Market Overview

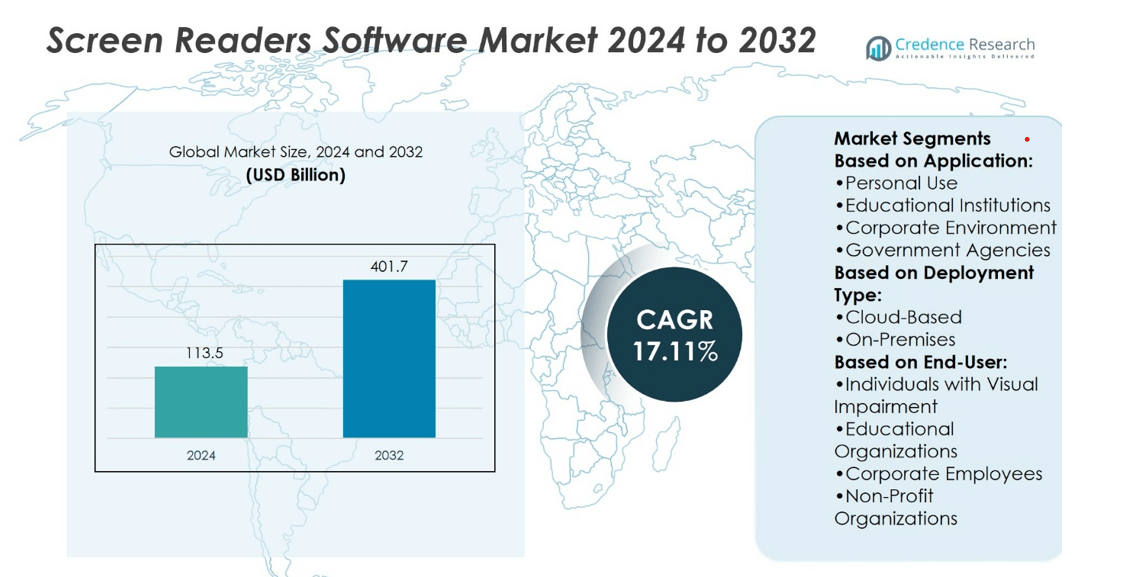

Screen Readers Software Market size was valued at USD 113.5 billion in 2024 and is anticipated to reach USD 401.7 billion by 2032, at a CAGR of 17.11% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Screen Readers Software Market Size 2024 |

USD 113.5 billion |

| Screen Readers Software Market, CAGR |

17.11% |

| Screen Readers Software Market Size 2032 |

USD 401.7 billion |

The Screen Readers Software Market grows through strong drivers such as increasing demand for digital accessibility, rising adoption of assistive technologies, and supportive government regulations mandating inclusive design. It benefits from expanding integration of screen readers into operating systems and mobile devices, which enhances usability and broadens access for visually impaired users. Trends highlight the use of artificial intelligence for natural-sounding voices, improved contextual understanding, and multilingual capabilities that meet global needs. It also shows momentum from the education and corporate sectors, where inclusivity initiatives and compliance requirements fuel consistent demand and encourage ongoing product innovation.

The Screen Readers Software Market demonstrates strong presence across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with North America leading due to advanced adoption of assistive technologies and regulatory support. Europe follows with emphasis on accessibility standards, while Asia-Pacific shows rapid growth from expanding digital literacy and mobile penetration. Key players shaping the market include Freedom Scientific, NV Access, Apple, Microsoft, Dolphin Computer Access, and Kurzweil Education, each driving innovation and expanding accessibility worldwide.

Market Insights

- The Screen Readers Software Market size was valued at USD 113.5 billion in 2024 and is projected to reach USD 401.7 billion by 2032, at a CAGR of 17.11%.

- Growing demand for digital accessibility and assistive technologies drives market expansion.

- Artificial intelligence integration improves natural voice quality, contextual accuracy, and multilingual support.

- Competition remains strong with established vendors leading innovation and open-source solutions widening access.

- High development costs and technical complexities act as restraints for new entrants.

- North America leads the market due to advanced adoption and regulatory mandates, while Europe follows with strict accessibility standards.

- Asia-Pacific emerges as the fastest-growing region, driven by digital literacy and mobile adoption.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Rising Demand for Inclusive Digital Solutions

The growing emphasis on digital accessibility across public and private sectors drives the Screen Readers Software Market. Governments and organizations implement strict compliance guidelines such as WCAG and ADA, creating consistent demand for solutions that ensure inclusivity. Businesses recognize that accessible platforms improve user engagement and customer retention, leading them to adopt advanced screen readers. It supports individuals with visual impairments by enabling equal participation in education, employment, and daily communication. The market gains momentum from this shift toward inclusivity, making accessibility a business imperative. Strong awareness campaigns and advocacy by disability rights groups reinforce this growth driver.

- For instance, WebAIM’s 2023–2024 Screen Reader User Survey collected responses from 1,539 participants and found that approximately 40.5% cited JAWS as their primary desktop or laptop screen reader, while 37.7% selected NVDA.

Expanding Adoption of Cloud-Based and Mobile Platforms

The widespread use of smartphones and cloud-based platforms accelerates the adoption of screen reader software. Mobile operating systems integrate accessibility features, which increases exposure and usage of screen readers among diverse demographics. It benefits users by offering seamless access to apps, documents, and web content anytime and anywhere. Enterprises also leverage cloud solutions to deliver scalable and cost-efficient accessibility tools. This trend strengthens the position of screen readers as essential components of the digital ecosystem. The Screen Readers Software Market thrives on these advancements, ensuring flexibility and ease of access across devices.

- For instance, Apple had sold more than 3 billion iPhones, all equipped with built-in VoiceOver screen reader capability, significantly broadening access to mobile accessibility tools across general and assistive user populations worldwide.

Technological Advancements in Artificial Intelligence and Voice Processing

Ongoing improvements in artificial intelligence and natural language processing elevate the functionality of screen readers. Enhanced speech synthesis delivers clearer, more human-like voices, improving the overall user experience. It enables quicker interpretation of complex layouts, images, and multilingual content, making screen readers more versatile. AI-driven customization allows personalized voice preferences and adaptive learning based on user habits. These innovations increase efficiency for professionals, students, and everyday users relying on accessibility support. The market benefits from continuous research investments that broaden the scope of practical applications.

Rising Education and Employment Accessibility Initiatives

Global initiatives to improve accessibility in education and workplaces contribute strongly to market expansion. Universities adopt screen readers to ensure compliance with accessibility regulations and foster equal opportunities for students. Employers integrate these solutions to support visually impaired employees and meet diversity goals. It drives adoption not only in advanced economies but also in emerging markets where awareness is increasing. Public institutions and NGOs also invest in awareness programs and subsidized technology distribution. The Screen Readers Software Market gains resilience from these collective efforts, establishing accessibility as a fundamental right rather than an optional feature.

Market Trends

Growing Integration with Mainstream Operating Systems

Screen reader technology is becoming a standard feature within leading operating systems, creating wider adoption across user segments. Companies like Microsoft, Apple, and Google enhance built-in accessibility features, reducing reliance on third-party tools. The Screen Readers Software Market benefits from this trend as native integration improves awareness and usability. It strengthens user confidence by ensuring consistent functionality across devices. Businesses also find value in deploying solutions that are compatible with widely used platforms. This trend promotes accessibility as a baseline expectation rather than a specialized service.

- For instance, WebAIM’s 2024 Screen Reader User Survey, which gathered responses from over 1,500 users, revealed that 37.3% of participants commonly use Narrator—Microsoft’s integrated screen reader for Windows desktop.

Increasing Use of Artificial Intelligence and Machine Learning

Artificial intelligence and machine learning are reshaping how screen readers interpret and present information. Advanced algorithms enhance accuracy in identifying visual content, complex layouts, and dynamic web elements. It allows users to access digital platforms more effectively with natural-sounding voices and predictive features. Developers leverage AI to create adaptive learning capabilities that improve user experience over time. The Screen Readers Software Market grows stronger with these innovations, offering solutions tailored to individual needs. Continuous improvements in processing power support this shift toward intelligent accessibility tools.

- For instance, Ghotit introduced its Analytics feature in Version 10, which allows users to track their writing activity. In early use, users checked around 750 words, a figure that quickly rose to 4,000 words in a short time—demonstrating the tool’s role in enabling expanding writing efforts among users with dyslexia or dysgraphia.

Rising Adoption in Education and Remote Learning Platforms

The demand for accessibility tools in education is expanding, fueled by the global shift toward digital and remote learning. Schools and universities deploy screen readers to support visually impaired students and comply with accessibility mandates. It enables equitable access to study materials, online assessments, and virtual classrooms. The market sees strong momentum from institutions investing in inclusive learning environments. Growth is also supported by partnerships between education technology providers and accessibility software developers. This trend highlights the importance of screen readers as core tools for inclusive education.

Expanding Role in Employment and Workplace Accessibility

Organizations across industries prioritize accessibility to meet regulatory standards and improve workforce inclusivity. Employers deploy screen readers to empower visually impaired staff and enhance productivity across digital workflows. It ensures that employees can interact with enterprise software, emails, and collaboration tools without barriers. The Screen Readers Software Market benefits from corporate initiatives promoting diversity and inclusion. Cloud-based deployments and cross-platform compatibility further increase adoption in enterprise settings. This trend underscores the role of screen readers as essential enablers of professional integration and equal opportunity.

Market Challenges Analysis

Limited Compatibility and Complex User Experience

One of the major challenges in the Screen Readers Software Market is limited compatibility across platforms, applications, and evolving digital environments. Many websites and enterprise software are not designed with accessibility in mind, which restricts the effectiveness of screen readers. It often leads to inconsistent performance, creating frustration for users who rely on seamless navigation. Complex interfaces, multimedia content, and dynamic layouts further increase barriers, making accessibility a secondary consideration in many digital platforms. Developers face difficulties in maintaining synchronization with rapid software updates across operating systems and browsers. This issue slows adoption and diminishes user confidence in the technology.

High Cost and Limited Awareness Across Emerging Regions

Affordability remains a barrier, particularly in emerging markets where economic constraints limit access to advanced accessibility solutions. Premium screen reader software often requires significant investment, putting it beyond the reach of many individuals and institutions. It restricts adoption among students, small enterprises, and non-profit organizations that aim to create inclusive environments. Awareness of accessibility tools also remains low in several regions, reducing the market’s penetration potential. Limited training programs and lack of localized language support further compound the challenge, leaving many users unable to benefit from available solutions. The Screen Readers Software Market must address these issues to expand its global reach and improve long-term sustainability.

Market Opportunities

Expanding Scope in Education and Public Sector Accessibility

The Screen Readers Software Market holds strong opportunities in education and public sector adoption, where inclusive access is becoming a regulatory and social priority. Schools, universities, and government bodies are investing in digital accessibility to comply with international standards and promote equal participation. It creates demand for advanced screen reader solutions that support diverse languages, adaptive learning, and user-friendly integration with e-learning platforms. Partnerships with edtech companies and public institutions strengthen the growth outlook by expanding user bases. Governments in emerging economies are also funding accessibility initiatives, opening new pathways for adoption. This environment positions screen readers as vital tools in shaping inclusive digital ecosystems.

Rising Potential in Emerging Markets and AI-Driven Innovation

Emerging markets offer significant growth potential as digital transformation accelerates and accessibility awareness improves. Low-cost internet penetration and increasing smartphone adoption create favorable conditions for screen reader integration across devices. It allows vendors to provide scalable, mobile-first solutions that reach larger populations. Artificial intelligence and natural language processing also open opportunities for innovation, enhancing usability with personalized voices, predictive navigation, and real-time translation. The Screen Readers Software Market stands to benefit from these advancements, capturing demand across consumer, enterprise, and institutional segments. Strategic investments in localized content and affordability-focused solutions will help unlock untapped opportunities in these regions.

Market Segmentation Analysis:

By Application

The Screen Readers Software Market is segmented into personal use, educational institutions, corporate environment, and government agencies. Personal use remains a strong segment, driven by individuals seeking accessibility for everyday digital interaction, communication, and content consumption. Educational institutions adopt screen readers to comply with accessibility regulations and ensure equal learning opportunities for students with visual impairments. Corporate environments show growing demand as businesses focus on inclusivity and employee productivity across digital platforms. Government agencies drive adoption by implementing accessibility mandates and investing in technology to improve public service delivery. It highlights the importance of screen readers across diverse functional areas where inclusivity and compliance converge.

- For instance, the Android Accessibility Suite—including TalkBack—has been downloaded more than 5 billion times worldwide according to the Google Play Store, highlighting how deeply integrated and widely deployed cloud-enabled accessibility tools have become in everyday mobile ecosystems.

By Deployment Type

Deployment is divided into cloud-based and on-premises solutions. Cloud-based deployment leads the segment due to its scalability, remote access, and cost efficiency, making it suitable for both individuals and organizations. It provides users with continuous updates and cross-platform compatibility, ensuring seamless performance across devices. On-premises deployment, while less flexible, continues to attract institutions with strict data security and compliance requirements. Educational institutions and government agencies often prefer on-premises solutions where control over sensitive data is critical. The market reflects a balanced demand pattern where flexibility and security drive the choice of deployment models.

- For instance, ViewPlus Technologies has delivered over 10,000 embossers worldwide, empowering blind and low-vision learners with tactile graphics and braille access across educational and personal use contexts.

By End User

End users include individuals with visual impairment, educational organizations, corporate employees, and non-profit organizations. Individuals form the core user base, reflecting the direct necessity of screen readers for independent living and digital accessibility. Educational organizations invest heavily to create inclusive learning environments and meet compliance standards. Corporate employees benefit from integration with workplace software, supporting organizational goals of diversity and equal opportunity. Non-profit organizations also play a key role by promoting accessibility awareness and distributing affordable or subsidized solutions. It demonstrates the widespread relevance of screen readers, cutting across personal, institutional, and social domains to ensure inclusive participation in the digital economy.

Segments:

Based on Application:

- Personal Use

- Educational Institutions

- Corporate Environment

- Government Agencies

Based on Deployment Type:

Based on End-User:

- Individuals with Visual Impairment

- Educational Organizations

- Corporate Employees

- Non-Profit Organizations

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America holds the largest share of about 34% of the global screen readers software market. This dominance comes from strong legal frameworks such as the Americans with Disabilities Act (ADA) and Section 508, which make it mandatory for organizations to provide accessible digital platforms. The United States leads adoption, supported by a mature technology sector and a culture of innovation. Canada also shows strong growth as government policies encourage inclusivity in education and workplaces. The presence of leading technology providers in this region makes it easier for enterprises and educational institutions to adopt advanced screen reader solutions. Widespread awareness of disability rights and accessibility compliance further strengthens North America’s position as the leading regional market.

Europe

Europe contributes around 28% of the global market. Countries such as Germany, the UK, and France are at the forefront, driven by the European Accessibility Act and country-level disability inclusion laws. These policies require organizations to ensure that their digital services are usable by people with visual impairments. Public awareness campaigns and nonprofit initiatives add to the demand for accessibility software. Many European universities and schools actively integrate screen readers to support inclusive education. The rise of digital transformation in industries such as banking, e-commerce, and healthcare also accelerates the adoption of accessibility solutions. Europe benefits from a balance of strict regulation, social awareness, and well-established technology infrastructure, ensuring steady growth in its market share.

Asia-Pacific

Asia-Pacific accounts for about 15% of the global market, and it is one of the fastest-growing regions. Countries like Japan, South Korea, and China are key drivers of demand. Japan has strong laws protecting the rights of persons with disabilities, while South Korea and China are seeing rapid adoption thanks to large populations and increasing internet penetration. India is another emerging market, where rising awareness of digital inclusion is leading to gradual adoption in schools, workplaces, and government programs. The growth is supported by expanding mobile phone usage, as screen readers on smartphones provide affordable accessibility options. Although APAC’s current share is smaller than North America or Europe, the pace of expansion suggests it will become a major growth contributor in the coming years.

Latin America

Latin America represents around 4% of the global screen readers market. Brazil leads the region, followed by Mexico and Argentina. Economic challenges limit widespread adoption, but NGOs and disability advocacy groups are actively pushing for more accessible technology. Growth is most visible in educational programs and public institutions, which are adopting screen reader solutions to serve students with visual impairments. Increasing smartphone penetration also helps, as mobile-based screen readers are often more affordable and easier to access than desktop solutions. Although the market is small, awareness is steadily growing.

Middle East & Africa

The Middle East and Africa together hold about 3% of the global market. Wealthier Gulf nations such as the UAE and Saudi Arabia are investing in accessibility technologies as part of smart city and digital inclusion initiatives. In Africa, adoption is limited due to economic and infrastructure barriers, but non-profit organizations and international aid programs are playing an important role in introducing screen reader solutions in schools and public offices. While market size is still low, the increasing importance of inclusive education and government digitalization plans are expected to slowly expand adoption across the region.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- NVDA

- Apple

- Clearview

- Ghotit

- Microszsoft

- AstroNova

- Serotek

- Google

- ViewPlus Technologies

- Kurzweil Education

Competitive Analysis

The Screen Reader Software Market features include, NVDA, Apple, Clearview, Ghotit, Microsoft, AstroNova, Serotek, Google, ViewPlus Technologies, Kurzweil Education. The screen readers software market shows strong competition shaped by innovation, accessibility, and integration across platforms. Established vendors focus on delivering advanced customization, robust functionality, and enterprise-ready features, while open-source projects expand adoption in cost-sensitive regions. Built-in screen readers from major operating systems ensure universal availability, creating high penetration among mainstream users. Differentiation comes from seamless cross-device integration, intuitive design, and ongoing enhancements that align with evolving accessibility standards. At the same time, niche providers strengthen their presence by tailoring solutions for education, corporate environments, and non-profits. The market increasingly emphasizes affordability, user-friendly interfaces, and continuous updates, ensuring both inclusivity and long-term growth potential.Top of FormBottom of Form

Recent Developments

- In May 2025, Apple announced powerful new accessibility features expected later in 2025, including Accessibility Nutrition Labels, further supporting inclusive technology development and user experience enhancements for visually impaired users.

- In April 2025, Amazon introduced the new Kindle Paperwhite with a waterproof design, becoming the first major e-reader manufacturer to offer a fully waterproof device (Amazon Press Release).

- In March 2024, Freedom Scientific introduced PictureSmart AI for JAWS, a new feature that uses artificial intelligence to describe images in detail. This feature improves the JAWS screen reader by helping visually impaired users understand visual content better through AI-generated descriptions, greatly enhancing their digital accessibility and user experience.

Report Coverage

The research report offers an in-depth analysis based on Application, Deployment Type, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand with rising global awareness of digital accessibility.

- Integration of screen readers into mainstream operating systems will strengthen adoption.

- Open-source solutions will gain momentum in cost-sensitive regions.

- Advancements in artificial intelligence will improve voice quality and contextual reading.

- Cloud-based deployment will increase flexibility and scalability for users.

- Educational institutions will drive demand through inclusive learning initiatives.

- Corporate environments will adopt screen readers to comply with workplace accessibility standards.

- Government regulations on digital inclusion will accelerate implementation.

- Multilingual support will broaden usage across diverse populations.

- Continuous innovation will enhance user experience and market competitiveness.