Market Overview

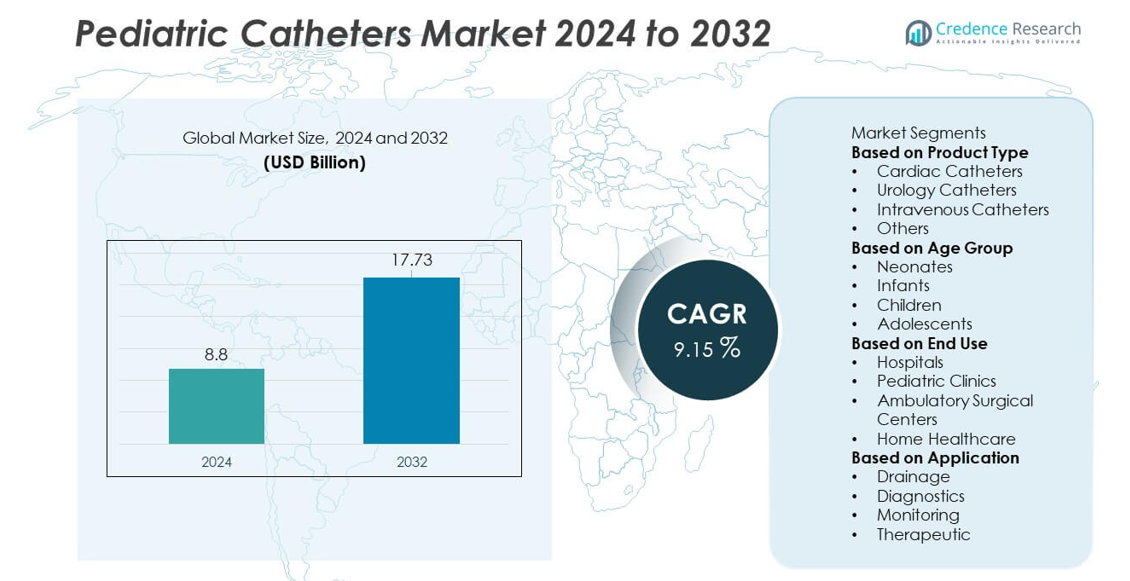

The Pediatric Catheters market reached USD 8.8 billion in 2024 and is projected to grow to USD 17.73 billion by 2032, registering a CAGR of 9.15% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Pediatric Catheters Market Size 2024 |

USD 8.8 billion |

| Pediatric Catheters Market, CAGR |

9.15% |

| Pediatric Catheters Market Size 2032 |

USD 17.73 billion |

The Pediatric Catheters market is shaped by major players such as Boston Scientific Corporation, Medtronic plc, B. Braun Melsungen AG, Cardinal Health, Inc., Teleflex Incorporated, Cook Medical, Smiths Medical, Terumo Corporation, AngioDynamics, Inc., and Fresenius Medical Care AG & Co. KGaA, all of which focus on advanced, biocompatible, and miniaturized catheter solutions designed for neonates and young children. These companies enhance product safety through antimicrobial coatings, flexible materials, and soft-tip designs that reduce procedure-related trauma. North America leads the market with a 37% share, supported by strong pediatric care infrastructure, followed by Europe with 29%, driven by advanced neonatal units, while Asia Pacific holds 24%, fueled by rising birth rates and expanding pediatric healthcare investments.

Market Insights

- The Pediatric Catheters market reached USD 8.8 billion in 2024 and will grow at a CAGR of 9.15% through 2032, driven by rising pediatric care needs and expanding neonatal treatments.

- Increasing preterm births and congenital disorders drive demand for advanced pediatric catheters, with intravenous catheters holding a 42% share due to widespread use in NICUs and emergency care.

- Trends such as miniaturized designs, biocompatible materials, and antimicrobial coatings influence product innovation, while minimally invasive pediatric procedures grow across both inpatient and outpatient settings.

- Leading companies such as Boston Scientific, Medtronic, B. Braun, and Teleflex strengthen competition through specialized catheter portfolios, though infection risks and limited skilled pediatric professionals remain key restraints.

- Regionally, North America leads with a 37% share, Europe follows with 29%, and Asia Pacific holds 24%, supported by expanding neonatal units, improving healthcare spending, and rising pediatric procedure volumes.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Segmentation Analysis:

By Product Type

Intravenous catheters lead the Pediatric Catheters market with a 42% share, driven by high demand in neonatal and pediatric intensive care for fluid administration, medication delivery, and nutritional support. Their wide use in emergency care and routine hospital procedures strengthens dominance across global healthcare systems. Cardiac catheters and urology catheters show steady growth due to rising congenital heart disorders and urinary tract abnormalities in infants. Advanced biocompatible materials and miniaturized catheter designs further support adoption. The “others” category expands with emerging neurovascular and gastrointestinal catheters tailored for minimally invasive pediatric procedures.

- For instance, B. Braun manufactures various micro-bore IV extension sets and lines using materials like polyurethane (PUR) or polyethylene (PE) to help provide precise fluid delivery, which can be beneficial in fields such as neonatal or pediatric care.

By Age Group

Neonates dominate the market with a 38% share, supported by increasing preterm birth rates and rising NICU admissions worldwide. These patients require frequent use of intravenous, umbilical, and specialty catheters for monitoring, diagnostics, and life-support procedures. Infants also generate strong demand due to growing pediatric surgical interventions and infection management. Children and adolescents represent expanding segments as chronic illnesses and congenital anomalies require long-term catheter-based therapies. Continuous improvement in safety features and infection-resistant materials strengthens adoption across all pediatric age groups.

- For instance, certain advanced neonatal monitoring systems leverage precision pressure sensors that, when used with appropriate vascular access devices, can detect clinically significant hemodynamic shifts and support continuous monitoring during high-acuity NICU procedures.

By End Use

Hospitals hold the largest share at 56%, driven by their high patient volume, advanced pediatric departments, and widespread use of catheters in NICUs, PICUs, and emergency wards. Hospitals rely on specialized catheter types for critical care, diagnostics, and minimally invasive interventions. Pediatric clinics show rising adoption as outpatient procedures and early-diagnosis programs increase globally. Ambulatory surgical centers gain traction with growing preference for day-care pediatric surgeries. Home healthcare expands steadily as long-term conditions and chronic care needs encourage the use of portable and user-friendly pediatric catheters.

Key Growth Drivers

Rising Prevalence of Congenital Disorders and Preterm Births

Growing cases of congenital heart defects, urinary tract abnormalities, and gastrointestinal complications increase the need for pediatric and neonatal catheterization. Rising global preterm birth rates further drive catheter demand across NICUs and PICUs. Hospitals rely on specialized, miniaturized catheters for safe fluid delivery, monitoring, and life-support procedures in fragile patients. Improved neonatal survival rates also expand long-term catheter usage. These clinical trends strengthen market growth as healthcare systems invest in advanced pediatric care infrastructure.

- For instance, Becton Dickinson (BD) produces a range of pediatric peripheral IV catheters. Proper securement and care of these catheters is crucial for reducing complications such as dislodgement and phlebitis, which are common issues in pediatric and neonatal units.

Advancements in Miniaturized and Biocompatible Catheter Technologies

Manufacturers introduce smaller, flexible, and biocompatible catheter designs to reduce trauma and improve safety for neonates and young children. Innovations include antimicrobial coatings, soft-tip materials, and improved kink resistance for better procedural outcomes. These enhancements support broader use across cardiac, urinary, neurovascular, and intravenous applications. Hospitals adopt advanced designs to lower infection risk and improve comfort during short- and long-term procedures. Continuous R&D investment accelerates adoption of next-generation pediatric catheter devices.

- For instance, Teleflex has engineered various central venous catheters, some of which feature a material blend or surface coating designed to improve material properties or reduce the risk of catheter-related bacterial adhesion.

Growing Demand for Minimally Invasive Pediatric Procedures

The shift toward minimally invasive diagnostics and treatments increases demand for specialized pediatric catheters. Surgeons and pediatric specialists use catheters for targeted drug delivery, interventional cardiology, and diagnostic imaging. Shorter recovery times, reduced trauma, and improved clinical outcomes encourage wider adoption. Rising availability of skilled pediatric specialists and better-equipped surgical centers further boosts usage. These trends support strong penetration of catheters across both inpatient and outpatient care settings.

Key Trends & Opportunities

Increasing Adoption of Home-Based Pediatric Care Solutions

Home healthcare expands as chronic illnesses, long-term nutrition support, and post-surgical recovery drive catheter use outside hospitals. Parents and caregivers adopt user-friendly, safe, and portable catheter systems supported by training and telehealth guidance. Manufacturers offer easy-to-use designs with infection-prevention features, supporting wider home-based adoption. This shift creates strong opportunities for innovative IV, enteral, and urinary catheters tailored for remote care.

- For instance, Cardinal Health produces home-care enteral feeding products, including feeding tubes and gravity sets, that incorporate the industry-standard ENFit® connection system.

Rising Investment in Pediatric Specialty Centers and NICUs

Governments and private healthcare providers increase investment in pediatric and neonatal intensive care facilities. These expansions boost demand for advanced catheters designed for fragile infants requiring continuous monitoring, fluid therapy, and interventions. New pediatric cardiac and urology units also raise the need for highly specialized catheters. Growth in pediatric medical infrastructure strengthens long-term market opportunities.

- For instance, polyurethane central venous catheters have a greater pressure tolerance than silicone catheters and are less likely to rupture under experimental conditions, enabling safe treatment during extended NICU stays.

Key Challenges

High Risk of Catheter-Associated Infections in Pediatric Patients

Infants and young children face higher vulnerability to catheter-associated bloodstream and urinary infections. Poor insertion techniques, prolonged catheterization, and limited infection-control resources in developing regions heighten risks. These complications increase healthcare costs and create barriers to widespread adoption. Manufacturers must invest heavily in antimicrobial coatings and improved safety features to address this challenge.

Limited Availability of Skilled Pediatric Professionals

Proper catheter insertion and management in neonates and children require specialized training. Many regions face shortages of pediatric clinicians and neonatal care experts, delaying adoption of advanced catheter techniques. Skill gaps increase procedural errors and raise safety concerns, restricting market expansion. Expanding training programs and improving care standards are essential to overcoming this barrier.

Regional Analysis

North America

North America leads the Pediatric Catheters market with a 37% share, supported by advanced pediatric healthcare infrastructure, strong NICU and PICU capacity, and high adoption of minimally invasive procedures. The region benefits from widespread availability of specialized pediatric surgeons and neonatal specialists who rely heavily on cardiac, intravenous, and urology catheters for critical care. Rising prevalence of congenital disorders and increased preterm birth rates strengthen clinical demand. Strong reimbursement frameworks, rapid adoption of biocompatible catheter materials, and continuous technological innovation by U.S.-based manufacturers further reinforce market leadership.

Europe

Europe holds a 29% share, driven by well-established pediatric hospitals and strong government focus on neonatal and child health programs. Countries such as Germany, France, and the UK invest heavily in NICU upgrades, increasing the use of advanced intravenous and cardiac catheters. Growing incidence of pediatric chronic illnesses supports higher procedure volumes across inpatient and outpatient settings. Strict safety regulations encourage the adoption of biocompatible and infection-resistant catheter materials. Expanding pediatric surgical capabilities and rising demand for minimally invasive interventions continue to strengthen Europe’s market position.

Asia Pacific

Asia Pacific accounts for a 24% share, propelled by rising birth rates, rapid improvement in pediatric care infrastructure, and increasing government investments in maternal and child health. China and India witness high catheter demand due to growing NICU admissions and expanding access to neonatal emergency care. Technological upgrades in pediatric cardiac and urology centers support wider adoption of specialized catheters. Increasing awareness of minimally invasive treatments and growing medical tourism also boost market presence. The region’s large population and improving healthcare spending create strong long-term growth prospects.

Latin America

Latin America holds a 6% share, supported by expanding pediatric hospital capacity and rising investment in neonatal care across Brazil, Mexico, and Argentina. Growing cases of congenital heart conditions and premature births increase the need for intravenous and cardiac catheters. Adoption of minimally invasive pediatric procedures grows in private hospitals and specialty clinics. However, limited access to advanced equipment in rural areas moderates growth. Improving healthcare reforms and rising training programs for pediatric specialists contribute to steady regional expansion.

Middle East & Africa

The Middle East & Africa region accounts for a 4% share, driven by increasing investment in pediatric and neonatal care, particularly in GCC countries. Hospitals across Saudi Arabia and the UAE adopt advanced catheter technologies to support high-quality NICU and PICU services. Growth in pediatric cardiac and urology centers strengthens demand for specialized catheters. In Africa, limited access to trained specialists and advanced neonatal equipment slows adoption, but international healthcare partnerships and public health initiatives are improving care standards. Expanding hospital infrastructure and rising awareness of pediatric treatment needs support gradual market growth.

Market Segmentations:

By Product Type

- Cardiac Catheters

- Urology Catheters

- Intravenous Catheters

- Others

By Age Group

- Neonates

- Infants

- Children

- Adolescents

By End Use

- Hospitals

- Pediatric Clinics

- Ambulatory Surgical Centers

- Home Healthcare

By Application

- Drainage

- Diagnostics

- Monitoring

- Therapeutic

By Geography

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Competitive Landscape

The competitive landscape features leading companies such as Boston Scientific Corporation, Medtronic plc, B. Braun Melsungen AG, Cardinal Health, Inc., Teleflex Incorporated, Cook Medical, Smiths Medical, Terumo Corporation, AngioDynamics, Inc., and Fresenius Medical Care AG & Co. KGaA, all of which strengthen the Pediatric Catheters market through continuous advancements in design, materials, and safety features. These players focus on developing miniaturized, biocompatible catheters tailored for neonates and infants, addressing the growing need for precision and reduced trauma in pediatric procedures. Investments in antimicrobial coatings, soft-tip technologies, and improved flexibility enhance product performance and reduce infection risks. Strategic collaborations with pediatric hospitals support product trials and clinical validation. Companies also expand manufacturing capabilities to meet rising demand across NICUs, PICUs, and outpatient pediatric centers. As minimally invasive procedures gain traction, competitive intensity increases around product innovation, regulatory compliance, and specialized catheter portfolios designed for diverse pediatric conditions.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

- Boston Scientific Corporation

- Medtronic plc

- Braun Melsungen AG

- Cardinal Health, Inc.

- Teleflex Incorporated

- Cook Medical

- Smiths Medical

- Terumo Corporation

- AngioDynamics, Inc.

- Fresenius Medical Care AG & Co. KGaA

Recent Developments

- In June 2025, Cook Medical recalled certain Beacon Tip Angiographic Catheters due to tip-separation issues — a Class I recall.

- In February 2025, Teleflex Incorporated announced plans to spin off its Urology, Acute Care, and OEM businesses into a new independent company.

Report Coverage

The research report offers an in-depth analysis based on Product Type, Age Group, End Use, Application and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- Demand for specialized neonatal and infant catheters will rise as preterm births increase.

- Miniaturized and flexible catheter designs will gain wider adoption in critical care.

- Antimicrobial and infection-resistant materials will become standard across most catheter types.

- Growth in minimally invasive pediatric procedures will expand the need for advanced catheters.

- Home healthcare adoption will increase, driving demand for user-friendly and safe catheter systems.

- Pediatric cardiac and urology interventions will accelerate demand for high-precision catheter solutions.

- Technological innovation will focus on reducing trauma and improving catheter placement accuracy.

- Emerging markets will see rapid expansion as pediatric care infrastructure improves.

- Manufacturers will enhance production capacity to meet rising NICU and PICU requirements.

- Collaboration between hospitals and device makers will strengthen product development and clinical validation.