Market Overview:

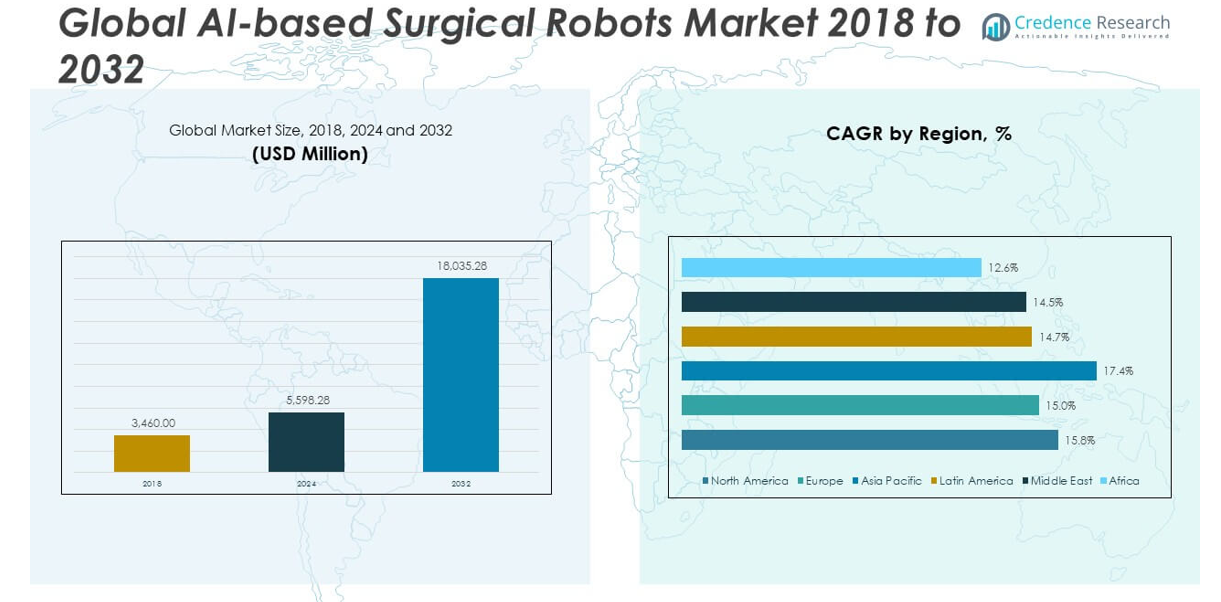

The Global AI-based Surgical Robots Market size was valued at USD 3,460.00 million in 2018 to USD 5,598.28 million in 2024 and is anticipated to reach USD 18,035.28 million by 2032, at a CAGR of 15.83% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| AI-based Surgical Robots Markett Size 2024 |

USD 5,598.28 million |

| AI-based Surgical Robots Market, CAGR |

15.83% |

| AI-based Surgical Robots Market Size 2032 |

USD 18,035.28 million |

Key drivers accelerating this market include the surging prevalence of chronic diseases such as cancer, orthopedic disorders, and cardiovascular conditions that demand complex surgical care. The rising preference for minimally invasive surgery has created a favorable environment for AI-enhanced surgical robots, as they offer greater precision, smaller incisions, reduced pain, and quicker patient recovery compared to traditional procedures. Technological advancements are further strengthening the market—robotic systems now incorporate AI algorithms for real-time decision support, machine learning for adaptive performance, and computer vision for enhanced anatomical recognition. These capabilities not only improve surgical accuracy but also assist in preoperative planning and intraoperative guidance. Another significant driver is the shortage of skilled surgeons in many regions, particularly in rural or underserved areas, which has led healthcare institutions to invest in surgical robots that can help bridge workforce gaps.

Regionally, North America leads the global market with the largest revenue share, driven by advanced healthcare infrastructure, early technology adoption, and strong reimbursement frameworks in the United States and Canada. In 2023, North America accounted for nearly 41%–50% of the total market revenue, and is expected to maintain this lead due to continued innovation and favorable government policies supporting AI in healthcare. The European market follows closely, with countries such as Germany, the UK, France, and the Netherlands witnessing increased penetration of surgical robotics in orthopedic, urological, and general surgeries. Supportive initiatives from the European Commission and national healthcare bodies are playing a vital role in fostering this growth. Meanwhile, the Asia-Pacific region is emerging as the fastest-growing market, propelled by rising healthcare investments, aging populations, and heightened awareness of the benefits of AI-assisted surgeries. Countries like China, Japan, India, and South Korea are seeing growing installations of AI-based surgical systems across both public and private hospitals. This surge is also supported by regional government programs aimed at modernizing healthcare delivery and promoting minimally invasive surgical techniques. Although currently smaller in market share, Latin America, the Middle East, and Africa are witnessing gradual growth fueled by infrastructure development, expanding medical tourism, and growing demand for technologically advanced healthcare solutions.

Market Insights:

- The Global AI-based Surgical Robots Market grew from USD 3,460.00 million in 2018 to USD 5,598.28 million in 2024 and is projected to reach USD 18,035.28 million by 2032, registering a CAGR of 15.83% during the forecast period.

- Rising patient demand for minimally invasive surgeries is pushing the adoption of AI-powered robotic systems that offer higher precision, quicker recovery, and reduced post-operative complications.

- Advancements in artificial intelligence and robotics, including real-time image guidance and machine learning for surgical planning, are enhancing system performance and expanding clinical applications.

- The global increase in chronic diseases such as cancer, cardiovascular disorders, and neurological conditions is creating sustained demand for advanced, repeatable, and precise surgical solutions.

- A growing shortage of trained surgeons, particularly in rural and underserved areas, is encouraging hospitals to invest in AI-based surgical robots that can support procedural consistency and reduce manual workload.

- High initial costs and ongoing maintenance expenses limit accessibility in low- and middle-income regions, while complex regulatory requirements delay product approvals and increase compliance burdens.

- North America dominates the market due to early technology adoption and supportive infrastructure, while Asia-Pacific is the fastest-growing region, driven by healthcare investment, aging populations, and government-backed modernization efforts.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Rising Demand for Minimally Invasive Surgical Procedures:

The growing preference for minimally invasive surgeries (MIS) is a major force driving the Global AI-based Surgical Robots Market. Patients increasingly choose MIS due to reduced post-operative pain, lower risk of infection, shorter hospital stays, and faster recovery times. Surgeons benefit from enhanced precision and control provided by robotic assistance, which translates to better clinical outcomes. Hospitals are investing in robotic systems to improve surgical efficiency and reduce the physical strain on medical staff. As patient awareness of MIS advantages increases, demand for AI-integrated robotic systems continues to rise. It positions surgical robots as essential tools in modern operating rooms across specialties such as urology, gynecology, orthopedics, and general surgery.

- For instance, Intuitive Surgical’s da Vinci Surgical System has been used in over 12 million procedures worldwide, with studies showing a 52% reduction in hospital stay duration for prostatectomy patients compared to traditional open surgery.

Technological Advancements in Artificial Intelligence and Robotics:

Rapid advancements in artificial intelligence and robotic technologies significantly strengthen market growth. AI algorithms are enhancing image-guided surgery, real-time decision-making, and motion scaling, while robotics enable superior dexterity and access to complex anatomical regions. The integration of machine learning improves surgical planning, outcome prediction, and adaptive performance during procedures. Companies are continuously innovating to build compact, cost-effective, and cloud-connected systems that support real-time collaboration and diagnostics. These developments make robotic-assisted surgeries safer, faster, and more reliable, fostering wider acceptance among surgeons and hospitals. The Global AI-based Surgical Robots Market reflects these innovations through increasing deployment in both developed and developing healthcare systems.

- For instance, Medtronic’s Hugo™ robotic-assisted surgery system leverages AI-driven analytics and has performed over 1,000 clinical procedures since its launch, with its Touch Surgery™ Enterprise platform supporting real-time intraoperative guidance and post-operative review.

Increasing Global Burden of Chronic Diseases Requiring Surgical Intervention:

The rising prevalence of chronic diseases such as cancer, cardiovascular disorders, and neurological conditions is pushing demand for advanced surgical solutions. Many of these conditions require precise, timely, and repeatable interventions that robotic systems can deliver. Robotic platforms equipped with AI capabilities enable minimally invasive treatment options, particularly for delicate or high-risk procedures. The aging global population also contributes to a higher surgical burden, with older patients requiring more frequent and complex procedures. Healthcare systems are adopting surgical robots to manage patient loads while maintaining quality standards. It supports long-term cost-efficiency by reducing complication rates and hospital readmissions.

Shortage of Skilled Surgeons and Emphasis on Workflow Optimization:

The global shortage of experienced surgeons is prompting healthcare institutions to rely more heavily on AI-based robotic systems. Surgical robots can standardize procedures, enhance consistency, and allow for remote collaboration and mentoring. AI-driven platforms can support less experienced surgeons by providing real-time feedback and intelligent assistance during operations. Hospitals are turning to robotic systems to minimize human error, streamline workflows, and improve overall surgical throughput. These systems also collect and analyze procedural data, contributing to continuous improvement in technique and patient safety. It aligns with hospital goals of achieving better outcomes while managing operational costs.

Market Trends:

Expansion of Outpatient and Ambulatory Surgical Centers:

A growing number of outpatient and ambulatory surgical centers (ASCs) are adopting AI-based robotic systems to enhance procedure efficiency and reduce patient turnaround time. The shift toward same-day surgeries reflects healthcare’s focus on cost containment, convenience, and shorter recovery periods. AI-powered surgical robots are being optimized for smaller, more mobile settings with limited space and faster procedural cycles. Companies are designing compact, modular robotic systems that can seamlessly integrate into outpatient environments. These installations lower the burden on hospitals and widen patient access to advanced surgical options. The Global AI-based Surgical Robots Market is witnessing increased penetration into outpatient care models that prioritize affordability and throughput.

- For instance, Stryker’s Mako SmartRobotics™ system has been installed in over 1,500 facilities globally, with more than 50% of its knee and hip procedures now performed in outpatient or ASC settings.

Integration of Cloud-Based Analytics and Remote Surgical Collaboration:

Cloud integration is transforming the way surgical data is captured, stored, and analyzed. Robotic platforms now include cloud-connected interfaces that enable remote monitoring, procedural benchmarking, and post-operative analytics. Surgeons and hospitals can collaborate in real time, access training modules, and review surgical performance metrics through centralized platforms. The trend supports continuous learning, quality assurance, and system-wide standardization. AI-powered robots leveraging cloud capabilities contribute to clinical transparency and efficiency, particularly in multi-site hospital networks. It strengthens interoperability across facilities and encourages adoption in large health systems.

- For instance, Johnson & Johnson’s Ottava platform is designed with cloud-based connectivity, enabling remote proctoring and performance analytics across multiple hospital sites, supporting remote collaborations in pilot programs.

Growth of Customized and Specialty-Specific Robotic Systems:

Manufacturers are moving away from one-size-fits-all systems and developing robotic platforms tailored to specific surgical fields. These specialty systems focus on particular procedures such as spine surgery, joint replacement, ENT, or pediatric interventions. Customization improves usability, reduces cost, and enhances surgeon confidence by focusing features on specific clinical needs. AI tools embedded within these platforms assist with workflow personalization, patient-specific planning, and predictive analytics. Hospitals increasingly prefer targeted solutions that address defined surgical demands over general-purpose robots. It supports deeper market segmentation and opens new growth avenues for technology providers.

Rising Investment in Training, Simulation, and Virtual Reality Integration:

Training platforms and simulation-based education are becoming critical components of robotic surgery programs. The integration of virtual reality (VR), augmented reality (AR), and immersive simulators is reshaping how surgeons are trained to use AI-based robotic systems. These tools provide realistic practice environments, allowing users to hone skills without patient risk. Hospitals are investing in dedicated simulation suites and digital modules to accelerate skill acquisition and maintain procedural proficiency. It enhances surgeon readiness and reduces onboarding time for new technologies. The Global AI-based Surgical Robots Market benefits from this trend as training innovations lower the adoption barrier and expand the surgeon base.

Market Challenges Analysis:

High Capital Costs and Limited Affordability in Emerging Markets:

The high upfront cost of AI-based surgical robotic systems remains a significant barrier to widespread adoption, particularly in low- and middle-income countries. Procurement, installation, training, and maintenance expenses place a heavy financial burden on hospitals with limited budgets. Many healthcare institutions in emerging markets prioritize basic infrastructure and essential care, limiting their capacity to invest in high-end surgical robotics. This cost challenge slows the penetration rate in developing regions, even when clinical benefits are evident. The Global AI-based Surgical Robots Market continues to expand in high-income countries, but its affordability gap hinders balanced global growth. Strategic financing models and public-private partnerships are required to address this disparity.

Complex Regulatory Landscape and Integration Challenges:

AI-based surgical robots face a complex and evolving regulatory environment that slows market entry and product innovation. Regulatory agencies require extensive clinical validation, cybersecurity assurance, and performance data before approving robotic platforms for clinical use. These requirements extend development timelines and increase compliance costs. Integration challenges within hospitals—such as compatibility with existing IT infrastructure, staff retraining, and workflow adjustments—add to adoption hurdles. The Global AI-based Surgical Robots Market must navigate these regulatory and operational complexities while ensuring patient safety and clinical efficacy. Clearer standards and harmonized global frameworks will be essential to streamline market access.

Market Opportunities:

Expansion into Emerging Economies with Growing Healthcare Investments:

Emerging markets present a strong growth opportunity for the Global AI-based Surgical Robots Market. Rising healthcare investments, improving hospital infrastructure, and increased government focus on digital health are creating a favorable environment for robotic surgical systems. Countries across Asia-Pacific, Latin America, and the Middle East are actively upgrading surgical capabilities to meet rising patient demand. Local manufacturing partnerships and tiered pricing strategies can help companies enter these regions more effectively. It enables broader deployment of AI-driven systems in secondary and tertiary care centers. Strategic collaborations with public and private healthcare entities will accelerate regional adoption.

Development of Cost-Effective and Portable Robotic Platforms:

There is significant potential in designing compact, scalable, and affordable AI-based surgical robots tailored for outpatient centers and smaller hospitals. These systems address the needs of facilities with limited budgets and physical space, expanding the market beyond large tertiary institutions. The Global AI-based Surgical Robots Market can benefit from modular systems that offer flexibility and ease of integration without compromising on functionality. Companies investing in simplified interfaces, cloud connectivity, and reduced hardware footprints will appeal to a wider customer base. It supports the democratization of surgical robotics and opens untapped demand in under-resourced regions.

Market Segmentation Analysis:

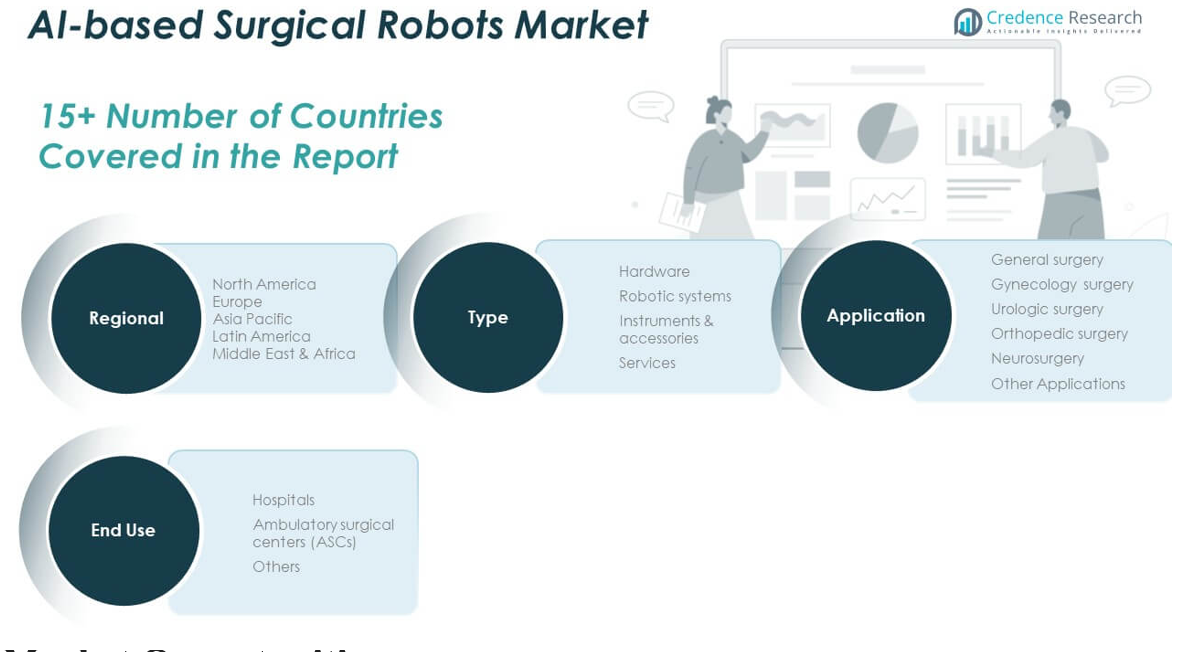

By Type

The Global AI-based Surgical Robots Market by type is dominated by the hardware segment, which includes robotic systems and instruments & accessories. Robotic systems account for the largest share due to their integral role in surgical procedures and high capital investment. Instruments and accessories generate recurring revenue through continuous demand for surgical tools and consumables. The services segment is also expanding as hospitals and clinics invest in maintenance, software updates, and operator training to ensure optimal performance and compliance.

- For instance, Zimmer Biomet’s ROSA® Knee System has seen over 40,000 procedures performed globally, with the company reporting a 30% year-over-year increase in demand for its robotic instruments and accessories.

By Application

The general surgery segment holds the largest share due to the wide range of procedures and early system adoption. Gynaecology surgery and urologic surgery are mature markets with established robotic use, especially for minimally invasive procedures. Orthopedic surgery and neurosurgery segments are witnessing rapid growth, driven by the need for high precision in bone and brain-related interventions. Other applications, including thoracic and colorectal surgeries, are expected to grow with advancements in imaging and navigation integration.

- For instance, CMR Surgical’s Versius® system has been adopted in over 130 hospitals worldwide, supporting more than 15,000 general, gynecological, and urological procedures since its commercial launch.

By End-Use

Hospitals are the primary end users, supported by robust budgets and comprehensive infrastructure that facilitate integration of robotic systems. Ambulatory Surgical Centers (ASCs) represent a fast-growing segment as compact and cost-efficient robots make outpatient robotic surgery viable. The others category, including academic and specialty clinics, is contributing to technology validation, procedural development, and early adoption, driving long-term expansion of the market.

Segmentation:

By Type Segment

- Hardware

- Robotic Systems

- Instruments & Accessories

- Services

By Application Segment

- General Surgery

- Gynaecology Surgery

- Urologic Surgery

- Orthopedic Surgery

- Neurosurgery

- Other Applications

By End-Use Segment

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America AI-based Surgical Robots Market size was valued at USD 1,393.69 million in 2018 to USD 2,230.32 million in 2024 and is anticipated to reach USD 7,176.27 million by 2032, at a CAGR of 15.8% during the forecast period. North America holds the largest share in the Global AI-based Surgical Robots Market, accounting for approximately 40% of total revenue. Advanced healthcare infrastructure, strong reimbursement systems, and early technology adoption drive growth across the United States and Canada. The U.S. leads the region due to high surgical volumes, favorable regulatory support, and heavy investment in R&D. Major hospitals across North America have integrated robotic systems into routine surgeries. Canada follows with steady growth, particularly in urology and gynecology applications. It continues to lead the global market in system innovation and clinical deployment.

Europe

The Europe AI-based Surgical Robots Market size was valued at USD 918.28 million in 2018 to USD 1,428.53 million in 2024 and is anticipated to reach USD 4,349.26 million by 2032, at a CAGR of 15.0% during the forecast period. Europe holds the second-largest market share, contributing approximately 25% of global revenue. Germany, the UK, and France are major contributors, with a high number of robotic installations across multi-specialty hospitals. Supportive EU regulations and national funding initiatives continue to accelerate adoption. Increasing focus on minimally invasive surgery in orthopedics, neurology, and oncology supports system expansion. Eastern European nations are gradually catching up, with rising investments in healthcare infrastructure. It remains a stable and innovation-friendly regional market.

Asia Pacific

The Asia Pacific AI-based Surgical Robots Market size was valued at USD 737.67 million in 2018 to USD 1,254.27 million in 2024 and is anticipated to reach USD 4,517.85 million by 2032, at a CAGR of 17.4% during the forecast period. Asia Pacific is the fastest-growing region, contributing nearly 22% of the global market. China, Japan, South Korea, and India are leading adopters, supported by government-backed healthcare reforms and increased private sector investment. Rising medical tourism, aging populations, and a growing middle-class fuel demand for advanced surgical options. Hospitals are increasingly adopting robotic platforms in oncology, gynecology, and general surgery. Local manufacturers are entering the market with affordable alternatives. It represents a high-growth region with expanding access and strong long-term potential.

Latin America

The Latin America AI-based Surgical Robots Market size was valued at USD 211.06 million in 2018 to USD 338.08 million in 2024 and is anticipated to reach USD 1,007.63 million by 2032, at a CAGR of 14.7% during the forecast period. Latin America holds around 6% of global market share, with Brazil and Mexico leading regional adoption. These countries are making progress in deploying robotic systems in urban hospitals and specialty clinics. The private healthcare sector is investing in AI-driven technologies for procedures in urology and general surgery. Cost and training remain key barriers, particularly in lower-income regions. Public-private collaborations and regional partnerships are slowly addressing these limitations. It shows steady growth with room for expanded access.

Middle East

The Middle East AI-based Surgical Robots Market size was valued at USD 142.55 million in 2018 to USD 217.18 million in 2024 and is anticipated to reach USD 636.74 million by 2032, at a CAGR of 14.5% during the forecast period. The Middle East is witnessing growing interest in robotic surgical systems, driven by national visions and investment in healthcare modernization. Saudi Arabia, UAE, and Israel are leading adopters with advanced facilities integrating robotic platforms. Medical tourism is driving demand for high-tech procedures, especially in private hospitals. The region’s market remains niche but is evolving with strong government support. High-end installations and focus on clinical excellence fuel adoption. It continues to attract manufacturers offering specialized robotic solutions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Accuray Incorporated

- Asensus Surgical US, Inc.

- CMR Surgical, Inc.

- Intuitive Surgical, Inc.

- Medtronic plc

- Meerecompany Inc.

- Moon Surgical

- Smith & Nephew

- Stryker Corporation

- Zimmer Biomet

Competitive Analysis:

The Global AI-based Surgical Robots Market is highly competitive, led by key players such as Intuitive Surgical, Medtronic, Stryker Corporation, Zimmer Biomet, and CMR Surgical. These companies focus on product innovation, clinical integration, and global expansion to strengthen their market positions. It sees increasing collaboration between technology firms and healthcare providers to accelerate AI integration and improve surgical outcomes. Emerging players like Moon Surgical and Meerecompany are entering the market with compact and cost-efficient systems, challenging traditional dominance. Major players invest in R&D, regulatory approvals, and strategic acquisitions to maintain their competitive edge. The market favors companies that offer a combination of precision, scalability, and data-driven performance. It continues to evolve with growing demand for specialized solutions, strong after-sales service, and real-time analytics, making technological differentiation a key success factor.

Recent Developments:

- In July 2025, Intuitive Surgical received CE mark approval for its fifth-generation da Vinci 5 Surgical System, authorizing its use for adult and pediatric minimally invasive procedures across Europe. The da Vinci 5 features over 150 enhancements, including force feedback technology and 10,000 times more computing power, aiming to improve patient outcomes and operational efficiency. This marks a significant milestone in Intuitive’s 30th year of robotic-assisted technology development.

- In April 2025, Medtronic submitted its Hugo™ soft tissue robotic surgery system for FDA approval with a urologic indication. The submission follows successful clinical studies demonstrating a 98.5% surgical success rate, surpassing the 85% benchmark. Hugo is already approved in over 25 countries, and this move positions Medtronic as a major competitor in the U.S. robotic surgery market.

- In April 2025, CMR Surgical secured over $200 million in new funding to accelerate the global rollout of its Versius soft tissue surgical system, with a particular focus on the U.S. market following FDA authorization for gallbladder removal procedures. This funding round is intended to support further innovation and expansion of Versius, which is now the second most widely used soft tissue surgical robot globally.

- In January 2025, Meerecompany signed a contract to supply its Revo-i surgical robotic system to Paraguay, marking its first entry into the South American market. This follows successful exports to Russia, Mongolia, and Uzbekistan in 2024, demonstrating the company’s expanding global reach and technological reliability.

Market Concentration & Characteristics:

The Global AI-based Surgical Robots Market is moderately concentrated, with a few dominant players holding significant market share and setting industry benchmarks. It is characterized by high entry barriers due to capital intensity, stringent regulatory requirements, and the need for continuous technological innovation. Leading companies maintain competitive advantages through proprietary technologies, extensive surgeon training programs, and strong distribution networks. It favors firms with robust R&D capabilities and a proven track record in clinical performance. The market exhibits high product differentiation, with vendors focusing on specialized systems tailored to specific surgical applications. It continues to evolve rapidly, driven by demand for precision, automation, and data-driven insights in surgical procedures.

Report Coverage:

The research report offers an in-depth analysis based on by type, application, and end-use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Global AI-based Surgical Robots Market is expected to witness sustained double-digit growth through 2032, driven by rising demand for precision surgeries.

- Advancements in AI, machine learning, and real-time data analytics will enhance robotic performance and expand clinical applications.

- Increasing healthcare investments in emerging economies will open new market opportunities for scalable robotic platforms.

- Development of compact, cost-effective systems will support adoption in outpatient and mid-sized surgical centers.

- Integration with cloud-based platforms will improve surgical planning, post-operative analysis, and cross-site collaboration.

- Regulatory support and fast-track approvals in key markets will accelerate the deployment of AI-based surgical systems.

- Rising medical tourism and demand for advanced surgical care will strengthen market growth in Asia Pacific and the Middle East.

- Collaborations between tech firms and medical device companies will drive innovation and platform integration.

- Growing emphasis on personalized and minimally invasive surgery will increase the need for intelligent surgical robots.

- Expansion of training and simulation infrastructure will reduce the learning curve and encourage wider surgeon adoption.