Autologous Stem Cell and Non Stem Cell Based Therapies Market Overview:

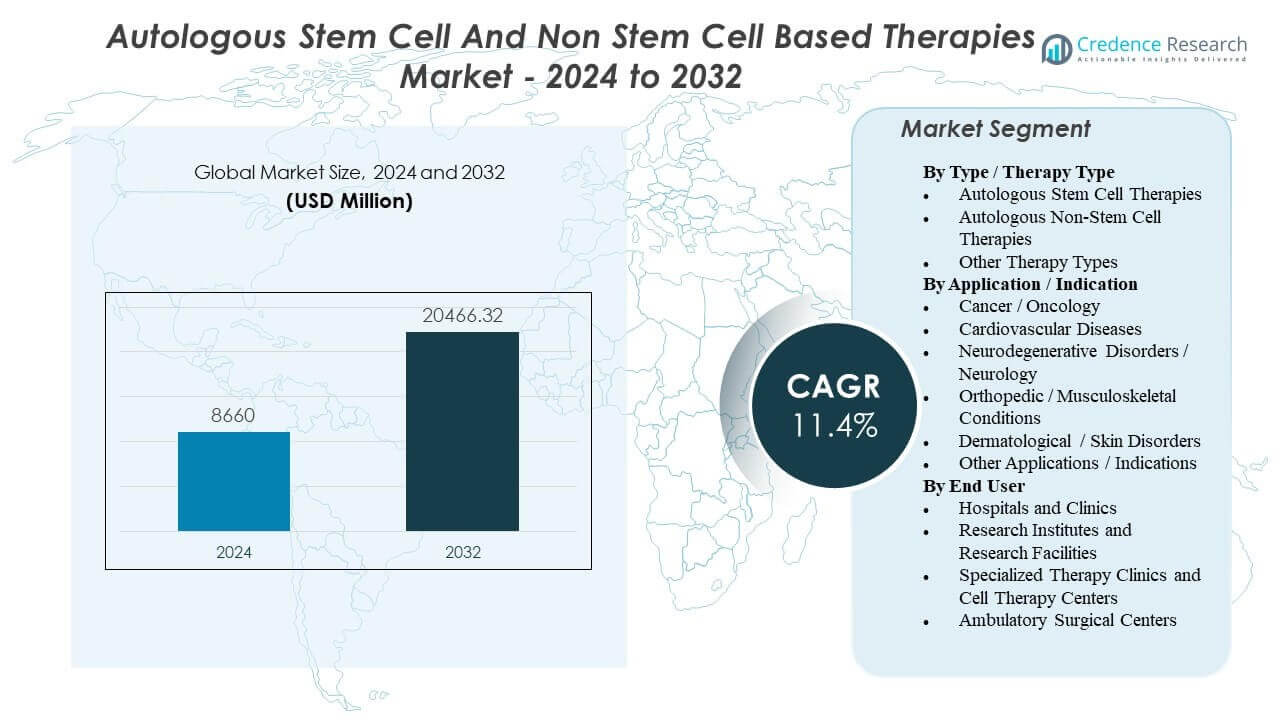

The Autologous Stem Cell and Non Stem Cell Based Therapies Market is projected to grow from USD 8,660 million in 2024 to an estimated USD 20,466.32 million by 2032, with a compound annual growth rate (CAGR) of 11.4% from 2024 to 2032.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Autologous Stem Cell and Non Stem Cell Based Therapies Market Size 2024 |

USD 8,660 million |

| Autologous Stem Cell and Non Stem Cell Based Therapies Market, CAGR |

11.4% |

| Autologous Stem Cell and Non Stem Cell Based Therapies Market Size 2032 |

USD 20,466.32 million |

Growth is largely supported by expanding clinical use of patient-specific cell therapies, especially in oncology, where defined care pathways and specialist-center capacity can translate into higher treatment volumes. At the same time, unmet needs in chronic and degenerative conditions continue to stimulate demand for regenerative approaches in select indications. Manufacturing progress particularly automation, closed processing, and improved logistics coordination also makes autologous workflows more feasible, improving consistency and scaling potential.

North America and Western Europe lead due to advanced infrastructure and specialist centers, while Asia-Pacific is emerging as capacity expands. Adoption varies by reimbursement, regulatory clarity, and the availability of trained cell-therapy sites.

The market includes autologous stem cell and non-stem cell therapies across oncology, cardiovascular, neurology, orthopedics, and dermatology. Delivery is concentrated in hospitals and specialized cell therapy centers, with research and ambulatory settings supporting trials and select procedures.

Autologous Stem Cell and Non Stem Cell Based Therapies Market Insights:

- Growth is being driven mainly by wider clinical use of autologous cell therapies in oncology, alongside rising chronic disease burden that supports regenerative use in selected indications.

- Scaling remains constrained by patient-specific manufacturing complexity, vein-to-vein timelines, capacity limits, and variability risks that can increase cost per treated patient and restrict access beyond major centers.

- North America and Western Europe lead due to established infrastructure and specialist sites, while Asia-Pacific is emerging as investment in cell-therapy capability and clinical participation increases.

- Market momentum is supported by improving manufacturing automation and logistics coordination, but adoption continues to depend on evidence strength, regulatory clarity, and reimbursement pathways by indication and geography.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Autologous Stem Cell and Non Stem Cell Based Therapies Market Drivers

Expanding clinical use of personalized immune-cell therapies in oncology is lifting baseline demand

Autologous immune-cell therapies are seeing wider use in oncology, particularly in hematologic cancers. As more treatment centers gain experience, referrals and patient identification tend to improve. This increases demand for apheresis, manufacturing capacity, and qualified treatment sites. The driver is strongest where individualized cell engineering has shown meaningful benefit in refractory disease settings.

- For instance, Novartis reports KYMRIAH (tisagenlecleucel) is available at more than 370 certified treatment centersacross 30 countries, which directly expands the operational footprint for apheresis collection, manufacturing slots, and qualified infusion sites.

Higher chronic-disease burden and unmet need in regenerative indications supports experimentation and adoption

Chronic and degenerative diseases are increasing the pool of patients looking for restorative treatment options. Autologous stem cell approaches are often explored where standard care does not restore function, especially in specialty and elective settings. Aging populations and musculoskeletal burden reinforce this demand in many health systems. Adoption still depends on local regulation and the strength of clinical evidence by indication.

- For instance, Vericel’s MACI (matrix‑applied characterized autologous cultured chondrocytes) was evaluated in the randomized SUMMIT trial where 144 patientswere treated and 137 (95%) completed the 2‑year assessment, with a reported mean lesion size of 8 cm².

Advancements in manufacturing automation and closed systems are improving feasibility at scale

Automation and closed processing systems are reducing manual steps and contamination risk in autologous workflows. Standardized manufacturing can improve consistency across sites and reduce batch variability. These improvements help developers scale commercial supply and late-stage trials more predictably. Over time, better yields and fewer failures can lower effective cost per treated patient.

Regulatory frameworks and expedited pathways can accelerate clinical translation for eligible programs

Clearer advanced-therapy regulatory frameworks reduce uncertainty about quality, traceability, and evidence expectations. Some programs can also benefit from accelerated pathways, shortening time-to-market in defined cases. Regulatory clarity supports better chain-of-custody design, which is critical for autologous products. This combination can increase the number of programs moving from trials toward commercialization.

Autologous Stem Cell and Non Stem Cell Based Therapies Market Trends and Opportunities

Point-of-care and distributed “micro-factory” models are emerging to reduce logistics friction

Developers are testing decentralized or hybrid manufacturing models to reduce transport and scheduling constraints. Producing closer to treatment sites can lower chain-of-custody risk and shorten turnaround times. This is relevant in regions with uneven cold-chain and specialist-site coverage. The opportunity is to pair automated platforms with standardized local quality oversight for broader hospital adoption.

Faster turnaround and improved scheduling are becoming competitive differentiators

Cycle time is becoming a key operational metric because delays affect both patient readiness and clinic capacity planning. Many autologous products still require multi-week vein-to-vein timelines, creating pressure to optimize end-to-end coordination. Companies are investing in better scheduling, capacity planning, and release-testing strategies to reduce variability. Vendors that reliably shorten turnaround can be advantaged in time-sensitive indications.

Growth in enabling technologies is creating a larger ecosystem beyond therapy developers

Spending is rising on enabling technologies such as automation, analytics/QC, chain-of-identity software, and specialized logistics. This reflects a shift toward building repeatable, compliant manufacturing at scale across more programs. The opportunity extends to recurring revenues from consumables, service contracts, and platform upgrades. Growth in automated/closed systems is commonly tracked as a supporting tailwind for the broader autologous therapy market.

Evidence generation and real-world data are shaping reimbursement pathways and market expansion

Payers are placing more emphasis on durability of benefit relative to high upfront treatment costs. This is pushing companies toward registries, real-world evidence, and outcomes tracking to support coverage decisions. The opportunity is to expand reimbursement through better patient selection and outcomes-based payment models. A constraint is that evidence accumulation takes time, which can slow adoption in cost-sensitive systems.

Autologous Stem Cell and Non Stem Cell Based Therapies Market Challenges Analysis

Autologous therapies remain expensive and operationally complex because each batch is patient-specific and requires strict chain-of-identity controls. Vein-to-vein timelines and limited manufacturing slots can constrain throughput and add scheduling friction at hospitals. Batch failures, variability, and cold-chain dependencies can further reduce usable capacity. These factors tend to limit access outside major centers and slow broad-based scaling.

- For example, Novartis’ KYMRIAH site materials emphasize strict cryogenic control—keeping the product below −120°C in transport and storage, with readings above −120°C treated as temperature excursions (with limited exceptions). They also require tightly coordinated thawing so that once the product reaches 20–25°C, it is infused within 30 minutes, highlighting how cold-chain reliance and scheduling precision affect real-world delivery.

Regulatory and reimbursement pathways can be uneven, especially for regenerative indications where evidence quality varies by use case. Compliance expectations for advanced therapies raise requirements for manufacturing controls, testing, and documentation. Payers often require stronger durability and comparative value evidence, which can narrow eligible populations. As a result, commercial growth frequently depends on health-system readiness and payment models, not only clinical interest.

- For example, the YESCARTA/TECARTUS REMS enrollment requirements specify that certified hospitals must keep at least two doses of tocilizumab per patient on-site, available for use within 2 hours of infusion if needed. Sites must also maintain documented procedures that can be reviewed in audits, making “site readiness” an operational compliance issue as much as a clinical one.

Autologous Stem Cell and Non Stem Cell Based Therapies Market Segmentation Analysis:

By Type / Therapy Type, Autologous Stem Cell Therapies are typically positioned around tissue repair and regenerative aims, with adoption influenced by evidence strength, regulatory clarity, and standardization of collection and processing. Autologous Non-Stem Cell Therapies are more strongly associated with immune-cell modalities, particularly where patient-specific cell preparation supports targeted disease management. Other Therapy Types often include niche or hybrid approaches that vary widely by region and clinical setting, which can make comparability across markets uneven.

By Application / Indication, Cancer / Oncology is generally the most commercially established segment due to defined treatment protocols and clearer reimbursement routes in many markets. Cardiovascular Diseases, Neurodegenerative Disorders / Neurology, Orthopedic / Musculoskeletal Conditions, and Dermatological / Skin Disorders are often more fragmented, reflecting variable trial maturity and heterogeneous patient populations. Other Applications / Indications capture smaller, emerging uses where evidence is still developing.

By End User, Hospitals and Clinics lead for complex therapies requiring multidisciplinary care, while Specialized Therapy Clinics and Cell Therapy Centers support higher procedure focus and workflow expertise. Research Institutes and Research Facilities drive trial activity and translational development, and Ambulatory Surgical Centers participate mainly where procedures and monitoring requirements are less intensive.

Segmentation:

By Type / Therapy Type

- Autologous Stem Cell Therapies

- Autologous Non-Stem Cell Therapies

- Other Therapy Types

By Application / Indication

- Cancer / Oncology

- Cardiovascular Diseases

- Neurodegenerative Disorders / Neurology

- Orthopedic / Musculoskeletal Conditions

- Dermatological / Skin Disorders

- Other Applications / Indications

By End User

- Hospitals and Clinics

- Research Institutes and Research Facilities

- Specialized Therapy Clinics and Cell Therapy Centers

- Ambulatory Surgical Centers

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

Regionally, North America (~42% share) leads the autologous stem cell and non-stem cell based therapies market, supported by a high concentration of specialized treatment centers, mature clinical trial infrastructure, and earlier integration of personalized cell therapies into oncology pathways. Europe (~28% share) follows, where adoption is shaped by strong academic networks and standardized protocols, but uptake can be paced by country-level health technology assessment and budgeting in public systems.

Asia-Pacific (~24% share) represents the fastest-moving expansion opportunity, driven by improving healthcare infrastructure, rising investment in advanced therapies, and growing participation in clinical research across major markets such as China and Japan. While oncology remains a key anchor, capacity build-out in cell processing and trained-site readiness is a practical limiter in parts of the region, creating uneven penetration between tier-1 and tier-2 cities.

Rest of the World (~5% share) remains earlier-stage, with demand concentrated in a limited number of private or specialized centers and constrained by reimbursement coverage, logistics capability, and availability of trained multidisciplinary teams.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Vericel Corporation

- BrainStorm Cell Therapeutics

- Cytori Therapeutics

- Fibrocell Science, Inc.

- Genzyme Corporation

- Caladrius Biosciences

- Regeneus Ltd.

- Dendreon Corporation

- Gilead Sciences

- Novartis

- Johnson & Johnson

- Bristol-Myers Squibb Company

Competitive Analysis:

Competition is defined by a mix of large biopharma leaders in autologous cell therapies and smaller specialists in regenerative or niche autologous modalities. Key named participants commonly cited for this market include Novartis and Gilead Sciences, alongside companies such as Dendreon Pharmaceuticals, Vericel, BrainStorm Cell, Cytori Therapeutics, Castle Creek Biosciences, Holostem SRL, Lisata Therapeutics, and U.S. Stem Cell. Differentiation is increasingly operational: reliable chain-of-identity, manufacturing success rates, and time-to-treat performance can influence center preference and capacity allocation. In oncology-focused autologous therapies, product leaders also compete on clinical durability, safety management, and label expansion strategies, with CAR-T representing a large share of the broader autologous therapy landscape in some assessments. Partnerships with CDMOs, automation providers, and treatment-center networks are common levers to expand access and stabilize supply.

Recent Developments:

- In Feb 2026, Eli Lilly and Company entered into a definitive agreement to acquire Orna Therapeutics to advance cell therapies. In the same announcement, Lilly said Orna’s lead program (ORN-252) is a clinical trial–ready, CD19-targeting in vivo CAR‑T therapy designed to treat B cell–driven autoimmune diseases, and that Orna shareholders could receive up to $2.4 billion in cash.

- In January 2026, Vericel Corporation reported business updates including initiation of the MACI Ankle™ MASCOT clinical study and continued expansion activities around MACI

- In April 2025, Cellino announced a strategic collaboration with Karis Bio aimed at industrializing a clinical-stage autologous induced pluripotent stem cell (iPSC)–derived cell therapy for peripheral artery disease and coronary artery disease.

- In June 2025, STEMCELL Technologies announced the acquisition of Cellular Highways Ltd (from TTP Group Ltd), a company focused on advanced cell sorting technologies used in cell and gene therapy workflows.

Report Coverage:

The research report offers an in-depth analysis based on Therapy Type, Application / Indication, and End User. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.