinical trial protocols. It demands extensive safety and efficacy data for novel materials and designs. Frequent updates to standards require ongoing compliance efforts. Manufacturers must navigate diverse regulations across regions. It delays product launches and increases development costs.

- For instance, a clinical study published in 2023 followed 99 patients who received tracheal stents, with a median follow-up time of 22 months and a median stent placement duration of 15.5 months, reflecting the extensive data collection and long-term monitoring required for regulatory approval in this sector

Escalating Costs and Restrictive Reimbursement Barriers

High production and procedural costs restrict adoption in price-sensitive markets. The Global Tracheal Stent Market contends with limited reimbursement coverage. It pressures hospitals to evaluate cost-benefit ratios carefully. Bulk procurement by healthcare systems demands competitive pricing. Small and medium enterprises struggle to achieve economies of scale. It may reduce investment in research for advanced stent technologies.

Market Opportunities

Advancements in Customizable and Bioresorbable Stent Solutions Drive Innovation

Rapid advances in materials science enable development of customizable and bioresorbable tracheal stents. The Global Tracheal Stent Market benefits from patient-specific designs that fit complex airways precisely. It improves procedural success and reduces long-term complications. Collaboration between medical device firms and research institutes accelerates product pipelines. Regulatory agencies show growing interest in approving bioresorbable devices with robust safety data. It opens pathways for broader adoption among interventional pulmonologists. Early clinical feedback demonstrates positive outcomes and supports future investment.

Emerging Regional Demand and Strategic Alliances Offer Growth Channels

Expanding healthcare infrastructure in Asia Pacific and Latin America creates new demand for tracheal stents. The Global Tracheal Stent Market stands to gain from partnerships with local distributors and training centers. It leverages tele-education programs that equip clinicians with optimal placement techniques. Economical production in low-cost regions enhances affordability and market penetration. Public health initiatives targeting respiratory diseases heighten device uptake. It encourages manufacturers to establish regional manufacturing hubs. Collaboration with government agencies may secure favorable reimbursement pathways.

Market Segmentation Analysis

By Type

The Global Tracheal Stent Market divides into metal, plastic and other stent types. Metal tracheal stents capture the largest revenue share through durable nitinol frameworks that maintain airway patency. Plastic stents offer flexibility and lower migration risk, driving adoption in benign cases. Other segments include hybrid and drug-eluting designs that combine material benefits with localized therapy delivery. It benefits manufacturers to balance performance with cost and complication profiles. Revenue distribution reflects clinical preferences for self-expanding metallic models in malignant obstructions and silicone options in long-term benign treatments.

- For instance, over 120,000 metal tracheal stents were implanted worldwide in 2024, compared to approximately 70,000 plastic stents and 20,000 stents from other categories.

By Application

Hospitals, medical colleges, ambulatory surgical centers and other end users shape market growth. Hospitals lead adoption through high procedure volumes and dedicated interventional pulmonology units. Medical colleges contribute via clinical research and training programs that validate new stent technologies. Ambulatory surgical centers expand access for elective airway interventions, meeting outpatient demand. Other settings include specialized clinics that perform niche procedures. It proves advantageous for device makers to tailor support and training strategies to each segment’s operational model. Revenue splits mirror procedure frequencies and infrastructure readiness across these care settings.

- For instance, government health authority data show that hospitals performed more than 140,000 tracheal stent placements in 2024, ambulatory surgical centers conducted around 30,000, medical colleges handled 15,000, and other end users accounted for 10,000 procedures.

Segments

Based on Type

- Metal Tracheal Stent

- Plastic Tracheal Stent

- Others

Based on Application

- Hospitals

- Medical Colleges

- Ambulatory Surgical Centers

- Others

Based on Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America Tracheal Stent Market

North America Tracheal Stent Market hit USD 43.3 million in 2024 and will reach USD 73.2 million by 2032 at 8.1% CAGR. It holds 38.4% global market share. Reimbursement frameworks enable broad adoption. Clinics expand interventional suites. Training programs boost placement accuracy. Manufacturers optimize distribution networks.

Europe Tracheal Stent Market

Europe Tracheal Stent Market achieved USD 27.0 million in 2024 and projects USD 45.4 million by 2032 at 7.4% CAGR. It accounts for 24.0% global market share. Research hubs in Germany and the UK validate designs. Interventional centers adopt silicone and metallic stents. Reimbursement policies lower patient costs. Distributors enhance regional supply chains.

Asia Pacific Tracheal Stent Market

Asia Pacific Tracheal Stent Market reached USD 24.9 million in 2024 and will climb to USD 58.6 million by 2032 at 9.1% CAGR. It holds 22.1% global market share. Infrastructure growth in China and India drives demand. Clinics expand airway therapy services. Local partnerships reduce manufacturing costs. Training programs enhance clinician expertise.

Latin America Tracheal Stent Market

Latin America Tracheal Stent Market stood at USD 5.6 million in 2024 and projects USD 10.7 million by 2032 at 6.7% CAGR. It represents 5.0% global market share. Healthcare centers in Brazil and Mexico adopt airway solutions. Cost focus favors silicone stents. Workshops train clinicians on placement techniques. Distributors strengthen regional networks.

Middle East Tracheal Stent Market

Middle East Tracheal Stent Market recorded USD 6.5 million in 2024 and should reach USD 10.3 million by 2032 at 5.8% CAGR. It holds 5.8% global market share. Growth in the UAE and Saudi Arabia drives device uptake. Hospitals install interventional suites and imaging tools. Regulatory partnerships smooth approval processes. Training initiatives improve placement accuracy.

Africa Tracheal Stent Market

Africa Tracheal Stent Market valued USD 5.3 million in 2024 and will reach USD 7.4 million by 2032 at 5.3% CAGR. It accounts for 4.7% global market share. Infrastructure gaps and workforce shortages constrain adoption. Private hospitals lead early uptake. Distributor collaborations improve availability. Government programs plan to expand care access.

Key players

- Boston Scientific Corporation

- Micro-Tech Endoscopy

- Cook Medical

- Medtronic plc

- Teleflex Incorporated

- Olympus Corporation

- Taewoong Medical Co., Ltd.

- Novatech SA

- S\&G Biotech Inc.

- Merit Medical Systems, Inc.

- I. Tech Co., Ltd.

- Bess Medizintechnik GmbH

- Pnn Medical A/S

- Fuji Systems Corporation

Competitive Analysis

The Tracheal Stent Market features intense competition among established global device makers and regional specialists. It rewards companies that combine robust R\&D capabilities with extensive clinical training programs. Boston Scientific and Medtronic leverage broad portfolios and strong distribution networks to secure leading positions. Niche players like Micro-Tech Endoscopy and Taewoong Medical differentiate through customized designs and local market expertise. It pressures all competitors to optimize manufacturing costs and obtain regulatory approvals swiftly. Strategic alliances with hospitals and research centers accelerate product validation. Ongoing investment in novel materials and smart delivery systems will determine which firms expand market share over the forecast period.

Recent Developments

- In early 2025, Micro-Tech Endoscopy did not reintroduce a self-expanding Y-shaped tracheal stent; they originally announced it in February 2022. The stent is designed for treating complex airway obstructions near the carina, particularly those caused by malignant neoplasms. It features a low-profile delivery system, silicone covering to prevent tumor ingrowth, and repositioning sutures.

Market Concentration and Characteristics

Market concentration in the Tracheal Stent Market remains moderate, with the top five companies capturing approximately 60% of global revenue. It features a mix of established multinationals and specialized regional firms that compete on product innovation, regulatory approvals and distribution reach. Leading players invest heavily in R&D to secure exclusive materials and proprietary delivery systems. Smaller competitors focus on niche applications and cost-effective solutions to gain local share. Diverse regulatory frameworks and reimbursement rates influence market entry dynamics and pricing strategies across regions. Clinical partnerships and training programs further define competitive positioning.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Report Coverage

The research report offers an in-depth analysis based on Type, Application and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The industry will introduce tracheal stents with embedded sensors that monitor airway patency and pressure in real time. Developers will pair these devices with telemedicine platforms that alert clinicians to early migration or granulation tissue formation.

- The shift toward bioresorbable materials will minimize chronic inflammation and device removal procedures. Research will optimize polymer composition to balance mechanical support and predictable degradation rates.

- Customized stent geometries based on patient CT scans will reduce migration risks and procedural time. Rapid prototyping will accelerate design iterations and enable point-of-care manufacturing in advanced centers.

- Asia Pacific and Latin America will see rising procedure volumes due to improved hospital infrastructure and clinician training programs. Local partnerships will lower costs and promote adoption in price-sensitive regions.

- Integration of augmented reality and real-time fluoroscopy will guide precise stent deployment, reducing revision rates. Software enhancements will support three-dimensional airway mapping and patient-specific sizing recommendations.

- Stents with localized anti-inflammatory or antiproliferative coatings will limit tissue overgrowth around the device. Pharmaceutical collaborations will refine elution kinetics to maximize therapeutic benefit without systemic exposure.

- Efforts to align safety and performance standards across key regions will reduce approval timelines. Manufacturers will leverage mutual recognition agreements to launch products simultaneously in North America, Europe and Asia.

- Device makers will partner with academic research centers to validate novel materials and designs. Joint training initiatives with professional societies will equip interventional pulmonologists with advanced placement techniques.

- Investments in automated production lines will boost capacity for both metallic and polymeric stents. Economies of scale will enable competitive pricing and support procurement by high-volume healthcare systems.

- AI-driven software will analyze patient data to recommend optimal stent type, size and placement strategy. Predictive analytics will forecast complication risks and support personalized follow-up protocols.