Market Overview:

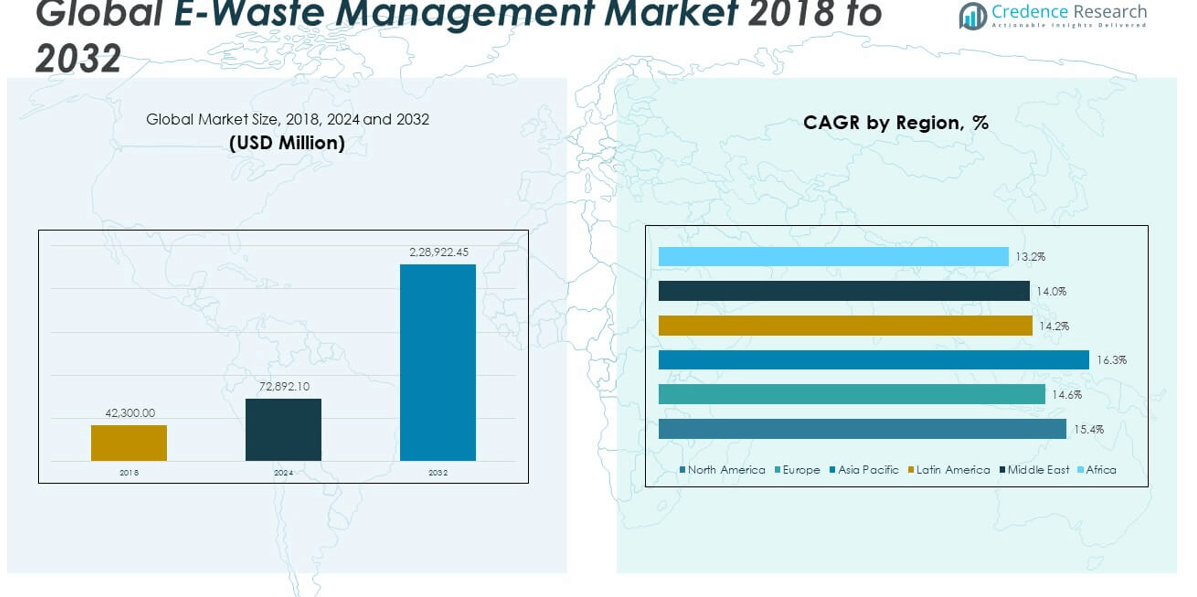

The Global E-Waste Management Market size was valued at USD 42,300.00 million in 2018 to USD 72,892.10 million in 2024 and is anticipated to reach USD 2,28,922.45 million by 2032, at a CAGR of 15.44% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| E-Waste Management Market Size 2024 |

USD 72,892.10 million |

| E-Waste Management Market, CAGR |

15.44% |

| E-Waste Management Market Size 2032 |

USD 2,28,922.45 million |

Multiple factors are driving this market forward. The widespread adoption of digital technology, increased affordability of consumer electronics, and growing disposable income levels have all contributed to a sharp rise in electronic product consumption. This has directly led to increased waste generation. At the same time, regulatory frameworks across many regions are becoming more stringent. Governments are enforcing producer responsibility laws, banning informal recycling, and mandating recycling targets to protect public health and the environment. These policy measures are creating a favorable ecosystem for formal recycling companies and service providers. In addition, the economic potential of recovering valuable materials such as gold, copper, and rare earth elements from e-waste has drawn significant investment. Technological advancements, including automation, AI-enabled sorting, and efficient material recovery methods, are making recycling operations more viable and scalable. Increased consumer awareness, environmental campaigns, and sustainability initiatives from corporations are also contributing to improved collection and disposal practices globally.

Regionally, the market is led by countries with mature recycling infrastructure and strong policy enforcement. Europe is a frontrunner, supported by well-established regulations, high public awareness, and robust collection systems. Its leadership position is reinforced by strict environmental directives and a strong push toward a circular economy. North America follows, with a stable market driven by regulatory support, corporate sustainability programs, and technological innovation. In contrast, Asia Pacific is the fastest-growing region, fueled by rapid urbanization, increasing consumption of electronics, and growing efforts to formalize recycling practices. Countries in this region are witnessing a transition from informal to formal waste management systems, supported by government initiatives and rising environmental consciousness. Latin America, the Middle East, and Africa currently represent smaller market segments, but growing infrastructure development and regulatory reforms are gradually unlocking their potential. Each region contributes uniquely to the global market, collectively shaping a dynamic and rapidly evolving landscape for e-waste management.

Market Insights:

- The Global E-Waste Management Market was valued at USD 42,300.00 million in 2018, reached USD 72,892.10 million in 2024, and is projected to grow to USD 2,28,922.45 million by 2032, registering a CAGR of 15.44% during the forecast period.

- The widespread use of digital devices and declining hardware costs have led to a sharp rise in electronic consumption, directly increasing e-waste volumes across all regions.

- Regulatory frameworks—such as Extended Producer Responsibility (EPR) and e-waste import bans—are helping formalize recycling operations and protect environmental and public health systems globally.

- The recovery of high-value materials like gold, copper, palladium, and rare earth elements is creating a multi-billion-dollar opportunity, making recycling economically viable and scalable.

- Technological advancements—including AI-enabled sorting, robotic dismantling, and digital tracking systems—are improving recovery rates and enhancing safety across formal e-waste processing facilities.

- A large share of global e-waste is still handled by unregistered informal sector operators, who often use hazardous methods that expose workers and ecosystems to lead, mercury, and cadmium.

- Regionally, Europe leads the market due to strong regulations and infrastructure, North America remains stable with corporate and government support, and Asia Pacific is the fastest-growing region due to rapid urbanization and policy reforms.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Surge in Electronic Device Consumption Across Households and Businesses Is Intensifying E-Waste Volumes:

The rapid adoption of consumer electronics is a primary force behind the expansion of the Global E-Waste Management Market. Shortened product life cycles, frequent upgrades, and declining hardware prices are accelerating the disposal of smartphones, laptops, TVs, and appliances. The growing integration of electronics into everyday life—from smart homes to connected healthcare and education—continues to inflate global e-waste volumes. Businesses are also contributing to the trend through frequent hardware refresh cycles and digitization of operations. The increase in e-waste is outpacing the capacity of existing waste systems, prompting demand for scalable, structured disposal and recycling solutions. It is creating mounting pressure on governments, manufacturers, and waste management providers to invest in robust e-waste infrastructure. The market is evolving to address this rising urgency through formal collection, processing, and recovery frameworks.

- For instance, Apple reported generating 52,490 tonnes of total waste in 2021. The company’s landfill diversion rate reached 68% in 2021, reflecting a significant commitment to structured e-waste management.

Regulatory Mandates and International Policies Are Accelerating Formal Waste Handling Practices:

Stringent regulatory frameworks are playing a critical role in shaping the Global E-Waste Management Market. Many governments are enforcing Extended Producer Responsibility (EPR) regulations that make manufacturers accountable for the entire lifecycle of their products, including take-back, recycling, and safe disposal. This shift is prompting companies to integrate recycling into product design and establish collection networks. Environmental protection agencies are imposing compliance standards on handling hazardous substances like lead, mercury, and cadmium, which are prevalent in discarded electronics. It is compelling market players to upgrade processes and invest in certified facilities. Policy instruments such as import restrictions on e-waste, landfill bans, and e-waste trading controls are further supporting the growth of formal recycling systems. These legal requirements are reshaping global supply chains and encouraging partnerships between OEMs, recyclers, and government bodies.

- For instance, Samsung has collected and recycled an average of 100 million pounds of e-waste per year in the United States since 2008, achieving recognition with the EPA SMM Gold Tier Award for eight consecutive years.

Economic Recovery Potential of Precious and Rare Materials Is Boosting Recycling Investments:

The high material value embedded in electronic waste is another key driver of the Global E-Waste Management Market. E-waste contains valuable metals such as gold, copper, palladium, and rare earth elements, which can be recovered and reused in manufacturing. With rising raw material prices and growing interest in resource efficiency, the economic incentive to recycle has significantly increased. Companies are investing in advanced recovery technologies to maximize output from discarded electronics. It is also helping reduce reliance on mining and lowering the environmental impact of raw material extraction. The financial attractiveness of recovering critical materials is prompting greater participation from private-sector stakeholders. This trend supports both environmental and economic objectives, making recycling a strategic business priority.

Technological Advancements Are Enhancing Efficiency, Safety, and Material Recovery Rates:

Innovation in processing and automation technologies is transforming how the Global E-Waste Management Market operates. Robotics, AI-based sorting systems, and sensor-based separation are improving accuracy and reducing labor dependency. These advancements are enhancing material recovery rates and minimizing human exposure to toxic components during dismantling. Digital platforms for tracking and auditing e-waste movements are strengthening regulatory compliance and transparency. It is also enabling better planning and coordination between collection centers and recycling facilities. Smart logistics and predictive analytics are helping streamline operations and reduce handling costs. The integration of technology is making e-waste management more scalable and responsive to rising demand.

Market Trends:

Growth of Refurbishment and Reuse Models Is Reshaping Electronic Product Life Cycles:

Refurbishment and resale of electronics are gaining traction as a parallel trend within the Global E-Waste Management Market. Consumers and organizations are turning toward certified refurbished products due to cost efficiency and environmental concerns. Brands and third-party vendors are expanding refurbishment channels to monetize returned or obsolete devices. This shift is reducing direct volumes of e-waste and extending product life cycles. It is also fostering secondary markets, especially in price-sensitive regions where access to new devices is limited. The rising preference for sustainable consumption is expected to support long-term development of reuse-focused systems across formal waste networks.

- For instance, Dell’s Tech Refresh & Recycle Program manages over 3 million assets annually, with 30% of returned gear going toward manufacturing refurbishment. In 2018, Apple refurbished more than 7.8 million devices, diverting over 48,000 metric tons of electronic waste from landfills.

Blockchain and Digital Tracking Tools Are Enabling Transparency and Chain of Custody:

Transparency in collection and disposal is becoming a critical requirement across the Global E-Waste Management Market. Stakeholders are adopting blockchain and digital tracking platforms to monitor e-waste from origin to final processing. These technologies offer immutable records that help enforce compliance, prevent illegal dumping, and verify responsible recycling. It is allowing regulators and producers to track performance against environmental targets. Digital tools also support efficient logistics and enhance coordination across facilities. The growing demand for traceability is positioning data-driven systems as an essential component of modern e-waste operations.

- For instance, blockchain-based IoT-enabled tracking systems have been implemented to monitor post-production business processes and operations on electronic devices. These systems use smart contracts to record actions on an immutable distributed ledger, ensuring transparency and traceability throughout the supply chain.

Reverse Logistics Networks Are Expanding Across Retail and Consumer Channels:

Retailers and electronics manufacturers are investing in reverse logistics infrastructure to support take-back initiatives. The Global E-Waste Management Market is seeing rapid development of return hubs, collection kiosks, and doorstep pickup models. These systems simplify consumer participation and improve e-waste collection efficiency. It is helping companies meet regulatory targets and align with sustainability goals. The integration of reverse logistics into product distribution networks is lowering operational costs and increasing recovery volumes. Stronger engagement between brands and consumers is enhancing circular economy outcomes.

Rise in Urban Mining and Closed-Loop Manufacturing Is Redefining Resource Strategies:

Urban mining is emerging as a key trend as manufacturers seek local, sustainable sources of critical raw materials. The Global E-Waste Management Market is responding with closed-loop manufacturing systems that reuse materials recovered from obsolete electronics. This approach supports supply chain resilience and reduces reliance on traditional mining. Companies are integrating recycled metals into new product lines without compromising quality. It is also attracting investment from industries sensitive to raw material shortages. This trend is expected to expand as regulatory and financial pressures drive demand for circular solutions.

Market Challenges Analysis:

Informal Sector Dominance and Unsafe Recycling Practices Continue to Undermine Formal Progress:

The dominance of the informal sector remains one of the most persistent challenges in the Global E-Waste Management Market. A significant share of e-waste is processed by unregistered entities using unsafe and environmentally harmful methods. Informal recycling exposes workers to toxic materials and contributes to soil and water contamination. It undermines the viability of formal systems by diverting high-value waste streams. Enforcement of regulations in developing economies remains inconsistent and poorly resourced. It limits the expansion of certified facilities and erodes trust in responsible disposal practices. This structural issue continues to create fragmentation and inefficiencies across the value chain.

High Cost of Advanced Recovery Technologies Is Limiting Access for Small Operators:

The implementation of automated dismantling, AI-based sorting, and high-efficiency recovery systems requires significant capital investment. Smaller recycling firms in the Global E-Waste Management Market struggle to adopt these technologies due to financial and operational constraints. Limited access to funding restricts their ability to scale operations or meet stringent compliance standards. It widens the gap between large, tech-enabled recyclers and low-resource players. Variability in material composition and lack of standardization also increase technical complexity. The high cost of innovation is slowing widespread technology adoption and reducing market competitiveness.

Market Opportunities:

Expansion of Producer-Led Collection Programs Is Opening New Growth Channels:

The Global E-Waste Management Market can benefit significantly from expanded producer responsibility programs. Manufacturers adopting in-house or partnered collection and recycling models can control material flows and recover more value. It creates new service models that support compliance while generating revenue from recovered assets.

Emerging Markets Offer Untapped Potential for Infrastructure and Investment:

Rising electronics adoption in Africa, Latin America, and parts of Asia is creating demand for formal waste management infrastructure. The Global E-Waste Management Market has opportunities to scale through public-private partnerships, localized processing hubs, and training initiatives that formalize operations in these underserved regions.

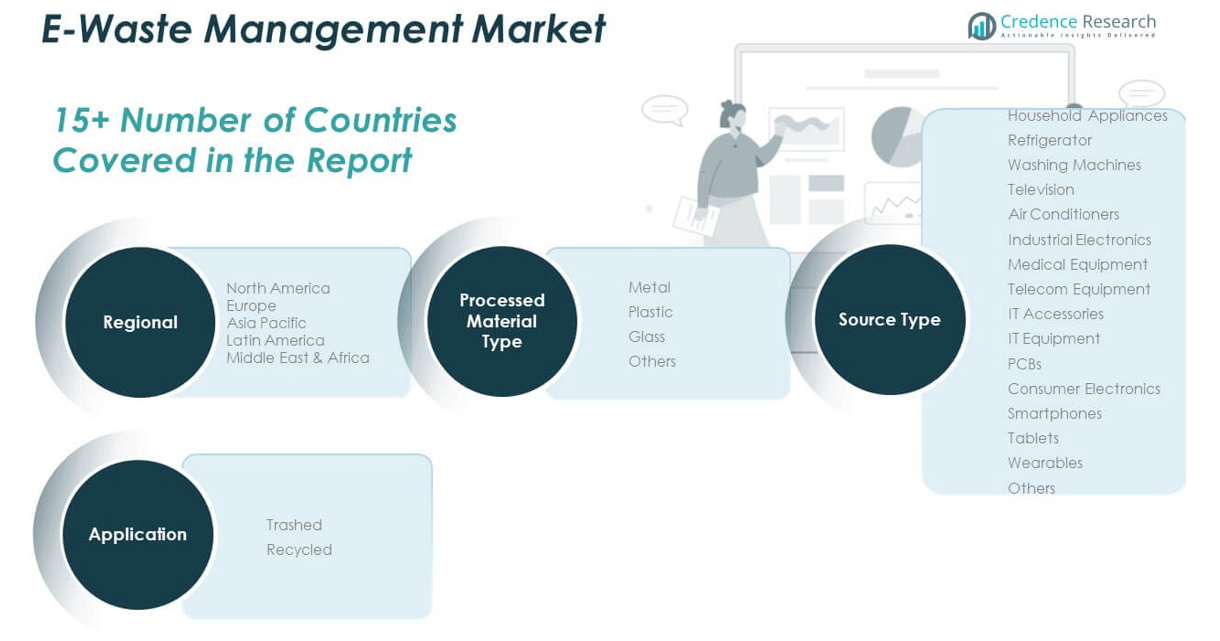

Market Segmentation Analysis:

By Processed Material Type

The Global E-Waste Management Market segments processed material into metal, plastic, glass, and others. Metals dominate the category due to their high recovery value and critical use in circuitry and connectors. Plastic follows, driven by large-scale disposal of casings, housings, and internal non-metal parts. Glass is primarily sourced from CRTs, LCDs, and other display units. The “others” category includes mixed materials such as ceramics, composite laminates, and rubber components that require specialized sorting.

- For instance, hydrometallurgical processes used in metal recovery from e-waste can achieve up to 95% recovery efficiency for metals, while biometallurgical approaches can reduce environmental impact by 30–50% compared to conventional methods.

By Application

By application, the market is divided into trashed and recycled segments. Recycled e-waste represents a growing share, supported by government mandates and corporate recycling initiatives. Companies and municipalities are investing in formal systems to maximize material recovery and minimize environmental impact. The trashed segment remains sizable, particularly in developing regions with limited infrastructure or enforcement. It reflects ongoing challenges in transitioning from informal to formal waste streams.

- For instance, ERI, one of North America’s largest e-waste recyclers, operates facilities capable of processing over 300 million pounds of electronic waste each year, highlighting the scale of infrastructure investments in the recycled segment.

By Source Type

Source type includes household appliances, industrial electronics, and consumer electronics. Household appliances contribute significantly, with refrigerators, washing machines, televisions, and air conditioners making up large e-waste volumes. Industrial electronics include medical equipment, telecom systems, IT accessories, IT equipment, and PCBs—items that often require technical dismantling and yield high-value materials. Consumer electronics such as smartphones, tablets, and wearables are increasing in volume due to short replacement cycles. Others include miscellaneous devices contributing to growing collection demand. The Global E-Waste Management Market is adapting its infrastructure to efficiently manage these diverse input streams.

Segmentation:

By Processed Material Type

- Metal

- Plastic

- Glass

- Others

By Application

By Source Type

- Household Appliances

- Refrigerator

- Washing Machines

- Television

- Air Conditioners

- Industrial Electronics

- Medical Equipment

- Telecom Equipment

- IT Accessories

- IT Equipment

- PCBs

- Consumer Electronics

- Smartphones

- Tablets

- Wearables

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America

The North America E-Waste Management Market size was valued at USD 8,650.35 million in 2018 to USD 14,585.27 million in 2024 and is anticipated to reach USD 45,693.33 million by 2032, at a CAGR of 15.4% during the forecast period. North America holds a significant share of the Global E-Waste Management Market, supported by mature infrastructure and strong policy enforcement. The United States and Canada lead through active implementation of Extended Producer Responsibility (EPR) and public-private recycling initiatives. It benefits from high consumer electronics turnover, driving continuous demand for efficient waste processing. Leading recyclers and automated facilities improve material recovery and reduce environmental risk. Regulatory agencies continue to promote digital tracking and certified disposal. The region’s structured approach reinforces growth in both capacity and compliance.

Europe

The Europe E-Waste Management Market size was valued at USD 11,209.50 million in 2018 to USD 18,570.91 million in 2024 and is anticipated to reach USD 55,113.69 million by 2032, at a CAGR of 14.6% during the forecast period. Europe leads the Global E-Waste Management Market by market share, driven by its advanced legal frameworks and strong push for a circular economy. It is supported by mandatory WEEE compliance, standardized take-back systems, and high public awareness. Countries like Germany, the UK, and France deploy efficient logistics and recovery infrastructure. Producers actively participate in take-back and recycling through formal channels. Europe promotes sustainable manufacturing by reintegrating recovered materials into supply chains. Its consistent policy execution ensures long-term market stability and innovation.

Asia Pacific

The Asia Pacific E-Waste Management Market size was valued at USD 17,440.29 million in 2018 to USD 30,843.99 million in 2024 and is anticipated to reach USD 102,923.72 million by 2032, at a CAGR of 16.3% during the forecast period. Asia Pacific holds the largest share of the Global E-Waste Management Market and is expanding at the fastest pace. It is fueled by rising electronic consumption, rapid urbanization, and improving government regulation. Countries such as China, India, and Japan are scaling formal recycling networks to reduce environmental harm. Informal sector activity remains high, prompting new legislation and capacity building. Foreign investments and local partnerships are increasing across sorting and dismantling segments. The region continues to transition from unregulated disposal toward structured, scalable waste management systems.

Latin America

The Latin America E-Waste Management Market size was valued at USD 2,216.52 million in 2018 to USD 3,775.08 million in 2024 and is anticipated to reach USD 10,821.16 million by 2032, at a CAGR of 14.2% during the forecast period. Latin America’s share of the Global E-Waste Management Market is growing steadily, with Brazil and Mexico at the forefront. It is benefiting from national recycling policies and pilot programs that encourage formal handling. Urban population growth and rising electronic penetration are creating more consistent waste streams. Enforcement and collection networks vary by country, but the trend favors increased regulation and private-sector participation. Informal recyclers continue to dominate in some areas, highlighting the need for education and infrastructure. Opportunities exist to scale local systems through regional cooperation and technology investment.

Middle East

The Middle East E-Waste Management Market size was valued at USD 1,658.16 million in 2018 to USD 2,681.96 million in 2024 and is anticipated to reach USD 7,624.38 million by 2032, at a CAGR of 14.0% during the forecast period. The Middle East contributes a modest share to the Global E-Waste Management Market but is gaining ground through national sustainability efforts. Countries such as the UAE and Saudi Arabia are introducing e-waste policies aligned with broader environmental strategies. It is supported by investments in formal collection and material recovery facilities. Awareness levels remain low in parts of the region, slowing adoption of structured systems. Strategic collaborations and public campaigns are helping improve recycling rates. The region’s market outlook is supported by rising electronics usage and growing government involvement.

Africa

The Africa E-Waste Management Market size was valued at USD 1,125.18 million in 2018 to USD 2,434.89 million in 2024 and is anticipated to reach USD 6,746.17 million by 2032, at a CAGR of 13.2% during the forecast period. Africa represents an emerging region in the Global E-Waste Management Market with significant growth potential. It faces major challenges from informal recycling, limited funding, and inadequate enforcement. Countries such as Nigeria, South Africa, and Egypt are making progress through national policy development and pilot programs. It is attracting support from international organizations to build safer, formal infrastructure. Consumer awareness remains a constraint, but education and outreach efforts are increasing. Africa’s long-term potential depends on scalable solutions, workforce training, and stronger regulatory support.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Aurubis AG

- Boliden Group

- Desco Electronic Recyclers

- EcoCentric

- ENVIRO-HUB HOLDINGS LTD.

- ERI

- Greentec

- Kuusakoski

- MRI Technologies

- Namo eWaste Management Ltd.

- Sims Limited

- Stena Metall AB

- Tetronics Environmental Technology Company

- Umicore

- WM Intellectual Property Holdings, L.L.C.

Competitive Analysis:

The Global E-Waste Management Market is highly competitive, with key players focusing on strategic partnerships, capacity expansion, and advanced recovery technologies to strengthen their market positions. Leading companies such as Sims Limited, Aurubis AG, Umicore, Boliden Group, and ERI operate large-scale recycling facilities with integrated services for collection, dismantling, and material recovery. It is characterized by strong regional presence, with firms leveraging regulatory compliance and environmental certifications to secure contracts. Players are investing in AI-based sorting systems, robotics, and sustainable logistics to improve efficiency and profitability. Emerging firms in Asia and Latin America are entering the formal market through government-backed initiatives and joint ventures. Established players focus on securing long-term agreements with OEMs and municipal authorities to ensure consistent e-waste supply. The market continues to evolve with technological innovation and policy-driven consolidation, creating a dynamic environment where scale, compliance, and innovation determine competitive advantage.

Recent Developments:

- In June 2025, Kuusakoski expanded its operations by acquiring a battery recycling company, enhancing its portfolio in e-waste material recovery and broadening its service offerings.

Market Concentration & Characteristics:

The Global E-Waste Management Market exhibits moderate to high market concentration, with a mix of large multinational players and regional operators. It is dominated by a few key companies with extensive processing capabilities, technological infrastructure, and long-term contracts with governments and electronics manufacturers. The market features strong regulatory influence, high entry barriers due to capital requirements, and complex compliance demands. It is fragmented in developing regions, where informal recycling remains prevalent and formal infrastructure is still emerging. Technological innovation, vertical integration, and environmental certifications define competitive positioning. The market’s structure supports consolidation, with larger firms acquiring smaller recyclers to expand service networks and improve material recovery efficiency.

Report Coverage:

The research report offers an in-depth analysis based on processed material type, application, and source type. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global e-waste volumes will drive sustained demand for scalable recycling infrastructure.

- Regulatory tightening will increase formal sector participation and phase out informal processing.

- Investment in AI, robotics, and automation will improve sorting accuracy and recovery rates.

- Urban mining and circular economy initiatives will enhance material reuse and resource security.

- Emerging markets will offer expansion opportunities through public-private partnerships and policy reforms.

- OEMs will increasingly integrate take-back and recycling programs into product lifecycles.

- Growth in consumer electronics and shorter device lifespans will fuel collection volumes.

- Compliance-driven contracts will favor certified recyclers with advanced processing capabilities.

- Education and awareness campaigns will boost participation in structured disposal systems.

- Digital tracking platforms will improve transparency, traceability, and reporting across the value chain.