Automated Ophthalmic Perimeters Market Overview:

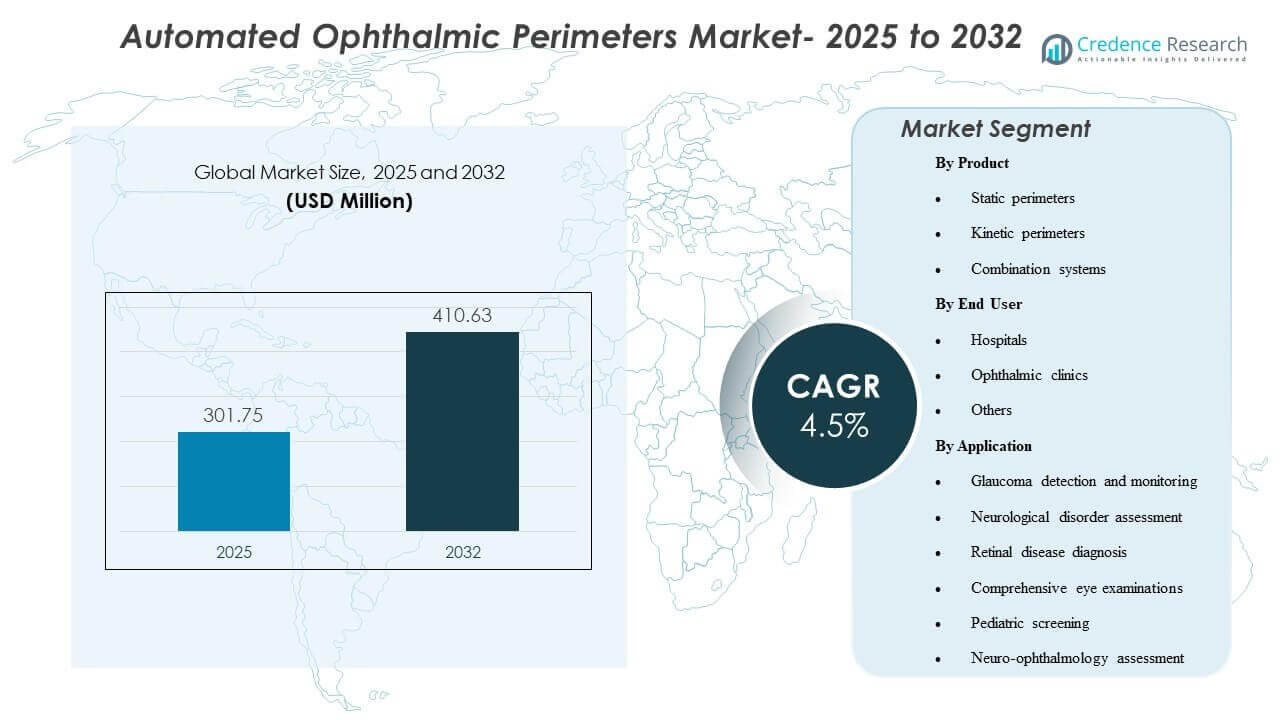

The global Automated Ophthalmic Perimeters Market size was valued at USD 301.75 million in 2025 and is expected to reach USD 410.63 million by 2032, growing at a CAGR of 4.5% from 2025 to 2032. Demand is primarily driven by the rising clinical need for reliable functional vision assessment in glaucoma care, where repeatable visual field testing supports earlier detection and tighter progression monitoring. Growth is further supported by modernization of ophthalmic diagnostic workflows, including faster test strategies, improved patient comfort, and broader adoption across specialty eye-care settings.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Automated Ophthalmic Perimeters Market Size 2025 |

USD 301.75 million |

| Automated Ophthalmic Perimeters Market, CAGR |

4.5% |

| Automated Ophthalmic Perimeters Market Size 2032 |

USD 410.63 million |

Key Market Trends & Insights

- The Automated Ophthalmic Perimeters Market is projected to grow from USD 301.75 million in 2025 to USD 410.63 million by 2032 at a CAGR of 4.5% (2025–2032).

- Static perimeters accounted for the largest product share of 37.6% in 2025, reflecting their central role in routine visual field testing pathways.

- Ophthalmic clinics accounted for the largest end-user share of 54.3% in 2025, supported by higher test throughput and dedicated glaucoma monitoring workflows.

- Glaucoma detection and monitoring accounted for the largest application share of 58.1% in 2025, reinforcing glaucoma as the dominant utilization driver for automated perimetry.

- Combination systems are increasingly positioned for broader clinical coverage as clinics seek to consolidate static and kinetic capabilities within single-platform workflows in the 2025–2032 forecast window.

Segment Analysis

Product and workflow preferences continue to shift toward solutions that reduce test time and improve repeatability without sacrificing diagnostic confidence. Faster thresholding strategies and software-led progression tracking are influencing upgrade decisions, particularly in high-volume settings that balance physician time, technician capacity, and patient tolerance. In parallel, device vendors are strengthening connectivity and analytics layers to improve longitudinal monitoring, which elevates the importance of consistent test protocols and data comparability across visits.

Adoption dynamics also reflect the growing emphasis on space efficiency and deployment flexibility in outpatient environments. Compact formats and alternative form factors are gaining interest in screening-oriented workflows and sites that lack dedicated dark rooms or large diagnostic suites. As clinics standardize glaucoma pathways and expand neuro-ophthalmic assessment capabilities, purchasing decisions increasingly weigh patient experience, workflow integration, and service support alongside core test performance.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Insights

Static perimeters accounted for the largest share of 37.6% in 2025. Static testing remains the most routinely deployed modality for glaucoma detection and longitudinal follow-up, supported by established clinical protocols and comparability across repeat visits. Workflow optimization is a key factor, as faster testing approaches and refined algorithms help clinics improve throughput and reduce patient fatigue. Static platforms also benefit from strong integration with progression analysis tools, which reinforces repeat utilization and replacement demand in practices focused on chronic disease management.

By End User Insights

Ophthalmic clinics accounted for the largest share of 54.3% in 2025. Specialty clinics typically run higher perimetry volumes per device due to concentrated glaucoma caseloads and structured follow-up schedules. These settings are more likely to invest in advanced perimetry features that support standardized testing, progression monitoring, and streamlined technician workflows. Clinics also benefit from tighter operational control over scheduling and testing protocols, which helps sustain utilization rates and supports faster refresh cycles compared to broader hospital-based deployment.

By Application Insights

Glaucoma detection and monitoring accounted for the largest share of 58.1% in 2025. Automated perimetry is widely used to identify functional field loss and track progression over time, making glaucoma the most consistent and repeat-driven application category. Ongoing monitoring requirements create recurring testing demand, especially for patients on treatment pathways that require longitudinal evaluation. The clinical importance of early detection and progression tracking further supports technology upgrades that improve reproducibility, reduce test time, and strengthen clinician confidence in trend interpretation.

Automated Ophthalmic Perimeters Market Drivers

Rising Glaucoma Case Management and Longitudinal Monitoring Needs

Glaucoma care relies heavily on repeatable functional testing to confirm progression and guide therapy adjustments. Automated perimetry supports standardized protocols that enable comparisons across visits, which increases routine testing volumes in clinical practice. As clinicians aim to intervene earlier, demand grows for tools that detect subtle functional changes and support confident decision-making. This reinforces replacement cycles and upgrades toward platforms that deliver consistent outputs and progression-ready analytics.

- For instance, iCare states that its COMPASS perimeter captures retinal images 25 times per second for active retinal tracking, while a clinical evaluation reported that its 95% limits of agreement in the central 10 degrees were about 20% narrower than Humphrey Field Analyzer, which supports more stable long-term follow-up.

Workflow Efficiency Improvements in Ophthalmic Diagnostics

Clinics and hospitals increasingly prioritize throughput and patient experience in diagnostic testing. Perimetry systems that reduce testing time and simplify setup can expand daily test capacity and improve patient compliance. Software enhancements that reduce technician burden and streamline interpretation also increase utilization intensity. Over time, workflow gains become a primary economic justification for upgrading devices beyond base functionality.

- For instance, ZEISS says Humphrey Field Analyzer 3 with SITA Faster 24-2 is approximately 50% faster than SITA Standard and about 30% quicker than SITA Fast while offering the same reproducibility.

Expansion of Specialty Eye-Care Networks and Outpatient Testing Capacity

Growth in ophthalmic clinics and specialty eye-care chains increases demand for standardized diagnostic equipment across multiple sites. Network operators tend to favor consistent test methodologies and centralized data practices that support clinical governance. Automated perimetry becomes a core diagnostic asset in these settings due to recurring glaucoma monitoring demand. This structural shift supports sustained placement growth, particularly in high-volume outpatient environments.

Broader Use in Neuro-Ophthalmic and Multi-Condition Assessment

Beyond glaucoma, perimetry contributes to evaluation of neurological disorders, neuro-ophthalmology conditions, and broader clinical assessments. As referrals rise for complex cases, clinics seek flexible platforms capable of supporting diverse testing needs. Combination capability and improved analytics support broader case mix handling without fragmenting workflows across multiple instruments. This expands addressable demand beyond single-indication purchasing behavior.

Automated Ophthalmic Perimeters Market Challenges

Automated perimetry adoption is constrained by patient cooperation requirements and test variability driven by fatigue, attention, and learning effects. These factors can increase repeat testing needs and complicate progression interpretation in borderline cases. Clinics must invest in technician training and standardized protocols to ensure consistency, which adds operational overhead. Variability concerns can slow adoption of newer form factors until confidence in repeatability is well established.

- For instance, Carl Zeiss Meditec states that its Humphrey Field Analyzer 3 with SITA Faster 24-2 is approximately 50% faster than SITA Standard and about 30% quicker than SITA Fast while offering the same reproducibility, a measurable improvement aimed at reducing fatigue-related variability during threshold testing.

Cost sensitivity remains a barrier in settings with limited diagnostic budgets, particularly outside major urban centers. Purchase decisions often compete with other ophthalmic imaging priorities, which can delay replacement cycles for perimetry systems that remain operational. Service availability and calibration needs also influence lifecycle economics, especially for multi-site networks. As a result, vendors must balance advanced feature sets with clear workflow and clinical value articulation.

Automated Ophthalmic Perimeters Market Trends and Opportunities

Technology differentiation is increasingly centered on faster test strategies, improved patient comfort, and software-supported progression monitoring. Platforms that integrate data management, interpretation support, and longitudinal tracking can strengthen clinical confidence and reduce time-to-decision. This trend supports opportunities in workflow-integrated ecosystems, where perimetry becomes part of a connected glaucoma management pathway. Vendors that align product design to standardized clinic operations are well positioned to capture upgrades and multi-site deployments.

Alternative form factors and compact deployment models are expanding access in space-constrained environments and screening-oriented workflows. Solutions that reduce room dependency and simplify installation can unlock incremental demand in outpatient sites and emerging markets. The opportunity is strongest where growing specialty clinic footprints and rising chronic eye disease burdens increase testing volumes. Over the forecast period, flexible deployment combined with consistent test outputs can broaden adoption beyond traditional instrument-room settings.

- For instance, CREWT Medical states that its portable IMOvifa smart perimeter does not require a dark room and reduces glaucomatous-eye test time from 7 minutes 24 seconds with conventional SAP to 5 minutes 40 seconds with its AIZE algorithm.

Regional Insights

North America (34.7%)

North America remains a leading region for automated perimetry adoption, supported by mature ophthalmology infrastructure and high utilization in glaucoma monitoring pathways. Specialty clinics and multi-physician practices drive demand for workflow-efficient systems that support standardized testing and progression tracking. Replacement demand is reinforced by expectations for integrated software workflows and reliable service coverage.

Europe (22.9%)

Europe shows strong demand anchored in established glaucoma care protocols and broad access to specialty ophthalmology services in major markets. Purchasing decisions emphasize clinical reliability, reproducibility, and integration into routine outpatient workflows. Modernization of diagnostic suites supports steady replacement, particularly in high-volume clinics and hospital eye departments.

Asia Pacific (26.4%)

Asia Pacific is supported by expanding eye-care access, rising chronic disease burden, and ongoing investment in hospital and clinic diagnostic capacity. Growth in outpatient ophthalmology networks and earlier detection priorities reinforces demand for efficient perimetry workflows. Large-population markets increase testing volumes, raising the importance of faster protocols and scalable deployment.

Latin America (7.8%)

Latin America demand is led by private ophthalmology groups and larger urban hospitals investing in core diagnostic platforms. Adoption is supported by gradual modernization of eye-care services, although budget constraints can extend replacement cycles. Vendor service footprint and training support remain key purchase criteria to maintain consistent testing protocols.

Middle East & Africa (8.2%)

Middle East & Africa adoption is driven by investments in specialty care capacity, particularly in higher-spend markets with expanding hospital networks and private clinics. Diagnostic infrastructure growth and rising focus on chronic eye disease management support demand. Underpenetration in several subregions creates longer-term potential, but access variability can limit near-term growth.

Competitive Landscape

Competition in automated ophthalmic perimeters is shaped by product performance consistency, workflow efficiency, and software capabilities that support progression monitoring and interpretation confidence. Vendors differentiate through faster test strategies, platform reliability, connectivity, and integration into broader ophthalmic diagnostic workflows. Service coverage, training support, and installed-base upgrade paths influence buyer decisions, particularly among multi-site clinic networks. Product portfolios that address both routine glaucoma monitoring and broader neuro-ophthalmic assessment needs strengthen competitive positioning.

Carl Zeiss Meditec / ZEISS International is widely recognized for emphasizing integrated perimetry workflows aligned to glaucoma management, combining test strategy performance with software-enabled longitudinal analysis. The company’s approach commonly focuses on clinical repeatability, progression tracking, and interoperability with complementary ophthalmic diagnostics. This positioning supports adoption in high-volume glaucoma practices that value standardized testing and consistent longitudinal outputs. Continuous enhancements across software and workflow elements reinforce differentiation beyond hardware specifications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Carl Zeiss Meditec / ZEISS International

- HAAG-STREIT GROUP

- Medmont

- OPTOPOL Technology Sp. z o.o.

- NIDEK Co., Ltd.

- OCULUS Optikgeräte GmbH / OCULUS, Inc.

- Kowa American Corporation

- Metrovision SA

- Heidelberg Engineering GmbH

- Canon Inc.

- Konan Medical, Inc.

- Topcon Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In October 2025, NIDEK Inc. announced U.S. distribution of the Medmont Meridia Vantage, describing the arrangement as a partnership that brings Medmont’s imaging technology together with NIDEK’s established sales and service infrastructure. For the automated ophthalmic perimeters market, this matters because it reinforces NIDEK’s position as a broader ophthalmic diagnostics supplier to eye-care practices.

- In August 2024, OCULUS launched Frequency Doubling Perimetry as a new capability within its Easyfield VR Virtual Reality Visual Field Analyzer & Screener. This update is directly relevant to the automated ophthalmic perimeters market because the source says FDP can help detect glaucomatous damage and other optic nerve diseases earlier than standard automated perimetry

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 301.75 million |

| Revenue forecast in 2032 |

USD 410.63 million |

| Growth rate (CAGR) |

4.5% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Outlook: Static perimeters, Kinetic perimeters, Combination systems; By End User Outlook: Hospitals, Ophthalmic clinics, Others; By Application Outlook: Glaucoma detection and monitoring, Neurological disorder assessment, Retinal disease diagnosis, Comprehensive eye examinations, Pediatric screening, Neuro-ophthalmology assessment |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Carl Zeiss Meditec / ZEISS International; HAAG-STREIT GROUP; Medmont; OPTOPOL Technology Sp. z o.o.; NIDEK Co., Ltd.; OCULUS Optikgeräte GmbH / OCULUS, Inc.; Kowa American Corporation; Metrovision SA; Heidelberg Engineering GmbH; Canon Inc.; Konan Medical, Inc.; Topcon Corporation |

| No. of Pages |

320 |

By Segmentation

By Product

- Static perimeters

- Kinetic perimeters

- Combination systems

By End User

- Hospitals

- Ophthalmic clinics

- Others

By Application

- Glaucoma detection and monitoring

- Neurological disorder assessment

- Retinal disease diagnosis

- Comprehensive eye examinations

- Pediatric screening

- Neuro-ophthalmology assessment

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa