Market Overview:

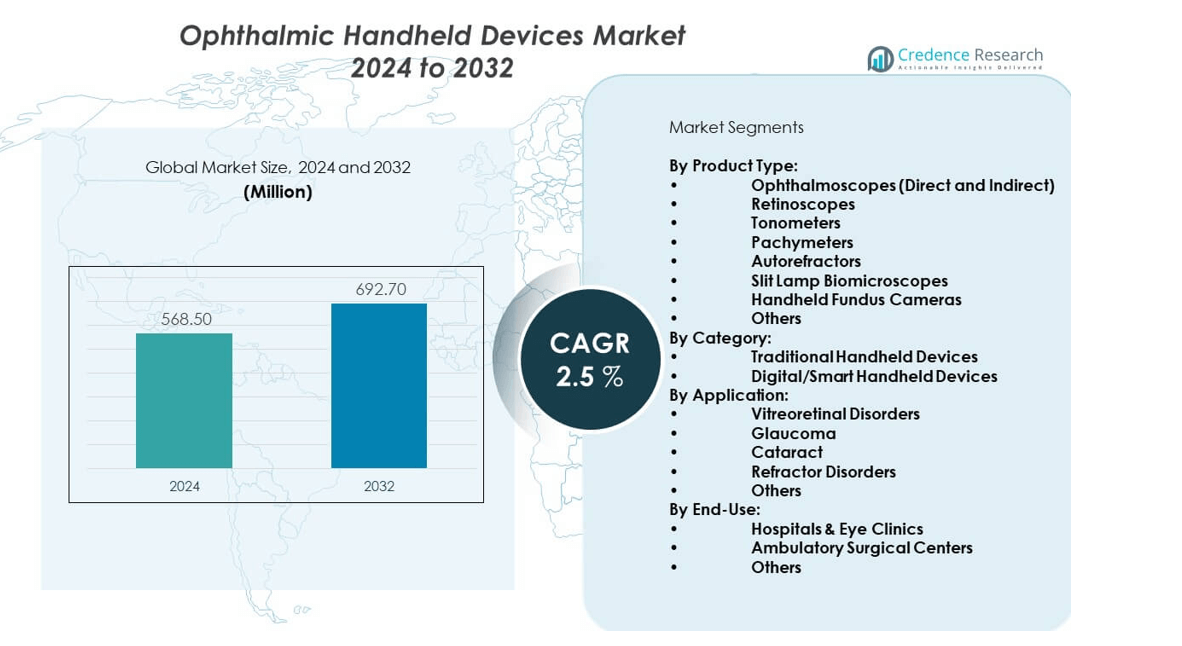

The ophthalmic handheld devices market is projected to grow from USD 568.5 million in 2024 to an estimated USD 692.7 million by 2032, reflecting a compound annual growth rate (CAGR) of 2.5% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ophthalmic Handheld Devices Market Size 2024 |

USD 568.5 million |

| Ophthalmic Handheld Devices Market , CAGR |

2.5% |

| Ophthalmic Handheld Devices Market Size 2032 |

USD 692.7 million |

Market growth is supported by an increase in global eye disorders such as cataracts, glaucoma, and age-related macular degeneration. Rising awareness of early detection and the need for convenient diagnostic solutions are further propelling demand. Healthcare providers are adopting these devices due to their portability, cost-effectiveness, and ability to deliver quick results in primary care and remote locations. The integration of digital platforms with handheld devices also strengthens clinical decision-making and patient monitoring.

Regionally, North America leads the ophthalmic handheld devices market due to strong healthcare infrastructure, higher adoption of advanced diagnostic technologies, and growing prevalence of vision disorders. Europe follows closely, supported by an expanding elderly population and favorable healthcare programs. Asia-Pacific is emerging as the fastest-growing region, driven by rising healthcare investments, increasing awareness of eye health, and unmet medical needs in rural areas. Latin America and the Middle East & Africa show gradual adoption, encouraged by improving healthcare facilities and government-led eye care initiatives.

Market Insights:

- The ophthalmic handheld devices market was valued at USD 568.5 million in 2024 and is expected to reach USD 692.7 million by 2032, growing at a CAGR of 2.5%.

- Growing prevalence of cataracts, glaucoma, and diabetic retinopathy is fueling demand for portable diagnostic tools.

- Technological advancements, including compact imaging systems and digital integration, are driving greater adoption in clinical and community settings.

- Limited awareness in low-resource regions and regulatory compliance hurdles remain key restraints for market expansion.

- North America leads the market due to advanced healthcare infrastructure and strong adoption of innovative diagnostic technologies.

- Europe shows steady growth supported by an aging population and favorable healthcare programs.

- Asia-Pacific is the fastest-growing region, driven by healthcare investments, rising awareness of eye care, and expanding screening programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Burden of Eye Disorders and Growing Need for Early Detection:

The ophthalmic handheld devices market is strongly driven by the growing burden of eye disorders worldwide. Increasing prevalence of cataracts, glaucoma, and diabetic retinopathy is creating steady demand for portable diagnostic solutions. Healthcare systems are prioritizing early detection to reduce complications and improve patient outcomes. Handheld devices provide a faster, cost-effective, and convenient option compared to large stationary equipment. Physicians prefer these tools for community health camps, outpatient clinics, and rural practices. The growing elderly population further expands the patient base requiring regular eye checkups. Preventive healthcare policies and awareness programs are also boosting the adoption of handheld devices. It positions the market as a critical enabler of timely and accessible vision care.

- For instance, Welch Allyn’s PanOptic ophthalmoscope enables rapid eye examination with a 25-degree wider field of view compared to traditional ophthalmoscopes, facilitating earlier detection of retinal abnormalities in over 150,000 screenings conducted in community settings globally.

Technological Advancements and Digital Integration in Diagnostic Tools:

Innovation in handheld ophthalmic tools is fueling their widespread adoption across healthcare systems. Advances in digital imaging and connectivity have made these devices more accurate, reliable, and user-friendly. Integration with mobile platforms allows data sharing, remote monitoring, and telemedicine applications. Cloud-enabled systems also enhance storage and analysis of patient records for better follow-up. Miniaturization has made devices lighter, easier to carry, and suitable for varied healthcare environments. Portable fundus cameras, tonometers, and autorefractors are now widely used by specialists. Such advancements increase diagnostic precision and patient confidence in treatments. The ophthalmic handheld devices market is benefiting from a wave of innovation reshaping diagnostic care.

- For instance, AI Optics’ portable Sentinel Camera, approved by FDA in January 2025, captures high-quality retinal images without dilation, integrates with electronic health records (EHR), and increases access to retinal screening.

Expanding Reach of Community Healthcare and Remote Eye Screening Programs:

Community health initiatives are significantly influencing the adoption of handheld ophthalmic devices. Governments and NGOs are deploying portable devices for rural and underserved populations. Screening programs for school children, elderly groups, and diabetics depend heavily on these tools. Handheld devices provide mobility and speed that traditional setups cannot match. They allow ophthalmologists to serve more patients with limited infrastructure. Partnerships with healthcare outreach programs further boost accessibility. Growing emphasis on preventive eye health supports long-term demand. It ensures that handheld devices remain essential to improving global vision care equity.

Cost Efficiency and Growing Preference for Affordable Diagnostic Solutions:

Affordability of handheld ophthalmic tools is a major driver of their adoption. Healthcare providers and small practices often face budget constraints for large, expensive diagnostic equipment. Handheld devices offer a practical balance between cost, portability, and functionality. Clinics in developing regions prefer such devices to expand patient access at lower cost. Rising healthcare expenditure pressures are pushing governments and institutions toward cost-efficient solutions. Portable devices also reduce the need for specialized infrastructure and space. Patients benefit from quicker checkups without significant added costs. The ophthalmic handheld devices market thrives on the demand for practical, budget-friendly diagnostic alternatives.

Market Trends:

Growing Adoption of Teleophthalmology and Remote Diagnostic Services:

Teleophthalmology is creating new opportunities for handheld device integration. Clinicians are increasingly using these tools for remote screening and virtual consultations. Devices that capture and transmit images directly to specialists improve access for remote patients. Cloud storage and AI-driven analysis enhance efficiency in telehealth models. This trend is transforming the delivery of eye care across both developed and emerging regions. Hospitals and clinics adopt such solutions to reduce patient backlog and streamline care. Insurance providers also support telehealth-based screenings for broader reach. The ophthalmic handheld devices market aligns closely with this digital transformation of healthcare.

Increasing Role of Artificial Intelligence in Clinical Decision-Making:

Artificial intelligence integration is becoming a defining trend for handheld ophthalmic devices. AI-powered diagnostic platforms can detect signs of diseases with high accuracy. These tools help clinicians improve diagnostic speed and reduce errors in early screening. AI algorithms analyze images from handheld fundus cameras or optical devices with greater precision. Such solutions enhance healthcare provider confidence in managing complex conditions. They also support non-specialists in primary care centers, widening the reach of diagnostics. AI-driven handheld devices are being adopted in both advanced and resource-limited settings. This trend is expected to elevate efficiency within the ophthalmic handheld devices market.

- For instance, the AI-enabled RetinaVue 700 from Welch Allyn has demonstrated a diagnostic accuracy rate exceeding 87% in detecting diabetic retinopathy, across clinical trials involving over 5,000 patients.

Rising Demand for Portable Devices in Pediatric and Geriatric Care:

Pediatric and geriatric populations are increasing the demand for easy-to-use handheld devices. Children and elderly patients often require frequent and non-invasive eye examinations. Handheld tools provide comfortable, quick, and patient-friendly diagnostics. Devices are being designed with ergonomic features to enhance usability in diverse age groups. Home-based healthcare providers also adopt such devices for bedside screenings. The need for accessible tools is particularly strong in aging populations with chronic eye conditions. Pediatric screenings are supported by government initiatives in schools and child health programs. It strengthens the demand pipeline for the ophthalmic handheld devices market.

- For instance, Home monitoring tools with digital integration facilitate bedside examinations and frequent screenings, especially crucial for elderly patients managing chronic eye conditions like glaucoma.

Expanding Use of Handheld Tools in Clinical Research and Screening Trials:

Clinical research programs are leveraging handheld devices to increase trial efficiency. Portable tools simplify data collection across diverse patient groups in multiple locations. Researchers value mobility and precision in large-scale vision screening studies. Pharmaceutical companies adopt handheld devices for drug trials targeting ophthalmic conditions. Nonprofit organizations use them to study the prevalence of eye diseases in developing regions. Such research efforts validate the reliability and importance of handheld diagnostics. Growing use in academic and commercial research enhances product acceptance. It reinforces the value of handheld devices within the ophthalmic handheld devices market.

Market Challenges Analysis:

Regulatory Compliance and Standardization Barriers in Device Adoption:

The ophthalmic handheld devices market faces significant regulatory and compliance hurdles. Each device must meet stringent approval standards to ensure safety and accuracy. Different countries maintain unique guidelines, creating delays in global product launches. Small manufacturers often struggle with the cost and complexity of certifications. Lack of universal testing standards limits interoperability and global adoption. Uncertainty in compliance procedures discourages investment in emerging markets. These challenges slow down innovation and market entry of new products. It remains a critical factor hindering overall market expansion.

Limited Awareness, Infrastructure Gaps, and Competition with Conventional Equipment:

Awareness gaps about handheld devices in low-resource regions restrict growth potential. Many healthcare providers rely on conventional diagnostic equipment due to established familiarity. Infrastructure limitations in remote areas further reduce accessibility for advanced handheld tools. Power supply and connectivity challenges limit device use in rural healthcare centers. Competition from larger stationary diagnostic systems creates hesitation in replacement decisions. Training gaps among healthcare professionals reduce the effective utilization of portable tools. Cost concerns in underfunded healthcare systems add another barrier. The ophthalmic handheld devices market must address these gaps to strengthen adoption.

Market Opportunities:

Expanding Integration with Digital Health Ecosystems and Telemedicine Platforms:

Growing adoption of digital health platforms presents strong opportunities for handheld ophthalmic devices. Seamless integration with telemedicine networks allows providers to extend diagnostic services beyond traditional settings. Healthcare organizations invest in digital solutions that enhance connectivity, patient record management, and cloud-based storage. Portable ophthalmic tools paired with mobile apps can offer efficient remote eye care. This combination strengthens outcomes in underserved regions and supports preventive care programs. Opportunities lie in developing tools that align with global telehealth infrastructure. The ophthalmic handheld devices market can scale rapidly with digital health advancements.

Rising Demand in Emerging Markets and Community Health Programs:

Emerging economies present significant untapped potential for handheld ophthalmic devices. Governments in Asia-Pacific, Latin America, and Africa are increasing investments in eye care programs. Community health projects deploy mobile screening units equipped with handheld tools. Growing public awareness of eye health creates a favorable environment for adoption. Local partnerships and NGO involvement further expand reach in underserved populations. Demand is strong in both rural and semi-urban regions with limited infrastructure. It highlights an opportunity for manufacturers to target cost-effective, durable, and accessible solutions. The ophthalmic handheld devices market is positioned to gain from these expanding outreach programs.

Market Segmentation Analysis:

By Product Type

The ophthalmic handheld devices market is categorized into ophthalmoscopes (direct and indirect), retinoscopes, tonometers, pachymeters, autorefractors, slit lamp biomicroscopes, handheld fundus cameras, and others. Ophthalmoscopes and tonometers hold significant share due to their widespread use in routine eye examinations and glaucoma detection. Handheld fundus cameras and digital autorefractors are gaining traction as advanced screening tools, driven by their efficiency in remote and community healthcare programs.

- For instance, The handheld devices market includes ophthalmoscopes, tonometers, retinoscopes, pachymeters, autorefractors, slit lamps, and fundus cameras. Ophthalmoscopes and tonometers are dominant due to routine glaucoma and eye exams. Advanced digital autorefractors and handheld fundus cameras are rising in community health and remote screening applications.

By Category

Based on category, the market is segmented into traditional handheld devices and digital/smart handheld devices. Digital/smart handheld devices are expected to grow faster due to integration with teleophthalmology, mobile platforms, and cloud-based data systems. Their ability to enhance diagnostic precision, streamline patient records, and support remote consultations positions them as a key growth driver. Traditional devices still hold importance in low-resource settings due to affordability and ease of use.

- For instance, Digital and smart handheld devices, integrated with teleophthalmology platforms and cloud data systems, enhance precision diagnostics and facilitate remote consultations. They hold faster growth prospects compared to traditional devices. However, affordability maintains demand for traditional devices in low-resource settings.

By Application

The ophthalmic handheld devices market is segmented into vitreoretinal disorders, glaucoma, cataract, refractor disorders, and others. Devices for glaucoma and cataract applications dominate the market, supported by the high global prevalence of these conditions. Vitreoretinal and refractor disorder applications are witnessing growing demand, particularly with increasing adoption of handheld fundus cameras and autorefractors in outpatient care and community screenings.

By End-Use

By end-use, the market is divided into hospitals & eye clinics, ambulatory surgical centers, and others. Hospitals and eye clinics account for the largest share due to their advanced infrastructure and high patient flow. Ambulatory surgical centers are witnessing rising adoption of handheld devices owing to their portability, efficiency, and suitability for smaller, specialized care facilities.

Segmentation:

By Product Type:

- Ophthalmoscopes (Direct and Indirect)

- Retinoscopes

- Tonometers

- Pachymeters

- Autorefractors

- Slit Lamp Biomicroscopes

- Handheld Fundus Cameras

- Others

By Category:

- Traditional Handheld Devices

- Digital/Smart Handheld Devices

By Application:

- Vitreoretinal Disorders

- Glaucoma

- Cataract

- Refractor Disorders

- Others

By End-Use:

- Hospitals & Eye Clinics

- Ambulatory Surgical Centers

- Others

By Region

- North America

- Europe

- Germany

- France

- UK.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- The Rest of the Middle East and Africa

Regional Analysis:

North America and Europe

North America holds the largest share of the ophthalmic handheld devices market, supported by advanced healthcare infrastructure and strong adoption of innovative technologies. The region benefits from high awareness of eye health and a growing elderly population requiring frequent eye examinations. Government-led screening initiatives and insurance coverage further encourage usage of handheld diagnostic tools. The presence of leading players and continuous product innovation also drive the regional dominance. Europe follows with a substantial share, supported by universal healthcare systems and high demand for portable solutions in aging populations. Strong regulatory standards encourage manufacturers to launch advanced devices that meet clinical precision. Together, North America and Europe account for the majority share of the global market.

Asia-Pacific

Asia-Pacific represents the fastest-growing region in the ophthalmic handheld devices market, driven by increasing healthcare investments and expanding awareness of preventive eye care. Rising cases of cataracts, glaucoma, and refractive errors create strong demand for handheld diagnostic solutions. Governments across India, China, and Southeast Asia are introducing large-scale vision screening programs, particularly in rural areas. The affordability and portability of these devices make them ideal for regions with limited infrastructure. Local manufacturers are also entering the market with cost-effective options to meet rising demand. Favorable government policies and public-private partnerships further support market growth in this region. It continues to build momentum as healthcare access improves across emerging economies.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa together hold a smaller share of the ophthalmic handheld devices market but represent important growth opportunities. In Latin America, Brazil and Mexico are leading markets due to expanding healthcare systems and increasing investments in diagnostic technology. In the Middle East & Africa, growth is supported by rising healthcare infrastructure development and government focus on preventive health initiatives. NGOs and international organizations play a vital role in distributing portable ophthalmic devices in underserved communities. Limited awareness and infrastructure gaps continue to challenge adoption rates. However, increasing urbanization and a growing patient base with chronic eye disorders create a favorable environment for long-term growth. It positions these regions as promising markets for future expansion.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Topcon Corporation

- NIDEK CO., LTD.

- ZEISS International

- HEINE Optotechnik GmbH & Co. KG

- Kowa Company Ltd.

- Haag-Streit Group

- Appasamy Associates

- Katalyst Surgical

- ASICO, LLC

- INKA Surgical Instruments

- Surgical Holdings

Competitive Analysis:

The ophthalmic handheld devices market is highly competitive, featuring both multinational corporations and regional players. Companies compete on innovation, product range, pricing, and distribution reach. Topcon Corporation, NIDEK CO., LTD., ZEISS International, and Haag-Streit Group maintain strong positions through advanced technologies and global networks. HEINE Optotechnik GmbH, Kowa Company Ltd., and Appasamy Associates strengthen their presence with cost-effective and specialized solutions. Smaller players such as Katalyst Surgical and ASICO, LLC focus on niche offerings and customized devices. Partnerships with hospitals and research organizations enhance product adoption. It remains a market where technological differentiation and affordability define long-term leadership.

Recent Developments:

- In March 2025, Topcon Corporation announced a collaboration with RadiusXR and Glaukos to launch Inspire, a lightweight wearable glaucoma screening device. Topcon will serve as the exclusive global distributor of Inspire, combining wearable diagnostics with their digital health platform to expand access to visual field exams worldwide.

- In July 2025, Topcon Healthcare also partnered with OKKO Health, a UK-based software company, investing in their home vision monitoring platform that uses smartphone technology for personalized eye care and patient engagement.

- In December 2024, NIDEK Co., Ltd. launched globally its NP-T PreLoaded Toric IOL Injection System, designed for superior operability and safe lens delivery. This preloaded system had been previously available only in Japan and is now expanded outside the U.S. market.

- In June 2025, ZEISS International (Carl Zeiss Vision) announced the acquisition of Brighten Optix, a leading provider of ortho-k and specialty contact lenses, broadening its myopia management portfolio and enhancing its presence in Greater China and Southeast Asia.

- In 2025, HEINE Optotechnik launched the new HEINE X Series of handheld diagnostic instruments, including the BETA X Otoscope and BETA X Ophthalmoscope. These products feature innovative optical systems, lighter durable materials, and interchangeable modules enhancing ophthalmic examination experience.

Report Coverage:

The research report offers an in-depth analysis based on product type, category, application, and end-use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising demand for digital and smart handheld devices integrated with AI platforms.

- Expansion of teleophthalmology fueling adoption in remote healthcare delivery.

- Growing prevalence of cataract and glaucoma driving sustained device usage.

- Emerging markets in Asia-Pacific offering strong opportunities for growth.

- Integration with electronic health records improving efficiency and adoption.

- Partnerships between manufacturers and NGOs enhancing rural healthcare access.

- Innovation in ergonomic and patient-friendly designs expanding use in pediatrics.

- Increasing focus on preventive eye care strengthening long-term demand.

- Portable devices gaining traction in academic research and clinical trials.

- Strong competition pushing companies toward continuous product innovation.