Market Overview:

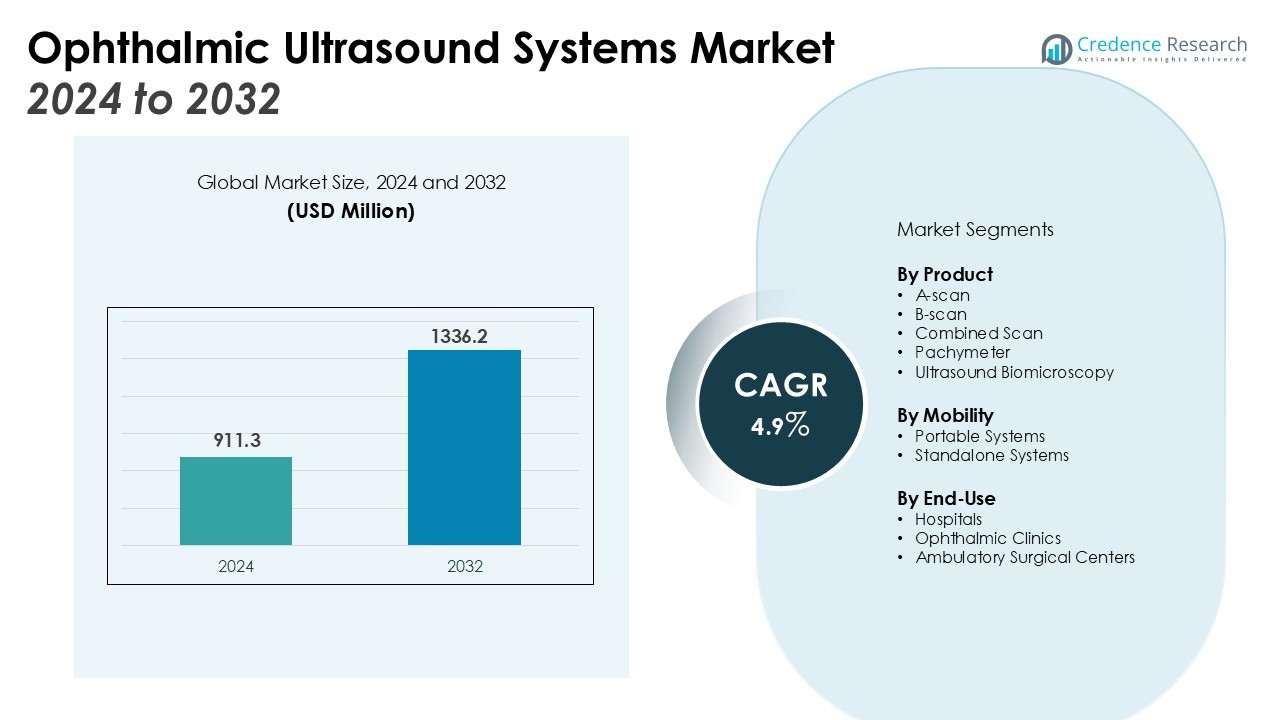

The Ophthalmic Ultrasound Systems Market size was valued at USD 911.3 million in 2024 and is anticipated to reach USD 1336.2 million by 2032, at a CAGR of 4.9% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Ophthalmic Ultrasound Systems Market Size 2024 |

USD 911.3 Million |

| Ophthalmic Ultrasound Systems Market, CAGR |

4.9% |

| Ophthalmic Ultrasound Systems Market Size 2032 |

USD 1336.2 Million |

Growth is primarily driven by the rising prevalence of eye diseases, such as cataracts, glaucoma, and retinal disorders. The growing elderly population, coupled with lifestyle changes that heighten the risk of visual impairments, is further accelerating adoption. Advancements in ultrasound probes, portability, and integration with other imaging modalities are also creating strong adoption opportunities across hospitals and specialty clinics. In addition, initiatives promoting early detection and treatment of eye diseases are strengthening demand globally.

Regional analysis highlights strong adoption in North America, supported by advanced healthcare infrastructure and significant patient awareness. Europe also maintains a substantial share, benefitting from well-established clinical practices and access to modern diagnostic tools. The Asia Pacific region is expected to experience the fastest growth, driven by expanding healthcare systems, large patient populations, and rising awareness of early eye disease management. Emerging markets in Latin America and the Middle East are also showing potential as healthcare access and investments in ophthalmology increase.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The Ophthalmic Ultrasound Systems Market was valued at USD 911.3 million in 2024 and is projected to reach USD 1336.2 million by 2032, advancing at a CAGR of 4.9%.

- Rising prevalence of cataracts, glaucoma, and retinal disorders is creating strong diagnostic demand across global healthcare systems.

- The growing elderly population combined with lifestyle-related risks is expanding the patient base for ophthalmic imaging solutions.

- Technological advancements in probes, portable models, and integrated platforms are enhancing diagnostic accuracy and workflow efficiency.

- North America holds 42% share, supported by advanced healthcare infrastructure, reimbursement frameworks, and high disease prevalence.

- Europe accounts for 28% share, benefitting from established clinical practices, screening programs, and healthcare modernization initiatives.

- Asia Pacific captures 22% share, recording the fastest growth, driven by large patient pools, rising investments, and growing awareness of early diagnosis.

Market Drivers:

Rising Prevalence of Eye Disorders Driving Demand

The Ophthalmic Ultrasound Systems Market is propelled by the increasing incidence of vision-threatening disorders. Conditions such as cataracts, glaucoma, and retinal diseases are becoming more common with aging populations worldwide. Early and accurate diagnosis is essential to prevent permanent vision loss, which strengthens the role of ultrasound imaging. Healthcare systems are prioritizing advanced tools that provide non-invasive and reliable assessments of ocular structures. This growing clinical need directly supports the adoption of ophthalmic ultrasound systems.

- For instance, Quantel Medical’s ABSolu system features a 20 MHz annular array probe that increases the depth of field by 70, enabling detailed imaging of the entire eye including vitreous and retina.

Expanding Elderly Population Increasing Diagnostic Requirements

An expanding elderly population is a significant driver of market growth. With age, individuals are more prone to chronic eye conditions requiring continuous monitoring and evaluation. Ophthalmic ultrasound systems offer a safe, repeatable, and cost-effective method to examine these patients. Hospitals and clinics are investing in these devices to meet the rising patient burden. The trend of increasing life expectancy globally continues to add momentum to the market.

Technological Advancements Enhancing System Efficiency

Ongoing advancements in imaging probes, portability, and system integration are reshaping market dynamics. Compact ultrasound systems with improved resolution and faster image acquisition are being adopted widely. It provides ophthalmologists with detailed insights into posterior eye structures that cannot be visualized directly. Integration with other diagnostic platforms also supports comprehensive eye care solutions. Continuous innovation strengthens confidence among practitioners and patients alike.

- For instance, Butterfly Network’s Butterfly iQ features the world’s first Ultrasound-on-a-Chip technology with nearly 10,000 integrated sensors in a single probe, the broadest FDA-cleared single ultrasound transducer ever released.

Growing Awareness and Supportive Healthcare Initiatives

Awareness campaigns and healthcare initiatives are encouraging earlier diagnosis and treatment of ocular diseases. Governments and organizations are focusing on reducing preventable blindness by promoting access to modern imaging devices. The Ophthalmic Ultrasound Systems Market benefits from these initiatives, particularly in developing regions where awareness is increasing rapidly. It creates opportunities for broader adoption in both public and private healthcare settings. Investments in healthcare infrastructure further accelerate the availability of advanced diagnostic systems.

Market Trends:

Integration of Advanced Imaging Technologies and Portable Solutions

The Ophthalmic Ultrasound Systems Market is experiencing a notable trend toward integration of advanced imaging capabilities and portable designs. Manufacturers are focusing on compact, high-resolution devices that can be deployed in both hospital and clinic settings. It offers improved diagnostic precision for conditions like retinal detachment, vitreous hemorrhage, and tumors where direct visualization is difficult. Portability enables use in remote or resource-limited areas, extending access to advanced eye care. The demand for devices that combine accuracy with ease of use is accelerating adoption globally. System upgrades with digital connectivity and automated image analysis further enhance workflow efficiency and clinical outcomes.

- For instance, FUJIFILM Sonosite’s Sonosite PX provides image resolution up to 15 MHz with a 15-inch touchscreen for easy bedside diagnostics.

Increasing Focus on Early Diagnosis and Preventive Eye Care

A growing trend emphasizes the importance of early diagnosis and preventive care in ophthalmology. Rising awareness of vision impairment risks has led to stronger demand for non-invasive imaging that supports timely intervention. The Ophthalmic Ultrasound Systems Market is benefiting from this shift, with healthcare providers adopting systems that deliver quick and reliable results. It supports initiatives aimed at reducing preventable blindness by enabling mass screenings and efficient patient management. Demand is also increasing in emerging economies where healthcare investments are expanding, and patient awareness is improving. The combination of policy support, technology development, and patient-centric care continues to shape long-term market growth.

- For instance, Ellex Inc.’s Eye Cubed ultrasound system offers an image acquisition rate of up to 25 frames per second, providing real-time detailed ocular imaging for faster diagnosis and enhanced patient care.

Market Challenges Analysis:

High Equipment Costs and Limited Accessibility in Developing Regions

The Ophthalmic Ultrasound Systems Market faces challenges related to high acquisition and maintenance costs. Advanced devices with enhanced imaging capabilities often remain unaffordable for small clinics and facilities in developing economies. It restricts widespread adoption, especially where healthcare budgets are limited. Limited reimbursement policies for diagnostic imaging also create financial barriers for both providers and patients. Shortages of skilled professionals who can operate specialized systems further hinder growth in underserved regions. These factors collectively slow down penetration in markets where demand for affordable eye care is rising.

Technological Complexity and Competitive Alternatives

The market encounters challenges from technological complexity and the presence of competing diagnostic modalities. While ultrasound provides valuable insights, ophthalmologists often prefer OCT and MRI for certain conditions due to higher resolution and broader applications. It places pressure on ultrasound manufacturers to continuously innovate and maintain relevance. Training requirements and potential misinterpretation of results also create risks for clinical accuracy. Regulatory hurdles for new product approvals can delay commercialization and limit timely adoption. Such challenges require consistent innovation and supportive policies to sustain market growth.

Market Opportunities:

Expansion Potential in Emerging Healthcare Markets

The Ophthalmic Ultrasound Systems Market holds significant opportunities in emerging economies where healthcare infrastructure is expanding rapidly. Rising investments in hospital facilities and diagnostic centers are creating demand for cost-effective imaging technologies. It allows healthcare providers to meet growing patient needs for early detection of cataracts, glaucoma, and retinal disorders. Government programs focused on reducing preventable blindness further open pathways for adoption in underserved areas. Increasing collaborations between international manufacturers and local distributors are also supporting market penetration. The combination of improved access, policy support, and rising awareness presents strong long-term opportunities.

Technological Innovation and Integration with Digital Platforms

Opportunities also stem from continuous technological innovation and integration with digital healthcare platforms. Advanced probes, portable models, and AI-enabled imaging features are reshaping system capabilities. It enhances diagnostic accuracy and reduces reliance on manual interpretation, improving patient outcomes. Integration with electronic medical records and teleophthalmology platforms further strengthens utility in modern healthcare ecosystems. Growing demand for multifunctional systems that combine speed, precision, and connectivity is likely to accelerate adoption. These innovations create competitive advantages for manufacturers and unlock new growth avenues across global markets.

Market Segmentation Analysis:

By Product

The Ophthalmic Ultrasound Systems Market is segmented into A-scan, B-scan, combined scan, pachymeter, and ultrasound biomicroscopy. Each category addresses specific diagnostic requirements, with B-scan systems preferred for posterior segment evaluations and A-scan systems vital in cataract surgeries for accurate axial length measurement. Combined scan devices are gaining popularity due to their dual capability, while pachymeters and biomicroscopy units support anterior segment and corneal assessments. It reflects the market’s shift toward specialized diagnostic tools that meet diverse ophthalmic needs.

- For instance, Topcon SP-2000P pachymeter measures corneal thickness with a mean difference of 32 micrometers compared to ultrasound pachymetry and provides consistent readings across operators.

By Mobility

Segmentation by mobility includes portable and standalone systems. Portable devices are gaining traction due to their compact form, ease of use, and suitability for community outreach programs. Standalone systems continue to see steady demand in hospitals and specialty centers where advanced imaging is prioritized. Portability expands diagnostic access in rural and resource-limited regions, creating new opportunities for adoption. It emphasizes how mobility influences investment decisions by healthcare providers.

By End-Use

End-use segments include hospitals, ophthalmic clinics, and ambulatory surgical centers. Hospitals hold the largest share due to high patient inflow and established infrastructure that supports integration of multiple imaging systems. Ophthalmic clinics are adopting these systems to strengthen specialized care and focus on early detection of vision-threatening conditions. Ambulatory surgical centers contribute to growth, supported by rising outpatient procedures and demand for cost-effective diagnostics. It demonstrates the broad relevance of ophthalmic ultrasound systems across varied healthcare environments.

- For instance, UH Rainbow’s Pediatric Research and Innovation in Sight & Motility (PRISM) Clinic uses this advanced 3-D ophthalmic ultrasound technology that provides intricately detailed views of eye tissues, crucial for early intervention in glaucoma, cataracts, and tumors.

Segmentations:

By Product

- A-scan

- B-scan

- Combined Scan

- Pachymeter

- Ultrasound Biomicroscopy

By Mobility

- Portable Systems

- Standalone Systems

By End-Use

- Hospitals

- Ophthalmic Clinics

- Ambulatory Surgical Centers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Strong Market Presence in North America

North America holds 42% share of the Ophthalmic Ultrasound Systems Market, making it the largest regional contributor. The region benefits from advanced healthcare infrastructure and early adoption of innovative diagnostic devices. It gains strength from high prevalence of glaucoma, diabetic retinopathy, and other ocular conditions that require frequent imaging. Favorable reimbursement structures and government-backed preventive care programs enhance accessibility to these systems. The presence of leading research institutions and specialized clinics accelerates integration of ultrasound into clinical workflows. Growing investments in high-performance imaging technologies continue to support regional leadership.

Established Clinical Practices Supporting Europe’s Growth

Europe accounts for 28% share of the Ophthalmic Ultrasound Systems Market, supported by widespread diagnostic infrastructure and robust clinical practices. Strong demand for non-invasive imaging solutions aligns with the region’s aging population and increasing eye health concerns. It is reinforced by national screening programs and targeted awareness campaigns to reduce preventable blindness. Hospitals and specialty clinics across Germany, France, and the U.K. are adopting advanced systems to improve diagnostic accuracy. Supportive regulatory frameworks and continuous healthcare modernization programs maintain steady growth across the region. Investments in upgrading ophthalmic care facilities further strengthen adoption.

Rapid Expansion Across Asia Pacific and Emerging Economies

Asia Pacific captures 22% share of the Ophthalmic Ultrasound Systems Market, recording the fastest growth among all regions. The market expansion is fueled by large patient pools, rising healthcare spending, and increasing awareness of early diagnosis. It is driven strongly by China and India, where public and private investments in ophthalmology are accelerating. Government-led programs to expand rural healthcare infrastructure further enhance system accessibility. Collaborations between international manufacturers and regional providers make advanced ultrasound devices more affordable. Emerging markets in Latin America and the Middle East are also gaining momentum with improving healthcare infrastructure and rising demand for modern eye diagnostics.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Sonomed Escalon

- APPASAMY ASSOCIATES

- NIDEK CO., LTD

- DGH Technology, Inc

- Metrovision

- Quantel Medical

- Optos

- Alcon (Novartis)

- Halma

- MicroMedical Devices

- Carl Zeiss Meditec AG

Competitive Analysis:

The Ophthalmic Ultrasound Systems Market features a competitive landscape shaped by technology-driven companies focusing on innovation and product differentiation. Key players emphasize advanced imaging capabilities, portability, and integration with digital healthcare platforms to strengthen market presence. It is defined by continuous research and development investments aimed at enhancing diagnostic accuracy and usability. Companies are also expanding global reach through strategic collaborations, distribution partnerships, and regulatory approvals in high-growth regions. Competitive intensity is influenced by pricing strategies, product portfolios, and after-sales support that cater to diverse clinical settings. Firms that successfully balance cost efficiency with advanced features are gaining stronger adoption in both developed and emerging healthcare markets. The market competition remains dynamic, with sustained emphasis on innovation and accessibility shaping long-term positioning.

Recent Developments:

- In December 2024, NIDEK announced the global launch of the NP-T Preloaded Toric IOL Injection System, making it available worldwide except in the United States.

- In February 2025, Optos announced the launch of MonacoPro, its next-generation ultra-widefield retinal imaging solution, with shipping scheduled to commence in March 2025.

- In May 2025, Alcon received U.S. Food and Drug Administration (FDA) approval for Tryptyr, a new prescription eye drop designed to treat dry eye disease.

Report Coverage:

The research report offers an in-depth analysis based on Product, Mobility, End-Use and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Ophthalmic Ultrasound Systems Market will expand steadily, driven by increasing demand for advanced ocular diagnostics.

- Rising prevalence of cataracts, glaucoma, and retinal disorders will sustain strong clinical need.

- Growing elderly populations worldwide will continue to boost adoption of non-invasive imaging tools.

- Portable ultrasound systems will gain higher traction due to convenience and suitability for outreach programs.

- Integration of artificial intelligence and digital platforms will enhance diagnostic precision and workflow efficiency.

- Hospitals will remain dominant end-users, while ophthalmic clinics and surgical centers will increase adoption.

- North America will maintain leadership with advanced infrastructure and strong awareness of eye health.

- Europe will retain significant share, supported by established clinical practices and modernization programs.

- Asia Pacific will experience the fastest growth, supported by large patient pools and rising healthcare investments.

- Emerging economies in Latin America and the Middle East will provide new opportunities as healthcare access expands.