Market Overview:

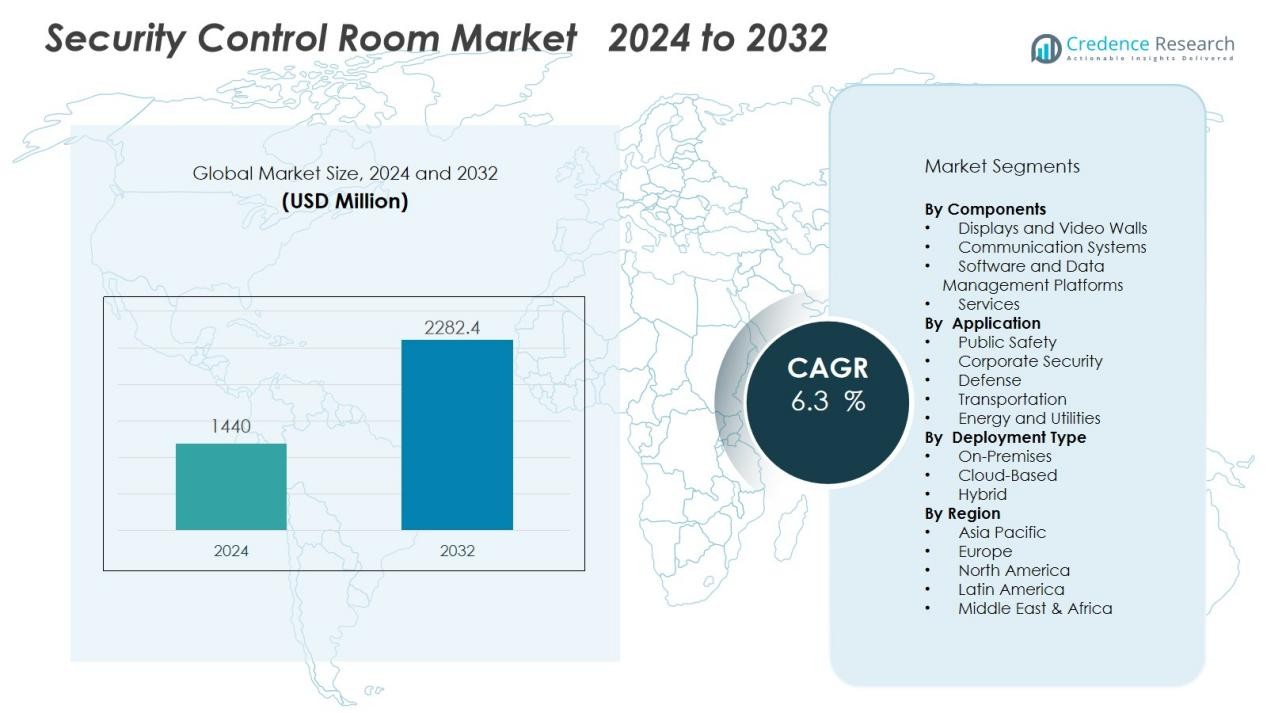

The security control room market size was valued at USD 1400 million in 2024 and is anticipated to reach USD 2282.4 million by 2032, at a CAGR of 6.3 % during the forecast period (2024-2032).

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Security Control Room Market Size 2024 |

USD 1400 Million |

| Security Control Room Market, CAGR |

6.3 % |

| Security Control Room Market Size 2032 |

USD 2282.4 Million |

Key drivers include growing security threats, higher investments in smart city infrastructure, and the need for real-time surveillance in corporate, defense, and transportation sectors. Organizations are focusing on operational efficiency, regulatory compliance, and faster threat detection, which is fueling demand for modernized control room solutions. Enhanced visualization tools, networked video walls, and cloud-based command systems are also accelerating adoption across large enterprises and government agencies.

Regionally, North America dominates the security control room market due to strong investment in public safety and advanced surveillance infrastructure. Europe follows with significant demand from critical infrastructure projects and regulatory frameworks on security compliance. Asia-Pacific is expected to register the fastest growth, supported by rapid urbanization, expanding smart city initiatives, and rising security spending in countries such as China, India, and Japan. The Middle East, Africa, and Latin America are also emerging markets, driven by ongoing infrastructure development and growing focus on counter-terrorism efforts.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Insights:

- The security control room market was valued at USD 1400 million in 2024 and is projected to reach USD 2282.4 million by 2032, growing at a CAGR of 6.3% during 2024–2032.

- Rising terrorism, cyberattacks, and organized crime drive the adoption of advanced control rooms for real-time monitoring and faster decision-making.

- Smart city projects and public safety initiatives are creating strong demand for integrated solutions with AI-driven analytics and visualization tools.

- Technological advancements in AI, IoT, and big data analytics are enhancing situational awareness, reducing response times, and improving operator efficiency.

- Corporate sectors, including energy, transportation, and manufacturing, are adopting control rooms to safeguard assets and strengthen operational continuity.

- High implementation costs, complex system integration, and data privacy concerns remain challenges that limit adoption among smaller organizations.

- North America holds 38% market share, Europe 27%, and Asia-Pacific 24%, with Asia-Pacific forecasted to grow fastest due to urbanization, smart city expansion, and increasing security investments.

Market Drivers:

Growing Threat of Security Breaches and Terrorism Driving Demand for Control Rooms:

The security control room market benefits from the increasing threat of terrorism, cyberattacks, and organized crime. Governments and enterprises are prioritizing real-time monitoring to protect critical infrastructure, airports, financial institutions, and defense facilities. Control rooms enable faster decision-making by consolidating multiple surveillance feeds and communication systems. The rise in security risks compels organizations to invest in advanced monitoring platforms.

- For instance, FLIR Systems’ thermal imaging cameras are installed in more than 1,200 critical infrastructure sites, providing enhanced perimeter security in low-visibility conditions and improving threat detection rates.

Rising Smart City Projects and Public Safety Initiatives Accelerating Market Growth:

Smart city projects are creating strong demand for integrated control room solutions. Governments worldwide are deploying traffic management, law enforcement, and emergency response systems that rely on centralized monitoring hubs. The security control room market gains momentum from these large-scale initiatives, which require advanced visualization, AI-driven analytics, and network integration. Investments in public safety further enhance adoption across urban infrastructure.

- For instance, Cisco Systems enabled the Barcelona city government with its Smart+Connected Digital Platform, integrating more than 8,000 IoT sensors and devices across traffic and public safety applications to facilitate real-time data sharing and emergency communication.

Technological Advancements Enhancing Efficiency and Situational Awareness:

Innovation in artificial intelligence, IoT, and big data analytics is transforming control room operations. It helps operators gain real-time situational awareness and predictive insights, reducing response time to incidents. Modern control rooms integrate video walls, cloud platforms, and mobile connectivity for seamless communication. The security control room market leverages these advancements to meet rising demands for precision and efficiency.

Increasing Corporate and Industrial Adoption Supporting Market Expansion:

Industries such as energy, transportation, and manufacturing are adopting control rooms to safeguard assets and maintain business continuity. Enterprises require reliable platforms for monitoring supply chains, workforce safety, and facility operations. It drives consistent investment in advanced command centers tailored to industrial needs. The security control room market expands further as corporate entities integrate security with operational management systems.

Market Trends:

Integration of AI, IoT, and Cloud Platforms Transforming Control Room Operations:

The security control room market is experiencing strong adoption of artificial intelligence, IoT devices, and cloud-based platforms. AI-driven analytics enhance surveillance by detecting anomalies, recognizing patterns, and predicting risks with greater accuracy. IoT connectivity links cameras, sensors, and alarms into centralized systems for streamlined monitoring. Cloud platforms improve scalability, allowing organizations to manage operations across multiple sites without heavy infrastructure investments. It also supports remote monitoring, which is becoming essential in corporate and public safety environments. These technology integrations improve efficiency and provide operators with real-time decision-making capabilities.

- For instance, Eagle Eye Networks’ cloud video surveillance platform supports more than 70,000 customers worldwide, providing uninterrupted remote video access through their cloud infrastructure.

Market Challenges Analysis:

Shift Toward Unified Visualization and Remote Collaboration Tools:

Modern control rooms are moving toward unified visualization systems and advanced video walls. Organizations are consolidating multiple security feeds into seamless interfaces, reducing operator fatigue and improving situational awareness. Remote collaboration tools are gaining importance, enabling multi-agency coordination during emergencies or cross-border operations. The security control room market leverages these tools to enhance efficiency across government agencies, defense, and large enterprises. Demand for modular, ergonomic designs is also rising, ensuring operator comfort and productivity during long monitoring cycles. It highlights the trend of combining technology with human-centric design to create highly functional and adaptive control environments.

- For example, Milestone Systems’ XProtect Corporate software handled over 10,000 simultaneous connected cameras during large international sporting events, ensuring uninterrupted multi-agency video sharing.

High Implementation Costs and Complex Integration Limiting Widespread Adoption:

The security control room market faces challenges from high setup costs and complex system integration. Establishing advanced control centers requires significant investment in hardware, software, and skilled personnel. Smaller organizations and municipalities often struggle to justify such expenses despite rising security threats. Integrating legacy systems with modern AI-driven platforms also creates compatibility issues. It slows adoption, especially in regions with budget constraints and limited technical expertise. Vendors must address affordability and standardization to expand market reach.

Data Privacy Concerns and Cybersecurity Risks Hindering Growth:

Control rooms manage sensitive data from surveillance networks, communication systems, and IoT devices, which creates significant privacy concerns. Increasing cyberattacks targeting centralized monitoring systems pose operational risks. The security control room market must tackle these threats by adopting advanced cybersecurity frameworks and compliance measures. Organizations are cautious about potential breaches that could compromise critical infrastructure or personal data. It makes regulatory adherence and system resilience key priorities for vendors and users. Building trust through robust security standards remains a major challenge for sustained market expansion.

Market Opportunities:

Expansion of Smart Cities and Critical Infrastructure Projects Creating Strong Growth Potential:

The security control room market has significant opportunities in the expansion of smart cities and critical infrastructure projects. Governments are investing heavily in intelligent traffic systems, public safety, and disaster management, all of which require centralized monitoring hubs. Control rooms are becoming the backbone of these initiatives by enabling real-time surveillance and coordinated response. It positions vendors to deliver advanced solutions that integrate AI, IoT, and big data analytics. Emerging economies are leading this push, supported by urbanization and infrastructure modernization. This trend provides a long-term growth path for technology providers.

Rising Corporate Adoption and Demand for Cloud-Based Solutions Driving Market Expansion:

Corporates across industries such as energy, logistics, and finance are embracing control rooms for operational efficiency and security. The security control room market benefits from the growing demand for cloud-based platforms that reduce infrastructure costs and allow flexible scaling. It also opens opportunities for service providers offering managed security solutions. The shift toward remote monitoring and multi-site coordination further accelerates adoption among enterprises. Vendors that provide modular, customizable, and cost-effective systems can tap into expanding corporate demand. This creates a dynamic growth environment for both established players and emerging firms.

Market Segmentation Analysis:

By Components:

The security control room market is segmented into displays and video walls, communication systems, software and data management platforms, and services. Displays and video walls dominate due to their role in real-time visualization of multiple data streams. Communication systems ensure seamless coordination across agencies and industries. Software platforms are expanding rapidly with the integration of AI, IoT, and predictive analytics. Services, including installation and maintenance, provide consistent revenue streams for vendors. It highlights the growing importance of technology-enabled, centralized monitoring solutions.

- For instance, Motorola Solutions deployed its ASTRO 25 communication system to connect over 100,000 public safety users in Houston, enabling real-time voice and data communication during emergency response operations.

By Application:

Applications include public safety, corporate security, defense, transportation, and energy and utilities. Public safety holds the largest share with demand driven by smart city programs and emergency response initiatives. Defense and transportation also contribute strongly, supported by investments in national security and traffic management. Corporate adoption is rising in industries such as finance and manufacturing. Energy and utilities rely on control rooms to secure critical infrastructure and maintain uninterrupted services. It reflects the wide applicability of control room solutions across industries.

- For instance, Motorola Solutions deployed its CommandCentral platform in the city of Boston, enabling real-time incident response coordination for over 1,000 emergency personnel. Defense and transportation also contribute strongly, supported by investments in national security and traffic management.

By Deployment Type:

Deployment types cover on-premises and cloud-based solutions. On-premises systems remain preferred in defense and high-security environments for greater control and data privacy. Cloud-based models are growing rapidly due to scalability, lower upfront costs, and multi-site accessibility. Hybrid deployments are emerging to combine security with operational flexibility. The security control room market benefits from the increasing shift toward cloud adoption, particularly among enterprises and public sector projects. It signals a future where hybrid and cloud platforms dominate deployments.

Segmentations:

By Components:

- Displays and Video Walls

- Communication Systems

- Software and Data Management Platforms

- Services

By Application:

- Public Safety

- Corporate Security

- Defense

- Transportation

- Energy and Utilities

By Deployment Type:

- On-Premises

- Cloud-Based

- Hybrid

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America:

North America held 38% market share in 2024, driven by large-scale investments in surveillance and security infrastructure. The region benefits from advanced adoption of AI, IoT, and cloud technologies in public safety projects. The United States leads demand with strong deployment across defense, transportation, and smart city initiatives. Canada also contributes with increasing investments in urban safety and infrastructure modernization. The security control room market in North America thrives on strict regulatory standards and high cybersecurity awareness. It continues to expand as enterprises and government agencies adopt integrated command and monitoring platforms. Vendors in the region focus on delivering scalable and high-performance solutions to meet growing needs.

Europe:

Europe accounted for 27% market share in 2024, supported by strict data protection laws and regulatory frameworks. Countries such as Germany, the United Kingdom, and France lead demand with strong adoption across critical infrastructure and corporate sectors. Rising focus on counter-terrorism and cross-border security strengthens the role of control rooms. The security control room market in Europe grows further through integration with transportation systems, utilities, and defense networks. It benefits from government-backed initiatives that prioritize public safety and resilience. Investments in modernizing infrastructure create steady demand for advanced visualization and real-time monitoring platforms. Vendors in the region emphasize compliance and innovation to sustain competitiveness.

Asia-Pacific:

Asia-Pacific held 24% market share in 2024 and is forecasted to record the highest growth rate. China dominates regional adoption, supported by extensive smart city programs and rising infrastructure investments. India follows with strong demand from urban safety, transportation, and industrial projects. Japan and South Korea contribute with advanced integration of AI-driven surveillance and monitoring solutions. The security control room market in Asia-Pacific gains momentum from rapid urbanization, rising crime rates, and increased focus on disaster management. It benefits from government initiatives and private sector participation in building resilient security ecosystems. Vendors are capturing opportunities by offering cost-effective, scalable, and modular solutions tailored to regional requirements.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Axis Communications

- Motorola Solutions

- Cisco Systems

- Tyco Integrated Security

- Avigilon

- Tyco International

- Honeywell

- IBM

- NEC Corporation

- Genetec

- Johnson Controls

- Panasonic

- Competitive Analysis:

The security control room market is highly competitive, shaped by global technology providers and security solution specialists. Key players include Axis Communications, Motorola Solutions, Cisco Systems, Tyco Integrated Security, Avigilon, Tyco International, Honeywell, and IBM. These companies focus on delivering integrated solutions that combine video surveillance, communication, analytics, and data management into centralized platforms. Strong investment in AI, IoT, and cloud technologies strengthens their portfolios and supports advanced security applications. It fosters innovation in visualization tools, real-time monitoring, and cybersecurity integration. Competition also intensifies through strategic partnerships, mergers, and service expansions that extend market presence. Vendors differentiate by offering scalable, cost-efficient, and customizable solutions to meet diverse needs across public safety, defense, transportation, and corporate sectors.

Recent Developments:

- In April 2025, Axis Communications launched new edge devices and advanced AI solutions at ISC West 2025, expanding its capabilities in recording servers, network speakers with displays, and precision air quality sensors.

- In May 2025, Motorola Solutions announced its acquisition of Silvus Technologies, a prominent developer of mobile ad-hoc (MANET) network technology, for $4.4 billion, with completion expected in late 2025.

- In May 2025, Cisco Systems revealed a new collaboration with the AI Infrastructure Partnership (AIP), joining major technology leaders to drive investment and innovation in AI-focused data centers and infrastructure.

Report Coverage:

The research report offers an in-depth analysis based on Components, Application, Deployment Type and Region. It details leading Market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current Market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven Market expansion in recent years. The report also explores Market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on Market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the Market.

Future Outlook:

- The security control room market will evolve with deeper integration of AI and machine learning for predictive threat detection.

- Cloud-based platforms will gain stronger traction, enabling cost-efficient deployment and remote monitoring capabilities.

- Smart city initiatives worldwide will drive demand for centralized control rooms with multi-agency coordination features.

- Cybersecurity resilience will become a key differentiator as vendors address rising risks of data breaches.

- Advanced visualization tools, such as immersive video walls and AR-enabled displays, will enhance situational awareness.

- Demand for modular and ergonomic control room designs will rise to support operator efficiency and comfort.

- The corporate sector will expand adoption, especially in industries like logistics, finance, energy, and manufacturing.

- Governments will prioritize investments in defense and critical infrastructure control rooms to strengthen national security.

- Emerging economies in Asia-Pacific, Latin America, and the Middle East will offer strong growth opportunities through urbanization and infrastructure projects.

- Partnerships between technology providers, governments, and system integrators will accelerate innovation and expand solution availability globally.