Market Overview

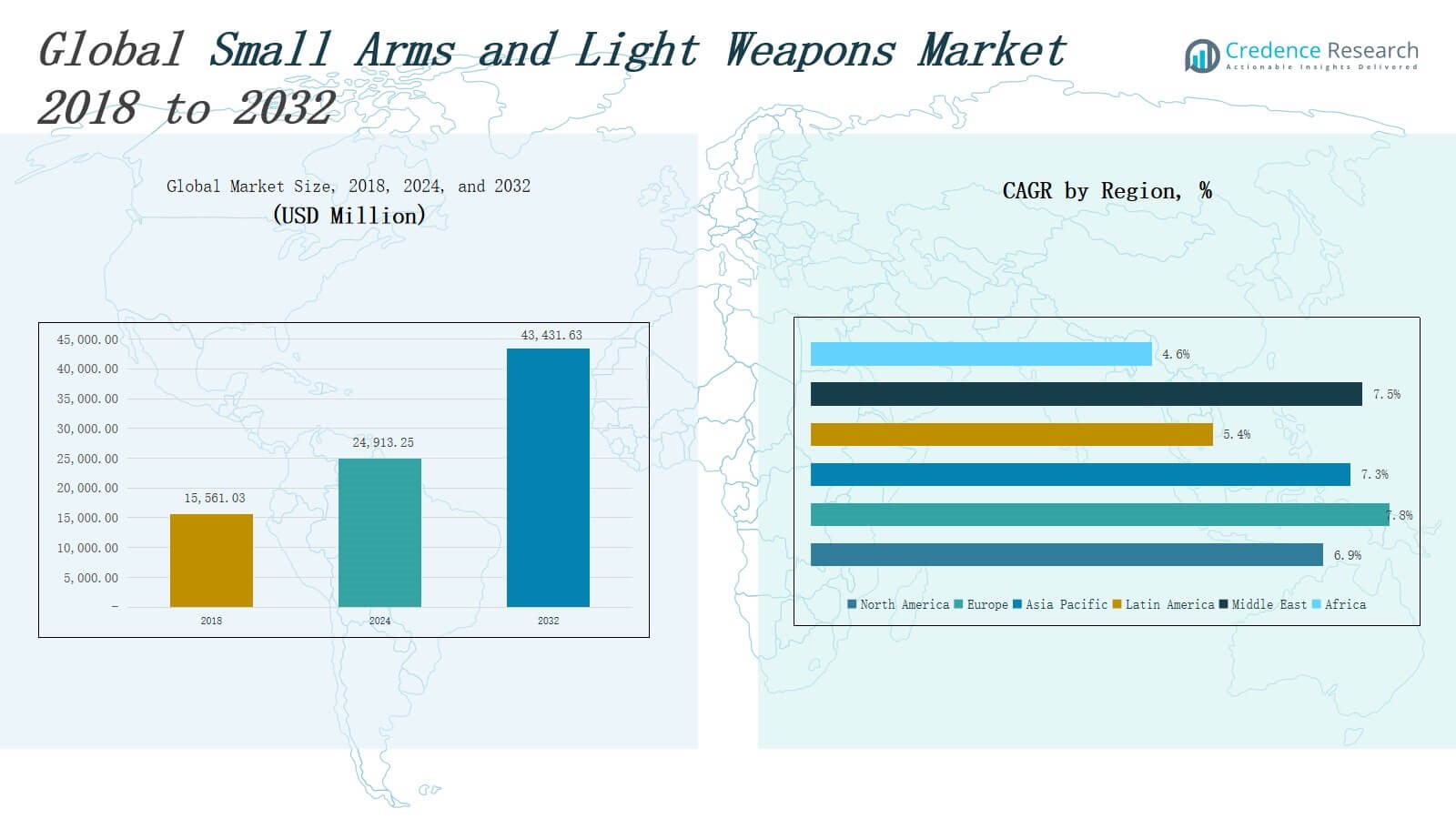

The Small Arms and Light Weapons Market size was valued at USD 15,561.03 million in 2018 to USD 24,913.25 million in 2024 and is anticipated to reach USD 43,431.63 million by 2032, at a CAGR of 7.17% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Small Arms and Light Weapons Market Size 2024 |

USD 24,913.25 Million |

| Small Arms and Light Weapons Market, CAGR |

7.17% |

| Small Arms and Light Weapons Market Size 2032 |

USD 43,431.63Million |

The Small Arms and Light Weapons (SALW) market is driven by increasing geopolitical tensions, rising defense budgets, and the modernization of military and law enforcement agencies worldwide. Growing demand for personal protection, border security, and counter-terrorism operations fuels procurement across both governmental and civilian sectors. Technological advancements such as modular weapon systems, lightweight materials, and smart optics are enhancing weapon performance and attracting end-users seeking improved accuracy and adaptability. Additionally, the rise in civilian gun ownership for sport shooting and self-defense, particularly in North America and parts of Europe, supports market expansion. Trends indicate a shift toward digitized and customizable weapon platforms, integration of electronic fire control systems, and adoption of 3D printing in component manufacturing. The market is also witnessing increased emphasis on export-oriented production and public-private partnerships in emerging economies. Regulatory developments and efforts to control illicit arms trafficking influence market dynamics, encouraging manufacturers to prioritize compliance and responsible sourcing.

The Small Arms and Light Weapons Market demonstrates strong geographical presence across North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa. North America leads in revenue share, driven by high civilian ownership and defense spending. Europe follows closely with robust military modernization and NATO-led demand. Asia Pacific shows rapid growth due to rising defense budgets in China, India, and South Korea. Latin America focuses on internal security and anti-crime operations, while the Middle East drives demand through military expansion and regional conflicts. Africa remains the smallest market but continues to procure arms for border security and peacekeeping. Key players include General Dynamics Corporation, Heckler & Koch GmBH, Sturm, Ruger & Company, FN Herstal, Colt’s Manufacturing, SIG Sauer, Lockheed Martin, Carl Walther GmbH, and Beretta S.p.A, each competing through innovation, global partnerships, and government contracts.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights

- The Small Arms and Light Weapons Market was valued at USD 24,913.25 million in 2024 and is projected to reach USD 43,431.63 million by 2032, driven by a strong 7.1% CAGR.

- Geopolitical tensions, counter-terrorism efforts, and rising defense budgets are fueling demand across military, paramilitary, and law enforcement sectors.

- Civilian ownership for self-defense and recreational shooting is rising in North America and Europe, supported by regulatory reforms and e-commerce expansion.

- Technological innovations such as smart optics, modular weapons, and 3D-printed components are transforming weapon performance and production efficiency.

- Strict international regulations and illicit arms trafficking concerns present major compliance challenges, especially for exports into sensitive regions.

- North America leads the market with USD 8,877.66 million in 2024 revenue, followed by Europe and rapidly growing Asia Pacific; Latin America, Middle East, and Africa show emerging demand.

- Key players include General Dynamics, Heckler & Koch, FN Herstal, SIG Sauer, Beretta, Colt’s Manufacturing, and Lockheed Martin, competing through innovation and global defense contracts.

Market Drivers

Rising Geopolitical Conflicts and Border Security Concerns

The Small Arms and Light Weapons Market is expanding due to intensifying regional conflicts, insurgency threats, and cross-border tensions. Governments are strengthening national security by increasing procurement of modern firearms for military and paramilitary forces. It supports rapid deployment and close-combat readiness. Law enforcement agencies seek improved operational capability for counterterrorism and riot control. Demand is particularly high in Asia, the Middle East, and Africa. Ongoing threats drive continuous investment in compact, reliable weapon systems.

- For instance, the United Arab Emirates has boosted domestic production and export of next-generation small arms, with locally manufactured rifles and pistols now being adopted by their armed forces and police, reflecting a documented shift toward self-reliance in hardware amid heightened internal security threats.

Growing Demand from Civilian and Commercial Sectors

The Small Arms and Light Weapons Market is gaining traction from rising civilian interest in firearms for self-defense, sports shooting, and hunting. Countries such as the United States, Canada, and parts of Europe are experiencing steady growth in personal gun ownership. It reflects broader concerns about personal safety and an expanding recreational shooting culture. Commercial shooting ranges and training academies contribute to rising demand. Regulatory shifts in gun ownership laws influence this growth. E-commerce platforms enhance accessibility.

- For instance, in 2023, the National Shooting Sports Foundation (NSSF) reported that 5.4 million Americans purchased their first firearm, with women accounting for approximately 42% of these first-time buyers.

Modernization of Military and Law Enforcement Agencies

The Small Arms and Light Weapons Market benefits from global efforts to replace aging armories with advanced, lightweight, and modular firearms. Governments prioritize investments in enhanced small arms that improve accuracy, durability, and adaptability. It supports mission-specific configurations and tactical upgrades. Increased adoption of red dot sights, suppressors, and electronic fire control systems strengthens combat readiness. Law enforcement units prefer ergonomic and user-friendly weapons. Modern logistics frameworks accelerate supply and inventory management.

Technological Advancements and Manufacturing Innovation

The Small Arms and Light Weapons Market is evolving through innovations in materials, design, and production processes. Industry players adopt polymers, carbon composites, and 3D printing to reduce weight and enhance durability. It enables mass customization and faster time-to-market. Smart weapons with digital sights and integrated tracking systems are gaining traction. Technological upgrades meet end-user expectations for precision and efficiency. Manufacturers partner with defense contractors to expand R&D. These advances drive competitive differentiation.

Market Trends

Shift Toward Lightweight, Modular, and Ergonomic Weapon Designs

The Small Arms and Light Weapons Market is experiencing a significant transition toward lightweight, modular platforms tailored for mission-specific flexibility. Forces prioritize ease of use, mobility, and quick adaptability in diverse combat environments. It supports integrated accessory compatibility, including advanced optics and suppressors. Compact weapon designs are gaining popularity among special forces and urban response units. Ergonomic features reduce fatigue and improve accuracy. Manufacturers focus on user-centric designs to meet operational demands.

- For instance, the SIG Sauer XM7 rifle, adopted by the U.S. Army in 2024, incorporates a free-float handguard, ambidextrous controls, and a quick-detach suppressor, making it lighter and more adaptable to various mission profiles compared to previous models.

Integration of Smart Technologies and Digital Fire Control Systems

The Small Arms and Light Weapons Market reflects a growing trend toward integration of smart technologies for enhanced functionality. Digital fire control systems, electronic aiming modules, and biometric user authentication are increasingly incorporated. It enables better target acquisition, reduced collateral damage, and improved operational control. Wireless connectivity and real-time performance diagnostics are gaining traction in both military and law enforcement applications. These technologies support data-driven training and maintenance. Users demand precision and customization in real-time environments.

- For instance, the U.S. Army’s adoption of the XM157 Fire Control optic on its Next Generation Squad Weapon features integrated laser rangefinding, ballistic calculation, and wireless connectivity to assist targeting and data-driven training in operational environments.

Increasing Investments in Research, Development, and Defense Partnerships

The Small Arms and Light Weapons Market is seeing sustained investment in R&D initiatives, driven by both public and private sector collaboration. Governments fund innovation to develop next-generation systems that offer greater range, reduced recoil, and enhanced lethality. It leads to strategic alliances between defense contractors and weapons manufacturers. These partnerships accelerate prototyping, testing, and product deployment cycles. Global defense exhibitions showcase innovation pipelines. Countries prioritize indigenous weapon development to reduce import dependency.

Rising Focus on Export-Oriented Production and Regulatory Compliance

The Small Arms and Light Weapons Market is trending toward export-led manufacturing strategies, especially in Eastern Europe, Asia, and Latin America. It allows domestic producers to leverage cost advantages and expand their international footprint. Exporters face increasing pressure to align with international arms trade regulations and ethical compliance norms. Transparency in supply chains and traceability of components are becoming standard practices. Regulatory compliance enhances market credibility. Export-friendly policies stimulate growth across emerging production hubs.

Market Challenges Analysis

Stringent Regulatory Frameworks and Export Restrictions

The Small Arms and Light Weapons Market faces significant pressure from evolving international and domestic regulations. Governments and global bodies impose strict controls on manufacturing, sales, and cross-border transfers of weapons. It creates compliance complexities for producers, especially small and medium enterprises. Policies such as the Arms Trade Treaty and end-user certification requirements limit expansion into sensitive regions. Unpredictable embargoes and export bans disrupt supply chains and delay delivery timelines. Compliance costs and legal risks often outweigh potential market gains in high-risk zones.

Proliferation Risks and Illicit Trade Concerns

The Small Arms and Light Weapons Market must navigate persistent concerns around illegal trafficking and misuse of weapons. It faces scrutiny from advocacy groups and policymakers concerned about rising gun violence and conflict escalation. Poor control in post-conflict zones contributes to black-market circulation. Manufacturers encounter reputational and operational risks when weapons end up in unauthorized hands. International pressure to tighten transparency and tracking of sales impacts volume and profitability. These challenges hinder market stability and long-term planning.

Market Opportunities

Rising Defense Modernization Programs Across Emerging Economies

The Small Arms and Light Weapons Market presents strong growth potential through expanding defense budgets in Asia-Pacific, Latin America, and the Middle East. Governments are prioritizing military modernization to counter regional threats and strengthen homeland security. It opens new procurement contracts for advanced, lightweight, and modular weapons. Nations such as India, Brazil, and Saudi Arabia are investing in tactical upgrades and soldier lethality programs. Domestic manufacturing and joint ventures support localization and technology transfer. These trends offer long-term opportunities for established and new entrants.

Growing Demand for Smart Weapons and Tactical Enhancements

The Small Arms and Light Weapons Market can capitalize on increasing interest in smart firearms equipped with digital sights, biometric locks, and wireless diagnostics. It reflects a shift toward data-driven defense strategies and real-time battlefield intelligence. Law enforcement agencies seek connected solutions to improve accuracy, accountability, and performance tracking. Civilian consumers also show interest in personal defense weapons with advanced safety features. Manufacturers integrating electronics and AI-enabled components can access high-margin segments. Demand for innovation continues to reshape procurement strategies globally.

Market Segmentation Analysis:

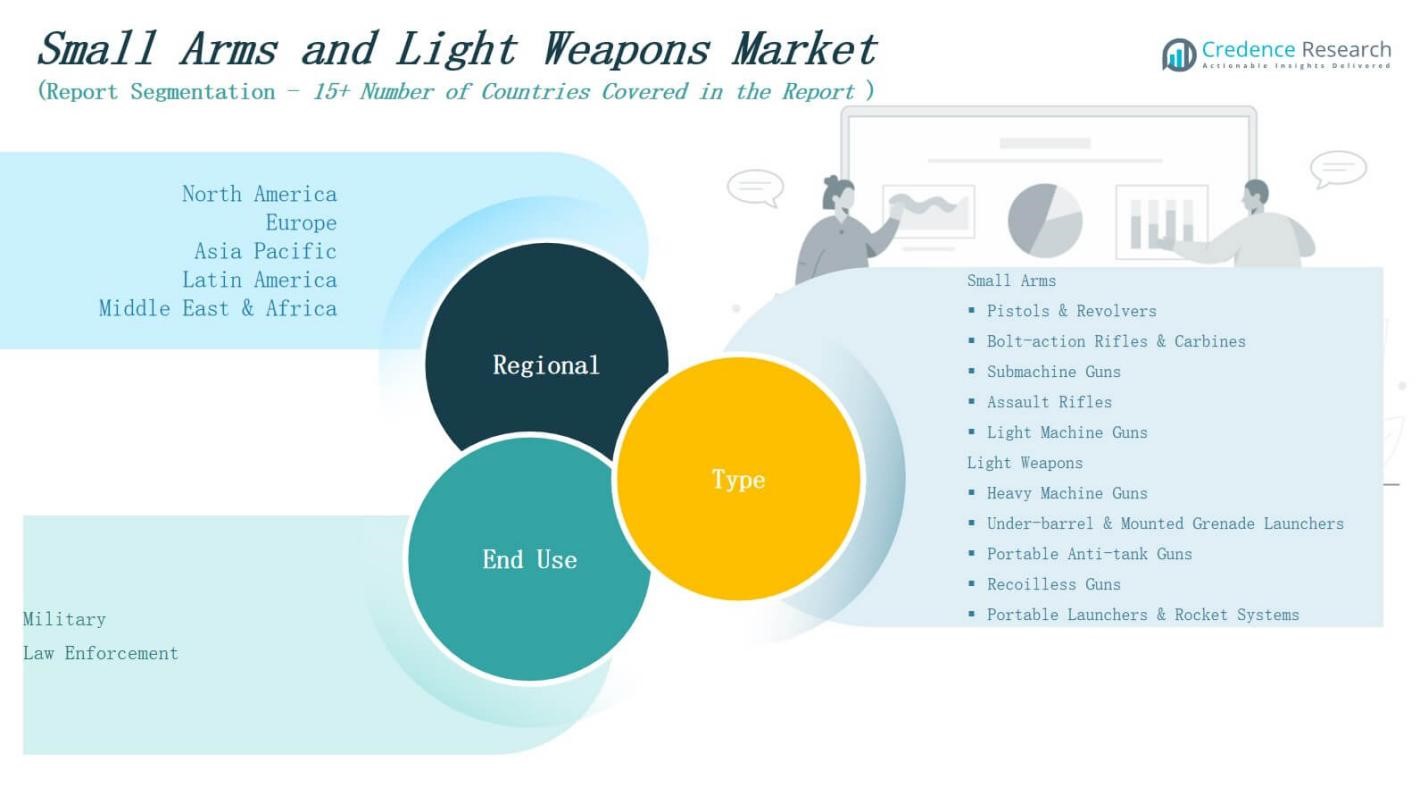

By Product

The Small Arms and Light Weapons Market is segmented into small arms and light weapons, each serving distinct operational needs. Small arms include pistols and revolvers, bolt-action rifles and carbines, submachine guns, assault rifles, and light machine guns. These are widely used in close-quarter combat, law enforcement, and civilian defense. Among them, assault rifles and pistols command strong demand due to their versatility, compactness, and ease of use. Light weapons comprise heavy machine guns, under-barrel and mounted grenade launchers, portable anti-tank guns, recoilless guns, and portable launchers and rocket systems. It supports military operations requiring high-impact firepower and mobility. Light weapons find extensive use in infantry, special operations, and anti-armor missions.

- For instance, the Glock 17 9mm pistol, widely adopted by police agencies globally, is known for its reliability and has been a standard sidearm for the UK Metropolitan Police since 2013.

By End Use

The Small Arms and Light Weapons Market is divided into military and law enforcement segments. Military forces dominate market share with large-scale procurement programs aimed at force modernization and threat preparedness. It supports the adoption of advanced automatic rifles, light machine guns, and portable launch systems. Law enforcement agencies focus on semi-automatic pistols, submachine guns, and non-lethal variants to ensure public safety and tactical flexibility. Rising internal security challenges and terrorism threats continue to drive demand in both segments. Strategic upgrades and international defense cooperation influence purchasing decisions.

- For instance, the U.S. Army awarded a contract to SIG Sauer for the Next Generation Squad Weapon (NGSW), including the XM7 rifle and XM250 automatic rifle, to replace the M4 and M249.

Segments:

Based on Product

Small Arms

- Pistols & Revolvers

- Bolt-action Rifles & Carbines

- Submachine Guns

- Assault Rifles

- Light Machine Guns

Light Weapons

- Heavy Machine Guns

- Under-barrel & Mounted Grenade Launchers

- Portable Anti-tank Guns

- Recoilless Guns

- Portable Launchers & Rocket Systems

Based on End Use

Based on Region

North America

Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

Latin America

- Brazil

- Argentina

- Rest of Latin America

Middle East

- GCC Countries

- Israel

- Turkey

- Rest of Middle East

Africa

- South Africa

- Egypt

- Rest of Africa

Regional Analysis

North America

The North America Small Arms and Light Weapons Market size was valued at USD 5,619.09 million in 2018 to USD 8,877.66 million in 2024 and is anticipated to reach USD 15,201.07 million by 2032, at a CAGR of 6.9% during the forecast period. North America holds the largest market share, driven by high civilian firearm ownership, robust defense spending, and advanced manufacturing capabilities. The United States leads in both domestic demand and global exports of small arms. It benefits from strong institutional frameworks, mature distribution networks, and ongoing defense modernization programs. Law enforcement agencies across the U.S. and Canada continue to upgrade their armory. The presence of major players like Sturm, Ruger & Company and Colt’s Manufacturing supports innovation and production scale.

Europe

The Europe Small Arms and Light Weapons Market size was valued at USD 4,582.72 million in 2018 to USD 7,619.90 million in 2024 and is anticipated to reach USD 13,941.55 million by 2032, at a CAGR of 7.8% during the forecast period. Europe commands a substantial share of the global market, supported by regional security initiatives and NATO-aligned procurement. Countries like Germany, France, and the UK invest heavily in soldier modernization and counterterrorism efforts. It maintains a strong defense industrial base with manufacturers such as Heckler & Koch and FN Herstal. Stricter regulatory frameworks influence civilian ownership but allow controlled market growth. Cross-border cooperation and joint ventures enhance technology exchange.

Asia Pacific

The Asia Pacific Small Arms and Light Weapons Market size was valued at USD 3,222.69 million in 2018 to USD 5,195.84 million in 2024 and is anticipated to reach USD 9,142.36 million by 2032, at a CAGR of 7.3% during the forecast period. Asia Pacific is witnessing rapid market growth, led by increased defense budgets and internal security challenges. Countries such as China, India, and South Korea focus on troop preparedness and border defense. It supports procurement of rifles, carbines, and portable launchers. Indigenous production and technology transfer initiatives are expanding. The market benefits from a large defense personnel base and rising paramilitary operations.

Latin America

The Latin America Small Arms and Light Weapons Market size was valued at USD 1,314.91 million in 2018 to USD 1,929.00 million in 2024 and is anticipated to reach USD 2,953.35 million by 2032, at a CAGR of 5.4% during the forecast period. Latin America represents a moderate share of the global market, driven by internal security issues and anti-narcotics operations. Brazil and Mexico lead demand, with military and law enforcement agencies procuring weapons for urban crime control and counterinsurgency. It faces procurement challenges due to budget limitations and import dependencies. Domestic manufacturing in Brazil is expanding to reduce reliance on foreign suppliers. Regional instability continues to drive steady demand.

Middle East

The Middle East Small Arms and Light Weapons Market size was valued at USD 602.21 million in 2018 to USD 980.16 million in 2024 and is anticipated to reach USD 1,745.95 million by 2032, at a CAGR of 7.5% during the forecast period. The Middle East demonstrates strong growth due to regional conflicts, military expansion, and border security concerns. Countries such as Saudi Arabia, Israel, and the UAE invest in advanced weapon systems and tactical upgrades. It benefits from defense partnerships with Western manufacturers and increased local assembly initiatives. Law enforcement and counterterrorism units continue to modernize. The market is also influenced by government-to-government arms agreements.

Africa

The Africa Small Arms and Light Weapons Market size was valued at USD 219.41 million in 2018 to USD 310.70 million in 2024 and is anticipated to reach USD 447.35 million by 2032, at a CAGR of 4.6% during the forecast period. Africa holds the smallest market share but remains strategically significant due to ongoing insurgencies and border conflicts. Nations such as South Africa and Egypt lead procurement initiatives and regional distribution. It relies heavily on imports and donor-funded defense programs. Demand centers on rifles, carbines, and portable machine guns for military and peacekeeping missions. Regional instability and arms trafficking challenge consistent growth. Efforts to develop local production remain limited.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- General Dynamics Corporation

- Heckler & Koch GmBH

- Sturm, Ruger & Company

- FN Herstal, S.A.

- Colt’s Manufacturing Company LLC

- SIG Sauer GmbH & Co.

- Lockheed Martin Corporation

- Carl Walther GmbH

- Beretta S.p.A

- Other Key Players

Competitive Analysis

The Small Arms and Light Weapons Market features a competitive landscape dominated by global defense manufacturers and specialized firearm producers. Key players such as General Dynamics Corporation, Beretta S.p.A, FN Herstal, and SIG Sauer focus on military contracts, innovation, and strategic partnerships. It remains highly fragmented, with companies competing on quality, reliability, and compliance with export regulations. Firms invest in R&D to enhance modularity, weight reduction, and smart features. Civilian demand supports product diversification, particularly in pistols and rifles. Regional manufacturers in Asia and Latin America aim to strengthen domestic capabilities through joint ventures and technology transfers. Market leaders benefit from established supply chains and long-standing government relationships. Pricing, performance, and product adaptability remain central to competitive positioning. Compliance with evolving international arms trade policies continues to influence market reach and expansion strategies.

Recent Developments

- In June 2025, TEMBO Defence signed a memorandum of understanding to set up a small-arms ammunition manufacturing facility in Amravati, Maharashtra, in partnership with a European firearms company that will purchase the full production output.

- In June 2025, SIG Sauer introduced the P211-GTO, a new double-stack 1911-style handgun, during its SIG NEXT 2025 event held from June 17–19.

- In May 2025, Rheinmetall formed a strategic partnership with Reliance Defence to produce medium- and heavy-caliber artillery ammunition at a new facility in Maharashtra.

- In June 2025, IWI’s Indian partner BSS Material Ltd completed successful trials of the AI-powered Negev NG-7 light machine gun with the Indian Army, demonstrating automated targeting capabilities at high altitudes.

Market Concentration & Characteristics

The Small Arms and Light Weapons Market exhibits moderate to high market concentration, with several global defense firms dominating supply to military, law enforcement, and civilian sectors. It features a mix of legacy manufacturers and regional players focused on specialized weapons and tactical systems. Companies compete on performance, durability, customization, and regulatory compliance. The market is characterized by long-term government contracts, export licensing challenges, and a steady demand cycle influenced by geopolitical instability and public security concerns. It supports continuous product innovation, including modular weapon platforms, lightweight materials, and digital enhancements. Entry barriers remain high due to strict legal frameworks, high capital investment, and technology requirements. Despite regulatory pressure, demand from civilian users and security forces ensures consistent revenue opportunities. The market favors players with global distribution, reliable supply chains, and strong R&D capabilities. It also shows a growing shift toward domestic production in emerging economies to reduce dependency on foreign imports.

Report Coverage

The research report offers an in-depth analysis based on Product, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Defense modernization programs will drive steady demand for modular and lightweight weapon systems.

- Civilian firearm ownership will continue to rise in regions with relaxed regulatory frameworks.

- Governments will invest more in indigenous weapon production to strengthen self-reliance.

- Smart weapon technologies with digital fire control systems will gain wider adoption.

- Export-oriented strategies will expand market reach for manufacturers in developing countries.

- Public-private partnerships will support innovation and manufacturing scale-up.

- Rising border conflicts and insurgencies will sustain procurement by military and paramilitary forces.

- Regulatory scrutiny will increase, requiring stricter compliance from arms producers.

- Law enforcement agencies will adopt more ergonomic and versatile weapons for urban operations.

- Use of advanced materials and additive manufacturing will reduce costs and improve weapon efficiency.