Market Overview

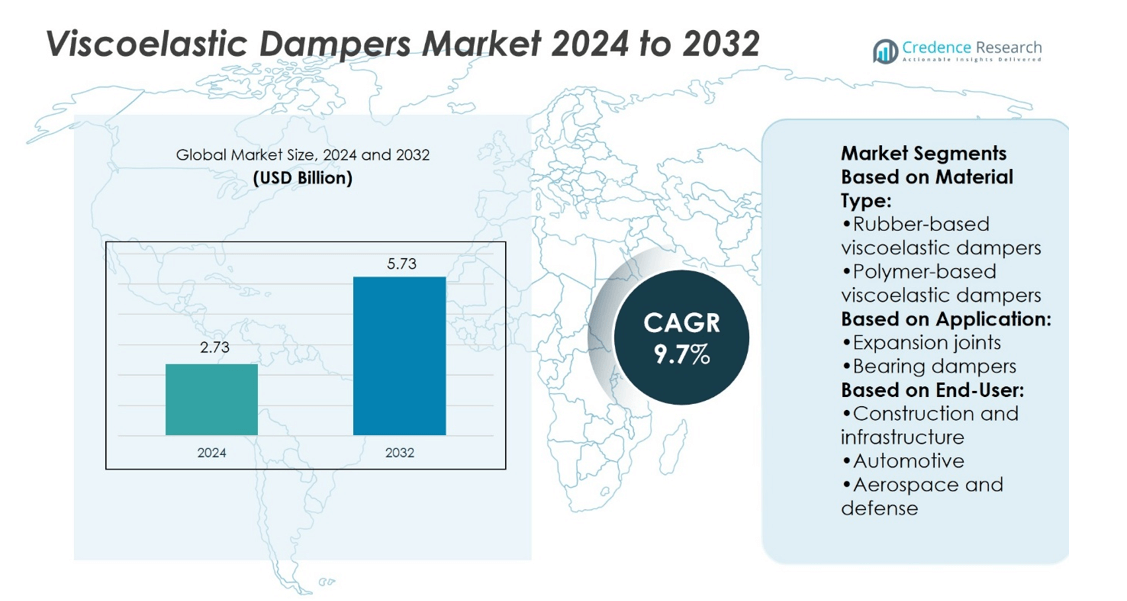

Viscoelastic Dampers Market size was valued at USD 2.73 billion in 2024 and is anticipated to reach USD 5.73 billion by 2032, at a CAGR of 9.7% during the forecast period.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Viscoelastic Dampers Market Size 2024 |

USD 2.73 billion |

| Viscoelastic Dampers Market, CAGR |

9.7% |

| Viscoelastic Dampers Market Size 2032 |

USD 5.73 billion |

The Viscoelastic Dampers Market grows through strong demand driven by seismic safety regulations, urbanization, and large-scale infrastructure projects. It benefits from increasing adoption in high-rise buildings, bridges, and industrial facilities where vibration control is critical. Rising focus on sustainability supports the use of durable, eco-friendly damping materials. Technological advancements in polymers enhance performance under diverse conditions and reduce long-term maintenance needs. Integration with smart monitoring systems further strengthens efficiency and reliability. Expanding applications across automotive, aerospace, and machinery sectors ensure continuous growth. These combined drivers and trends position viscoelastic dampers as a core component of resilient infrastructure worldwide.

North America leads the Viscoelastic Dampers Market with strong regulatory support, while Asia-Pacific records the fastest growth through rapid urbanization and large-scale infrastructure projects. Europe maintains significant share driven by retrofitting programs and sustainable construction practices, whereas Latin America and the Middle East & Africa show gradual adoption supported by urban development initiatives. Key players shaping the competitive landscape include ZF Friedrichshafen AG, BorgWarner, CONTINENTAL AG, Schaeffler Group, Delphi, Visteon, General Motors, TrelleborgVibracoustic, Tuopu, and Hubei Guangao.

Market Insights

- Viscoelastic Dampers Market size was valued at USD 2.73 billion in 2024 and is anticipated to reach USD 5.73 billion by 2032, at a CAGR of 9.7%.

- Seismic safety regulations, urbanization, and infrastructure projects drive consistent adoption in construction and industrial sectors.

- Trends include polymer-based innovations, eco-friendly damping materials, and integration with smart monitoring systems.

- The competitive landscape features strong players focusing on R&D, cost optimization, and global expansion strategies.

- High installation costs and technical complexities remain restraints that limit adoption in cost-sensitive regions.

- North America leads with regulatory enforcement, Europe grows through retrofitting, and Asia-Pacific shows fastest expansion with mega projects.

- Latin America and Middle East & Africa gradually adopt dampers supported by urban development and modernization programs.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers

Seismic Safety Regulations Driving Adoption

Governments worldwide impose strict building codes to ensure safety during earthquakes. The Viscoelastic Dampers Market benefits directly from these mandates, as dampers reduce vibrations and structural risks. It provides an effective solution for high-rise buildings, bridges, and industrial facilities. Compliance with regulations drives large-scale adoption in seismic zones. Urban planners prioritize structures with damping systems to meet resilience standards. This regulatory push ensures long-term demand and market growth.

- For instance, Miller Metal Fabrication expanded its Bridgeville facility by 60,000 square feet, completing construction around 2022. The facility is equipped with fiber lasers capable of high-speed cutting for various metals, which enhances efficiency for industrial projects.

Rising Infrastructure Investments Globally

Countries invest heavily in new infrastructure, including commercial complexes, airports, and transport systems. The Viscoelastic Dampers Market grows as developers integrate dampers to enhance durability and safety. It supports longer lifespans for critical projects while reducing repair costs. Mega infrastructure projects in Asia and the Middle East increase product demand. Growing urbanization and modernization programs strengthen this trend further. Infrastructure upgrades in mature economies also maintain steady adoption rates.

- For instance, Geuder’s NanoEdge® single-use trephines feature blade progression of 0.0625 mm per quarter-turn and 0.25 mm per full rotation for highly precise corneal cuts in keratoplasty.

Technological Advancements and Material Innovation

Research drives continuous improvements in damping materials and installation methods. The Viscoelastic Dampers Market benefits from innovative polymers that offer better energy dissipation. It enhances flexibility for applications in varied climates and structural conditions. Advancements also reduce installation complexity and maintenance needs. Manufacturers develop customizable solutions tailored to project-specific demands. These innovations improve cost efficiency and strengthen product competitiveness in global markets.

Focus on Building Resilience and Sustainability

Resilience against disasters remains a priority for governments and private developers. The Viscoelastic Dampers Market plays a key role in ensuring safety without heavy structural modifications. It aligns with sustainability goals by reducing material use and extending building life cycles. Growing awareness of climate-related risks strengthens adoption in both developed and developing regions. Energy-efficient solutions appeal to environmentally conscious construction firms. The dual focus on resilience and sustainability drives continuous market expansion.

Market Trends

Integration with Smart and Adaptive Structures

The Viscoelastic Dampers Market shows strong momentum with the integration of smart structural technologies. It supports real-time monitoring of vibration and energy dissipation in buildings and bridges. Sensors combined with dampers enhance adaptive response to dynamic loads. Architects and engineers increasingly adopt these solutions in urban construction projects. Smart city initiatives amplify the use of intelligent damping systems. This trend ensures safer, more efficient infrastructure aligned with modern design needs.

- For instance, 3M supplied its VHB™ tapes for a major construction project in Singapore, the Jewel Changi Airport. The tapes were used to bond over 9,000 glass panels in the building’s facade, demonstrating their strength, durability, and ability to handle the dynamic loads of a large structure.

Adoption in High-Rise and Complex Constructions

The construction of tall towers and large-span bridges fuels steady demand for advanced damping systems. The Viscoelastic Dampers Market benefits from engineering designs that require vibration control without adding heavy structural weight. It provides effective protection against wind-induced oscillations and seismic activities. Developers adopt dampers to extend structural life and ensure safety. Urbanization drives large-scale construction in Asia-Pacific and the Middle East. This trend positions dampers as a critical component in future architectural projects.

- For instance, LMK Thermosafe’s Thermosafe Type B Induction Drum Heater warms a 205-liter steel drum using an alternating current power source, such as a 110/120V supply rated at 1,500 watts. Two units can be stacked to cover the full drum height safely in Zone 2 areas.

Shift Toward Lightweight and High-Performance Materials

Manufacturers focus on developing viscoelastic materials with superior energy absorption capacity. The Viscoelastic Dampers Market evolves through the use of polymers that perform consistently across temperature ranges. It reduces maintenance needs and enhances long-term reliability. Lightweight designs improve installation efficiency for both retrofits and new constructions. Research efforts continue to optimize cost-performance balance. This trend reinforces industry competitiveness while addressing varied global construction demands.

Growth of Retrofit and Renovation Applications

Aging infrastructure across developed regions increases the importance of structural retrofitting. The Viscoelastic Dampers Market expands as governments and private developers prioritize safety upgrades. It enables cost-effective reinforcement without complete structural overhauls. Public spending on infrastructure rehabilitation supports this trend across North America and Europe. Building owners adopt dampers to meet new safety standards and extend asset lifecycles. Growing emphasis on resilience ensures retrofitting remains a critical growth area for the market.

Market Challenges Analysis

High Installation Costs and Technical Complexity

The Viscoelastic Dampers Market faces a major challenge due to high upfront costs and technical demands. It requires specialized expertise for design, placement, and integration within complex structures. Limited availability of trained professionals in emerging markets slows large-scale adoption. High initial investment discourages smaller construction firms from implementing damping systems. Retrofitting older buildings with dampers also increases project expenses and timelines. These financial and technical barriers restrict widespread deployment, particularly in cost-sensitive regions.

Performance Limitations under Variable Conditions

The Viscoelastic Dampers Market encounters issues related to material behavior in diverse environments. It shows reduced efficiency when exposed to extreme temperatures or long-term stress cycles. Consistent performance remains difficult in projects located in highly variable climatic zones. Concerns about long-term durability create hesitation among infrastructure developers. Limited standardization in testing methods adds to uncertainty in performance evaluation. These challenges slow acceptance in some markets and highlight the need for continued material innovation.

Market Opportunities

Rising Demand in Emerging Economies

The Viscoelastic Dampers Market holds strong opportunities in rapidly urbanizing regions such as Asia-Pacific, Latin America, and the Middle East. It supports large-scale construction projects where seismic safety and long-term durability are priorities. Governments allocate significant funds toward resilient infrastructure, creating new demand channels. Expanding metro systems, airports, and high-rise developments increase the scope of adoption. Local manufacturing initiatives further reduce costs, making dampers more accessible. These factors combine to create robust growth prospects across developing economies.

Advancements in Material Science and Customization

The Viscoelastic Dampers Market benefits from continuous research in polymers and high-performance materials. It enables manufacturers to deliver products with improved thermal stability, flexibility, and cost efficiency. Custom-designed dampers tailored to specific building requirements gain traction among global developers. Integration with digital monitoring tools expands functionality and strengthens adoption. Growing focus on sustainability encourages eco-friendly damping solutions aligned with green construction standards. These advancements create a pathway for broader applications and long-term competitive advantage.

Market Segmentation Analysis:

By Material Type

The Viscoelastic Dampers Market by material type divides into rubber-based and polymer-based dampers. Rubber-based dampers remain widely adopted for their flexibility and cost-effectiveness in construction projects. Polymer-based dampers gain traction due to superior thermal stability and energy dissipation capabilities. It supports performance in extreme environments where traditional rubber faces durability issues. Developers and engineers prefer advanced polymer-based solutions for high-rise and specialized infrastructure. The growing shift toward material innovation strengthens overall market adoption.

- For instance, During early interim analysis of Phase III trials for exa-cel (now known as Casgevy™), data presented showed that 24 of 27 evaluable patients with transfusion-dependent beta-thalassemia (TDT) achieved transfusion independence

By Application

The Viscoelastic Dampers Market by application includes building and construction, seismic dampers, wind dampers, vibration control dampers, bridges and infrastructures, expansion joints, bearing dampers, industrial machinery, machinery mounts, equipment vibration control, automotive, engine mounts, suspension systems, noise and vibration control, and others. It finds maximum use in building and construction where structural stability is essential. Seismic and wind dampers hold significant demand in earthquake-prone and high-wind regions. Industrial machinery applications expand as manufacturers seek vibration reduction in equipment. Automotive applications such as engine mounts and suspension systems also contribute steadily to growth. Diverse application areas ensure continuous market expansion across industries.

- For instance, Pall’s pilot microfiltration system successfully treated raw water with turbidity levels as high as 450 NTU, yet still delivered filtrate turbidity under 0.1 NTU across extended operations. This performance minimized downtime and reduced the reliance on chemical pre-treatment in municipal facilities.

By End-User

The Viscoelastic Dampers Market by end-user segments into construction and infrastructure, automotive, aerospace and defense, and manufacturing and machinery. Construction and infrastructure dominate adoption due to regulatory safety requirements and urban development projects. Automotive applications continue to expand with rising focus on passenger comfort and vehicle durability. Aerospace and defense sectors adopt dampers for noise, vibration, and shock management in aircraft and defense systems. Manufacturing and machinery use it to safeguard high-precision equipment and enhance operational efficiency. Strong demand across these sectors underlines the versatile value of viscoelastic dampers in global markets.

Segments:

Based on Material Type:

- Rubber-based viscoelastic dampers

- Polymer-based viscoelastic dampers

Based on Application:

- Expansion joints

- Bearing dampers

Based on End-User:

- Construction and infrastructure

- Automotive

- Aerospace and defense

Based on the Geography:

- North America

- Europe

- UK

- France

- Germany

- Italy

- Spain

- Russia

- Belgium

- Netherlands

- Austria

- Sweden

- Poland

- Denmark

- Switzerland

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Thailand

- Indonesia

- Vietnam

- Malaysia

- Philippines

- Taiwan

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Peru

- Chile

- Colombia

- Rest of Latin America

- Middle East

- UAE

- KSA

- Israel

- Turkey

- Iran

- Rest of Middle East

- Africa

- Egypt

- Nigeria

- Algeria

- Morocco

- Rest of Africa

Regional Analysis

North America

North America accounted for 34% share of the Viscoelastic Dampers Market in 2024, leading global adoption. Strong enforcement of seismic safety regulations in the United States and Canada drives consistent demand for damping solutions in high-rise buildings, bridges, and critical infrastructure. It benefits from mature construction practices where safety and long-term performance remain priorities. The presence of advanced research facilities and material innovation centers supports continuous product development. Retrofit projects in earthquake-prone areas of California and new infrastructure investments across urban regions sustain steady growth. North America also integrates dampers into smart building projects, aligning with energy efficiency and resilience goals.

Europe

Europe represented 27% share of the Viscoelastic Dampers Market in 2024, supported by widespread urban renewal and sustainability-driven construction practices. It maintains robust demand due to strict EU building codes and emphasis on energy efficiency. Countries such as Germany, Italy, and France focus heavily on retrofitting aging infrastructure with damping systems. Rising investments in transport projects, bridges, and metro systems also strengthen adoption. European manufacturers invest in polymer-based innovations to improve thermal stability and eco-friendly performance. With governments prioritizing climate resilience, Europe ensures viscoelastic dampers remain integral to both new builds and rehabilitation projects.

Asia-Pacific

Asia-Pacific held 29% share of the Viscoelastic Dampers Market in 2024, ranking as the fastest-growing region. Rapid urbanization in China, India, and Southeast Asia generates demand for damping solutions in skyscrapers, airports, and transport corridors. It supports large-scale infrastructure investments backed by government funding and private capital. Frequent seismic activity in Japan and parts of Southeast Asia fuels adoption of seismic dampers for structural resilience. Growing construction of bridges and industrial facilities further accelerates market growth. Regional suppliers focus on cost-efficient materials to meet rising demand from developing economies. Asia-Pacific is expected to expand its share further due to continuous mega project developments.

Latin America

Latin America captured 6% share of the Viscoelastic Dampers Market in 2024, reflecting growing but still emerging adoption. Brazil, Mexico, and Chile drive regional demand through investments in commercial construction and seismic safety projects. It faces challenges from limited awareness and budget constraints among smaller developers. Government-led initiatives for urban renewal and transportation networks support gradual integration of damping technologies. International partnerships with global manufacturers help improve accessibility of advanced solutions. Latin America is projected to see steady gains as resilience-focused construction policies gain momentum.

Middle East & Africa

The Middle East & Africa accounted for 4% share of the Viscoelastic Dampers Market in 2024, representing the smallest but steadily developing region. Large-scale construction projects in the UAE, Saudi Arabia, and Qatar create demand for vibration control systems in skyscrapers, airports, and stadiums. It benefits from government-backed infrastructure modernization programs, particularly under Vision 2030 initiatives. Africa shows slower adoption due to limited construction budgets but holds potential in South Africa and Nigeria through urban development. Growing interest in sustainable and resilient building practices adds momentum to regional adoption. With continued infrastructure expansion, this region will remain a niche but promising contributor.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis

Competitive Analysis

The Viscoelastic Dampers Market include ZF Friedrichshafen AG, Tuopu, Delphi, BorgWarner, Hubei Guangao, CONTINENTAL AG, General Motors, TrelleborgVibracoustic, Visteon, and Schaeffler Group. The Viscoelastic Dampers Market shows a highly competitive landscape shaped by innovation, regional expansion, and strong focus on application-specific solutions. Companies compete by advancing material technologies that improve thermal stability, energy absorption, and long-term durability across construction, automotive, and industrial uses. Strategic collaborations with infrastructure developers and automotive manufacturers support deeper market penetration. Regional firms emphasize cost-effective solutions, while global players prioritize R&D-driven designs for advanced performance. The competitive dynamic highlights a balance between affordability and high-end innovation, ensuring continuous growth opportunities across diverse end-use sectors.

Recent Developments

- In June 2024, Alcon received FDA clearance for its UNITY Vitreoretinal Cataract System (VCS) and UNITY Cataract System (CS). These are the first products from Alcon’s new Unity portfolio. This clearance marks a significant milestone for Alcon, as it expands its offerings in the eye care market.

- In April 2024, Carl Zeiss Meditec AG announced the acquisition of the Dutch Ophthalmic Research Center (D.O.R.C.). This strategic move aims to consolidate the companies’ strengths and drive innovation in ophthalmic medical devices and surgery.

- In January 2024, Rayner, a UK-based ophthalmic company, acquired Sophi, a Swiss manufacturer known for its innovative phacoemulsification systems. The acquisition aims to diversify Rayner’s surgical offerings, integrating Sophi’s advanced fluidics and wireless technologies to improve cataract surgery outcomes.

- In April 2023, Canadian eye health company Bausch + Lomb launched the StableVisc cohesive ophthalmic viscosurgical device (OVD) and the TotalVisc Viscoelastic System in the US. The company stated that StableVisc helps maintain space in the eye’s anterior chamber, allowing doctors to remove and replace the clouded natural lens.

Report Coverage

The research report offers an in-depth analysis based on Material Type, Application, End-User and Geography. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook

- The market will expand through rising adoption in seismic safety projects.

- Demand will grow in high-rise buildings and smart infrastructure developments.

- Polymer-based dampers will gain share due to better performance and durability.

- Retrofit projects will create consistent opportunities in developed economies.

- Emerging economies will drive demand with large-scale construction programs.

- Automotive applications will expand with focus on vibration and noise reduction.

- Integration with digital monitoring systems will increase product value.

- Material innovation will reduce costs and improve energy dissipation efficiency.

- Government regulations will continue to enforce adoption in safety-critical projects.

- Sustainability goals will push the use of eco-friendly damping solutions.