Behavioral & Mental Health Software Market Overview:

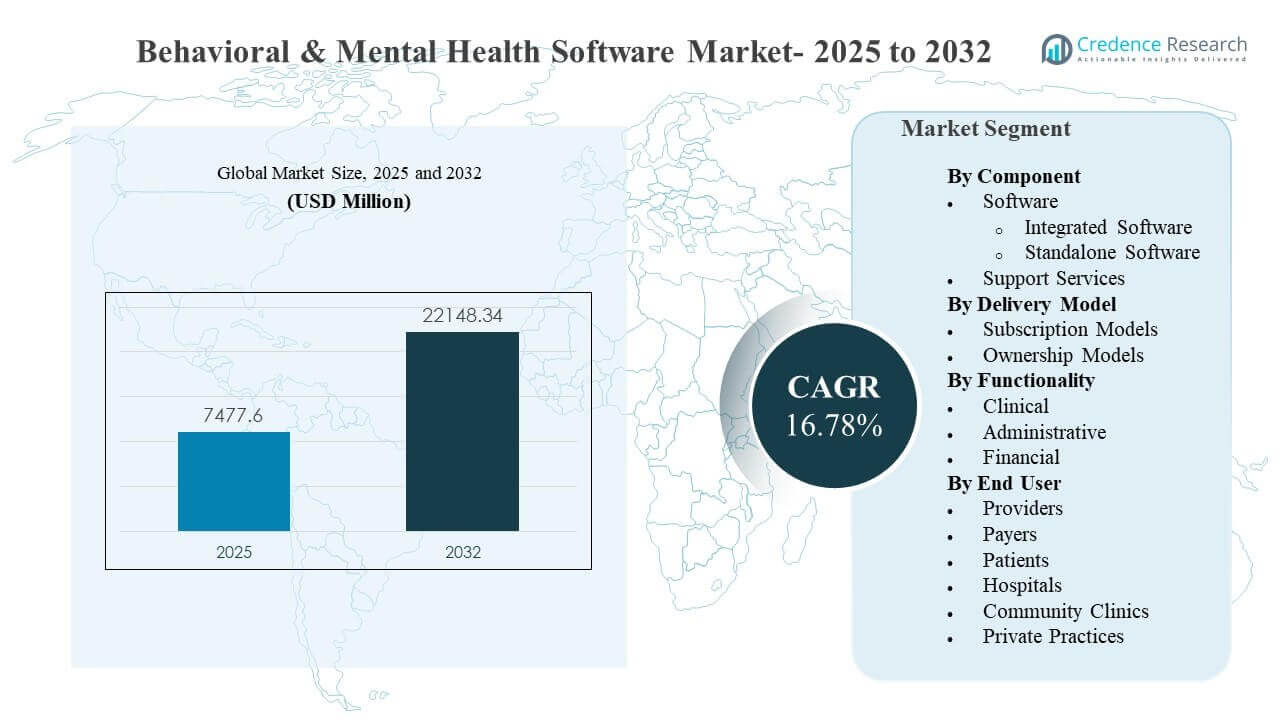

The global Behavioral & Mental Health Software Market size was estimated at USD 7,477.6 million in 2025 and is expected to reach USD 22,148.34 million by 2032, growing at a CAGR of 16.78% from 2025 to 2032. Growth is primarily driven by provider demand for digitized clinical workflows that reduce documentation burden, standardize care plans, and improve continuity of behavioral care across settings. Expansion of virtual care, payer emphasis on measurable outcomes, and broader enterprise modernization programs are accelerating platform adoption across hospitals, community clinics, and private practices.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Behavioral & Mental Health Software Market Size 2025 |

USD 7,477.6 million |

| Behavioral & Mental Health Software Market, CAGR |

16.78% |

| Behavioral & Mental Health Software Market Size 2032 |

USD 22,148.34 million |

Key Market Trends & Insights

- The market is projected to expand at a 16.78% CAGR (2025–2032), reflecting rapid modernization of behavioral care workflows across provider organizations.

- Software accounted for the largest share of 62.3% in 2025, supported by platform consolidation and demand for end-to-end capabilities across care and operations.

- Clinical functionality represented 55.1% share in 2025, indicating that clinical documentation, care plans, and treatment management remain the most monetized capability set.

- Hospitals held 41.9% share in 2025 among end users, reflecting enterprise purchasing power and multi-department integration needs.

- North America captured 40.7% share in 2025, indicating the largest installed base and strongest near-term spending intensity for behavioral software solutions.

Segment Analysis

Behavioral and mental health software buying is increasingly anchored around reducing clinician administrative load and improving patient access, which elevates demand for clinical documentation, measurement-based care, and integrated intake-to-billing workflows. Higher visit volumes, workforce shortages, and the scaling of virtual and hybrid care models push organizations toward platforms that unify clinical, administrative, and financial processes to minimize rework and handoffs.

Adoption patterns also reflect a widening customer mix, with large health systems prioritizing interoperability and enterprise analytics while smaller practices favor simpler deployments and predictable pricing. As implementation complexity rises with multi-site care networks and new care pathways, support services remain essential for onboarding, training, optimization, and workflow redesign. Over time, differentiation is shifting toward embedded intelligence, configurable workflows, and data-driven care management that strengthens both clinical outcomes and operational performance.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Component Insights

Software accounted for the largest share of 62.3% in 2025. Demand is concentrated in platforms that centralize behavioral documentation, care planning, and patient engagement in a single system to reduce fragmentation. Integrated solutions are preferred where organizations need consistent workflows across sites and service lines. Ongoing product updates and compliance-driven changes also support continued investment in core software platforms.

By Delivery Model Insights

Subscription models lead adoption due to predictable costs, faster deployment, and simplified upgrades that reduce internal IT burden. Subscription delivery aligns with the need for continuous workflow improvements and frequent feature releases as care models evolve. This model also supports multi-location standardization and centralized analytics without requiring large upfront investment. Ownership models persist in some environments where internal hosting and tighter control over infrastructure are prioritized.

By Functionality Insights

Clinical accounted for the largest share of 55.1% in 2025. Clinical modules drive day-to-day utilization, making them the primary value center for providers seeking standardized documentation and care delivery. Behavioral organizations prioritize tools that streamline progress notes, treatment plans, and evidence-based interventions across care teams. Clinical functionality also supports consistency in quality reporting and care coordination as organizations scale service delivery.

By End User Insights

Hospitals accounted for the largest share of 41.9% in 2025. Hospitals invest in behavioral software to integrate psychiatric services with broader clinical operations, standardize care pathways, and support multidisciplinary workflows. Enterprise purchasing also reflects needs for interoperability with other systems, reporting, and governance across departments. As hospitals expand outpatient and virtual behavioral programs, demand increases for platforms that support cross-setting continuity.

Behavioral & Mental Health Software Market Drivers

Expanding access needs and care pathway digitization

Behavioral care delivery is increasingly shifting toward scalable, standardized workflows that support faster intake, triage, and longitudinal management. Organizations invest in software to reduce manual processes and improve consistency across clinician teams and locations. Digitized documentation and structured care plans help increase throughput without sacrificing clinical quality. Platform-based delivery also enables better patient engagement, follow-up, and coordination across services. These factors collectively sustain demand for comprehensive behavioral software.

- For example, Eleos Health’s AI documentation layer enabled one network, ReachLink, to cut average note-writing time from 12.7 minutes to 7.3 minutes per session, a 42.5% reduction.

Provider operational pressure and workforce constraints

Clinician capacity constraints and administrative burden continue to pressure behavioral providers to modernize operations. Software helps reduce time spent on routine documentation, scheduling coordination, and manual communication with patients and referral partners. Better task automation and workflow standardization can improve staff utilization and reduce operational bottlenecks. As organizations face staffing variability and rising demand, efficiency-led purchasing remains a core growth driver. This pushes adoption across both enterprise systems and smaller practices.

Shift toward integrated clinical, administrative, and financial workflows

Behavioral organizations increasingly prefer solutions that connect clinical documentation to intake, billing, and revenue-cycle processes. Integrated workflows reduce duplication and improve data accuracy from the point of care through claims submission and reconciliation. This is especially important for multi-site providers managing high visit volumes across different payer rules and service configurations. Better linkage between clinical and financial data improves operational control and reporting. The result is sustained demand for integrated platforms.

Greater emphasis on measurable outcomes and analytics

Care models are increasingly influenced by outcomes tracking and performance reporting requirements across provider and payer environments. Software supports consistent capture of clinical metrics, care-plan compliance, and service utilization. Organizations use dashboards and analytics to identify gaps in access, adherence, and follow-up, improving both care quality and resource planning. This supports organizational initiatives around quality improvement and population health approaches in behavioral care. Stronger measurement expectations continue to expand software adoption.

- For instance, Lyra Health’s retrospective analyses show that each additional therapy session and each additional digital video lesson completed are independently associated with statistically significant decreases in standardized anxiety and depression scores across thousands of members.

Behavioral & Mental Health Software Market Challenges

Behavioral providers often operate with constrained IT resources, which can slow selection, implementation, and optimization of new platforms. Integration complexity rises when organizations must connect behavioral systems with broader clinical platforms, billing tools, and external reporting requirements. Workflow redesign requires clinician buy-in, and adoption can be uneven when teams are accustomed to legacy processes. Data migration and configuration effort can extend deployment timelines, delaying ROI realization.

- For instance, an EHR optimization study across 11 practices integrating behavioral health and primary care found that clinicians created multiple workarounds for behavioral templates, leading to inconsistent documentation in more than 30% of reviewed encounters until new standardized workflows were agreed and retrained.

Privacy, security, and regulatory requirements create additional friction, especially where multiple care settings and third-party services are involved. Maintaining consistent data governance across clinical documentation, patient engagement features, and analytics can be difficult. Smaller providers may struggle with change management, training, and process standardization, limiting the pace of full-feature adoption. These barriers can increase reliance on support services and lengthen sales and implementation cycles.

Behavioral & Mental Health Software Market Trends and Opportunities

Artificial intelligence and workflow automation are increasingly embedded into behavioral software to reduce clinician burden and improve documentation quality. Tools that streamline intake, triage, and follow-up are gaining attention because they directly address access and operational constraints. Platform providers are expanding configurable templates, structured assessments, and guided workflows that improve consistency across care teams. This trend creates opportunities for vendors that can combine usability with governance and auditability.

- For instance, GRAND Mental Health in Oklahoma reported saving more than 400 staff hours within six months of deploying an AI assistant that auto-completed over 80% of each progress note and reduced documentation time by more than 50% across its Certified Community Behavioral Health Clinic network.

Market opportunity is also expanding in underserved settings where digitization is still early-stage, including smaller practices and community clinics. Subscription-based delivery and modular platform design reduce barriers to adoption and enable stepwise capability expansion. As virtual and hybrid care models mature, demand rises for platforms that unify patient engagement, clinical workflows, and operational management across settings. Vendors that support interoperability and scalable analytics are positioned to benefit from these adoption shifts.

Regional Insights

North America

North America held the largest share at 40.7% in 2025, supported by a mature healthcare IT environment and strong demand for operational efficiency in behavioral care delivery. Provider organizations prioritize integrated platforms that connect clinical and administrative workflows across sites. Adoption is reinforced by ongoing modernization programs and a high focus on scalable access models, including virtual and hybrid care.

Europe

Europe represented 24.6% in 2025, reflecting continued investment in digitized care delivery and standardized documentation across healthcare systems. Providers increasingly seek tools that improve care coordination, reporting, and workflow consistency across multi-site service delivery. The market also benefits from initiatives aimed at improving access and quality measurement in behavioral health services.

Asia Pacific

Asia Pacific accounted for 22.4% in 2025, driven by growing digital health adoption and expanding behavioral care needs across diverse healthcare settings. Organizations prioritize scalable software deployment and operational streamlining as service demand rises. Opportunities are strongest where providers are actively modernizing outpatient networks and integrating behavioral care into broader care models.

Latin America

Latin America held 7.9% in 2025, supported by steady digitization progress and increasing use of structured workflows to manage service delivery. Provider adoption is influenced by budget constraints and variability in infrastructure maturity across countries. Subscription models and modular deployments are typically attractive for organizations seeking rapid value with controlled costs.

Middle East & Africa

Middle East & Africa represented 4.4% in 2025, reflecting earlier-stage adoption but increasing interest in digitized care models and capacity expansion. Growth is supported by modernization initiatives, rising awareness, and expanding private healthcare delivery. Demand tends to favor solutions that can scale across sites and support standardized operational workflows.

Competitive Landscape

Competition is shaped by vendors expanding platform breadth across clinical, administrative, and financial functions, supported by cloud delivery and configurable workflows. Differentiation increasingly centers on usability, implementation speed, interoperability readiness, and embedded automation that reduces clinician workload. Companies compete through partnerships, product enhancements, and footprint expansion into underserved provider segments such as community clinics and private practices. Consolidation and portfolio expansion remain common as buyers prefer fewer systems with broader coverage.

Oracle (Cerner) typically competes through enterprise-grade platform capabilities that emphasize scalability, workflow standardization, and integration within larger healthcare IT environments. The company’s approach aligns with organizations seeking modernized EHR architectures and more unified clinical and operational data layers. Competitive strength is reinforced by broad solution breadth and enterprise deployment experience. Continued modernization focus supports positioning for large provider organizations seeking system-wide standardization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Oracle (Cerner)

- Epic Systems

- Netsmart Technologies

- Qualifacts

- Core Solutions

- Welligent

- NextGen Healthcare

- AdvancedMD

- Kareo

- Meditab

- Holmusk

- Valant

- Credible Behavioral Health

- Allscripts

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2026, Netsmart Technologies announced an expanded collaboration with Pyramid Healthcare, under which Pyramid will implement Netsmart’s myAvatar EHR and the Bells AI-powered clinical documentation suite to support integrated behavioral health and addiction treatment across its multistate system, enhancing telehealth, e-prescribing, and recovery-focused care experiences for more than 56,000 individuals annually.

- In January 2026, Core Solutions expanded its Cx360 Intelligence platform with built-in Certified Community Behavioral Health Clinic (CCBHC) reporting and compliance capabilities, aiming to ease regulatory reporting while helping behavioral health organizations leverage AI-enhanced workflows for better operational and clinical performance.

- In October 2025, AdvancedMD launched “AdvancedMD Now,” a cloud-based, self-service unified practice management, EHR, and patient engagement platform specifically designed for small mental health practices with up to three providers, featuring DSM-5–aligned workflows, long-form documentation tools, and outcome-focused features tailored to behavioral health needs.

- In July 2025, Core Solutions unveiled Cx360 Intelligence, an AI-powered behavioral health EHR platform that embeds real-time artificial intelligence into clinical workflows—either augmenting existing EHRs or operating as a full AI-native EHR system—to accelerate documentation, support decision-making, and improve outcomes for mental health and intellectual and developmental disability (IDD) providers.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 7477.6 million |

| Revenue forecast in 2032 |

USD 22148.34 million |

| Growth rate (CAGR) |

16.78% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Component Outlook: Software (Integrated Software, Standalone Software), Support Services; By Delivery Model Outlook: Subscription Models, Ownership Models; By Functionality Outlook: Clinical, Administrative, Financial; By End User Outlook: Providers, Payers, Patients, Hospitals, Community Clinics, Private Practices |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Oracle (Cerner), Epic Systems, Netsmart Technologies, Qualifacts, Core Solutions, Welligent, NextGen Healthcare, AdvancedMD, Kareo, Meditab, Holmusk, Valant, Credible Behavioral Health, Allscripts companies |

| No.of Pages |

327 |

Segmentation

Component

- Software [Integrated Software, Standalone Software]

- Support Services

Delivery Model

- Subscription Models

- Ownership Models

Functionality

- Clinical

- Administrative

- Financial

End User

- Providers

- Payers

- Patients

- Hospitals

- Community Clinics

- Private Practices

Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa