Market Overview:

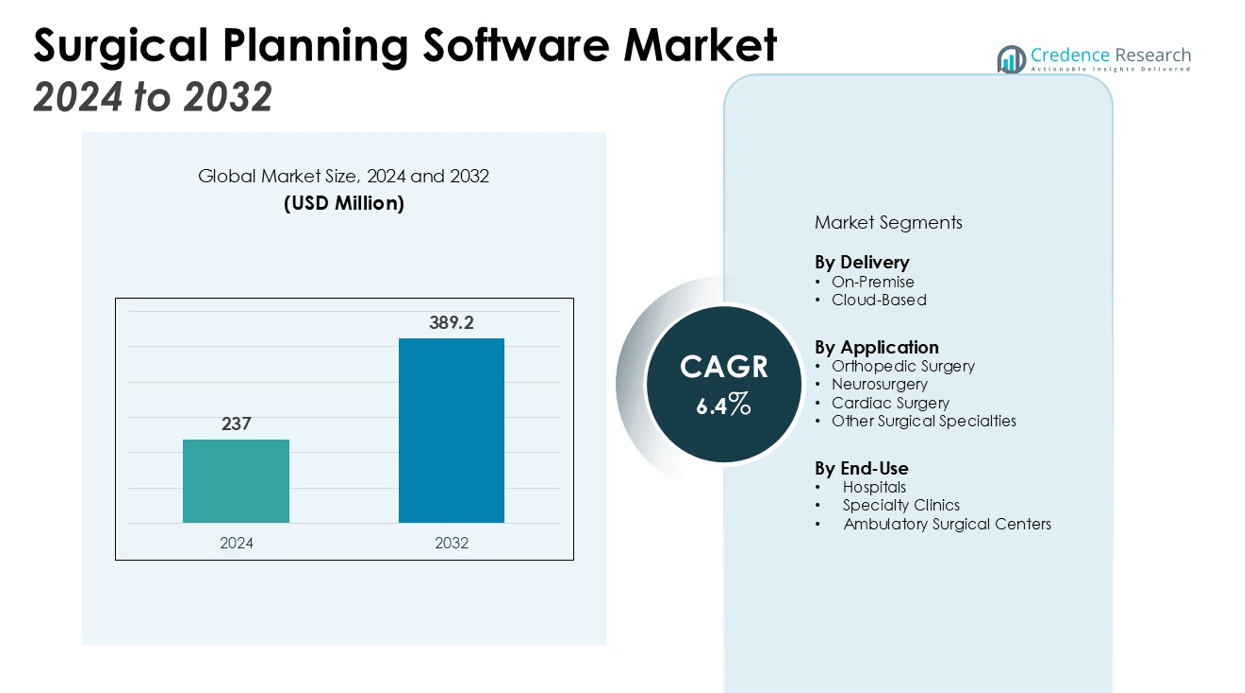

The Surgical Planning Software Market size was valued at USD 237 million in 2024 and is anticipated to reach USD 389.2 million by 2032, at a CAGR of 6.4% during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Surgical Planning Software Market Size 2024 |

USD 237 million |

| Surgical Planning Software Market, CAGR |

6.4% |

| Surgical Planning Software Market Size 2032 |

USD 389.2 million |

Key market drivers include the increasing prevalence of chronic diseases and complex surgical cases, which necessitate detailed preoperative planning and simulation. The integration of artificial intelligence, 3D visualization, and augmented reality technologies within surgical planning platforms is further accelerating market growth. Additionally, the global shift towards minimally invasive procedures and the need for patient-specific solutions are encouraging healthcare providers to invest in advanced planning software to enhance surgical workflows and reduce complications. The surge in collaborations between medical device companies and software developers is also fostering innovation and broadening the adoption of cutting-edge surgical planning solutions.

Regionally, North America commands the largest share of the Surgical Planning Software Market, attributed to the presence of a technologically advanced healthcare infrastructure and significant R&D investments. Europe follows closely, supported by a rising number of elective surgeries and favorable regulatory policies. The Asia Pacific region is expected to register the fastest growth, driven by expanding healthcare access, increasing healthcare expenditure, and rapid digital transformation in countries such as China, India, and Japan. Growing government initiatives to modernize healthcare infrastructure across emerging economies are further supporting regional market expansion.

Market Insights:

- The Surgical Planning Software Market reached USD 237 million in 2024 and is expected to grow to USD 389.2 million by 2032, reflecting a CAGR of 6.4% during the forecast period.

- Increasing prevalence of chronic diseases and complex surgeries is driving strong demand for advanced preoperative planning and simulation tools.

- Integration of artificial intelligence, 3D visualization, and augmented reality is enhancing surgical precision and setting new standards for clinical outcomes.

- Adoption of minimally invasive and patient-specific surgical techniques is accelerating investments in digital planning software across hospitals and specialty centers.

- High implementation costs, integration complexities, and data security concerns are key challenges limiting adoption in smaller healthcare facilities and emerging economies.

- North America holds 42% market share, supported by advanced healthcare infrastructure, robust R&D activity, and presence of leading vendors.

- Asia Pacific commands 19% market share and stands out as the fastest-growing region, fueled by rising healthcare spending, rapid technology adoption, and government-led digital health initiatives.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Burden of Chronic Diseases and Complex Surgical Procedures

The growing prevalence of chronic conditions such as cardiovascular disorders, cancer, and orthopedic issues has increased the number of complex surgical interventions globally. The Surgical Planning Software Market benefits from this trend, as healthcare providers prioritize precise and individualized surgical planning to improve patient outcomes. Accurate preoperative visualization and simulation play a crucial role in addressing complications associated with high-risk cases. Hospitals and specialty clinics are adopting advanced software to meet rising patient demands and enhance surgical success rates.

- For instance, using the virtual reality cardiac surgical planning software, CorFix, participants with minimal training were able to design a patient-specific, tube-shaped Fontan graft in an average time of just 5.49 minutes.

Integration of Advanced Technologies Enhancing Clinical Precision

The incorporation of artificial intelligence, 3D imaging, and augmented reality within surgical planning platforms is transforming the standard of care. These technologies enable surgeons to visualize anatomical structures in greater detail, optimize procedural strategies, and reduce intraoperative errors. The Surgical Planning Software Market is witnessing significant investment in R&D from both established healthcare IT players and medical device companies. Innovative solutions leveraging AI-driven analytics and virtual modeling are setting new benchmarks for preoperative planning efficiency.

- For instance, in an initial institutional study on an augmented reality head-mounted display navigation system, surgeons successfully placed 205 consecutive pedicle screws in the thoracic, lumbar, and sacral spine.

Shift Toward Minimally Invasive and Patient-Specific Solutions

Healthcare systems are increasingly adopting minimally invasive surgical techniques to lower recovery times and reduce risks of complications. The Surgical Planning Software Market supports this shift by enabling highly accurate, patient-specific procedural mapping. Surgeons can tailor interventions based on detailed digital models, thereby achieving optimal outcomes with fewer post-surgical complications. Hospitals recognize the value of such software in streamlining workflow and enhancing overall surgical productivity.

Collaborations and Industry Partnerships Accelerating Adoption

Collaborations between software developers, medical device manufacturers, and healthcare institutions are rapidly advancing the capabilities of surgical planning solutions. The Surgical Planning Software Market continues to expand its reach through joint ventures, technology licensing agreements, and strategic partnerships. These alliances accelerate the development and deployment of interoperable, user-friendly platforms. It facilitates widespread adoption and supports continuous innovation across diverse surgical specialties.

Market Trends:

Rapid Integration of Artificial Intelligence and Augmented Reality

Artificial intelligence and augmented reality are redefining the capabilities of surgical planning platforms, enabling new standards in clinical accuracy and efficiency. The Surgical Planning Software Market has seen a marked increase in AI-powered features for predictive analytics, automatic segmentation, and real-time surgical simulation. These advancements allow surgeons to access precise anatomical reconstructions and optimize procedures based on data-driven recommendations. Augmented reality overlays further enhance intraoperative guidance, supporting more informed decision-making during surgery. Hospitals and surgical centers are incorporating these innovations to improve workflow, shorten planning time, and increase the overall quality of patient care. It strengthens the competitive edge of vendors focused on developing adaptive and intelligent planning solutions.

- For instance, Augmedics’ xvision Spine System uses an augmented reality headset that gives surgeons a form of “X-ray vision” during spinal procedures, and as of 2022, over 2,000 commercial cases had been successfully completed using this technology.

Expansion of Cloud-Based Solutions and Interoperable Ecosystems

Cloud-based deployment models are gaining significant traction, facilitating remote access, scalability, and secure data sharing across care teams. The Surgical Planning Software Market is witnessing a surge in platforms designed to seamlessly integrate with electronic health records, imaging devices, and surgical robots. These interoperable ecosystems ensure continuity of care by centralizing patient information and streamlining multidisciplinary collaboration. Hospitals value the flexibility and efficiency offered by cloud-native software, particularly in geographically dispersed networks and telemedicine-driven practices. The trend toward modular, API-enabled architectures enables rapid customization and integration with emerging healthcare technologies. It reinforces the market’s transition toward digital-first, data-driven surgical environments.

- For instance, Siemens Healthineers’ syngo.via on AWS unified imaging at 23 geographically dispersed radiology centers of HT Médica in Spain, cutting setup times from weeks to hours.

Market Challenges Analysis:

High Implementation Costs and Integration Complexities

The high upfront investment required for advanced software and supporting hardware remains a primary barrier for many healthcare providers. The Surgical Planning Software Market faces resistance from smaller hospitals and clinics due to budget constraints and limited IT infrastructure. Integration with existing systems, such as electronic health records and imaging modalities, often demands substantial resources and technical expertise. It creates operational challenges that can slow the adoption rate. Uncertainties around return on investment and ongoing maintenance costs also deter potential users. These factors collectively restrict market penetration, especially in emerging economies.

Regulatory Hurdles and Data Security Concerns

Strict regulatory requirements and compliance standards pose challenges for software vendors seeking to enter new markets. The Surgical Planning Software Market must address evolving healthcare data protection laws, patient privacy standards, and device certification processes. It must also contend with cybersecurity risks and concerns over data breaches, which are particularly acute in digital health environments. Hospitals prioritize solutions with proven safeguards and transparent data management protocols. Navigating regulatory frameworks and ensuring data integrity remain crucial for sustained market growth.

Market Opportunities:

Emergence of Personalized and Predictive Surgical Solutions

The rising focus on personalized medicine offers significant growth prospects for the Surgical Planning Software Market. Advanced platforms now provide surgeons with tailored procedural strategies based on patient-specific data, improving both accuracy and outcomes. AI-driven analytics and predictive modeling enable proactive risk assessment, allowing for better preoperative decision-making. Hospitals value these capabilities to reduce complications and shorten recovery times. The growing demand for individualized treatment plans encourages further innovation in the sector. It creates new opportunities for vendors to differentiate their offerings.

Expansion into Emerging Markets and Ambulatory Care Settings

Expanding healthcare infrastructure across emerging economies presents a strong opportunity for market growth. The Surgical Planning Software Market stands to benefit from government investments in digital health and rising adoption of minimally invasive procedures outside traditional hospital environments. Ambulatory surgery centers and specialty clinics are investing in advanced planning tools to optimize workflows and improve efficiency. Demand for cost-effective and scalable solutions supports rapid market entry in these regions. It positions software providers to establish a foothold in high-potential geographies while broadening their global reach.

Market Segmentation Analysis:

By Delivery

The Surgical Planning Software Market is segmented by delivery into on-premise and cloud-based solutions. On-premise software remains the preferred choice for large hospitals and academic institutions seeking maximum control over data security and system integration. Cloud-based platforms are gaining momentum due to their scalability, ease of remote access, and cost-effective implementation, appealing especially to ambulatory surgery centers and smaller clinics. The flexibility offered by cloud models supports collaborative planning across geographically dispersed care teams and improves interoperability with other healthcare IT systems.

- For instance, Materialise Mimics software, a leading on-premise solution, achieves a geometric accuracy with an average deviation of approximately 0.3 mm in the 3D reconstruction of femur heads from CT scans, enabling precise surgical planning.

By Application

The market encompasses applications in orthopedic surgery, neurosurgery, cardiac surgery, and other complex surgical specialties. Orthopedic surgery dominates this segment, reflecting the high demand for preoperative planning in joint replacement and trauma cases. Neurosurgery and cardiac surgery are adopting advanced planning tools for precise procedural mapping and risk reduction. Detailed anatomical visualization and virtual simulation capabilities are transforming surgical workflows. It is enabling greater procedural accuracy across diverse surgical disciplines.

- For instance, Stryker’s Mako Robotic Surgery System has facilitated over 1 million joint replacement procedures globally to date, contributing to enhanced implant alignment and patient outcomes in knee, hip, and partial-knee arthroplasties.

By End-Use

End-use segmentation includes hospitals, specialty clinics, and ambulatory surgical centers. Hospitals account for the largest market share due to high surgical volumes and robust resources for adopting advanced technologies. Specialty clinics and ambulatory surgical centers are becoming significant end-users, motivated by the need for efficient workflows and improved patient outcomes. It supports streamlined processes and better surgical results across all care settings. The market’s adaptability highlights its importance in the evolving landscape of surgical care.

Segmentations:

By Delivery

By Application

- Orthopedic Surgery

- Neurosurgery

- Cardiac Surgery

- Other Surgical Specialties

By End-Use

- Hospitals

- Specialty Clinics

- Ambulatory Surgical Centers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America Maintains Market Leadership

North America holds 42% share of the Surgical Planning Software Market, maintaining its status as the leading regional market. The United States delivers the largest contribution, supported by a strong healthcare infrastructure and major investments in medical technology. Hospitals and clinics in this region benefit from high R&D spending, access to skilled healthcare professionals, and favorable reimbursement policies. Leading software vendors and medical device manufacturers are headquartered in North America, consolidating its dominance. The market continues to grow through strategic partnerships between healthcare institutions and technology providers focused on digital transformation.

Europe Drives Adoption Through Regulatory Support

Europe accounts for 29% share of the Surgical Planning Software Market, propelled by an increasing number of elective surgeries and supportive regulatory frameworks. Countries such as Germany, the United Kingdom, and France are advancing the adoption of digital surgical planning tools to boost efficiency and clinical outcomes. Regional governments invest in interoperable and standardized solutions to drive digital health initiatives. Collaboration between public health systems and private sector innovators supports further market development. The region demonstrates steady growth as healthcare providers emphasize patient safety, data integration, and minimally invasive techniques.

Asia Pacific Emerges as the Fastest-Growing Region

Asia Pacific captures 19% share of the Surgical Planning Software Market and stands as the fastest-growing region. Growth here is fueled by rising healthcare expenditure and rapid adoption of advanced technologies in countries such as China, India, and Japan. Significant government investments in digital health infrastructure and workforce training are modernizing the sector. Hospitals and specialty centers are adopting advanced software to manage increasing surgical volumes and achieve better patient outcomes. The region offers strong long-term potential for global vendors focused on market expansion and innovation partnerships.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Stryker

- Zimmer Biomet.

- Medtronic

- Materialise

- Brainlab AG

- 3D Systems Inc.

- mediCAD Hectec GmbH

- DePuy Synthes (Johnson & Johnson Medical Devices Companies)

- CANON MEDICAL SYSTEMS USA, INC.

- General Electric Company

- Renishaw Plc.

Competitive Analysis:

The Surgical Planning Software Market features a competitive landscape defined by global technology leaders, specialized healthcare IT firms, and established medical device manufacturers. Leading companies such as Materialise, Brainlab, GE Healthcare, Siemens Healthineers, and Stryker hold significant market shares through advanced product portfolios and a strong international presence. Strategic collaborations with hospitals, research institutions, and device makers enable these firms to drive innovation and expand market reach. New entrants and niche players focus on developing specialized solutions with artificial intelligence, 3D visualization, and cloud integration to address evolving clinical needs. The market rewards continuous investment in R&D, robust customer support, and regulatory compliance. It fosters a dynamic environment where technological advancements, customer partnerships, and global expansion strategies determine long-term success. Competitive intensity remains high as vendors seek to differentiate through product innovation, user-friendly interfaces, and enhanced clinical value.

Recent Developments:

- In July 2025, Inari Medical, now a part of Stryker, launched the InThrill Thrombectomy System, a device for removing blood clots from small vessels and access points in dialysis patients.

- In July 2025, Zimmer Biomet announced a definitive agreement to acquireo acquire orthopedic robotics firm Monogram Technologies Inc.

- In June 2025, Brainlab announced the spin-off of its Snke Group, enabling both companies to pursue their distinct growth strategies more effectively.

Market Concentration & Characteristics:

The Surgical Planning Software Market demonstrates moderate concentration, with a few leading multinational corporations and several specialized technology firms controlling the majority of global sales. It is characterized by continuous technological advancement, a strong focus on clinical precision, and high regulatory standards. Product differentiation centers on the integration of artificial intelligence, 3D visualization, and seamless interoperability with healthcare IT systems. Companies compete by offering user-friendly platforms, robust customer support, and customized solutions tailored to various surgical specialties. It displays significant barriers to entry due to substantial R&D requirements, complex certification processes, and the need for established clinical partnerships.

Report Coverage:

The research report offers an in-depth analysis based on Delivery, Application, End-Use and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Surgeons will leverage real‑time intraoperative guidance via augmented reality overlays to enhance precision and decision-making.

- Vendors will develop AI-powered predictive analytics to anticipate complications and optimize surgical strategies.

- Cloud-native platforms will become standard, enabling secure remote collaboration and unified patient data access.

- Interoperable solutions will link planning software with surgical robots, imaging systems, and electronic health records.

- Personalization will grow, with patient-specific anatomical models guiding procedure customization and reducing variability.

- Adoption will extend into outpatient surgery centers and specialized clinics seeking efficient surgical workflows.

- Partnerships between medical device manufacturers and digital health providers will accelerate platform innovation.

- Regulatory frameworks will evolve to support software validation and streamline approval across global markets.

- Emerging economies will invest heavily in digital infrastructure, broadening access to advanced planning tools.

- Vendors will prioritize user-centric interfaces and training programs to enhance clinical adoption and improve surgical outcomes.