Market Overview

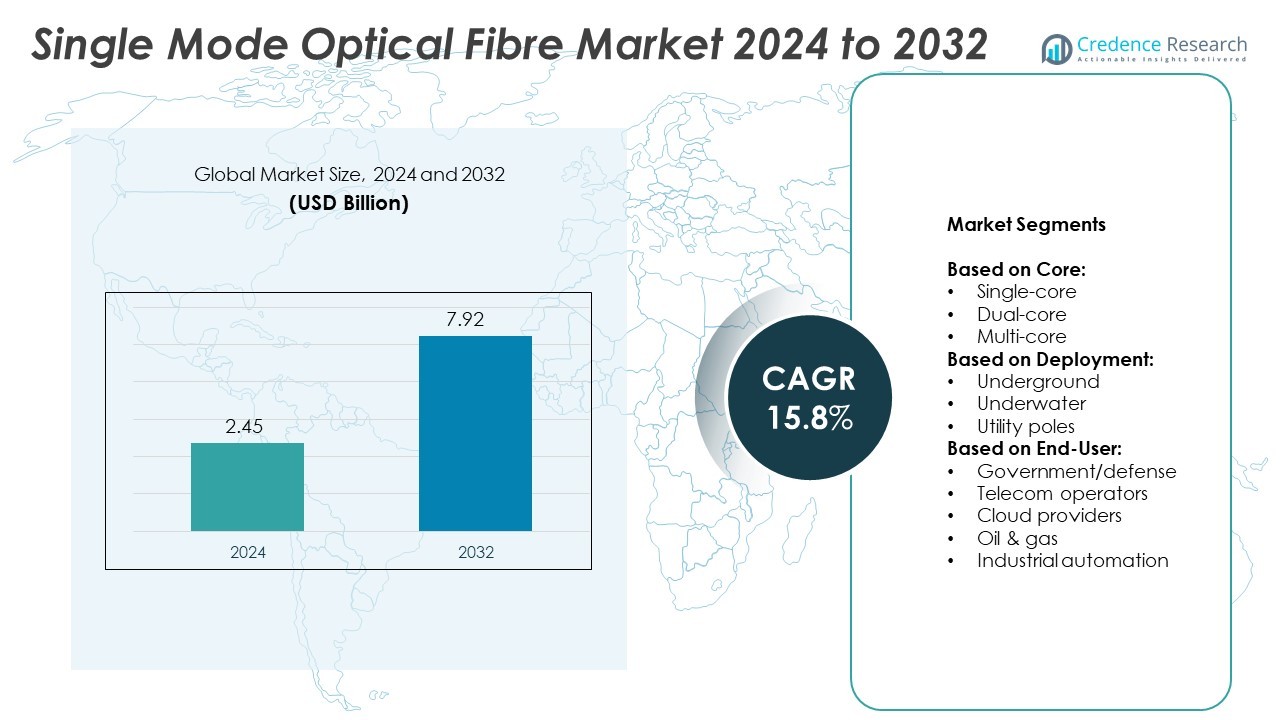

The Single Mode Optical Fibre Market size was valued at USD 2.45 billion in 2024 and is anticipated to reach USD 7.92 billion by 2032, at a CAGR of 15.8% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Single Mode Optical Fibre Market Size 2024 |

USD 2.45 Billion |

| Single Mode Optical Fibre Market, CAGR |

15.8% |

| Single Mode Optical Fibre Market Size 2032 |

USD 7.92 Billion |

The Single Mode Optical Fibre market grows rapidly, driven by the rising demand for high-speed connectivity across telecom, cloud computing, and data center networks. Expanding 5G rollouts and fibre-to-the-home projects strengthen adoption, supported by government investments in broadband and smart city initiatives. It benefits from increasing reliance on AI, IoT, and industrial automation that require low-latency and high-capacity networks. Trends highlight advancements in bend-insensitive and low-loss fibre designs that enhance efficiency and scalability.

Asia-Pacific leads the Single Mode Optical Fibre market, supported by large-scale 5G rollouts, broadband expansion, and strong fibre manufacturing capacity. North America follows with advanced telecom infrastructure and growing cloud adoption, while Europe emphasizes digital strategies and sustainability-driven fibre projects. Latin America and the Middle East & Africa show steady progress through government-backed broadband initiatives and undersea cable investments. Key players shaping the market include Prysmian, Corning, Sumitomo Electric, and Fujikura, each focusing on innovation and strategic partnerships to strengthen their global presence.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Single Mode Optical Fibre market was valued at USD 2.45 billion in 2024 and is projected to reach USD 7.92 billion by 2032, growing at a CAGR of 15.8% between 2025 and 2032.

- Strong demand for high-speed connectivity, expanding 5G infrastructure, cloud computing, and fibre-to-the-home deployments are driving adoption across both developed and emerging economies.

- Technological trends emphasize innovations in bend-insensitive and low-loss fibre designs, ensuring longer transmission distances, higher capacity, and improved efficiency for telecom and data center networks.

- The competitive landscape is defined by global leaders such as Prysmian, Corning, Sumitomo Electric, and Fujikura, supported by regional players offering cost-efficient alternatives tailored to local needs.

- High installation costs, complex deployment requirements, and supply chain vulnerabilities remain restraints that limit faster adoption in certain geographies, particularly rural and underserved regions.

- Asia-Pacific leads growth due to large-scale telecom projects and strong domestic fibre production, North America follows with advanced data centers and 5G rollouts, Europe shows steady growth with digital initiatives, while Latin America and the Middle East & Africa expand gradually through broadband and submarine cable projects.

- The market outlook reflects growing opportunities from smart city projects, AI-driven workloads, and undersea connectivity investments, with sustainability practices and resilient supply networks shaping long-term strategies for global adoption.

Market Drivers

Rising Adoption in Telecommunications and 5G Networks

The Single Mode Optical Fibre market benefits from the global shift toward high-speed and reliable communication infrastructure. Telecom operators deploy advanced networks to meet data traffic demand driven by smartphones, IoT devices, and streaming platforms. It supports long-distance transmission with minimal signal loss, making it ideal for core and metro networks. Governments and private players invest in 5G rollouts that require extensive fibre backhaul. Leading service providers extend fibre-to-the-home projects to improve connectivity. This trend positions single mode fibre as a foundation for modern digital ecosystems.

- For instance, Sumitomo Electric supplied over 20,000 kilometers of optical fibre for NTT’s 5G backhaul expansion in Japan in 2023.

Expanding Data Center Infrastructure and Cloud Computing Growth

Global cloud adoption and hyperscale data centers strengthen demand for efficient fibre solutions. Enterprises and consumers rely on cloud platforms that process enormous data volumes daily. The Single Mode Optical Fibre market gains traction through its ability to provide high bandwidth and low latency, essential for advanced computing environments. It integrates seamlessly into high-capacity links connecting global data hubs. Technology giants continue to scale networks for AI workloads, requiring superior fibre solutions. This creates steady deployment opportunities across established and emerging regions.

- For instance, corning delivered more than 100 million Homes globally in 2023, supporting large-scale data center connectivity.

Government Initiatives and Smart City Development Projects

Public sector investments in smart cities and national broadband initiatives enhance demand for advanced fibre infrastructure. The Single Mode Optical Fibre market aligns with strategic projects aimed at improving digital inclusion and e-governance services. It supports intelligent traffic management, surveillance systems, and energy-efficient grids. Developing economies prioritize large-scale fibre rollouts to bridge connectivity gaps. Policymakers allocate funds to rural broadband networks, increasing fibre penetration beyond urban areas. These efforts accelerate the long-term adoption curve across multiple sectors.

Advancements in Fibre Technology and Performance Enhancements

Continuous innovation improves the performance and efficiency of fibre solutions. The Single Mode Optical Fibre market benefits from advancements in bend-insensitive designs and low-loss cables. It ensures consistent transmission quality under demanding environmental conditions. Manufacturers develop fibres that meet the needs of 400G and 800G systems in next-generation networks. Research focuses on materials that reduce attenuation and expand transmission capacity. These technological gains reinforce fibre’s position as a critical enabler of global connectivity.

Market Trends

Growing Integration of Fibre in 5G and Next-Generation Networks

The Single Mode Optical Fibre market experiences momentum from the rapid global deployment of 5G technology. Network operators strengthen fibre backhaul to handle massive increases in mobile data traffic. It supports seamless connectivity between base stations and core networks with superior speed and reliability. Enterprises adopt private 5G networks for industrial automation and IoT applications, requiring advanced fibre infrastructure. Continuous investment in ultra-low latency communication accelerates this shift. These trends position fibre as the backbone of future telecommunications ecosystems.

- For instance, Prysmian delivered 6,000 kilometers of fibre cables for India’s BharatNet Phase-II broadband project in 2023.

Rising Demand from Hyperscale Data Centers and Cloud Services

The growth of hyperscale facilities and cloud platforms reshapes global fibre demand. The Single Mode Optical Fibre market supports ultra-fast data transfer across large networks connecting storage, compute, and application systems. It addresses the need for efficient, high-capacity links in regions with expanding AI and big data workloads. Cloud service providers expand transcontinental fibre routes to ensure uninterrupted services. Enterprises migrate critical workloads to distributed data centers that require scalable and reliable optical infrastructure. This sustained demand strengthens fibre’s relevance in modern computing ecosystems.

- For instance, Fujikura introduced a new ultra-low-loss fibre with 0.14 dB/km attenuation at 1550 nm wavelength.

Increasing Deployment in Smart Cities and IoT Infrastructure

Smart city development creates strong adoption opportunities for advanced fibre networks. The Single Mode Optical Fibre market aligns with projects integrating IoT-enabled systems for transportation, utilities, and security. It ensures uninterrupted connectivity for sensors, cameras, and automated services. Governments invest heavily in nationwide broadband plans to connect urban and rural populations. The expansion of intelligent grids and digital healthcare facilities relies on robust fibre deployment. These trends establish fibre as a strategic enabler of urban transformation.

Technological Innovations Driving Higher Capacity Solutions

Continuous innovation in fibre technology enhances efficiency and scalability. The Single Mode Optical Fibre market benefits from developments such as bend-insensitive fibre, low-loss cable designs, and compatibility with 400G and 800G systems. It supports transmission over longer distances without compromising performance. Manufacturers focus on advanced materials that minimize attenuation and increase bandwidth capacity. Research in ultra-dense wavelength division multiplexing extends the life of existing infrastructure. These advancements ensure fibre remains central to high-capacity global networks.

Market Challenges Analysis

High Installation Costs and Complex Deployment Requirements

The Single Mode Optical Fibre market faces barriers linked to the high cost of installation and infrastructure development. Extensive trenching, cabling, and network integration require significant capital investments, particularly in underserved or rural areas. It often involves challenges in securing rights-of-way and navigating regulatory frameworks that delay project execution. Network operators weigh the long-term benefits against immediate financial constraints, slowing widespread adoption. Smaller service providers find it difficult to compete with large incumbents that possess stronger resources. These cost and complexity issues limit the speed of global fibre rollout.

Supply Chain Vulnerabilities and Limited Skilled Workforce

The Single Mode Optical Fibre market encounters disruptions caused by global supply chain dependencies. Raw material shortages, shipping delays, and fluctuating commodity prices increase uncertainty for manufacturers. It also struggles with a shortage of skilled professionals capable of managing complex installation and maintenance tasks. The lack of technical expertise in emerging regions constrains the pace of adoption. Geopolitical tensions further add to risks, impacting cross-border trade of fibre components and equipment. These challenges underscore the importance of resilient supply networks and workforce development initiatives.

Market Opportunities

Expanding Role in Global 5G and Broadband Initiatives

The Single Mode Optical Fibre market presents strong opportunities through large-scale 5G deployments and national broadband projects. Governments allocate significant budgets to strengthen digital infrastructure and extend connectivity to underserved regions. It provides the backbone for high-speed, low-latency communication networks essential for industries and households. Telecom operators expand fibre-to-the-home and fibre-to-the-building initiatives to meet growing data consumption. The rise of private 5G networks for industrial automation further expands adoption. These opportunities reinforce fibre’s role as a critical enabler of next-generation connectivity.

Rising Demand from Cloud, AI, and Data Center Expansion

The Single Mode Optical Fibre market benefits from rapid growth in data-intensive technologies and hyperscale computing facilities. Cloud service providers and enterprises continue to expand global data center capacity to support AI, IoT, and big data applications. It enables high-capacity, low-loss transmission required for distributed workloads across regions. Demand for intercontinental fibre links rises as organizations seek to reduce latency in cross-border operations. Investments in undersea cable projects further highlight the growing reliance on fibre for global communication. These opportunities position fibre at the core of digital transformation worldwide.

Market Segmentation Analysis:

By Core:

The Single Mode Optical Fibre market demonstrates diverse growth potential across core types. Single-core fibres remain dominant due to their widespread use in telecom and broadband applications, offering high efficiency for long-distance transmission. Dual-core fibres gain adoption in specialized networks that require redundancy and improved data throughput. Multi-core fibres represent an emerging segment with strong potential in high-capacity data centers and advanced research networks. It provides enhanced bandwidth within a smaller footprint, making it attractive for next-generation connectivity demands. These variations highlight the adaptability of fibre solutions across evolving technological needs.

- For instance, Yangtze Optical Fibre and Cable supplied 10,000 kilometers of G.652D fibre for China Mobile’s 5G network expansion.

By Deployment:

It shape the pace and scope of fibre adoption. Underground deployment maintains a leading position, offering protection against environmental hazards and ensuring network stability in urban and rural areas. Underwater deployment expands rapidly with the rising need for international connectivity through submarine cable projects. Utility pole deployment remains cost-effective for shorter distances and regions where quick installation is required. The Single Mode Optical Fibre market gains strength from these deployment models, each addressing specific geographic and operational challenges. It ensures reliability across both domestic and cross-border communications.

- For instance, Nexans delivered 5,000 kilometers of fibre for Saudi Arabia’s NEOM smart city project.

By End-User:

It provide further clarity on demand drivers. Telecom operators account for the largest share, driven by fibre-to-the-home projects and 5G backhaul requirements. Government and defense agencies invest in secure and resilient fibre networks for national security and strategic communication. Cloud providers expand their reliance on fibre to connect hyperscale data centers and support AI-driven workloads. Oil and gas industries utilize fibre for monitoring and communication in remote and harsh environments. Industrial automation depends on high-speed, low-latency fibre to optimize operations and enable smart manufacturing. It continues to diversify adoption across multiple industries, reinforcing its role as a core enabler of digital infrastructure.

Segments:

Based on Core:

- Single-core

- Dual-core

- Multi-core

Based on Deployment:

- Underground

- Underwater

- Utility poles

Based on End-User:

- Government/defense

- Telecom operators

- Cloud providers

- Oil & gas

- Industrial automation

Based on the Geography:

- North America

- Europe

- Germany

- France

- UK.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- The Rest of the Middle East and Africa

Regional Analysis

North America

North America holds a market share of 24%, driven by advanced digital infrastructure and rapid expansion of high-speed connectivity projects. The United States leads the adoption with large-scale fibre-to-the-home deployments and extensive investment in 5G backhaul networks. It benefits from strong involvement of major telecom providers that continue to upgrade legacy systems with single mode fibre. Canada follows with government-backed broadband programs that extend connectivity to underserved rural and northern regions. Cloud service providers strengthen reliance on fibre to support hyperscale data centers and growing AI workloads. The Single Mode Optical Fibre market in North America grows steadily with rising demand for secure, reliable, and low-latency communication networks. It reinforces fibre as the backbone of next-generation digital services across the region.

Europe

Europe accounts for 18% of the market share, reflecting strong regulatory support and coordinated digital strategies across member states. The European Union’s initiatives to achieve widespread gigabit connectivity by 2030 encourage accelerated fibre deployment. It benefits from consistent investments in key markets such as Germany, France, and the United Kingdom, where telecom operators partner with governments to expand network reach. Industrial automation and energy sectors also contribute to demand, requiring high-speed and resilient connectivity. Data center growth in countries like Ireland and the Nordics further strengthens adoption of fibre for cross-border operations. The Single Mode Optical Fibre market in Europe demonstrates steady momentum, shaped by sustainability priorities and strong policy frameworks. It ensures the region continues to compete effectively in the global digital economy.

Asia-Pacific

Asia-Pacific dominates the global landscape with a market share of 41%, underscoring its leadership in telecom and broadband development. Countries such as China, Japan, South Korea, and India drive mass adoption through 5G rollouts and fibre-to-the-home projects. It supports exponential growth in data traffic generated by mobile usage, IoT devices, and video streaming platforms. Smart city initiatives and industrial digitalization further enhance reliance on fibre networks. The presence of large-scale fibre manufacturing hubs in China adds cost efficiency and accelerates deployment capacity. The Single Mode Optical Fibre market in Asia-Pacific thrives on both domestic consumption and global supply chain advantages. It maintains its leadership role by aligning with national digital infrastructure goals and enterprise modernization.

Latin America

Latin America represents 9% of the market share, showing gradual progress in fibre adoption compared to developed economies. Brazil, Mexico, and Chile lead investment in broadband infrastructure supported by government and private partnerships. It enables telecom operators to expand network coverage for a growing population of digitally active consumers. Undersea cable systems play a critical role in linking Latin American markets to global data hubs. Cloud adoption also grows steadily, prompting higher demand for reliable fibre networks. The Single Mode Optical Fibre market in Latin America benefits from industrial applications in oil, gas, and energy where remote operations require secure connectivity. It continues to build momentum as infrastructure challenges are addressed through public and private investment.

Middle East & Africa

The Middle East & Africa account for 8% of the market share, reflecting its status as an emerging but high-potential region. GCC countries spearhead adoption through ambitious projects in smart cities, broadband connectivity, and national digital transformation agendas. It supports telecom operators deploying fibre-to-the-home services to meet rising consumer and enterprise demand. Africa sees growing investment in both terrestrial and undersea fibre networks to bridge the connectivity gap across vast regions. Cloud service providers expand capacity in countries like South Africa and the UAE, reinforcing demand for advanced fibre infrastructure. The Single Mode Optical Fibre market in this region also benefits from investments in oil & gas and government modernization initiatives. It positions the region for sustained growth as infrastructure and access improve over time.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Prysmian

- Fujikura

- LS Cable and System

- Humanetics

- CommScope

- Yangtze Optical Fiber and Cable

- Sumitomo Electric

- Nexans

- Corning

- Birla Furukawa

- HTGD

- Furukawa

Competitive Analysis

The leading players in the Single Mode Optical Fibre market include Prysmian, Fujikura, LS Cable and System, Humanetics, CommScope, Yangtze Optical Fiber and Cable, Sumitomo Electric, Nexans, Corning, Birla Furukawa, HTGD, and Furukawa. These companies compete by leveraging advanced manufacturing capabilities, strong global distribution networks, and continuous investment in research and development. Innovation remains central, with emphasis on developing bend-insensitive, low-loss, and high-capacity fibre solutions that address the needs of 5G, cloud computing, and hyperscale data centers. Strategic collaborations with telecom operators and governments further strengthen their market positioning, enabling large-scale deployment projects worldwide. The competitive landscape also reflects a balance between regional dominance and global expansion strategies. Established players focus on strengthening supply chains and scaling production capacity to meet rising demand from broadband and smart city initiatives. Emerging players and regional manufacturers compete by offering cost-efficient solutions tailored to specific markets. Companies invest heavily in sustainability practices and advanced materials to align with evolving industry standards. Continuous expansion of undersea cable projects, coupled with growing demand for industrial automation, creates new opportunities for competition. The market remains highly dynamic, defined by technology leadership, pricing strategies, and the ability to address both mature and emerging economies effectively.

Recent Developments

- In 2025, Corning announced that it would showcase next‑generation fiber and cable solutions for AI networks Optical Fiber Communication Conference and Exposition, focusing on dense, scalable connectivity for data centers.

- In 2025, Prysmian entered a long‑term partnership with Relativity Networks, focusing on volume production of hollow‑core optical fiber and cable to support AI‑centric data centers

- In 2025, Prysmian launched its enhanced BendBrightXS 200 µm fibre, providing telecom operators with improved bend‑insensitive, future‑proof solutions

Market Concentration & Characteristics

The Single Mode Optical Fibre market shows moderate to high concentration, shaped by the presence of global leaders with strong manufacturing capacity, technological expertise, and extensive distribution networks. It is characterized by continuous innovation in fibre designs, including bend-insensitive and low-loss solutions, to meet the growing requirements of 5G, hyperscale data centers, and international broadband projects. Competition intensifies around large-scale contracts with telecom operators, governments, and cloud service providers, where established firms leverage economies of scale and R&D strength. Regional manufacturers contribute by offering cost-effective alternatives tailored to local needs, though they face barriers in scaling globally. Strategic partnerships, long-term supply agreements, and investment in sustainable practices define competitive positioning. The Single Mode Optical Fibre market reflects a dynamic structure where product performance, scalability, and reliability remain central to gaining market share. It continues to evolve as industry players adapt to rising demand for high-speed, low-latency, and future-ready communication infrastructure worldwide.

Report Coverage

The research report offers an in-depth analysis based on Core, Deployment, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand steadily with strong adoption in 5G and next-generation telecom networks.

- Demand will rise from hyperscale data centers supporting AI, IoT, and cloud applications.

- Governments will continue to invest in national broadband and smart city projects.

- Fibre-to-the-home deployments will accelerate in both developed and emerging economies.

- Technological innovation will drive new fibre designs with lower loss and higher capacity.

- Submarine cable projects will increase to strengthen global data connectivity.

- Industrial automation will boost demand for reliable high-speed fibre networks.

- Sustainability practices will shape manufacturing and deployment strategies.

- Competition will intensify with regional players offering cost-efficient solutions.

- The market will evolve into a critical enabler of global digital transformation.