Market Overview:

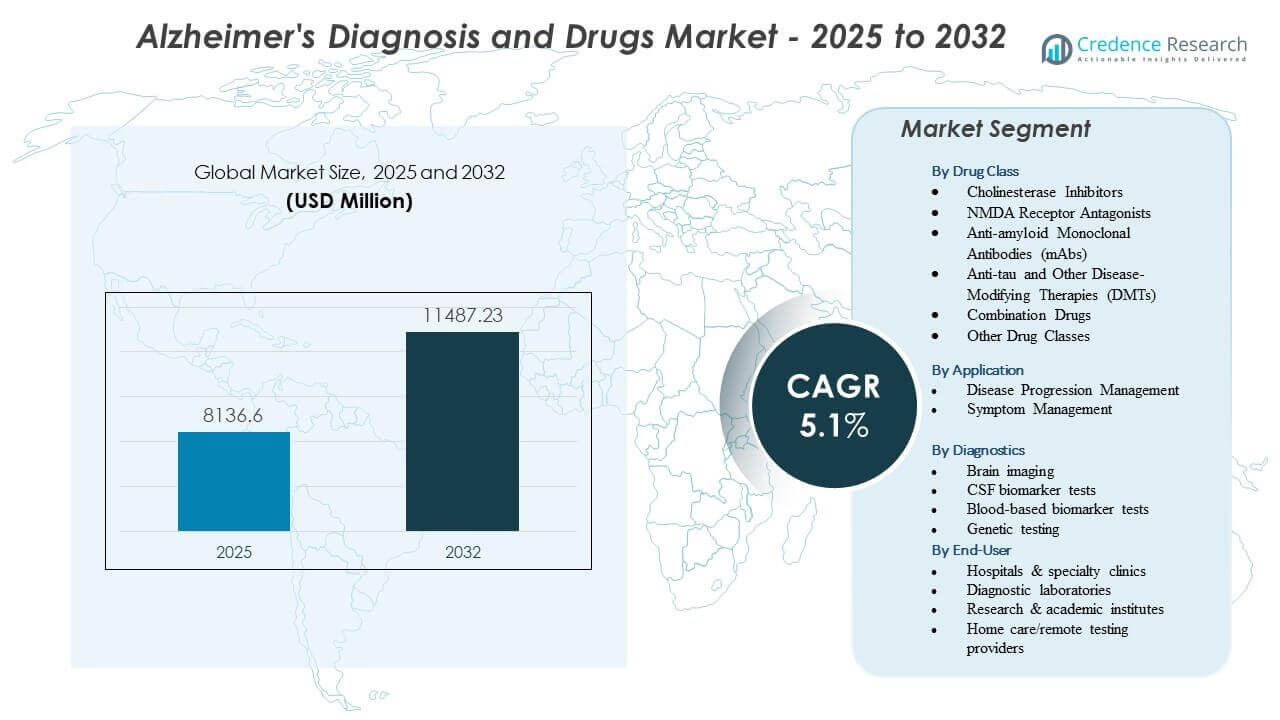

The Alzheimer’s Diagnosis and Drugs Market is projected to grow from USD 8,136.6 million in 2025 to an estimated USD 11,487.23 million by 2032, with a compound annual growth rate (CAGR) of 5.1% from 2025 to 2032.

| RT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Alzheimer’s Diagnosis and Drugs Market Size 2025 |

USD 8,136.6 million |

| Alzheimer’s Diagnosis and Drugs Market, CAGR |

5.1% |

| Alzheimer’s Diagnosis and Drugs Market Size 2032 |

USD 11,487.23 million |

Market Insights:

- Demand strengthens as healthcare systems prioritize early detection supported by biomarker adoption, improved imaging accuracy, and growing reliance on disease-modifying therapies in clinical practice.

- Market restraints persist due to high diagnostic costs, limited specialist availability, and uneven access to advanced testing in developing regions, slowing uniform adoption.

- North America leads growth due to strong infrastructure and rapid therapy uptake, while Europe maintains steady expansion through structured dementia strategies and high testing capacity.

- Asia-Pacific emerges as the fastest-growing region with rising awareness, expanding neurology services, and wider integration of biomarker and imaging tools across major healthcare networks.

Market Drivers

Rising Global Prevalence and Earlier Clinical Detection

Growing awareness pushes families to seek medical help sooner, which supports early-stage diagnosis across many care settings. New screening programs help clinicians identify symptoms before severe decline. The Alzheimer’s Diagnosis and Drugs Market benefits from rising diagnostic demand. Biomarker-based tests gain wider acceptance, helping physicians improve accuracy. Hospitals expand neurology units to handle higher caseloads. Pharmaceutical firms speed up work on targeted therapies. Governments publish dementia roadmaps to strengthen access to evaluation tools. Public interest in early prediction technologies continues to rise.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Advancements in Imaging, Biomarkers, and Diagnostic Accuracy

PET scans, MRI techniques, and CSF biomarkers create stronger confidence in test results across diverse populations. Clinicians adopt advanced tools that detect brain changes before severe cognitive loss. The Alzheimer’s Diagnosis and Drugs Market gains momentum from stronger diagnostic clarity. Imaging vendors improve hardware and software, which helps reduce interpretation errors. Researchers explore blood-based biomarkers to support less invasive testing. Health systems train specialists to improve diagnostic workflows. Pharmaceutical firms use these tools to enhance trial enrollment accuracy. Earlier detection helps match patients to suitable therapies.

- For instance, Siemens Healthineers’ Biograph Vision PET/CT system improves image resolution to 3.2 mm, enabling more precise quantification of amyloid burden.

Growth in Disease-Modifying Drug Research and New Therapeutic Pipelines

Drug developers increase investment in monoclonal antibodies aimed at slowing cognitive decline. Research teams explore precision therapies linked to genetic risk factors. The Alzheimer’s Diagnosis and Drugs Market expands with new trial activity. Firms collaborate with academic centers to test next-generation drug candidates. Regulators refine guidance to support more efficient study designs. Patients gain faster access to innovative therapies through expanded trial networks. Companies aim to lower disease progression rates with targeted modalities. Growing investment supports steady momentum in drug discovery programs.

- For instance, Eli Lilly’s donanemab Phase 3 TRAILBLAZER-ALZ 2 trial achieved a 35% slowing of decline on the integrated AD rating scale.

Supportive Regulatory Pathways and Strengthening Government Initiatives

Regulators create fast-track pathways for promising therapies with strong clinical potential. Agencies encourage real-world evidence to support long-term safety reviews. The Alzheimer’s Diagnosis and Drugs Market gains support from structured policy reforms. Countries issue dementia action plans to expand diagnostic access. Public funding helps hospitals improve equipment and specialist capacity. Governments promote awareness programs to drive early consultation. Health ministries adopt new reimbursement terms for advanced tests. Policy changes help strengthen system-wide response capabilities.

Market Trends

Shift Toward Non-Invasive and Accessible Testing Models

Blood-based biomarker tests gain strong interest because they reduce patient burden. Early research shows promise in detecting amyloid levels with simple draws. The Alzheimer’s Diagnosis and Drugs Market sees growing adoption of accessible testing. Companies work on scalable platforms suited for primary care. Health systems explore these models to expand coverage in rural areas. Diagnostic firms refine sensitivity levels for broad use. Physicians expect these tools to reshape clinical workflows. Broader access may support earlier therapeutic intervention.

Integration of AI and Digital Platforms for Cognitive Assessment

AI tools help clinicians analyze speech, behavior, and memory tasks with higher precision. Digital assessments reduce exam time and improve consistency across facilities. The Alzheimer’s Diagnosis and Drugs Market benefits from the rising use of smart platforms. Hospitals deploy remote cognitive screening apps to support aging populations. AI models support triage decisions in busy clinics. Developers work on real-time scoring engines to help neurologists. Telehealth platforms integrate these tools to expand reach. Digital adoption helps monitor patients between visits.

Expansion of Home-Based Monitoring and Remote Care Programs

Families prefer home-based monitoring tools to evaluate daily functional changes. Wearable sensors track sleep patterns, movement, and cognitive cues. The Alzheimer’s Diagnosis and Drugs Market sees stronger demand for remote oversight. Technology firms develop devices that alert caregivers to behavioral shifts. Clinicians use remote data to guide medication adjustments. Health systems support home programs to reduce emergency visits. Insurance groups show interest in reimbursing remote solutions. This shift improves patient comfort and long-term engagement.

- For instance, Biofourmis’ FDA-cleared digital platform has been used in clinical studies to monitor daily functional patterns and physiological changes in older adults, supporting early identification of cognitive decline markers relevant to Alzheimer’s research.

Growing Collaboration Between Tech Firms, Research Bodies, and Pharma

Research partnerships help accelerate work on fast, reliable diagnostic models. Tech firms supply advanced analytics platforms to improve research outputs. The Alzheimer’s Diagnosis and Drugs Market gains strength from cross-sector innovation. Pharmaceutical developers use these partnerships to improve trial precision. Academic groups contribute biomarker datasets to support discovery. Joint ventures help scale tools for commercial use. This collaboration helps shorten development cycles. Many players align resources to build integrated care ecosystems.

- For instance, Eisai and Biogen collaborate with major academic groups such as ACTC and ADNI to support lecanemab research, using large biomarker-rich cohorts like the CLARITY-AD Phase 3 trial, which enrolled 1,795 participants. These partnerships strengthen validation of amyloid and tau biomarker performance across diverse clinical populations.

Market Challenges Analysis

High Diagnostic Costs and Uneven Access Across Healthcare Systems

Specialized tests such as PET scans and CSF biomarker panels remain expensive. Many regions lack trained neurologists for early-stage diagnosis. The Alzheimer’s Diagnosis and Drugs Market faces long wait times in public hospitals. Rural populations struggle with limited access to advanced tools. Health systems face pressure to fund new diagnostic platforms. Families encounter financial strain due to ongoing testing needs. Drug assessments require regular follow-up, which adds cost burden. Limited reimbursement policies widen the access gap for vulnerable groups.

Complex Drug Development Pathways and High Clinical Failure Rates

Developers face long timelines to prove clinical effectiveness in diverse patient groups. Many drug candidates fail to meet cognitive improvement endpoints. The Alzheimer’s Diagnosis and Drugs Market must navigate strict regulatory expectations. Trial designs require large patient pools and long monitoring periods. Safety concerns often delay progression to advanced phases. High R&D spending strains company budgets during slow development cycles. Companies face hurdles in proving long-term disease modification. These barriers slow the pace of drug innovation across the field.

Market Opportunities

Emerging Blood-Based Diagnostics and Precision-Therapy Pathways

Blood biomarker platforms can reach primary care clinics and widen early detection access. These models offer faster testing and lower patient discomfort. The Alzheimer’s Diagnosis and Drugs Market gains strong potential from scalable diagnostics. Companies can design integrated screening programs across large health networks. Biomarker-driven insights support more precise treatment selection. Researchers explore genetic targeting approaches for high-risk groups. Health systems may adopt tiered screening programs based on these tools. Early-stage therapeutic alignment creates major commercial value.

Expansion of Digital Cognitive Tools and Global Dementia Preparedness Plans

Digital platforms offer continuous monitoring and personalized cognitive tracking. These tools help clinicians understand real-time changes in daily life. The Alzheimer’s Diagnosis and Drugs Market benefits from the rising need for remote care. Governments invest in dementia preparedness strategies to strengthen evaluation systems. Technology firms can partner with hospitals to expand adoption. Pharmaceutical companies use digital endpoints to improve trial efficiency. Remote monitoring improves patient management in underserved regions. This creates room for new business models and stronger ecosystem collaboration.

Market Segmentation Analysis:

By Drug Class

The Alzheimer’s Diagnosis and Drugs Market shows strong activity across major drug classes that support both symptom relief and disease modification. Cholinesterase inhibitors and NMDA receptor antagonists remain widely used for symptom stabilization, while anti-amyloid mAbs and anti-tau DMTs gain momentum due to their disease-targeting potential. Combination drugs support improved adherence and broader clinical utility. Other emerging drug classes expand innovation across neurological pathways.

By Application

Application trends divide into disease progression management and symptom management, giving providers structured pathways for tailored patient care. This structure helps clinicians match treatments to disease stage. Growth links closely to rising diagnosis rates worldwide.

By Diagnostic

Diagnostic technologies strengthen early detection across many care settings, supporting broader use of biomarker and imaging tools in the Alzheimer’s Diagnosis and Drugs Market. Brain imaging remains central for structural and functional assessment, while CSF tests provide high diagnostic accuracy for amyloid and tau burden. Blood-based biomarkers show strong adoption due to easier sampling and growing clinical reliability. Genetic testing offers insight into hereditary risk and disease susceptibility. These tools help clinicians refine treatment paths and guide therapeutic eligibility. Hospitals expand capacity for advanced diagnostics. Wider testing adoption improves early intervention outcomes.

- For instance, Quanterix’s Simoa® p-tau217 assay achieved over 90% accuracy in distinguishing Alzheimer’s pathology, supporting its use as a scalable clinical biomarker.

By End-User

End-user groups shape adoption across the Alzheimer’s Diagnosis and Drugs Market by directing diagnostic workflows, therapy access, and patient support. Hospitals and specialty clinics lead with advanced imaging and infusion capabilities, while diagnostic laboratories manage high-volume biomarker testing with reliable turnaround times. Research and academic institutes validate biomarkers and advance drug development, strengthening clinical decision-making. Home care and remote testing providers expand convenient monitoring options for aging populations. Strong integration between clinics, laboratories, and home-based tools improves diagnostic accuracy, supports timely therapy adjustments, and enhances long-term patient management through coordinated care.

- For instance, Labcorp provides plasma Aβ42/40 ratio testing to help clinicians evaluate early Alzheimer’s pathology, using high-sensitivity mass spectrometry methods validated in clinical research. The company supports broad access to these tests through its nationwide network of patient service centers, enabling widespread clinical adoption.

Segmentation:

By Drug Class

- Cholinesterase Inhibitors

- NMDA Receptor Antagonists

- Anti-amyloid Monoclonal Antibodies (mAbs)

- Anti-tau and Other Disease-Modifying Therapies (DMTs)

- Combination Drugs

- Other Drug Classes

By Application

- Disease Progression Management

- Symptom Management

By Diagnostics

- Brain imaging

- CSF biomarker tests

- Blood-based biomarker tests

- Genetic testing

By End-User

- Hospitals & specialty clinics

- Diagnostic laboratories

- Research & academic institutes

- Home care/remote testing providers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

North America holds the largest share of the Alzheimer’s Diagnosis and Drugs Market with about 45%, driven by strong diagnostic infrastructure and early adoption of advanced therapies. Hospitals lead investment in imaging systems, biomarker testing, and infusion centers that support new drug classes. The region benefits from active clinical trials run by major pharmaceutical firms. Providers follow well-established dementia care pathways that improve detection and monitoring. The Alzheimer’s Diagnosis and Drugs Market gains steady growth here due to high awareness and structured reimbursement. It remains the most influential region in shaping product uptake.

Europe accounts for roughly 30% of the global share due to strong healthcare coverage and rising demand for early-stage testing. Countries expand dementia strategies that promote biomarker adoption and structured care delivery. Clinics invest in MRI, PET, and CSF analysis capacity to support standardized diagnosis. Pharmaceutical companies collaborate with academic institutes to strengthen real-world evidence. Research bodies refine genetic testing and blood-based biomarker programs. The Alzheimer’s Diagnosis and Drugs Market benefits from consistent regulatory support across major markets. It maintains stable demand due to an aging population.

Asia-Pacific holds close to 20% of global share and represents the fastest-growing region due to rising investment in imaging and biomarker capabilities. Governments expand national dementia programs that support early detection. Hospitals upgrade neurology units to meet higher patient volumes. Diagnostic labs introduce blood-based biomarker tests to support wider access. Research centers in Japan, China, and South Korea drive innovation in disease-modifying therapies. The Alzheimer’s Diagnosis and Drugs Market gains long-term momentum here due to unmet diagnostic needs. It sees strong potential from growing awareness and improved healthcare access.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- AstraZeneca PLC

- Bristol-Myers Squibb Company

- Johnson & Johnson (Janssen)

- Eli Lilly and Company

- Hoffmann-La Roche AG

- Biogen Inc.

- Novartis AG

- AbbVie Inc.

- Eisai Co., Ltd.

- Teva Pharmaceutical Industries Ltd.

- Merck KGaA / Merck & Co.

- Zydus Lifesciences Ltd. (Zydus Group)

- Lupin Limited

- Supernus Pharmaceuticals, Inc.

- Corium Inc.

- Grifols, S.A.

- Siemens Healthineers / Siemens Healthcare GmbH

- Lantheus

- Fujirebio

- C2N Diagnostics

- Quanterix

- Sysmex

Competitive Analysis:

The Alzheimer’s Diagnosis and Drugs Market remains highly competitive due to strong participation from global pharmaceutical leaders and diagnostic technology firms. Companies such as Eli Lilly, Biogen, Roche, and Eisai drive progress in disease-modifying therapies, focusing on monoclonal antibodies and targeted mechanisms. It gains rising innovation as developers refine anti-amyloid and anti-tau pipelines to improve clinical outcomes. Diagnostic companies expand blood-based biomarker platforms to support broader testing access. Siemens Healthineers, Fujirebio, Quanterix, and C2N Diagnostics lead efforts to improve accuracy and turnaround times. Laboratories such as Labcorp and Quest Diagnostics strengthen the ecosystem with high-volume testing capacity. Collaboration between research institutes, tech developers, and pharma groups accelerates trial execution and biomarker validation. The competitive landscape moves toward integrated diagnostic-therapeutic models that enhance patient management and expand market reach.

Recent Developments:

- In January 2026, the FDA accepted Eisai’s priority-review filing for an autoinjector formulation of lecanemab, expanding at-home dosing options for this Alzheimer’s treatment.

- In May 2025, Sanofi acquired Vigil Neuroscience for $470 million, adding the investigational Alzheimer’s drug VG-3927 a TREM2-targeting small molecule to its neurology pipeline.

Report Coverage:

The research report offers an in-depth analysis based on Drug Class, Application, Diagnostics, End-User, and Region. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- The Alzheimer’s Diagnosis and Drugs Market will see faster adoption of disease-modifying therapies as clinical confidence improves.

- Blood-based biomarker tests will expand early detection, increasing testing volumes across primary care settings.

- Imaging and CSF biomarker capacity will grow in hospitals as demand for accurate staging rises worldwide.

- Digital cognitive tools and remote monitoring platforms will strengthen patient assessment outside traditional clinics.

- Pharma companies will increase investment in anti-amyloid and anti-tau pipelines to support long-term disease management.

- Combination therapies will gain attention for targeting multiple biological pathways more effectively.

- Genetic testing adoption will rise in high-risk populations as providers integrate personalized care strategies.

- Collaboration between diagnostic labs and specialty clinics will improve test accessibility and clinical decision-making.

- Asia-Pacific will gain momentum due to rising awareness, expanding diagnostic infrastructure, and improving care pathways.

- Integrated diagnostic-therapeutic models will become central to shaping treatment alignment and long-term patient support.