| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Alpha Thalassemia Treatment Market Size 2024 |

USD 1,202.81 million |

| Alpha Thalassemia Treatment Market, CAGR |

6.51% |

| Alpha Thalassemia Treatment Market Size 2032 |

USD 1,982.50 million |

Market Overview:

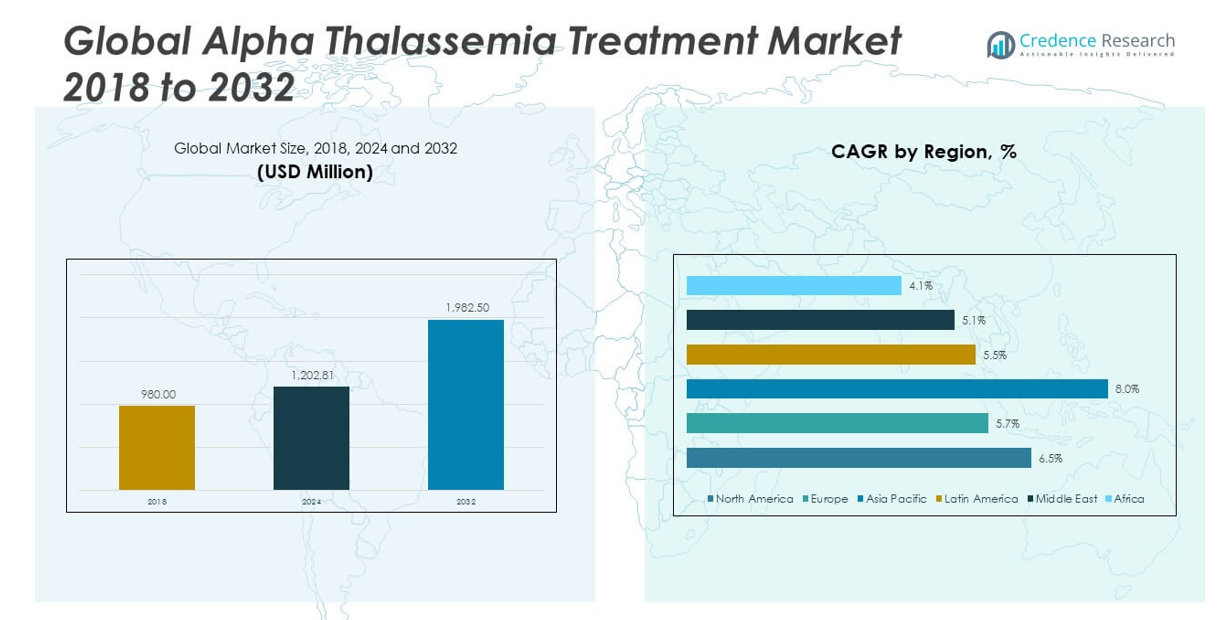

The Global Alpha Thalassemia Treatment Market size was valued at USD 980.00 million in 2018 to USD 1,202.81 million in 2024 and is anticipated to reach USD 1,982.50 million by 2032, at a CAGR of 6.51% during the forecast period.

The primary growth drivers for the Global Alpha Thalassemia Treatment Market include the rising prevalence of alpha thalassemia disorders, particularly severe forms like hemoglobin H disease and hemoglobin Bart’s hydrops fetalis, which often require lifelong medical intervention. The need for regular blood transfusions and iron chelation therapy among patients with transfusion-dependent thalassemia sustains demand for essential treatment protocols. In parallel, technological advances in bone marrow transplantation, stem cell therapy, and the emergence of gene editing platforms like CRISPR are transforming the therapeutic landscape. Pharmaceutical and biotechnology companies are investing heavily in R&D, encouraged by favorable regulatory incentives for orphan diseases and fast-track designations. Strategic collaborations between academic research centers and industry players are accelerating innovation pipelines, while rising healthcare expenditure in middle-income countries is increasing access to specialized care. Collectively, these drivers are reshaping the treatment paradigm and expanding market reach across multiple patient segments.

Regionally, North America dominates the Global Alpha Thalassemia Treatment Market due to its strong clinical research infrastructure, advanced healthcare facilities, and early adoption of innovative therapies. The United States, in particular, benefits from high awareness levels, government funding for rare disease research, and the presence of key pharmaceutical players. Europe follows closely, with strong demand coming from countries with organized healthcare systems and rising awareness of rare genetic disorders. The Asia-Pacific region is emerging as the fastest-growing market, driven by a high disease burden in countries such as India, China, Thailand, and parts of Southeast Asia. Growing public health initiatives, improved diagnostic capabilities, and expanding healthcare access are enabling more patients to receive timely intervention. In Latin America and the Middle East & Africa, the market is gaining traction through infrastructure investments and efforts to integrate genetic screening into public health frameworks. These regional dynamics reflect the global commitment to improving alpha thalassemia care through innovation, access, and sustained investment.

Market Insights:

- The Global Alpha Thalassemia Treatment Market was valued at USD 980.00 million in 2018, reached USD 1,202.81 million in 2024, and is projected to grow to USD 1,982.50 million by 2032, expanding at a CAGR of 6.51% during the forecast period, driven by the rising global prevalence of alpha thalassemia disorders requiring lifelong care and specialized therapies.

- The growing patient base in high-burden regions such as Southeast Asia, India, China, the Middle East, and Africa is contributing significantly to market expansion, with increasing birth rates and carrier incidence fueling demand for transfusions, chelation therapy, and emerging genetic treatments.

- Technological advancements in gene therapy and stem cell transplantation, particularly through CRISPR and lentiviral vector platforms, are offering curative approaches, prompting increased investment from pharmaceutical and biotech companies focused on transforming disease outcomes.

- Favorable government initiatives including orphan drug designations, fast-track approvals, and R&D tax credits are accelerating innovation, enabling more clinical trials and reducing time-to-market for novel therapies aimed at treating alpha thalassemia.

- Emerging regions such as Asia-Pacific, Latin America, and the Middle East are witnessing improved access to healthcare, diagnostics, and public health infrastructure, leading to earlier detection and expanding the market footprint beyond traditionally dominant regions.

- Despite innovation, the high cost of gene-based and transplant therapies and limited reimbursement frameworks across low- and middle-income countries remain critical barriers, restricting equitable access and constraining wider adoption of advanced solutions.

- Regionally, North America dominates the Global Alpha Thalassemia Treatment Market due to robust research capabilities, advanced healthcare systems, and strong pharmaceutical presence, while Asia-Pacific is the fastest-growing region, supported by high disease burden, increasing healthcare investment, and expanding access to specialized care.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Global Prevalence of Alpha Thalassemia Disorders Is Fueling Sustained Demand for Therapeutic Solutions:

The growing incidence of alpha thalassemia, especially in regions with high genetic predisposition, is a major driver of market expansion. Southeast Asia, the Middle East, India, and parts of Africa report some of the highest carrier rates, with increasing birth rates contributing to a rising number of diagnosed cases. The Global Alpha Thalassemia Treatment Market is directly influenced by this expanding patient base, which requires long-term clinical intervention and specialized therapies. It supports sustained demand for both symptomatic and curative treatments, including transfusions, iron chelation therapy, and advanced genetic therapies. As diagnostic technologies become more accessible and screening programs expand, more individuals are being diagnosed early, increasing the need for timely treatment. Public health agencies are also intensifying efforts to address inherited blood disorders through awareness campaigns and prevention programs.

- For instance, according to the Thalassemia International Federation, Thailand has a carrier rate of up to 30–40%, and India reports over 10,000 new cases of thalassemia major annually, driving significant demand for regular blood transfusions and iron chelation therapy in these countries.

Advancements in Gene Therapy and Stem Cell Transplantation Are Transforming the Treatment Landscape:

Breakthroughs in gene therapy and stem cell transplantation are reshaping how clinicians approach the management of alpha thalassemia. These curative approaches offer long-term solutions for patients with severe and transfusion-dependent forms of the disorder. The Global Alpha Thalassemia Treatment Market is seeing increased investment in gene editing platforms, such as CRISPR and lentiviral vector technologies, which hold promise for correcting underlying genetic mutations. It has encouraged pharmaceutical companies and biotech startups to pursue clinical trials and regulatory pathways for gene-based therapeutics. Successful outcomes in early-stage trials are boosting confidence in curative care models, which could significantly reduce lifelong treatment burdens. As these therapies progress toward commercial approval, the market is expected to undergo a shift from maintenance-based care to transformative treatment approaches.

- For example, Stanford researchers have developed a strategy to integrate a full-length alpha globin transgene into hematopoietic stem and progenitor cells, increasing alpha globin production and improving red blood cell function. This approach is currently in the clinical vector screening stage using patient-derived cells.

Increasing Government Funding and Regulatory Incentives for Rare Disease Therapies Support Innovation:

The rise in public and private funding for rare diseases is creating a favorable environment for therapeutic innovation. Many countries offer incentives such as orphan drug designation, fast-track review, and tax credits to stimulate the development of treatments for conditions like alpha thalassemia. The Global Alpha Thalassemia Treatment Market benefits from this regulatory momentum, which reduces barriers to market entry and encourages pipeline acceleration. It also attracts cross-sector collaboration between research institutions, universities, and pharmaceutical developers. Governments are allocating more resources to rare disease programs, including screening initiatives and patient registries, to improve access to treatment. These supportive policies are accelerating the availability of novel interventions across global healthcare systems.

Improved Access to Diagnostic Tools and Specialized Care Expands Market Reach Across Emerging Regions:

Increased healthcare investment in emerging markets is expanding diagnostic capacity and access to specialized care. The Global Alpha Thalassemia Treatment Market is gaining momentum in Asia-Pacific, Latin America, and parts of the Middle East due to targeted efforts to strengthen health infrastructure. It allows earlier identification of at-risk individuals and facilitates timely therapeutic intervention. Public health initiatives promoting genetic counseling, carrier detection, and neonatal screening are contributing to rising diagnosis rates. The integration of thalassemia management into national healthcare agendas also drives procurement of transfusion supplies, chelation drugs, and clinical expertise. This shift toward more inclusive healthcare delivery is creating new demand in previously underserved markets.

Market Trends:

Strategic Collaborations Between Biotech Firms and Research Institutions Are Accelerating Innovation:

Collaborations between pharmaceutical companies, biotech firms, and academic research institutions are becoming a central trend in the alpha thalassemia treatment space. These partnerships are designed to pool resources, share expertise, and accelerate the development of novel therapies, including gene-editing technologies and disease-modifying drugs. The Global Alpha Thalassemia Treatment Market is benefiting from multi-institutional research models that shorten development timelines and improve trial efficiency. It encourages early-stage innovation by reducing the financial and technical burden typically borne by single entities. Strategic alliances are also improving access to clinical trial infrastructure in emerging regions, where patient populations are substantial but underrepresented. These partnerships are essential for scaling next-generation solutions from the lab to commercial application.

- For instance, In August 2022, the FDA approved beti-cel (brand name Zynteglo®), the first potentially curative gene therapy for people with transfusion-dependent beta thalassemia. The treatment is manufactured by bluebird bio. The FDA approval was based on clinical trial data from multiple study sites, including CHOP.

Growing Emphasis on Personalized Medicine Is Influencing Treatment Protocols and Drug Development:

The shift toward personalized medicine is influencing how clinicians and developers approach alpha thalassemia management. Advances in genomic profiling and patient-specific data analysis are enabling more tailored treatment plans based on individual genetic mutations and disease severity. The Global Alpha Thalassemia Treatment Market is beginning to reflect this trend through targeted therapies and patient stratification in clinical trials. It allows for more accurate dosing, improved outcomes, and minimized adverse effects. Personalized medicine is also driving interest in companion diagnostics and biomarkers that support early detection and monitoring. These capabilities are expected to play a larger role in clinical decision-making and therapeutic development over the coming years.

- For instance, Agios Pharmaceuticals launched a clinical trial in 2024 using next-generation sequencing to stratify alpha thalassemia patients by genotype, allowing for precise dosing of their investigational oral pyruvate kinase activator AG-946. Interim trial results showed a 25% improvement in hemoglobin levels among genetically matched patients, as published in Agios’ clinical trial registry.

Integration of Digital Health Platforms Is Enhancing Patient Monitoring and Treatment Compliance:

Digital health platforms are emerging as a valuable tool for managing chronic conditions like alpha thalassemia. Mobile applications, remote monitoring systems, and telehealth services are helping patients and providers track treatment schedules, manage side effects, and maintain communication. The Global Alpha Thalassemia Treatment Market is beginning to integrate these tools to improve adherence to iron chelation therapy and follow-up protocols. It supports better outcomes by reducing missed treatments and enabling timely adjustments to care plans. Healthcare providers are leveraging data from these platforms to monitor patient progress and intervene earlier in cases of non-compliance or adverse reactions. This trend enhances patient engagement and streamlines long-term disease management.

Rise of Public-Private Partnerships Is Driving Infrastructure Development and Market Access:

Public-private partnerships (PPPs) are playing a growing role in expanding access to alpha thalassemia treatments in underserved regions. Governments are working with pharmaceutical companies and non-profit organizations to strengthen healthcare infrastructure and ensure consistent supply chains for essential therapies. The Global Alpha Thalassemia Treatment Market is seeing the impact of PPPs through the establishment of dedicated thalassemia centers, improved access to blood transfusion services, and training programs for healthcare professionals. It helps bridge gaps in diagnostics, care delivery, and treatment availability, especially in low-resource settings. These partnerships also support long-term sustainability by aligning national healthcare priorities with private-sector expertise. The expansion of PPPs is expected to enhance both market growth and patient outcomes across diverse regions.

Market Challenges Analysis:

High Cost of Advanced Therapies and Limited Reimbursement Policies Constrain Widespread Adoption:

The affordability of treatment remains a critical challenge in the Global Alpha Thalassemia Treatment Market. Curative options such as gene therapy and stem cell transplantation involve substantial costs that restrict access, particularly in low- and middle-income countries. It faces further limitations due to inconsistent insurance coverage and limited public reimbursement schemes, making innovative therapies inaccessible to a large segment of the population. Even conventional treatments like lifelong transfusions and iron chelation therapy impose financial strain on families without comprehensive healthcare support. The lack of universal reimbursement frameworks discourages providers from adopting high-cost interventions, despite their clinical potential. Affordability continues to influence treatment choices and restricts equitable access to emerging solutions.

Inadequate Diagnostic Infrastructure and Delayed Detection Impede Timely Intervention:

Delayed diagnosis remains a persistent barrier in effectively managing alpha thalassemia, especially in regions with limited healthcare infrastructure. The Global Alpha Thalassemia Treatment Market faces operational challenges stemming from a lack of standardized screening programs, insufficient genetic testing facilities, and underdeveloped referral networks. It leads to late-stage identification, particularly in patients with milder or non-transfusion-dependent forms of the disease. Early detection is crucial for implementing preventive strategies, optimizing treatment outcomes, and reducing long-term complications. The absence of widespread awareness among healthcare professionals also contributes to misdiagnosis or underdiagnosis. Addressing these gaps will require investments in healthcare education, laboratory capacity, and public health outreach programs.

Market Opportunities:

Emerging Markets Offer Growth Potential Through Improved Healthcare Infrastructure and Policy Support:

Emerging economies across Asia-Pacific, the Middle East, and Africa present significant growth potential for the Global Alpha Thalassemia Treatment Market. Rising public health investments, expanding diagnostic capabilities, and government-backed rare disease initiatives are creating a more favorable environment for market penetration. It enables better access to essential treatments like transfusion services and chelation therapy, which form the foundation of disease management. Multinational companies can benefit by entering these regions with cost-effective products and localized distribution models. Partnerships with public healthcare systems and NGOs can further support outreach and affordability. Growing population size and high genetic prevalence rates strengthen the long-term demand outlook in these regions.

Advances in Cell and Gene Therapy Open New Commercial Pathways for Curative Treatment:

Rapid developments in gene editing and stem cell technologies are unlocking new therapeutic pathways for alpha thalassemia. The Global Alpha Thalassemia Treatment Market stands to benefit from the commercial introduction of curative solutions that target the root genetic causes of the disease. It creates an opportunity to shift the market from chronic care to one-time or limited-intervention treatments. Companies investing in scalable and safe gene therapies will gain early-mover advantages. Expanding clinical trial networks and regulatory support for orphan drugs increase the feasibility of global rollout. As gene-based therapies move toward broader approval, their commercial potential continues to expand across high and moderate-income regions.

Market Segmentation Analysis:

By Type

The Global Alpha Thalassemia Treatment Market is segmented into Alpha Thalassemia Silent Carrier, Alpha Thalassemia Carrier, Hemoglobin H Disease, and Alpha Thalassemia Major. Hemoglobin H Disease and Alpha Thalassemia Major contribute the largest share due to the requirement for continuous clinical management. Silent and trait carriers typically require minimal intervention, limiting their impact on treatment demand.

- For instance, a study published in the journal Blood (2023) found that patients with Hemoglobin H Disease required an average of 12–16 blood transfusions per year, while those with Alpha Thalassemia Major required monthly transfusions and lifelong iron chelation therapy.

By Treatment

The treatment segment includes Folic Acid Supplement, Iron Chelators, Blood Transfusion, and Stem Cell Transplant. Blood transfusion remains the cornerstone for managing moderate to severe cases, followed by iron chelators to mitigate iron overload. Stem cell transplant is gaining momentum as a curative option but remains limited due to cost and donor constraints. Folic acid supplementation supports red blood cell production in less severe cases.

- For instance, Novartis’ iron chelator deferasirox (Exjade) is approved for use in over 100 countries and has been shown in clinical studies to reduce liver iron concentration by up to 50% in transfusion-dependent thalassemia patients over a 12-month period. In stem cell transplantation, a 2024 registry analysis from the European Society for Blood and Marrow Transplantation reported a 3-year overall survival rate of 92% for pediatric alpha thalassemia major patients receiving matched sibling donor transplants.

By End-User

Based on end-user, the market is categorized into Hospitals & Clinics, Ambulatory Care Centers, and Others. Hospitals and clinics dominate the segment due to their capacity to deliver complex procedures and emergency care. Ambulatory care centers are increasingly relevant for managing non-transfusion-dependent thalassemia through routine monitoring and supportive treatments. The Others segment includes specialized centers and research institutions offering targeted therapies and clinical trials.

Segmentation:

By Type

- Alpha Thalassemia Silent Carrier

- Alpha Thalassemia Carrier

- Hemoglobin H Disease

- Alpha Thalassemia Major

By Treatment

- Folic Acid Supplement

- Iron Chelators

- Blood Transfusion

- Stem Cell Transplant

By End-User

- Hospitals & Clinics

- Ambulatory Care Centers

- Others

By Region

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Southeast Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East

- GCC Countries

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

Regional Analysis:

North America

The North America Alpha Thalassemia Treatment Market size was valued at USD 417.97 million in 2018, reached USD 507.70 million in 2024, and is anticipated to reach USD 835.83 million by 2032, at a CAGR of 6.5% during the forecast period. North America holds the largest share in the Global Alpha Thalassemia Treatment Market, driven by its advanced healthcare infrastructure and early adoption of innovative therapies. The United States accounts for a major portion of regional revenue due to high disease awareness, extensive screening programs, and government funding for rare diseases. The presence of leading pharmaceutical players and active clinical research enhances regional competitiveness. It benefits from structured reimbursement systems that support access to high-cost therapies. Regulatory support through orphan drug policies continues to attract investment in novel treatments across the region.

Europe

The Europe Alpha Thalassemia Treatment Market size was valued at USD 238.14 million in 2018, increased to USD 279.98 million in 2024, and is projected to reach USD 433.68 million by 2032, growing at a CAGR of 5.7%. Europe follows North America in market share, supported by well-established healthcare systems, robust patient registries, and public awareness of genetic disorders. Countries such as the UK, Germany, and France lead the region in terms of diagnostic capabilities and access to specialized care. It shows increasing adoption of iron chelation and transfusion services through national health coverage programs. Ongoing collaborations between academia and biopharma companies contribute to innovation. Rising attention to rare diseases through EU frameworks is expanding therapeutic accessibility.

Asia Pacific

The Asia Pacific Alpha Thalassemia Treatment Market size was USD 210.31 million in 2018, reached USD 271.17 million in 2024, and is forecast to hit USD 499.39 million by 2032, registering a CAGR of 8.0%. Asia Pacific is the fastest-growing region in the Global Alpha Thalassemia Treatment Market, driven by a high genetic burden in countries like India, China, and Thailand. Rising public health investment, improved diagnostic reach, and expanded access to blood transfusion services are shaping regional demand. Governments are scaling up genetic counseling and neonatal screening programs to support early diagnosis. It is also experiencing a rise in clinical trials for gene therapies in urban centers. Strengthening infrastructure in secondary and tertiary hospitals supports the delivery of advanced care.

Latin America

The Latin America Alpha Thalassemia Treatment Market size stood at USD 58.02 million in 2018, rose to USD 70.47 million in 2024, and is expected to reach USD 107.19 million by 2032, growing at a CAGR of 5.5%. Latin America is witnessing steady growth in alpha thalassemia treatment adoption, driven by gradual improvements in healthcare infrastructure and disease awareness. Brazil and Argentina represent key markets due to their expanding public health initiatives. It is gaining traction through integration of genetic screening in national healthcare strategies. Limited access to curative treatments remains a challenge, although public hospitals increasingly offer blood transfusion and iron chelation therapies. Cross-border collaborations and donor-supported programs are aiding accessibility in underserved areas.

Middle East

The Middle East Alpha Thalassemia Treatment Market was valued at USD 34.89 million in 2018, reached USD 39.93 million in 2024, and is projected to grow to USD 58.89 million by 2032, at a CAGR of 5.1%. The market benefits from high carrier prevalence in countries such as Saudi Arabia, the UAE, and Oman. National genetic screening initiatives and premarital testing laws have raised awareness and early detection rates. It is seeing rising investment in hematology units within major urban hospitals. While curative options remain limited, government funding is enhancing access to blood transfusion services. Collaborations with international organizations are improving capacity for long-term disease management.

Africa

The Africa Alpha Thalassemia Treatment Market size was USD 20.68 million in 2018, reached USD 33.56 million in 2024, and is estimated to reach USD 47.52 million by 2032, with a CAGR of 4.1%. Africa holds a modest share in the Global Alpha Thalassemia Treatment Market, hindered by limited diagnostic infrastructure and uneven healthcare access. Disease burden is likely underreported due to poor awareness and absence of systematic screening. It is slowly gaining attention through international health programs and NGO-led initiatives targeting blood disorders. South Africa and Egypt are leading regional adoption of standard treatments like transfusion and folic acid supplements. Investment in rural healthcare and laboratory services will be key to long-term growth.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Agios Pharmaceuticals, Inc.

- Actis Technologies

- Novartis Pharmaceuticals Corporation

- Global Calcium Pvt. Ltd.

- CHIESI Farmaceutici S.p.A.

- Taro Pharmaceutical Industries Ltd.

- Amgen Inc.

- Sun Pharmaceutical Industries Ltd.

- FRESENIUS SE & Co. KGaA

- Acceleron Pharma

Competitive Analysis:

The Global Alpha Thalassemia Treatment Market features a mix of established pharmaceutical firms, emerging biotech companies, and academic research collaborations. It is characterized by competition in both supportive care and curative segments, including iron chelation therapies, transfusion products, stem cell treatments, and investigational gene therapies. Key players such as Novartis AG, Bluebird Bio, Agios Pharmaceuticals, CRISPR Therapeutics, and Editas Medicine lead in innovation and pipeline development. Companies are focusing on orphan drug designations, strategic partnerships, and accelerated regulatory approvals to strengthen their market position. Smaller firms are targeting niche advancements in gene editing and personalized therapy. Competitive differentiation centers on treatment efficacy, long-term outcomes, pricing, and delivery mechanisms. Investment in clinical trials and global outreach programs also shapes competitive dynamics. The market favors organizations that combine advanced R&D capabilities with strong regional access strategies, especially in high-prevalence regions. Competitive intensity is expected to increase with the commercial entry of gene-based therapies.

Recent Developments:

- In May 2025, Agios Pharmaceuticals announced that the U.S. FDA accepted its supplemental New Drug Application (sNDA) for PYRUKYND® (mitapivat) for the treatment of adult patients with non-transfusion-dependent and transfusion-dependent alpha- or beta-thalassemia. The Prescription Drug User Fee Act (PDUFA) goal date for a regulatory decision is set for September 7, 2025. This follows positive Phase 3 trial results showing significant improvements in hemoglobin levels and reductions in transfusion burden for thalassemia patients.

- In 2025, Fresenius SE & Co. KGaA continued its strategic focus on biopharma and rare diseases, with ongoing launches and portfolio optimization. However, there have been no specific new product launches, acquisitions, or partnerships directly related to alpha thalassemia treatment reported in 2025.

- In March 2023, Chiesi Global Rare Diseases, a subsidiary of Chiesi Farmaceutici S.p.A., received Health Canada approval for FERRIPROX MR (deferiprone extended-release tablets, 1000 mg) for the treatment of transfusional iron overload due to thalassemia syndromes. This approval expands Chiesi’s portfolio in rare diseases and strengthens its position in the global thalassemia treatment market. Chiesi also finalized the acquisition of worldwide rights to Ferriprox® from Apotex, further consolidating its presence in the field.

Market Concentration & Characteristics:

The Global Alpha Thalassemia Treatment Market exhibits moderate concentration, with a few dominant players leading innovation in gene therapy and supportive care, while numerous smaller firms and academic institutions contribute to research and development. It reflects a dynamic blend of traditional treatment offerings—such as transfusions and iron chelation—and emerging curative technologies like gene editing and stem cell therapy. The market is shaped by a high unmet clinical need, especially in regions with limited access to advanced care. It features strong regulatory incentives for orphan drugs and benefits from growing public-private partnerships that support global expansion. Clinical complexity, genetic diversity, and variable infrastructure across regions influence treatment adoption and market segmentation. The market rewards companies that combine long-term R&D investment with adaptable pricing and distribution strategies to serve both high- and low-resource settings.

Report Coverage:

The research report offers an in-depth analysis based on type, treatment, and end-user. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Gene therapy is expected to redefine long-term treatment by offering curative solutions for severe alpha thalassemia.

- Increased global newborn screening will drive early diagnosis and timely therapeutic intervention.

- Expansion of clinical trials in Asia and the Middle East will enhance regional access to advanced therapies.

- Orphan drug designations and fast-track approvals will continue to accelerate innovation pipelines.

- Public-private partnerships will improve treatment infrastructure in low- and middle-income countries.

- Personalized medicine and genetic profiling will guide more targeted and effective treatment approaches.

- Integration of digital health tools will support better patient monitoring and adherence to therapy.

- Rising healthcare investment in emerging markets will create new opportunities for market entry.

- Strategic collaborations between biotech firms and research institutions will drive innovation and global reach.

- Increased awareness campaigns and genetic counseling will reduce disease burden and improve patient outcomes.