Battery Backup Market

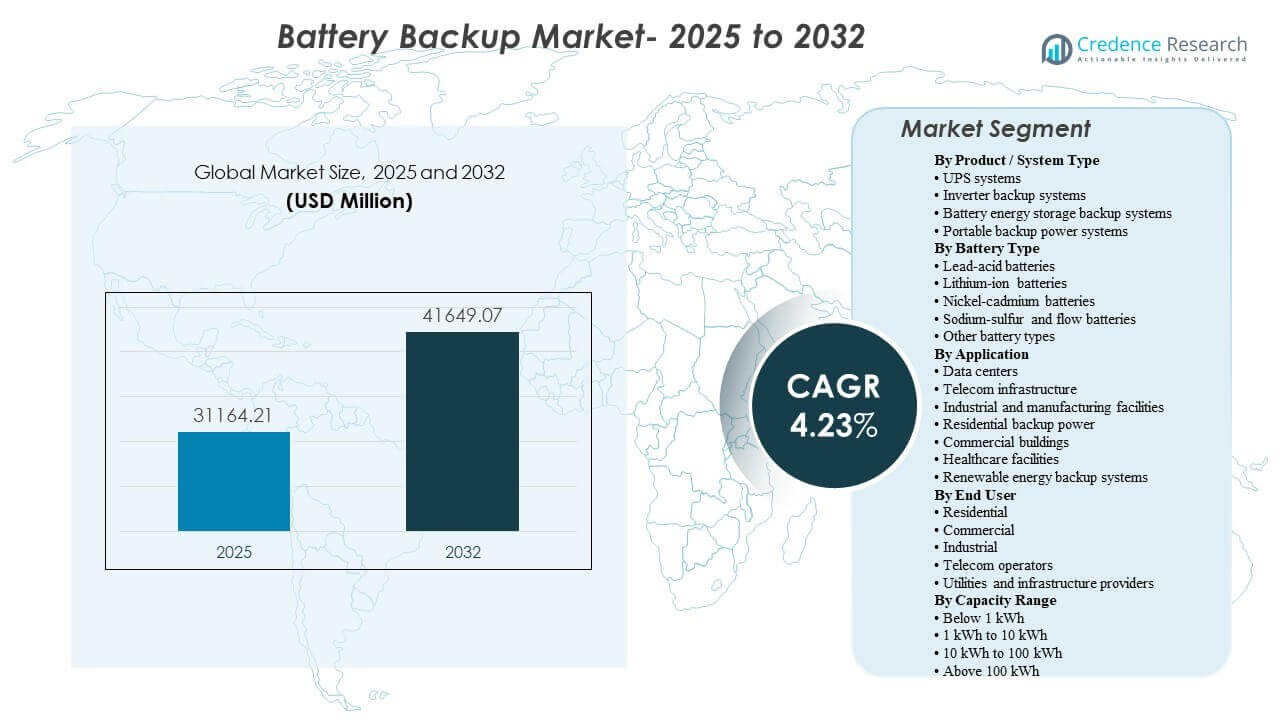

The global Battery Backup Market size was estimated at USD 31,164.21 million in 2025 and is expected to reach USD 41,649.07 million by 2032, growing at a CAGR of 4.23% from 2025 to 2032. Demand is primarily supported by rising uptime requirements across digital infrastructure and critical facilities, where power-quality protection and short-to-medium duration resilience remain operational priorities. Growth momentum is additionally supported by expanding deployments across Asia Pacific and steady replacement cycles in mature commercial and industrial installations.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Battery Backup Market Size 2025 |

USD 31,164.21 million |

| Battery Backup Market, CAGR |

4.23% |

| Battery Backup Market Size 2032 |

USD 41,649.07 million |

Key Market Trends & Insights

- The Battery Backup Market is projected to expand from USD 31,164.21 million in 2025 to USD 41,649.07 million by 2032, reflecting a 4.23% CAGR over 2025–2032.

- Asia Pacific accounted for 34% share in 2025, reflecting the region’s scale in infrastructure expansion and backup adoption across industrial and residential settings.

- North America represented 29% share in 2025, supported by high penetration of backup solutions in commercial facilities and mission-critical environments.

- Data centers represented 35% share (2023) within UPS battery backup power demand, reflecting the continued dominance of critical-load applications in backup investments.

- Lithium-ion accounted for 87.6% share (2025) in portable power station demand, indicating accelerating preference for higher energy density and lifecycle characteristics in compact backup formats.

Segment Analysis

Battery backup demand is shaped by a mix of mission-critical uptime needs and distributed resilience requirements. Data centers and telecom sites continue to prioritize low-transfer-time backup, stable power conditioning, and monitoring integration, supporting adoption of modern UPS platforms and higher-performance battery configurations. In parallel, residential and small commercial demand remains anchored in practical runtimes, ease of installation, and cost-performance tradeoffs, which sustains inverter-based and compact storage-backed solutions in many markets.

Across battery chemistries, lithium-ion adoption strengthens in use cases where lifecycle value, footprint reduction, and faster response are prioritized, especially in higher-value commercial and infrastructure environments. Lead-acid continues to maintain relevance in established UPS ecosystems where familiarity, serviceability, and replacement networks remain strong. Longer-duration technologies such as flow systems remain more aligned to stationary storage-backed backup requirements rather than compact continuity applications.

By Product / System Type Insights

UPS systems remain central to the market due to their role in providing seamless continuity and power conditioning for sensitive loads, and they accounted for the largest share at 41% in 2025. Data center and telecom applications favor architectures that support scalability, redundancy, and remote monitoring to reduce operational risk. Inverter backup systems retain relevance for residential and small commercial users where cost sensitivity and straightforward deployment guide purchasing. Battery energy storage backup systems gain traction where resilience is paired with energy management goals, particularly in facilities that value flexibility beyond short ride-through.

By Battery Type Insights

Lithium-ion batteries continue to expand their role in backup deployments where lifecycle economics and footprint constraints influence procurement decisions, and they held the largest share at 50% in 2025. The preference is reinforced in applications that require frequent cycling, compact form factors, or simplified maintenance practices. Lead-acid batteries remain widely deployed in conventional UPS environments due to established supply chains and service familiarity. Nickel-cadmium batteries persist in selected industrial contexts where robustness under harsh operating conditions matters, while sodium-sulfur and flow batteries are more often aligned with stationary, longer-duration backup needs.

By Application Insights

Data centers are a core application segment because service continuity and downtime avoidance are tightly linked to business risk and compliance expectations. Telecom infrastructure relies on backup to maintain network availability across distributed sites and edge deployments, driving demand for robust solutions and remote monitoring. Industrial and manufacturing facilities deploy backup to protect automation systems and reduce disruption from power events that can affect yield and safety. Residential backup power adoption is shaped by outage preparedness and the growing linkage between home energy storage and distributed generation. Healthcare facilities prioritize continuity for essential systems and critical equipment, supporting stable demand for reliable backup configurations.

By End User Insights

Residential buyers typically prioritize right-sized capacity, ease of use, and reliable operation during outages, supporting steady uptake of inverter and compact storage solutions. Commercial users focus on protecting IT loads, security systems, and building services where short disruptions can create operational and reputational costs. Industrial end users emphasize durability, serviceability, and integration with site electrical infrastructure to ensure predictable performance under variable conditions. Telecom operators require resilient backup across many locations and often value standardized platforms that simplify fleet management. Utilities and infrastructure providers increasingly consider storage-backed backup configurations where resilience planning intersects with grid-support and continuity requirements.

By Capacity Range Insights

Below 1 kWh solutions are commonly adopted for targeted loads such as networking equipment, lighting, and essential electronics where portability and affordability drive selection. The 1 kWh to 10 kWh range remains a primary band for residential backup needs because it aligns with typical household critical-load coverage and practical system sizing. The 10 kWh to 100 kWh range supports expanded resilience for small commercial facilities and larger homes, especially where backup is paired with distributed generation. Above 100 kWh systems are typically aligned with commercial, industrial, and infrastructure settings that require higher runtime capacity and system-level integration.

Battery Backup Market Drivers

Rising critical-load uptime requirements across digital infrastructure

The expansion of digital services increases the operational cost of downtime, reinforcing investment in backup power continuity. Data centers require stable power quality and immediate ride-through capability to protect IT loads. Telecom networks depend on distributed backup to maintain service availability during power interruptions. Monitoring and manageability features further strengthen replacement demand as operators seek predictable performance and remote diagnostics.

Increasing adoption of distributed backup in residential and small commercial settings

Outage preparedness continues to influence household and small business decisions regarding backup power solutions. Residential buyers often seek practical runtimes for essential appliances and connectivity loads. Inverter-based and compact storage-backed systems provide accessible pathways for backup adoption in many markets. Growth is also supported by improving product usability and safer, more integrated deployment options.

Transition toward higher-performance battery configurations and lower total cost of ownership

Battery choice increasingly affects lifecycle cost, footprint, and maintenance requirements in backup deployments. Lithium-ion adoption grows in applications where longer service life and reduced maintenance align with operational priorities. Space-constrained installations also favor solutions that deliver higher energy density and simplified cabinet layouts. This transition supports both new deployments and retrofit upgrades within installed UPS and backup ecosystems.

- For instance, Eaton states that its 9PX lithium-ion UPS delivers 8 to 10 years of life expectancy, recharges to up to 90% in 3 hours, provides 2 to 3 times longer battery life than lead-acid alternatives, and can deliver up to double the runtime at typical loads compared with equivalent VRLA models.

Industrial continuity and process protection requirements

Manufacturing and industrial facilities face operational risk from power disturbances that can impact automation, quality, and safety systems. Backup investments are used to protect sensitive controls, reduce downtime-related losses, and maintain safe operations. Industrial users also value robust designs that withstand site conditions and support serviceability. The breadth of industrial applications supports diverse system sizing and chemistry selection across the market.

- For instance, ABB’s PCS100 UPS-I is positioned for industrial protection in ratings from 150 kVA to 3000 kVA, and ABB reports installed systems totaling hundreds of MVA at manufacturers including Samsung and other LCD plants, while ABB’s UPS portfolio also specifies up to 96% overall efficiency and overload capability of 150% for 1 minute in critical power applications.

Battery Backup Market Challenges

Battery backup deployments face cost and configuration complexity challenges that vary by use case and system size. Upfront investment, installation requirements, and the need for compatible electrical infrastructure can slow decision-making in price-sensitive segments. Maintenance and lifecycle management requirements also differ by chemistry and operating environment, which can increase ownership complexity for buyers without dedicated technical support.

- For instance, Tesla states that each Megapack is delivered fully assembled with up to 3 MWh of storage and 1.5 MW of inverter capacity, and the company says a 250 MW / 1 GWh plant can be deployed in less than three months on a three-acre footprint, which highlights how product-level engineering can directly reduce installation complexity and deployment time at utility scale.

Supply chain variability and performance standardization remain additional barriers in some regions. Battery availability, component lead times, and compliance considerations can influence project timelines and equipment choices. Buyers may also face tradeoffs among runtime, footprint, and serviceability, especially in constrained installations. These constraints increase the importance of vendor service coverage, diagnostics, and robust warranty structures.

Battery Backup Market Trends and Opportunities

The market continues to shift toward smarter, more connected backup systems with greater monitoring and control functionality. Remote diagnostics, predictive maintenance, and software integration improve operational visibility for commercial and infrastructure buyers. Modular designs and scalable architectures also support faster deployment and staged expansion for evolving critical-load needs.

- For instance, Vertiv’s Liebert EXL S1 UPS integrates Vertiv LIFE Services for remote diagnostic and preventive monitoring, supports parallel operation of up to 8 units, covers a 625–1200 kVA/kW range, and reaches up to 99% efficiency in Dynamic Online mode, which demonstrates how suppliers are combining digital oversight with scalable high-capacity backup platforms.

Another opportunity is the growth of storage-backed backup configurations that combine resilience with energy management capabilities. Systems that support flexible sizing and integration with distributed generation can address both continuity and optimization goals. This creates expansion potential in commercial buildings, industrial facilities, and selective residential applications. Product differentiation increasingly centers on lifecycle value, footprint efficiency, and integrated service ecosystems.

Regional Insights

North America

North America held 29% share in 2025, supported by strong demand from commercial facilities and mission-critical environments that prioritize uptime and power quality. Data center growth and edge expansion support continued investment in UPS systems and scalable backup configurations. Replacement demand is reinforced by lifecycle upgrades and monitoring-driven operations practices. Buyer emphasis often centers on reliability, service coverage, and compliance-aligned deployment.

Europe

Europe accounted for 22% share in 2025, driven by modernization of facility power infrastructure and continuity requirements across commercial and industrial operations. Backup demand is supported by replacement cycles and the need for predictable performance in critical environments. Energy management priorities also influence interest in storage-backed backup in selected applications. Purchasing decisions typically emphasize reliability, safety, and integration into building and IT operations.

Asia Pacific

Asia Pacific led the market with 34% share in 2025, supported by large-scale infrastructure expansion and broad adoption across industrial, telecom, and residential segments. Rapid digitalization contributes to higher backup penetration in IT, edge, and network deployments. Demand is also influenced by diversified requirements ranging from compact residential backup to higher-capacity commercial and industrial systems. Scale and variety across end users encourage a wide mix of system types and battery chemistries.

Latin America

Latin America represented 8% share in 2025, supported by backup needs in commercial facilities and telecom infrastructure where continuity is critical. Adoption is influenced by power-quality concerns and the need to protect essential loads across distributed sites. Growth opportunities emerge in commercial buildings and critical services where downtime risk is increasingly recognized. The market often values cost-effective solutions with strong serviceability and availability.

Middle East & Africa

Middle East & Africa accounted for 7% share in 2025, supported by critical infrastructure projects, expanding telecom requirements, and selective growth in data center capacity. Backup demand is reinforced by continuity needs in healthcare and essential services. Deployment patterns vary significantly by country, shaped by infrastructure investment cycles and procurement practices. Vendors with strong project execution and service coverage are typically better positioned in complex installations.

Competitive Landscape

Competition is shaped by product reliability, total cost of ownership, monitoring ecosystems, and the breadth of service and channel coverage. Suppliers differentiate through scalable UPS architectures, integrated battery cabinets, and software platforms that improve visibility and maintenance planning. Portfolio breadth across residential, commercial, industrial, and infrastructure applications strengthens positioning by enabling consistent vendor selection across multiple use cases. Partnerships and product line refresh cycles are used to address changing battery preferences and evolving buyer requirements.

Schneider Electric continues to compete through a broad portfolio that spans UPS systems and backup power solutions across residential, commercial, and critical-load environments. The company’s positioning benefits from integrated power management capabilities and a strong ecosystem for monitoring and lifecycle support. Product continuity across multiple power classes supports standardized deployment strategies for enterprise and infrastructure buyers. Service reach and established channel presence further support adoption and replacement demand.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Schneider Electric

- APC by Schneider Electric

- Eaton Corporation

- ABB Ltd.

- Emerson Electric Co.

- CyberPower Systems

- Tripp Lite

- Delta Greentech

- Tesla, Inc.

- LiftMaster

- Vertiv Group Corp.

- Mitsubishi Electric Corporation

- Toshiba Corporation

- Huawei Technologies Co., Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Recent Developments

- In May 2025, ABB expanded its UPS portfolio with new PowerValue models for enterprise data centers, including lithium-battery-based systems aimed at power protection and backup reliability. ABB highlighted longer runtime, lower maintenance, cost-effectiveness, and battery management system integration as key features of the new launch.

- In July 2025, Honeywell announced the acquisition of Nexceris’ Li-ion Tamer business to strengthen its battery fire detection and life-safety portfolio for lithium-ion battery applications. Honeywell said Li-ion Tamer’s off-gas detection technology helps identify thermal runaway risks early, making the acquisition relevant to battery backup, energy storage, and data center safety solutions.

- In November 2025, Trina Storage signed an MoU with Pacific Green Energy Group to deliver up to 5 GWh of battery energy storage systems between 2026 and 2028. The partnership is intended to support large-scale storage deployments that improve grid reliability and expand advanced battery-backed power infrastructure in Australia and other international markets.

- In December 2025, Farmers Electric Cooperative and Base Power launched the first residential battery program in Farmers’ Northeast Texas service area, offering members an affordable whole-home backup solution. Under the partnership, Base Power said it will deploy 20 MW of dispatchable capacity through networked residential battery systems, while Farmers uses the systems for peak shaving and energy arbitrage without affecting member bills.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 31,164.21 million |

| Revenue forecast in 2032 |

USD 41,649.07 million |

| Growth rate (CAGR) |

4.23% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product / System Type, By Battery Type, By Application, By End User, By Capacity Range |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Schneider Electric; APC by Schneider Electric; Eaton Corporation; ABB Ltd.; Emerson Electric Co.; CyberPower Systems; Tripp Lite; Delta Greentech; Tesla, Inc.; LiftMaster; Vertiv Group Corp.; Mitsubishi Electric Corporation; Toshiba Corporation; Huawei Technologies Co., Ltd. |

| No. of Pages |

324 |

Segmentation

By Product / System Type

- UPS systems

- Inverter backup systems

- Battery energy storage backup systems

- Portable backup power systems

By Battery Type

- Lead-acid batteries

- Lithium-ion batteries

- Nickel-cadmium batteries

- Sodium-sulfur and flow batteries

- Other battery types

By Application

- Data centers

- Telecom infrastructure

- Industrial and manufacturing facilities

- Residential backup power

Commercial buildings

- Healthcare facilities

- Renewable energy backup systems

By End User

- Residential

- Commercial

- Industrial

- Telecom operators

- Utilities and infrastructure providers

By Capacity Range

- Below 1 kWh

- 1 kWh to 10 kWh

- 10 kWh to 100 kWh

- Above 100 kWh

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa