Benign Prostatic Hyperplasia Market Overview:

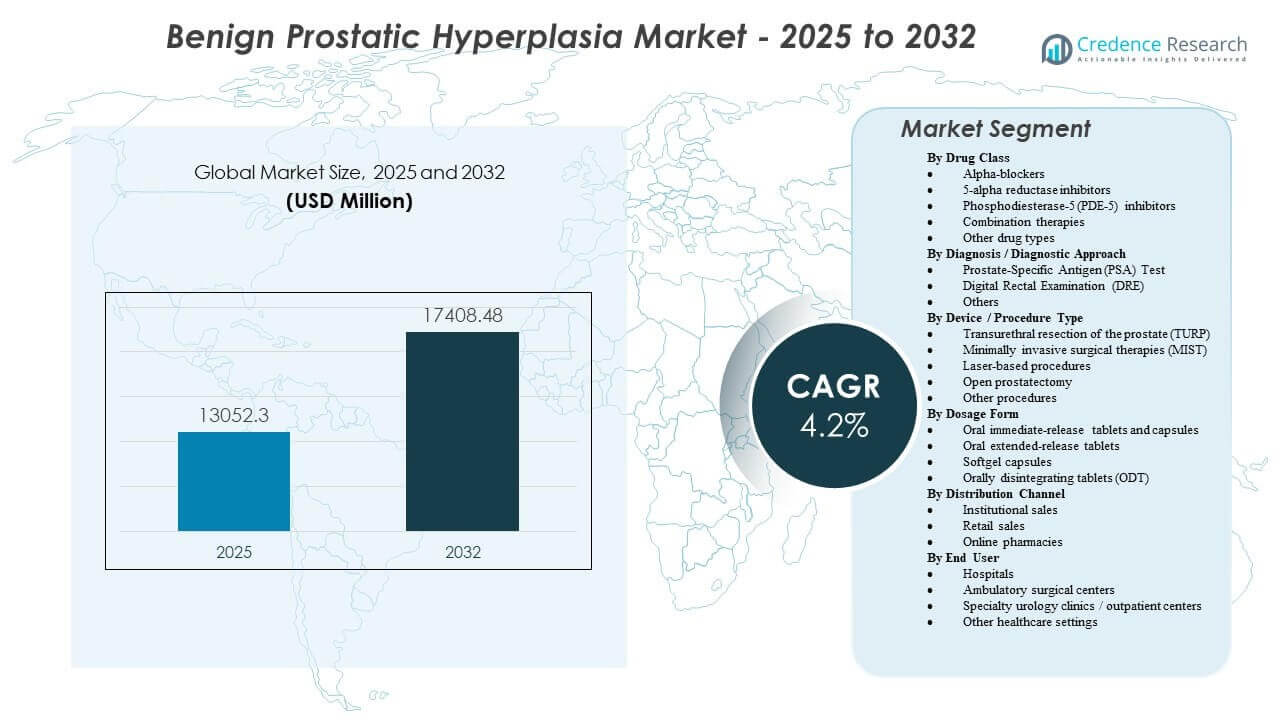

The global Benign Prostatic Hyperplasia Market size was estimated at USD 13,052.3 million in 2025 and is expected to reach USD 17,408.48 million by 2032, growing at a CAGR of 4.2% from 2025 to 2032. Growth is primarily supported by the expanding treated prevalence of lower urinary tract symptoms in aging male populations, which increases long-duration medication use and steady procedure volumes across urology care pathways. Continued adoption of minimally invasive interventions and broader access to specialist evaluation in developing healthcare systems further strengthens demand across both drug and device-based treatment approaches.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Benign Prostatic Hyperplasia Market Size 2025 |

USD 13,052.3 million |

| Benign Prostatic Hyperplasia Market, CAGR |

4.2% |

| Benign Prostatic Hyperplasia Market Size 2032 |

USD 17,408.48 million |

Key Market Trends & Insights

- The market expands from USD 13,052.3 million (2025) to USD 17,408.48 million (2032), reflecting a 4.2% CAGR over the forecast period.

- Alpha-blockers hold the largest share at ~44.6%, supported by first-line prescribing for symptom relief and high generic availability across major markets.

- Institutional sales account for ~68.2%, reflecting the role of hospitals and integrated provider networks in initiating therapy and managing procedure-led pathways.

- Hospitals represent ~64.1% of end-user demand, driven by higher diagnostic depth, referral concentration, and surgical capacity for moderate-to-severe cases.

- TURP contributes ~36.4% of procedure volume/value, indicating sustained utilization of established surgical standards alongside newer minimally invasive options.

Segment Analysis

The market shows a dual-growth structure, with chronic pharmacotherapy anchoring recurring revenue and procedural innovation shaping site-of-care shifts. Treatment selection is increasingly influenced by symptom severity, prostate size, comorbidity burden, and patient preference for faster recovery. As awareness and diagnostic activity increase, a larger share of patients move from watchful waiting into active medication use, and a subset escalates into device-based interventions when symptoms persist or progression risk rises.

Competitive differentiation is strengthening across both drug and device segments. In pharmaceuticals, differentiation is shaped by adherence, tolerability, and combination use in higher-risk patients. In procedures, differentiation is driven by outpatient feasibility, safety profiles, durability of symptom improvement, and the ability to treat broader prostate anatomies. This dynamic supports ongoing innovation, training-driven adoption, and expanding availability across hospitals, ambulatory centers, and specialty urology clinics.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Drug Class Insights

Alpha-blockers accounted for the largest share of ~44.6%. Their leadership is supported by rapid symptom relief, broad physician familiarity, and suitability for a wide range of symptom severities in routine practice. High generic penetration improves affordability and supports persistence in maintenance therapy, especially in price-sensitive health systems. Combination therapies also contribute to category stability, as clinicians escalate treatment in patients with larger prostates or higher progression risk, keeping drug pathways central to long-term management.

By Diagnosis / Diagnostic Approach Insights

BPH diagnosis remains anchored in practical, clinic-friendly evaluation pathways that prioritize accessibility and repeatability in routine care. PSA testing is widely used alongside symptom scoring to support risk assessment and guide referral decisions, particularly when clinicians need to rule out malignancy concerns. DRE remains relevant as a point-of-care assessment that supports triage and initial urology workups. As routine checkups expand and awareness improves, diagnostic approaches increasingly act as a gateway to earlier treatment initiation and structured follow-up.

By Device / Procedure Type Insights

Transurethral resection of the prostate (TURP) accounted for the largest share of ~36.4%. It retains strong utilization due to durable outcomes and established clinical confidence, especially for patients requiring definitive symptom relief. Adoption of minimally invasive surgical therapies continues to rise because many approaches fit outpatient settings and offer faster recovery compared to conventional surgery. Laser-based procedures benefit from improved hemostasis and procedural flexibility in selected patient cohorts. Overall, the procedure mix is increasingly shaped by site-of-care migration, provider training availability, and patient preference for lower invasiveness.

By Dosage Form Insights

Oral solid formats remain the preferred delivery route due to convenience in chronic therapy and broad reimbursement and pharmacy availability. Immediate-release tablets and capsules are commonly used for standard initiation and titration patterns, supporting wide uptake across primary and specialist care. Extended-release formulations support once-daily routines and tolerability considerations for long-term management. Softgels and ODT formats provide additional options aligned with administration convenience and patient preference, supporting adherence in select populations.

By Distribution Channel Insights

Institutional sales accounted for the largest share of ~68.2%. Hospitals and large provider networks channel a significant portion of diagnosis, prescription initiation, and procedure-led care, which concentrates early treatment decisions in institutional pathways. Institutional procurement also supports device-based procedures and bundled care delivery, reinforcing its dominance in overall value capture. Retail pharmacies remain important for long-term medication refills and local accessibility, particularly for stable patients on maintenance therapy. Online pharmacies continue to expand in refill-driven demand, supported by home delivery convenience and subscription-based medication management in some markets.

By End User Insights

Hospitals accounted for the largest share of ~64.1%. They lead due to stronger diagnostic capability, access to advanced imaging and surgical infrastructure, and referral capture for complex or progressed cases. Hospitals also act as the core environment for procedure adoption, clinician training, and post-procedure monitoring. Ambulatory surgical centers expand as minimally invasive options enable safe outpatient workflows and cost-efficient care pathways. Specialty urology clinics and outpatient centers grow through evaluation volume, follow-up management, and selective procedure offerings aligned with local reimbursement and clinical capacity.

Benign Prostatic Hyperplasia Market Drivers

Rising treated prevalence in aging male populations

BPH incidence increases with age, expanding the patient pool requiring symptom evaluation and long-term management. As men live longer, the duration of therapy and monitoring expands, strengthening recurring drug demand. Higher awareness and routine health evaluations increase the share of patients who move from under-diagnosis into active treatment. This driver supports steady demand across both medications and procedural options.

Expanding use of long-duration pharmacotherapy and combination regimens

Many patients remain on therapy for extended periods to manage symptoms and reduce progression risk. First-line prescribing supports high initiation volumes, and therapy escalation increases as symptoms persist or anatomical factors change. Combination approaches are increasingly used in patients with higher progression risk profiles, reinforcing category depth. Chronic use patterns support stable prescription volume and recurring revenue in pharmacy channels.

- For instance, long-term trials show that chronic dutasteride therapy at 0.5 mg daily can reduce serum dihydrotestosterone by about 93% over 2 years, while finasteride 5 mg daily reduces levels by roughly 70% over 4 years, and combination regimens with alpha‑blockers demonstrate superior reduction in BPH progression versus monotherapy.

Growth in minimally invasive procedures and outpatient suitability

Demand for lower invasiveness and shorter recovery supports wider adoption of minimally invasive surgical therapies. Outpatient feasibility expands the addressable care setting, helping providers deliver interventions with reduced hospitalization burden. Increasing clinician familiarity and training programs also support procedure uptake across new sites of care. This driver supports device utilization alongside continued use of established surgeries.

- For instance, five‑year clinical data on Rezūm water vapor therapy report a surgical retreatment rate of 4.4%, while pivotal UroLift prostatic urethral lift data show a 13.6% surgical retreatment rate at five years and sustained symptom relief, highlighting durable outcomes that can be delivered in outpatient settings.

Improved access to urology care pathways and diagnostic infrastructure

Expansion of diagnostic centers, specialist networks, and referral pathways increases treatment penetration beyond major urban hubs. Earlier identification supports earlier therapy initiation, which raises cumulative lifetime treatment value per patient. Broader access also increases follow-up rates, supporting repeat prescriptions and monitoring. Over time, this strengthens the overall treated population and supports both drug and device market expansion.

Benign Prostatic Hyperplasia Market Challenges

Treatment outcomes can vary by patient anatomy, symptom severity, and comorbidity burden, which complicates standardized care pathways and can slow therapy optimization. Side effects and tolerability concerns may reduce adherence in chronic pharmacotherapy, particularly in older patients managing multiple medications. In procedures, variability in provider experience and training availability can influence outcomes and adoption speed. These factors can create uneven uptake across geographies and sites of care.

- For instance, in Insightec’s MR-guided focused ultrasound thalamotomy trial for essential tremor, patients meeting imaging-based prognostic cutoffs achieved a 69.8% tremor improvement at 2 years versus 43.6% in others, highlighting how patient-specific factors materially alter response to the same technology.

Pricing and reimbursement pressures also shape adoption and product mix. High generic penetration compresses value growth in mature drug classes, forcing competition to rely on differentiation and patient persistence rather than pricing power. Procedure reimbursement complexity and regional policy variation can delay adoption of newer approaches. In emerging markets, limited specialist density and diagnostic access can constrain treated prevalence despite large underlying patient pools.

Benign Prostatic Hyperplasia Market Trends and Opportunities

Procedure innovation continues to shift the market toward outpatient-friendly care models, creating opportunities for technologies that offer predictable outcomes with shorter recovery. Devices that expand eligibility across wider prostate anatomies or reduce perioperative burden are positioned to gain share as providers seek scalable workflows. Growth is also supported by broader clinician education and increased patient awareness, which improves acceptance of early intervention. These trends favor solutions that integrate well into routine urology pathways.

- For instance, Boston Scientific’s Rezūm Water Vapor Therapy has demonstrated a 48% improvement in International Prostate Symptom Score (IPSS) and a 49% increase in maximum urinary flow rate at five years, supporting durable symptom relief in an office or outpatient setting.

Medication management is also evolving toward patient-friendly regimens and adherence support. Once-daily dosing preference, tolerability-led switching, and refill optimization are shaping prescribing and channel strategies. Online pharmacy growth supports recurring revenue models for maintenance therapy, particularly in urban populations. Opportunities expand for companies that combine strong clinical evidence, clear patient selection criteria, and effective provider training or distribution coverage.

Regional Insights

North America

North America represents the largest regional share at ~34.27%, supported by high diagnosis rates, broad access to urology specialists, and established treatment pathways. Prescription therapy remains deeply embedded in routine LUTS management, while procedure volumes benefit from strong hospital and outpatient infrastructure. Adoption of minimally invasive approaches is supported by reimbursement frameworks and training-driven diffusion across provider networks. The region also sees strong uptake of device innovation tied to patient preference for quicker recovery.

Europe

Europe accounts for ~25.83%, with demand shaped by aging demographics, structured primary-to-specialist referral pathways, and broad access to pharmacotherapy. Hospitals and specialty centers play a central role in procedure-led care for moderate-to-severe symptoms. Treatment decisions often balance long-term medication use with interventional escalation based on symptom persistence and quality-of-life impact. Adoption patterns vary by country, driven by reimbursement structures and specialist capacity.

Asia Pacific

Asia Pacific contributes ~27.06%, supported by a large patient base and improving access to diagnosis and specialist care. Urban centers are expanding urology service availability, increasing treatment penetration and follow-up monitoring. Growth is strengthened by rising awareness and increasing capacity for minimally invasive procedures in leading healthcare systems. The region’s mix includes high-volume pharmacotherapy demand alongside growing procedural adoption as infrastructure matures.

Latin America

Latin America holds ~6.49%, with demand concentrated in major urban markets where diagnostic access and specialist availability are stronger. Private healthcare expansion supports uptake of both medications and selected interventional procedures. However, uneven access outside large cities can limit treated prevalence and follow-up continuity. Growth opportunities improve as diagnostic networks expand and outpatient pathways become more accessible.

Middle East & Africa

Middle East & Africa represents ~6.35%, supported by investment in private hospitals and specialist services in select countries. Demand is driven by expanding access to diagnostics, greater health awareness, and gradual adoption of modern urology procedures. However, access variability and reimbursement differences can slow adoption outside developed sub-regions. Over time, capacity-building in tertiary care centers supports growth in both pharmacotherapy and procedure volumes.

Competitive Landscape

Competition spans established pharmaceutical portfolios and device-driven procedural innovation. Drug-market competition is shaped by generic availability, formulary positioning, and therapy persistence, with differentiation supported by tolerability, dosing convenience, and combination use in higher-risk patients. Device and procedure competition centers on clinical outcomes, safety, outpatient feasibility, and the ability to treat broader patient profiles with predictable recovery. Provider training, evidence generation, and channel coverage remain key levers for adoption and share gain.

Abbott Laboratories maintains a broad healthcare footprint that supports participation across diagnostic and therapeutic pathways connected to urology care delivery. Its positioning benefits from integrated healthcare channel access and relationships across institutional and retail environments. Such scale can support go-to-market execution, distribution reach, and alignment with evolving care pathways as outpatient adoption rises. Competitive impact is reinforced when product portfolios connect smoothly with routine clinical workflows and monitoring needs.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AbbVie Inc. (Allergan)

- Astellas Pharma Inc.

- Boehringer Ingelheim GmbH

- GlaxoSmithKline plc (GSK)

- Merck & Co., Inc.

- Pfizer Inc.

- Sanofi S.A.

- Teva Pharmaceutical Industries Ltd.

- Boston Scientific Corporation

- Teleflex Incorporated (NeoTract / UroLift)

- Olympus Corporation

- KARL STORZ SE & Co. KG

- PROCEPT BioRobotics Corporation

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In December 2025, ProVerum Limited announced that the United States Food and Drug Administration had granted regulatory approval to its ProVee System, described as the first of a new generation of prostatic urethral stents designed specifically for the minimally invasive treatment of benign prostatic hyperplasia.

- In December 2025, Zenflow Inc. received approval from the United States Food and Drug Administration for its Spring Implant and Delivery System as a first-line interventional therapy for men with benign prostatic hyperplasia, a milestone that allows Zenflow to introduce a new reversible implant-based option that aims to combine the durability of an interventional procedure with the flexibility traditionally associated with pharmacologic management of BPH.

- In August 2025, ProVerum Limited reported the closing of an USD 80 million Series B equity financing round led by MVM Partners with participation from OrbiMed and other institutional investors, with proceeds earmarked to advance clinical development and commercialization of the ProVee System as a minimally invasive, nitinol-based solution for benign prostatic hyperplasia.

- In April 2025, Medicus Pharma Inc. entered into an acquisition agreement to purchase Antev for approximately USD 75 million in order to obtain global rights to Teverelix, a gonadotropin-releasing hormone antagonist being developed to prevent acute urinary retention and reduce the need for surgery in patients with benign prostatic hyperplasia (BPH),

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 13,052.3 million |

| Revenue forecast in 2032 |

USD 17,408.48 million |

| Growth rate (CAGR) |

4.2% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Drug Class Outlook: Alpha-blockers, 5-alpha reductase inhibitors, Phosphodiesterase-5 (PDE-5) inhibitors, Combination therapies, Other drug types; By Diagnosis / Diagnostic Approach Outlook: Prostate-Specific Antigen (PSA) Test, Digital Rectal Examination (DRE), Others; By Device / Procedure Type Outlook: Transurethral resection of the prostate (TURP), Minimally invasive surgical therapies (MIST), Laser-based procedures, Open prostatectomy, Other procedures; By Dosage Form Outlook: Oral immediate-release tablets and capsules, Oral extended-release tablets, Softgel capsules, Orally disintegrating tablets (ODT); By Distribution Channel Outlook: Institutional sales, Retail sales, Online pharmacies; By End User Outlook: Hospitals, Ambulatory surgical centers, Specialty urology clinics / outpatient centers, Other healthcare settings |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Abbott Laboratories; AbbVie Inc. (Allergan); Astellas Pharma Inc.; Boehringer Ingelheim GmbH; GlaxoSmithKline plc (GSK); Merck & Co., Inc.; Pfizer Inc.; Sanofi S.A.; Teva Pharmaceutical Industries Ltd.; Boston Scientific Corporation; Teleflex Incorporated (NeoTract / UroLift); Olympus Corporation; KARL STORZ SE & Co. KG; PROCEPT BioRobotics Corporation |

| No. of Pages |

330 |

Segmentation

By Drug class

- Alpha-blockers

- 5-alpha reductase inhibitors

- Phosphodiesterase-5 (PDE-5) inhibitors

- Combination therapies

- Other drug types

By Diagnosis / diagnostic approach

- Prostate-Specific Antigen (PSA) Test

- Digital Rectal Examination (DRE)

- Others

By Device / procedure type

- Transurethral resection of the prostate (TURP)

- Minimally invasive surgical therapies (MIST)

- Laser-based procedures

- Open prostatectomy

- Other procedures

By Dosage form

- Oral immediate-release tablets and capsules

- Oral extended-release tablets

- Softgel capsules

- Orally disintegrating tablets (ODT)

By Distribution channel

- Institutional sales

- Retail sales

- Online pharmacies

By End user

- Hospitals

- Ambulatory surgical centers

- Specialty urology clinics / outpatient centers

- Other healthcare settings

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa