Market Overview

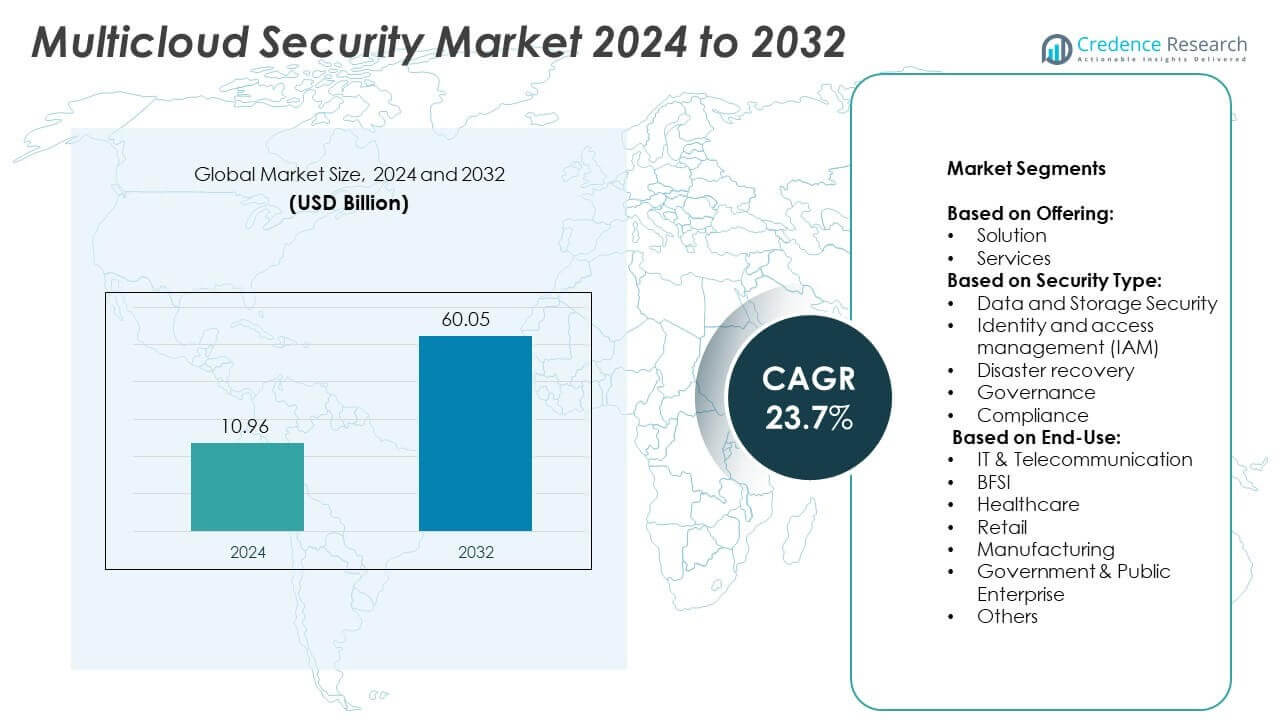

Multicloud Security Market size was valued at USD 10.96 Billion in 2024 and is anticipated to reach USD 60.05 Billion by 2032, at a CAGR of 23.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Multicloud Security Market Size 2024 |

USD 10.96 Billion |

| Multicloud Security Market, CAGR |

23.7% |

| Multicloud Security Market Size 2032 |

USD 60.05 Billion |

The Multicloud Security market grows due to increasing cloud adoption, rising cyber threats, and stricter data regulations. Enterprises demand centralized security platforms to manage complex multicloud environments efficiently. Trends such as zero-trust architecture, AI-driven threat detection, and data-centric protection shape product innovation. Organizations prioritize compliance, automation, and secure remote access across hybrid deployments. Security vendors respond by integrating identity controls, encryption tools, and policy enforcement features. This evolving landscape strengthens demand for flexible, scalable, and industry-specific security solutions.

North America leads the Multicloud Security market due to mature cloud infrastructure, strong regulatory frameworks, and high enterprise adoption. Europe follows with demand driven by GDPR compliance and rising focus on cloud sovereignty. Asia Pacific shows rapid growth supported by digital transformation across manufacturing, telecom, and finance sectors. Key players active across these regions include Google Cloud, IBM Corporation, Microsoft Corporation, and Wiz. These companies expand through partnerships, localized offerings, and investments in cloud-native security capabilities to meet region-specific requirements.

Market Insights

- The Multicloud Security market was valued at USD 10.96 Billion in 2024 and is projected to reach USD 60.05 Billion by 2032, growing at a CAGR of 23.7%.

- Rising demand for centralized cloud security, driven by growing hybrid deployments and strict compliance requirements, is fueling market expansion.

- Organizations are adopting zero-trust architecture, AI-powered threat detection, and automated compliance tools to secure complex multicloud environments.

- Leading companies such as Google Cloud, Microsoft Corporation, Wiz, and IBM Corporation invest in cloud-native security platforms and AI-enhanced analytics to stay competitive.

- Lack of standardization across cloud providers and shortage of skilled professionals hinder seamless security implementation across hybrid systems.

- North America dominates the market due to early technology adoption and strong cloud infrastructure; Europe and Asia Pacific follow with rising demand from regulated sectors.

- Vendors are focusing on region-specific compliance solutions, edge computing protection, and scalable platforms to meet evolving enterprise security needs globally.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Complexity of Hybrid and Multicloud Architectures Increases Need for Centralized Security Management

Enterprises are shifting toward hybrid and multicloud strategies to enhance scalability, resilience, and workload distribution. However, managing security across multiple cloud platforms—each with distinct configurations—poses serious risks. The Multicloud Security market is expanding because businesses need unified tools to oversee access control, policy enforcement, and threat response across cloud environments. Lack of visibility and inconsistent security policies make these systems vulnerable to breaches. Companies now demand integrated security solutions that consolidate management across public, private, and on-premise platforms. This trend supports strong demand for cross-cloud compliance and centralized monitoring frameworks.

- For instance, Industry statistics underscore the scale of cybersecurity challenges and the prevalence of lateral movement tactics, where attackers move deeper into networks after an initial breach. According to a Barracuda Networks study analyzing data from August 2023 to July 2024, nearly 44% of foiled ransomware attacks were detected during the lateral movement phase. Reports also indicate that over 25% of all cyberattacks involve lateral movement, a crucial stage in most advanced persistent threats

Escalating Cyber Threats and Sophisticated Attack Vectors Drive Security Prioritization Across Cloud Deployments

Cyberattacks targeting cloud environments are growing in scale and complexity. Threat actors exploit configuration errors, access gaps, and weak encryption protocols. The Multicloud Security market is responding to increasing enterprise focus on threat detection, incident response, and vulnerability management. Enterprises must now defend dynamic cloud infrastructures while maintaining service uptime. Security providers offer automated remediation, anomaly detection, and behavioral analytics to prevent lateral movement of attacks. It helps organizations avoid data breaches and reputational damage by reducing response time.

- For instance, According to reports from various cybersecurity firms and industry, enterprises in general can face a high volume of potential threats, with some receiving thousands of security alerts daily, and the average cost of a data breach in the healthcare sector is particularly high. In 2024, the average cost of a data breach in healthcare reached $9.77 million

Rising Compliance Pressure From Global Data Protection and Industry-Specific Regulations Fuel Security Investments

Governments worldwide enforce stricter data privacy and cloud governance mandates. Frameworks like GDPR, HIPAA, and CCPA require organizations to demonstrate full control over sensitive data across cloud platforms. The Multicloud Security market gains traction as enterprises seek tools to prove compliance and secure regulated workloads. Security platforms now include audit trails, policy management, and continuous compliance assessments. It ensures companies avoid legal penalties and meet audit demands efficiently. Regulatory complexity across borders further strengthens the need for specialized security solutions.

Surge in Remote Work and SaaS Adoption Highlights Need for Access Control and Secure Connectivity

Remote work accelerated cloud service usage and made endpoint protection more challenging. Organizations rely on SaaS tools, virtual desktops, and cloud collaboration platforms. The Multicloud Security market benefits from rising demand for identity management, single sign-on, and zero-trust frameworks. Security must now extend beyond traditional firewalls to remote users and unmanaged devices. It provides secure application access while maintaining user productivity. Vendors continue to enhance network segmentation and identity-based controls to meet this demand.

Market Trends

Increased Adoption of Zero Trust Architecture Across Multi-Vendor Cloud Environments

Organizations no longer trust internal or external networks by default. Zero Trust Architecture (ZTA) applies strict identity verification before granting access to any resource. The Multicloud Security market aligns with this shift, integrating zero trust principles into cloud security strategies. Enterprises use microsegmentation, least-privilege access, and continuous verification to limit lateral movement. It supports secure application access across hybrid cloud and edge environments. Vendors embed ZTA into identity management, workload protection, and API gateways.

- For instance, According to Okta’s “Businesses at Work 2024” report (based on 2023 data), the average number of applications deployed per company grew 4% year-over-year to 93

Integration of AI and Machine Learning to Automate Threat Detection and Response

AI and ML technologies now play a growing role in cloud threat analysis. These tools analyze large volumes of traffic and event data to detect anomalies faster than human analysts. The Multicloud Security market reflects this shift with intelligent platforms that identify attack patterns and trigger real-time responses. AI-driven systems enhance endpoint detection, behavioral analytics, and automated remediation. It helps reduce dwell time and improves incident resolution accuracy. Security vendors also use machine learning to refine policy recommendations.

- For instance, In a January 2025 study, Zylo reported that large enterprises (over 10,000 employees) used an average of 660 SaaS applications.

Shift Toward Unified Security Platforms for Centralized Monitoring and Cloud-Native Protection

Businesses increasingly demand centralized control over cloud workloads. Point solutions cause fragmented visibility, which hinders fast threat response. The Multicloud Security market trends toward unified platforms that offer comprehensive dashboards, workload discovery, and centralized policy enforcement. These platforms streamline operations by consolidating alerts and reducing redundant tools. It supports agile IT teams managing complex deployments across AWS, Azure, Google Cloud, and others. Market leaders now offer native integration with CI/CD pipelines and DevSecOps tools.

Rising Importance of Data-Centric Security to Protect Sensitive Assets Across Distributed Environments

Cloud environments create multiple data access points, making traditional perimeter security less effective. Enterprises focus on protecting data at rest, in motion, and in use. The Multicloud Security market supports this trend with encryption, tokenization, and rights management tools. It enables secure collaboration while controlling how data is shared or stored across platforms. Data-centric security also helps meet compliance mandates more efficiently. Vendors now offer policy-driven frameworks that classify and protect sensitive information automatically.

Market Challenges Analysis

Lack of Standardization Across Cloud Providers Complicates Security Policy Implementation

Each cloud provider has its own tools, configurations, and access control frameworks. This lack of standardization creates significant integration and management challenges. The Multicloud Security market must address compatibility gaps across platforms like AWS, Azure, and Google Cloud. Security teams struggle to maintain consistent policies, leading to potential misconfigurations and gaps in protection. It increases the risk of unauthorized access and data leakage. Vendors need to offer flexible solutions that adapt to provider-specific environments without sacrificing control.

Shortage of Skilled Professionals Limits Effective Multicloud Security Deployment

The growing complexity of multicloud environments requires specialized skills in cloud architecture and cybersecurity. However, the industry faces a global shortage of qualified professionals. The Multicloud Security market feels this constraint, as enterprises delay adoption or fail to maximize existing security investments. Security tools remain underutilized due to limited internal expertise. It places added pressure on automation and managed service offerings. Training programs and simplified interfaces must evolve to bridge this skills gap.

Market Opportunities

Growing Demand for Industry-Specific Multicloud Security Solutions Creates Niche Expansion Potential

Sectors like healthcare, finance, and government have distinct compliance, privacy, and workload security needs. Enterprises seek tailored solutions that align with their industry’s data handling and regulatory frameworks. The Multicloud Security market can tap into this demand by offering vertical-specific features such as HIPAA compliance modules or financial data encryption standards. Customizable frameworks and prebuilt policy templates simplify deployment in complex environments. It allows providers to differentiate offerings and build long-term client relationships. This niche-driven approach supports targeted growth across regulated industries.

Expansion of Edge Computing and IoT Devices Increases Demand for Distributed Security Models

Edge computing and connected devices are reshaping cloud network architectures. Data now flows across dispersed endpoints, edge nodes, and cloud cores. The Multicloud Security market sees strong opportunity in providing distributed security that covers edge workloads and device communication. Enterprises need scalable solutions to monitor and protect remote environments without adding complexity. It encourages development of lightweight agents, secure APIs, and identity-based controls. Companies that support edge-native security models can capture early growth in this evolving segment.

Market Segmentation Analysis:

By Offering:

The Multicloud Security market divides into solutions and services. Solutions dominate due to growing demand for integrated platforms that offer threat detection, access control, and encryption. Enterprises prioritize these tools to safeguard workloads across hybrid environments. Services segment grows steadily with rising need for deployment support, policy configuration, and managed security operations. It plays a key role for firms with limited in-house expertise or highly dynamic workloads. Growth in consulting and compliance audits further boosts the services segment.

- For instance, Stellar Cyber has partnered with RSM US LLP, which provides Managed Detection and Response (MDR) services using the Stellar Cyber platform. Through this partnership and the use of the platform, Stellar Cyber has stated that it has helped customers like RSM US LLP achieve over a 70% reduction in response times across 70,000 endpoints.

By Security Type:

Identity and access management (IAM) leads due to its core role in zero-trust frameworks. IAM ensures secure authentication and access permissions across cloud providers. Data and storage security follows closely, driven by strict data protection laws and enterprise concerns over cloud-based data leaks. Governance tools help companies enforce security policies, monitor compliance, and maintain centralized oversight. Compliance tools gain traction in regulated sectors like banking and healthcare. Disaster recovery shows strong adoption across industries that prioritize business continuity during outages or attacks. It supports fast workload restoration with minimal downtime.

- For instance, Tata Communications offers a managed security service that analyzes 25 million network flow records per minute using AI and ML to assist telecom operators. MSSPs allow telecom companies to leverage specialized expertise and resources to secure their infrastructure and maintain compliance, especially as workloads and data become more distributed.

By End-Use:

IT and telecommunication companies are the primary adopters due to their large-scale cloud infrastructure and dynamic applications. The Multicloud Security market expands in the BFSI sector where high-value transactions and regulatory requirements demand strict control. Healthcare follows, driven by the need to protect patient data and maintain HIPAA compliance. Retail invests in securing customer information and transaction platforms, especially with rising e-commerce volumes. Manufacturing firms deploy multicloud solutions for production monitoring and ERP integration, increasing demand for endpoint and API security. Government and public enterprises seek sovereignty, resilience, and data integrity, making multicloud protections essential. Others segment includes energy, logistics, and education, all adopting cloud services with tailored security needs.

Segments:

Based on Offering:

Based on Security Type:

- Data and Storage Security

- Identity and access management (IAM)

- Disaster recovery

- Governance

- Compliance

Based on End-Use:

- IT & Telecommunication

- BFSI

- Healthcare

- Retail

- Manufacturing

- Government & Public Enterprise

- Others

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of the Multicloud Security market, accounting for 39.2% of the global revenue in 2024. The region benefits from early cloud adoption, a mature IT ecosystem, and strong presence of leading cloud service providers such as Amazon Web Services, Microsoft Azure, and Google Cloud. Enterprises in the U.S. and Canada are aggressively adopting hybrid and multicloud strategies to support digital transformation, data analytics, and remote operations. With increasing cyber threats and strict regulations such as HIPAA, SOX, and the California Consumer Privacy Act (CCPA), companies prioritize robust security frameworks. The regional market is further supported by high spending on cybersecurity technologies, growing investments in AI-based threat detection, and adoption of zero-trust models. Government initiatives to secure critical infrastructure and the presence of numerous managed service providers also drive market momentum in North America. It remains a prime hub for multicloud innovation, product launches, and strategic partnerships in cloud security.

Europe

Europe represents the second-largest market with a share of 27.6% in 2024. The region’s growth is driven by strict data protection frameworks such as the General Data Protection Regulation (GDPR) and emerging EU-level cybersecurity policies. Countries like Germany, France, and the UK lead in cloud adoption and enforce cloud sovereignty initiatives to maintain data control. Enterprises across banking, healthcare, and public services increasingly rely on multicloud environments to enhance operational flexibility and meet localization requirements. The Multicloud Security market benefits from rising focus on secure data sharing, compliance monitoring, and user authentication. Cloud security vendors collaborate with European partners to deliver region-specific capabilities, including privacy-first architecture and encrypted services. It also sees growing demand for services from SMEs integrating public and private cloud platforms while seeking cost-effective and compliant security models.

Asia Pacific

Asia Pacific accounts for 19.3% of the Multicloud Security market in 2024, driven by rapid cloud expansion and rising digital transformation across key economies such as China, India, Japan, and South Korea. The region witnesses strong demand from IT, telecom, and manufacturing sectors deploying multicloud frameworks for scalability and disaster resilience. Large enterprises and startups alike prioritize securing distributed cloud workloads, particularly with growing risks of cyber espionage and ransomware. Regulatory measures such as India’s Digital Personal Data Protection Act and Japan’s APPI compliance standards further push organizations to enhance multicloud defenses. Cloud-native security tools offering real-time monitoring, IAM, and automated compliance are gaining popularity. Regional players and global providers continue to invest in data centers and security partnerships to strengthen in-market presence. It shows potential for fastest growth during the forecast period due to digital government initiatives and SME adoption in Southeast Asia.

Latin America

Latin America captures 8.1% of the global Multicloud Security market share in 2024. Brazil and Mexico drive most of the regional demand, supported by increased migration to cloud services across financial institutions, retail, and public agencies. Organizations invest in multicloud strategies to improve service availability and business continuity. However, cybersecurity skills shortage and limited regulatory enforcement still affect adoption rates. The market sees growing interest in managed security services, identity management, and endpoint protection to compensate for internal resource gaps. It also benefits from regional data protection laws, such as Brazil’s LGPD, encouraging organizations to implement structured security policies. Local providers partner with global vendors to deliver cost-effective solutions tailored to regional compliance and threat patterns.

Middle East and Africa

The Middle East and Africa hold a market share of 5.8% in 2024, showing steady growth with expanding digital infrastructure and increasing cloud adoption in countries such as the UAE, Saudi Arabia, and South Africa. Governments and large enterprises in the region prioritize secure cloud transformation, especially across sectors like oil & gas, banking, and healthcare. The Multicloud Security market benefits from national cybersecurity strategies and growing awareness of zero-trust architecture. With regional concerns around data localization and sovereignty, security solutions focused on workload encryption, governance, and access control gain traction. Providers invest in regional data centers and partner with local firms to comply with domestic regulations. The rise of smart city initiatives and digital government services continues to push demand for scalable and secure multicloud frameworks.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Google Cloud

- Wiz

- Fujitsu Ltd.

- IBM Corporation

- Cloud4C

- Lacework

- Microsoft Corporation

- Imperva

- Atos SE

- Amazon Web Services (Amazon)

- Palo Alto

- Proofpoint

Competitive Analysis

The competitive landscape of the Multicloud Security market features major players such as Google Cloud, Wiz, IBM Corporation, Microsoft Corporation, Imperva, Amazon Web Services, Cloud4C, Fujitsu Ltd., Lacework, Atos SE, Palo Alto, and Proofpoint. These companies focus on delivering comprehensive cloud-native security solutions tailored to hybrid and multicloud environments. Vendors compete by offering identity and access management, workload protection, data encryption, threat detection, and compliance automation. Large cloud providers integrate security functions directly into their platforms, enhancing visibility, scalability, and interoperability. Cybersecurity-focused firms provide advanced analytics, behavioral monitoring, and zero-trust frameworks to secure user access and workload integrity. Strategic partnerships with service integrators and managed security providers strengthen market presence and support global deployments. Players continuously invest in R&D to improve AI-driven threat response, automate policy enforcement, and reduce detection time. Many vendors also tailor solutions to meet the specific regulatory needs of sectors like BFSI, healthcare, and public services. Competitive differentiation depends on ease of integration, support for multi-vendor environments, and proven scalability across large enterprises. As multicloud adoption grows, vendors that deliver flexible, unified, and cost-effective security platforms will retain a strong foothold in the market.

Recent Developments

- In May 2025, Imperva launched its Elastic WAF (Web Application Firewall), which is powered by a new AI-infused security engine.

- In 2025, AWS announced the upcoming launch of its second Secret Cloud Region (Secret‑West Region), aimed at supporting classified U.S. government workloads.

- In 2024, Microsoft Corporation provides Microsoft Defender for Cloud with unified cloud-native security features across Azure, AWS, Google Cloud, with real-time security posture management, integrated XDR, and DevOps security enhancements as of 2024

Report Coverage

The research report offers an in-depth analysis based on Offering, Security Type, End-Use and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will grow with increasing adoption of hybrid and multicloud strategies by global enterprises.

- Organizations will prioritize integrated security platforms that offer centralized control across diverse cloud environments.

- AI and machine learning will play a larger role in threat detection, behavior analytics, and automated response.

- The shift toward zero-trust frameworks will drive innovation in identity and access management solutions.

- Compliance demands will grow due to evolving regional and industry-specific data protection regulations.

- Cloud-native security solutions will expand to support containerization, microservices, and edge computing.

- Demand for industry-specific multicloud security tools will rise in finance, healthcare, and government sectors.

- Partnerships between cloud service providers and cybersecurity firms will strengthen to offer end-to-end protection.

- Organizations will invest in employee training and managed services to address the cloud security skills gap.

- Multicloud security adoption will accelerate in emerging markets due to increasing digital transformation initiatives.