Base Editing Market Overview:

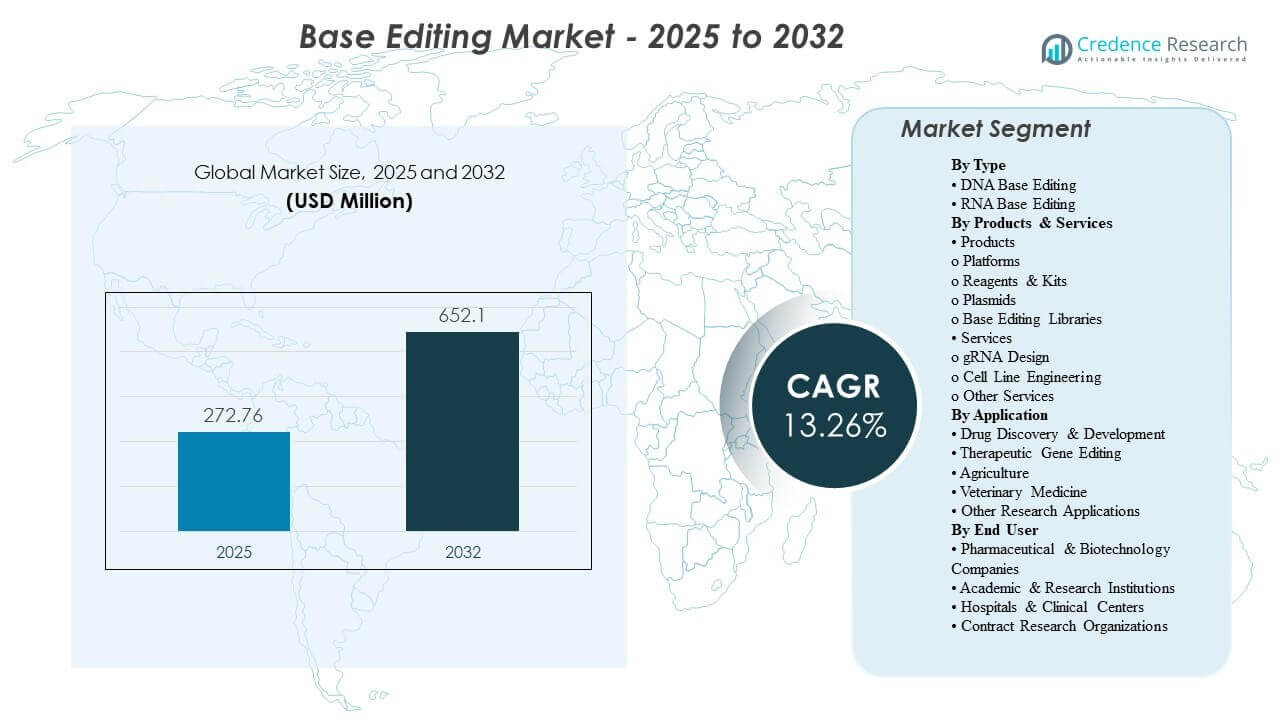

The global Base Editing Market size was estimated at USD 272.76 million in 2025 and is expected to reach USD 652.1 million by 2032, growing at a CAGR of 13.26% from 2025 to 2032. Expanding use of base editing in translational research and preclinical validation is strengthening demand for reliable editing systems, screening-ready libraries, and reproducible workflows that can be deployed across multiple targets and cell types. North America remains the largest revenue contributor, supported by deep biotech funding, advanced research infrastructure, and a dense ecosystem of genome engineering tool providers.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Base Editing Market Size 2025 |

USD 272.76 Million |

| Base Editing Market, CAGR |

13.26% |

| Base Editing Market Size 2032 |

USD 652.1 Million |

Key Market Trends & Insights

- North America accounted for 42.7% of Base Editing Market revenue in 2025, reflecting the highest concentration of advanced genome engineering programs and tool commercialization.

- Drug Discovery & Development held 50.9% share in 2025, driven by large-scale functional genomics, target validation, and disease-model creation demand.

- Pharmaceutical & Biotechnology Companies represented 52.4% share in 2025, supported by higher budgets for repeat experimentation, validation, and pipeline translation.

- The Base Editing Market is forecast to expand at 13.26% CAGR (2025–2032) as editing performance improves and adoption spreads from research into therapeutic development workflows.

- Market value increased from USD 272.76 million (2025) toward a projected USD 652.1million (2032), indicating accelerated scaling of platforms, reagents, and service ecosystems.

Segment Analysis

Base Editing Market adoption is advancing as organizations prioritize precise single-base changes for functional studies and candidate validation in early development. A meaningful portion of pathogenic single-nucleotide variants can be theoretically addressable through base editing approaches, which supports sustained interest in expanding editor libraries, optimizing guide design, and improving cell-type coverage. Demand also rises as research teams standardize assay pipelines and require consistent performance across multiple experimental contexts, strengthening recurring purchases of reagents, plasmids, and validated constructs.

Commercial activity increasingly connects tool providers, service specialists, and therapeutic developers across a shared workflow chain. Product ecosystems benefit from repeat usage patterns across screening, model development, and validation cycles, whereas services benefit from specialized expertise requirements in guide optimization, engineered cell lines, and custom workflows. As more programs move from exploratory studies toward translational proof points, stakeholders place higher weight on reproducibility, documentation, and workflow support.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Base Editing Market growth also reflects broader diversification of end-use settings. Biopharma demand remains central due to pipeline-driven purchasing and the need for scalable, quality-controlled inputs. Academic and research institutions contribute strongly through method development, discovery experimentation, and grant-funded programs that expand platform familiarity and workforce capability, supporting downstream adoption in commercial settings.

Type Insights

DNA Base Editing leads Base Editing Market adoption because DNA-level edits can create stable, heritable changes that support long-lived disease models and durable therapeutic hypotheses. DNA base editor toolchains also benefit from more established validation practices in many laboratories, enabling clearer benchmarking across targets and cell lines. RNA Base Editing continues to expand in specialized use cases where transient modulation, reduced permanent genomic alteration, or reversible study designs are preferred.

Products & Services Insights

Products lead Base Editing Market revenue because platforms, reagents, kits, plasmids, and libraries are repeatedly purchased across iterative screening and validation cycles. Standardized product formats reduce setup burden and enable faster onboarding for laboratories adding base editing to existing genome engineering stacks. Service demand rises in parallel as programs require expert guide design, engineered cell lines, and troubleshooting support to meet performance targets in complex biological systems.

Application Insights

Drug Discovery & Development accounted for the largest share of 50.9% in 2025. Drug Discovery & Development leads because base editing accelerates target validation and variant functionalization by enabling precise perturbations with efficient experimental throughput. Drug Discovery & Development also benefits from editor libraries that support broad screening programs across multiple targets and phenotypes. Drug Discovery & Development remains the most repeatable use case because discovery pipelines rely on recurring experimentation cycles that increase demand for consistent tools and workflow support.

End User Insights

Pharmaceutical & Biotechnology Companies accounted for the largest share of 52.4% in 2025. Pharmaceutical & Biotechnology Companies lead because pipeline-driven programs require sustained procurement of tools, reagents, and engineering capabilities across multiple stages of R&D. Pharmaceutical & Biotechnology Companies also prioritize reproducibility, QC discipline, and vendor support, which concentrates spending on validated product ecosystems. Pharmaceutical & Biotechnology Companies increasingly engage specialized partners for guide design and engineered models, further expanding spending across products and services.

Base Editing Market Drivers

Expanding use of precision editing in discovery workflows

Base Editing Market growth is supported by rising demand for accurate, scalable variant testing in discovery pipelines. Research teams use base editing to create precise point mutations that align closely with disease-relevant biology and mechanistic hypotheses. These workflows shorten iteration time versus broader perturbation methods, improving research efficiency and decision quality. Wider adoption in functional genomics increases recurring demand for standardized reagents, plasmids, and libraries.

Increasing translational focus across gene editing programs

More gene editing programs are moving beyond exploratory research toward translational validation and therapy-enabling evidence. Base Editing Market participants increasingly need tools that perform reliably across relevant cell types and disease models, which strengthens demand for optimized platforms and expert services. Program teams also require traceability and robust documentation to support downstream development activities. This shift increases purchasing intensity from biopharma stakeholders and accelerates ecosystem buildout.

Growth in enabling tool ecosystems and workflow standardization

Base Editing Market expansion benefits from improved availability of end-to-end solutions that integrate editor systems, guide design, and screening-ready libraries. Workflow standardization reduces technical friction and helps new users deploy base editing with higher success rates. Repeatable protocols also increase confidence in cross-lab reproducibility, which supports broader procurement and scale-up. As tool stacks mature, adoption extends into more research groups and more project types.

- For instance, Synthego reported that its ICE analysis platform produced results highly comparable with NGS at an r2 of 0.96, supported batch analysis of hundreds of samples, and reduced analysis cost by about 100-fold relative to NGS, illustrating how standardized tools can make editing workflows easier to scale and reproduce.

Rising demand for specialized engineering and outsourced expertise

Base Editing Market demand rises as organizations outsource portions of genome engineering workflows to accelerate timelines and reduce internal complexity. gRNA design, cell line engineering, and custom services reduce trial-and-error cycles for teams without deep in-house editing expertise. Outsourcing also supports parallelization of experiments across multiple targets, increasing throughput. This driver strengthens services revenue and expands partnerships between tool vendors and specialized providers.

- For instance, Revvity states that its Pin-point cell engineering services combine more than a decade of expertise across hundreds of cell types, and that its platform supports multiple edits in a single round through a fast-track multiplex editing workflow, which directly aligns with demand for outsourced, high-complexity engineering support.

Base Editing Market Challenges

Base Editing Market adoption continues to face performance variability across targets, delivery methods, and cell types, which can reduce reproducibility and extend optimization cycles. Differences in editing window behavior, bystander edits, and assay sensitivity can complicate interpretation and slow program progression. Many teams must invest in repeated validation to confirm functional outcomes, increasing cost and cycle time. These constraints can delay broader deployment in complex disease models and translational settings.

Base Editing Market scaling also faces operational constraints tied to quality expectations and documentation, especially for programs moving toward clinical relevance. Higher standards for traceability and process consistency can increase supplier qualification efforts and internal governance needs. Intellectual property complexity can influence platform selection and partnership structures. Talent and training gaps in advanced genome engineering further limit rapid expansion across smaller institutions and new adopters.

- For instance, Verve Therapeutics reported that VERVE-102 was well tolerated across 14 participants with no treatment-related serious adverse events and only one infusion-related reaction, and that every participant receiving at least 50 mg total RNA achieved more than 50% LDL-C reduction, with a mean reduction of 59% and a maximum reduction of 69%, underscoring the kind of delivery control and process consistency required for clinically relevant scale-up.

Market Trends and Opportunities

Base Editing Market innovation increasingly focuses on improving editing precision, efficiency, and compatibility with diverse delivery approaches. Tool providers are expanding editor variants and guide design frameworks to improve performance across genomic contexts and reduce off-target risk. Wider library availability supports high-throughput study designs, enabling faster hypothesis testing and better prioritization in discovery pipelines. These shifts expand the accessible user base and reinforce recurring product consumption patterns.

- For instance, Beam Therapeutics reported that its inlaid base editor for BEAM-102 achieved editing levels of over 70% in CD34+ cells from both sickle trait and sickle cell disease donors, and the company also disclosed PAM-expanded base editor variants that could potentially target up to 95% of all point mutations correctable with base editors.

Base Editing Market opportunity also grows as applications broaden beyond human therapeutics into agriculture and veterinary use cases where precise edits can improve traits and disease resilience. Organizations exploring non-traditional applications seek flexible platforms and partner support to navigate organism-specific constraints and validation methods. As research capacity expands in emerging regions, demand increases for standardized kits and service support. These factors collectively create growth headroom across both products and services.

Regional Insights

North America

North America held 42.7% share of the Base Editing Market in 2025, supported by dense biotech clusters, strong academic research output, and active commercialization of genome engineering tool stacks. North America demand benefits from high R&D intensity, established procurement pathways, and strong collaboration between tool suppliers and therapeutic developers. North America also leads in workflow standardization, which increases repeat purchasing of validated reagents and libraries.

Europe

Europe captured 27.1% share of the Base Editing Market in 2025, supported by strong academic networks, cross-border research programs, and expanding translational activity. Europe adoption is reinforced by structured research funding and growing interest in precision gene editing for disease modeling and early development. Europe also shows increasing demand for outsourced engineering services to accelerate programs within resource-constrained teams.

Asia Pacific

Asia Pacific represented 18.2% share of the Base Editing Market in 2025, reflecting expanding research capacity, improving lab infrastructure, and rising participation in genome engineering programs. Asia Pacific growth is supported by increasing numbers of biotechnology startups, broader availability of molecular biology inputs, and deeper training pipelines. Asia Pacific demand also benefits from expanding discovery work in both therapeutic and non-therapeutic applications.

Latin America

Latin America accounted for 7.6% share of the Base Editing Market in 2025, supported by gradual expansion of research institutions and increasing engagement with advanced life-science methods. Latin America adoption is often concentrated in leading academic centers and select biopharma initiatives. Latin America demand strengthens as standardized kits and service-based engagement reduce barriers for teams with limited in-house engineering capability.

Middle East & Africa

Middle East and Africa reached 4.4% share of the Base Editing Market in 2025, reflecting early-stage but improving research investment and infrastructure development. Middle East and Africa demand is growing through select national research initiatives and partnerships that expand access to advanced tools. Middle East and Africa adoption improves as training programs and service support reduce the complexity of deploying base editing workflows.

Competitive Landscape

Base Editing Market competition spans tool suppliers offering platforms, reagents, plasmids, and libraries, alongside service providers specializing in guide design and engineered models, and therapeutic developers integrating base editing into pipelines. Differentiation is shaped by editor performance, workflow reliability, documentation quality, delivery compatibility, and the ability to support customers from early discovery through validation. Partnerships and co-development agreements are used to accelerate adoption and expand use-case coverage. Product ecosystem breadth and repeat-use consumables remain key levers for revenue scaling.

Danaher Corporation participates in enabling infrastructure across life science and diagnostics, positioning Danaher Corporation to support base editing workflows through instruments, reagents, and adjacent laboratory solutions. Danaher Corporation benefits from channel scale and embedded customer relationships across research and applied settings. Danaher Corporation can also support standardization and quality expectations through integrated workflows that reduce variability and improve reproducibility for advanced molecular applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Danaher Corporation

- Beam Therapeutics

- Merck KGaA

- Revvity

- GenScript

- ElevateBio

- Maravai LifeSciences

- Intellia Therapeutics

- Cellectis

- Creative Biogene

- Bio Palette Co., Ltd.

- Addgene

- Synthego

- EdiGene

- Pairwise

- ProQR Therapeutics

- KromaTiD

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In October 2025, Bristol Myers Squibb announced a definitive agreement to acquire Orbital Therapeutics a key collaborator of Beam Therapeutics for $1.5 billion in cash. As part of this transaction, Beam Therapeutics, which held approximately 75 million shares (~17% fully diluted stake) in Orbital, converted those shares into $255.1 million in cash by December 8, 2025, with up to an additional $26.3 million possible.

- In July 2025, Beam Therapeutics entered into an Agreement and Plan of Merger to acquire an early-stage life sciences company, issuing 403,128 shares of its common stock as an upfront payment. The deal also included up to $89 million in potential milestone payments contingent on development, clinical, and commercial achievements, payable in cash or stock at Beam’s discretion.

- In February 2025, Maravai LifeSciences completed its acquisition of Officinae Bio’s DNA and RNA business, combining Officinae’s AI-enabled mRNA design platforms with Maravai and TriLink BioTechnologies’ manufacturing capabilities to support next-generation mRNA and CRISPR programs.

- In January 2025, Maravai LifeSciences also acquired intellectual property and relevant assets from Molecular Assemblies, expanding its ability to help customers develop next-generation mRNA and CRISPR nucleic acid-based therapies.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 272.76 million |

| Revenue forecast in 2032 |

USD 652.1million |

| Growth rate (CAGR) |

13.26% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

Type Outlook: DNA Base Editing; RNA Base Editing; Products & Services Outlook: Products (Platforms; Reagents & Kits; Plasmids; Base Editing Libraries); Services (gRNA Design; Cell Line Engineering; Other Services); Application Outlook: Drug Discovery & Development; Therapeutic Gene Editing; Agriculture; Veterinary Medicine; Other Research Applications; End User Outlook: Pharmaceutical & Biotechnology Companies; Academic & Research Institutions; Hospitals & Clinical Centers; Contract Research Organizations |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Danaher Corporation, Beam Therapeutics, Merck KGaA, Revvity, GenScript, ElevateBio, Maravai LifeSciences, Intellia Therapeutics, Cellectis, Creative Biogene, Bio Palette Co., Ltd., Addgene, Synthego, EdiGene, Pairwise, ProQR Therapeutics, KromaTiD |

| No. of Pages |

335 |

Segmentation

By Type

- DNA Base Editing

- RNA Base Editing

By Products & services

- Products

- Platforms

- Reagents & Kits

- Plasmids

- Base Editing Libraries

- Services

- gRNA Design

- Cell Line Engineering

- Other Services

By Application

- Drug Discovery & Development

- Therapeutic Gene Editing

- Agriculture

- Veterinary Medicine

- Other Research Applications

By End user

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutions

- Hospitals & Clinical Centers

- Contract Research Organizations

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa