Autosamplers Market Overview

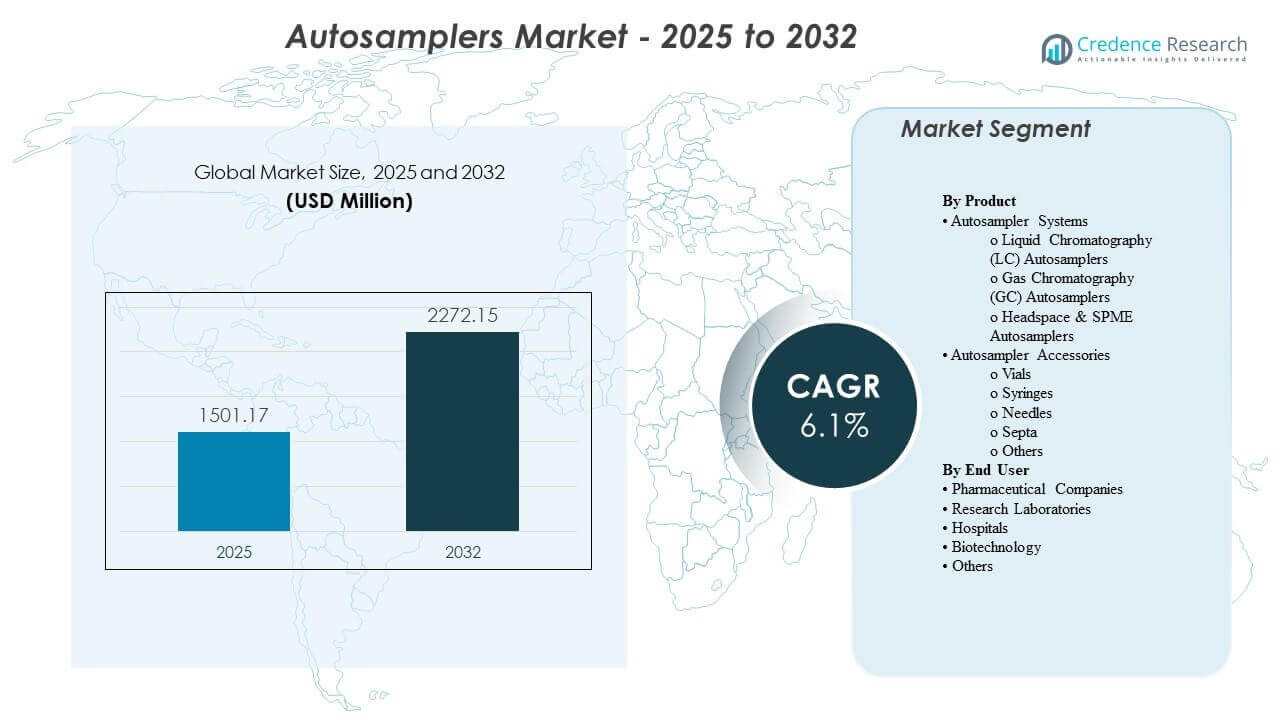

The global Autosamplers market size was estimated at USD 1501.17 million in 2025 and is expected to reach USD 2272.15 million by 2032, growing at a CAGR of 6.1% from 2025 to 2032. Growth is primarily driven by rising demand for automated, high-throughput analytical workflows in regulated environments where repeatability, traceability, and unattended operation are critical. Expanding pharmaceutical manufacturing, broader adoption of chromatography across quality control and R&D, and increasing test volumes in food, environmental, and clinical laboratories continue to support steady market expansion.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Autosamplers Market Size 2024 |

USD 1501.17 million |

| Autosamplers Market, CAGR |

6.1% |

| Autosamplers Market Size 2032 |

USD 2272.15 million |

Key Market Trends & Insights

- The Autosamplers Market is projected to expand at a CAGR of 6.1% from 2025 to 2032, reflecting sustained automation investments across analytical labs.

- Autosampler Systems accounted for the largest share of 58.6%, supported by continuous replacement demand and upgrades tied to chromatography platform refresh cycles.

- Pharmaceutical and biopharmaceutical end users represented 44.53% of demand, driven by method validation needs, compliance requirements, and high daily sample loads.

- North America held 37.2% of global revenue, supported by a dense installed base of analytical instruments and strong spending on regulated testing.

- Europe captured 26.41% share, reflecting mature pharma, chemicals, and food testing ecosystems that sustain consistent autosampler utilization.

Segment Analysis

Autosamplers Market demand is shaped by the need to increase throughput, reduce operator-to-operator variability, and standardize injection and sample handling performance across routine and complex workflows. Labs increasingly prioritize autosamplers that integrate seamlessly with chromatography stacks, provide higher sample capacity, and support reliable, unattended overnight operation to maximize instrument utilization. Replacement cycles are also influenced by lab digitization initiatives that favor standardized hardware-software ecosystems, enabling easier method transfer and consistent performance across multiple sites.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Buyer behavior increasingly reflects a lifecycle-cost mindset rather than a one-time equipment purchase approach. Service contracts can represent up to 35% of lifecycle spend for large installed bases, encouraging buyers to prioritize vendors with strong field service coverage, predictable maintenance programs, and parts availability. Remote diagnostics capabilities can reduce on-site visits by up to 40%, improving uptime and accelerating troubleshooting, which is particularly important for QC labs operating under tight release schedules. These factors reinforce demand for reliable systems and bundled service offerings.

By Product Insights

Autosampler Systems accounted for the largest share of 58.6%. Leadership is supported by sustained demand for automated injection and sample handling across LC, GC, and headspace workflows where repeatability and throughput directly impact laboratory productivity. System upgrades are also driven by higher sample capacity requirements and tighter integration with instrument control software for audit-ready data capture. Replacement demand remains consistent as laboratories modernize chromatography platforms and standardize configurations across sites.

By End User Insights

Pharmaceutical and biopharmaceutical companies accounted for the largest share of 44.53%. Dominance is driven by high-volume QC testing, method validation routines, and strict compliance requirements that reward automation and consistent performance. Pharma labs prioritize autosamplers that reduce manual handling, minimize injection variability, and support unattended sequencing for continuous operation. Ongoing expansion of manufacturing and analytical testing capacity further sustains demand for robust autosampler deployments.

Autosamplers Market Drivers

Rising throughput requirements in regulated analytical testing

Pharmaceutical quality control and regulated testing environments increasingly require high sample throughput to meet release timelines and compliance expectations. Autosamplers enable unattended sequencing, consistent injections, and repeatable handling that reduce variability across operators and shifts. Automated sampling also supports better traceability and structured run documentation, which aligns with audit readiness needs. As test volumes rise, labs invest in autosampling to maximize instrument utilization and minimize downtime between runs.

- For instance, Thermo Scientific’s Vanquish Split Sampler (HT/FT) lists an injection cycle time “down to 8 s,” injection volume precision of “<0.25% area RSD” at 1 µL (caffeine in water), and minimum sample required of 2 µL at a 1 µL injection volume—capabilities that directly support high-throughput, unattended sequences in regulated environments.

Expansion of chromatography applications across industries

Chromatography continues to be widely used across pharmaceuticals, biotechnology, chemicals, food testing, and environmental analysis. Autosamplers help labs handle diverse sample matrices with consistent injection performance, improving repeatability across methods and instruments. Broader application coverage increases demand for configurable systems that support different vial formats, volumes, and temperature needs. This cross-industry adoption strengthens baseline demand beyond pharma-centric testing.

- For instance, Waters’ ACQUITY UPLC I‑Class PLUS Sample Manager‑FTN specifies a sample-compartment temperature range of 4.0 to 40.0 °C (settable in 0.1 °C increments), a cool time of ≤60 min from ambient to 4 °C, and an injection volume range of 0.1 to 10.0 µL as standard (up to 1000.0 µL with an optional extension loop), supporting broader method needs across industries.

Productivity gains and reduced manual error risk

Manual sampling introduces risk of inconsistent injections, handling errors, and bottlenecks in high-volume workflows. Autosamplers reduce repetitive manual steps and improve run-to-run consistency, supporting stronger reproducibility in routine analysis. Laboratories value automation that improves staff efficiency and allows analysts to focus on higher-value tasks like method development and data interpretation. These productivity benefits remain a core purchase driver, especially for multi-instrument labs.

Service-led procurement and uptime-focused purchasing

Many buyers evaluate autosamplers based on total cost of ownership, service responsiveness, and uptime performance rather than hardware specifications alone. Service contracts form a meaningful share of lifecycle spending, influencing vendor preference toward established support ecosystems and predictable maintenance programs. Remote monitoring and diagnostics reduce troubleshooting time and help prevent unplanned downtime. This shift supports stronger demand for vendors that bundle service, software, and hardware into cohesive support models.

Autosamplers Market Challenges

Autosamplers Market adoption can be constrained by high upfront costs for advanced configurations, particularly for smaller laboratories with limited capital budgets. In some environments, legacy instrument compatibility and software integration complexity slow upgrades and increase implementation timelines. Validation and change-control requirements can also extend deployment cycles in regulated labs, delaying replacement decisions even when productivity gains are clear. Procurement processes may prioritize lowest initial cost, which can limit adoption of higher-end systems despite lifecycle benefits.

Operational challenges also arise from the need to maintain consistent performance across diverse sample matrices and varying laboratory conditions. Consumables and accessory selection can impact reliability and carry recurring costs that buyers closely scrutinize. Training and standard operating procedure alignment across sites can be difficult for multi-location organizations, especially during instrument standardization programs. Supply-chain variability for parts and service availability in certain geographies can further influence vendor selection and installed base expansion.

- For instance, Shimadzu’s Nexera SIL-40C lists a cycle time of ≤ 7 seconds, carryover performance of 0.0005% with rinse (and 0.0025% with no needle rinsing), temperature control from 4 to 45°C with ±2°C accuracy, and scalability to 16,000+ samples on a single system using up to three plate changers—attributes that increase the operational importance of harmonized consumables, consistent SOPs, and dependable local service logistics.

Autosamplers Market Trends and Opportunities

Labs are increasingly standardizing automation stacks that combine instruments, autosamplers, and software into unified workflows to improve repeatability and simplify method transfer. This trend supports demand for integrated ecosystems, centralized monitoring, and configurable autosampling platforms tailored to different chromatography workflows. Growth in high-throughput testing environments is also accelerating demand for higher-capacity samplers designed for extended unattended runs. Vendors that simplify usability and integration are well-positioned to benefit from these shifts.

- For instance, Agilent states its 1290 Infinity III Multisampler is rated up to 1300 bar and can load up to 16 microtiter plates (up to 6,144 samples), with internal robotics that move microtiter plates and other sample containers from the sample hotel to a central workspace for processing steps and injections.

Service modernization is creating opportunity in remote diagnostics, predictive maintenance, and faster parts logistics. Buyers increasingly prioritize uptime, making service differentiation a competitive lever that can influence long-term customer retention. There is also opportunity in expanding autosampler penetration into emerging lab markets where testing capacity is growing in food safety, environmental monitoring, and clinical diagnostics. Vendors that offer scalable configurations and strong local support networks can capture incremental demand in these areas.

Regional Insights

North America

North America held the largest share of 37.2% of global revenue, supported by high instrument density and strong demand from regulated pharmaceutical testing. The region benefits from a mature ecosystem of analytical laboratories, robust R&D activity, and broad adoption of lab automation to improve productivity. Established service networks and replacement demand from large installed bases further support steady purchasing.

Europe

Europe represented 26.41% of revenue, driven by mature pharmaceutical manufacturing, chemicals testing, and established food safety frameworks. The region’s demand is supported by consistent instrument utilization across QC and R&D labs, along with ongoing modernization programs focused on standardization and compliance. Procurement tends to emphasize reliability and lifecycle support, reinforcing demand for established vendor platforms.

Asia Pacific

Asia Pacific accounted for 24.87% share, supported by expanding pharmaceutical manufacturing and growing analytical testing volumes across multiple industries. Adoption is strengthened by investment in lab infrastructure and increasing focus on throughput and quality compliance. Price sensitivity can be higher in parts of the region, but rising automation penetration and expanding capacity continue to lift demand.

Latin America

Latin America contributed 6.76% of revenue, supported by growing testing activity in pharmaceuticals, food, and environmental monitoring. Market expansion is influenced by laboratory modernization initiatives and gradual increases in automation budgets, particularly in larger urban and industrial centers. Demand remains smaller than North America and Europe due to a lower installed base and uneven lab infrastructure.

Middle East & Africa

Middle East & Africa held 5.04% share, with demand concentrated in pockets where industrial testing, food safety, and healthcare lab capacity are expanding. Growth is supported by modernization of laboratory services and gradual adoption of automated workflows in key hubs. Vendor reach and service availability can influence purchasing decisions, making distribution and support capabilities important competitive factors.

Competitive Landscape

Competition in the Autosamplers Market centers on breadth of autosampling coverage across LC, GC, and headspace workflows, alongside software integration that improves usability and compliance readiness. Vendors differentiate through reliability, higher sample capacity, modular accessory ecosystems, and service-led offerings that reduce downtime. Platform compatibility with chromatography stacks and strong field support remain important factors that influence replacement and standardization programs. Commercial strategies often combine instrument bundling, multi-year service agreements, and application support to deepen customer retention.

Agilent Technologies maintains a strong position through deep chromatography integration, broad autosampler configurations, and a focus on workflow reliability for regulated and high-throughput labs. The company emphasizes system-level optimization that improves repeatability and reduces manual handling, aligning with QC and R&D productivity goals. Ongoing portfolio upgrades and support programs reinforce adoption among customers that standardize analytical platforms across sites. Service strength and compatibility across instrument families further support long-term account retention.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies

- Waters Corporation

- Shimadzu Corporation

- Thermo Fisher Scientific

- PerkinElmer

- Merck

- Bio-Rad Laboratories

- Restek

- Gilson

- JASCO

- SCION Instruments

- CTC Analytics

- GERSTEL

- Tecan Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, Shimadzu announced that it had released the PL-40 Automation-Compatible Plate Loader for LC/LC-MS systems. Shimadzu positioned PL-40 as addressing the bottleneck of manually loading pretreated plates into instruments, enabling a more fully automated workflow from pretreatment to analysis.

- In February 2026, Shimadzu Scientific Instruments published details for its SIL-40/SIL-40C HPLC autosamplers, describing configurations that can be paired with up to three plate changers and scaled to very high sample capacity. The same product information highlights features such as a needle-in-flowpath design to minimize carryover and (for SIL-40C) cooled temperature control intended to protect thermally sensitive samples.

- In June 2025, Agilent Technologies announced it would introduce its 1290 Infinity III Hybrid Multisampler at the HPLC 2025 conference in Bruges, Belgium. In the same announcement, Agilent described the multisampler as supporting both traditional flow-through injection and Feed Injection Mode to improve peak shapes and reduce sample-prep needs in LC workflows.

- In May 2025, Hypha Labs, Inc. entered a strategic partnership with Lucidity Systems to obtain early access to Lucidity’s newly launched variable loop autosampler upgrade (as described in a market report’s “Recent Industry Developments”). The same note also mentions Hypha Labs acquiring a state-of-the-art HPLC machine as part of upgrading its analytical capabilities.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 1501.17 million |

| Revenue forecast in 2032 |

USD 2272.15 million |

| Growth rate (CAGR) |

6.1% |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Outlook: Autosampler Systems (Liquid Chromatography (LC) Autosamplers, Gas Chromatography (GC) Autosamplers, Headspace & SPME Autosamplers); Autosampler Accessories (Vials, Syringes, Needles, Septa, Others); By End User Outlook: Pharmaceutical Companies, Research Laboratories, Hospitals, Biotechnology, Others |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Agilent Technologies, Waters Corporation, Shimadzu Corporation, Thermo Fisher Scientific, PerkinElmer, Merck, Bio-Rad Laboratories, Restek, Gilson, JASCO, SCION Instruments, CTC Analytics, GERSTEL, Tecan Group |

| No. of Pages |

330 |

Segmentation

BY PRODUCT

- Autosampler Systems

- Liquid Chromatography (LC) Autosamplers

- Gas Chromatography (GC) Autosamplers

- Headspace & SPME Autosamplers

- Autosampler Accessories

- Vials

- Syringes

- Needles

- Septa

- Others

BY END USER

- Pharmaceutical Companies

- Research Laboratories

- Hospitals

- Biotechnology

- Others

BY REGION

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa