Biguanides Market Overview:

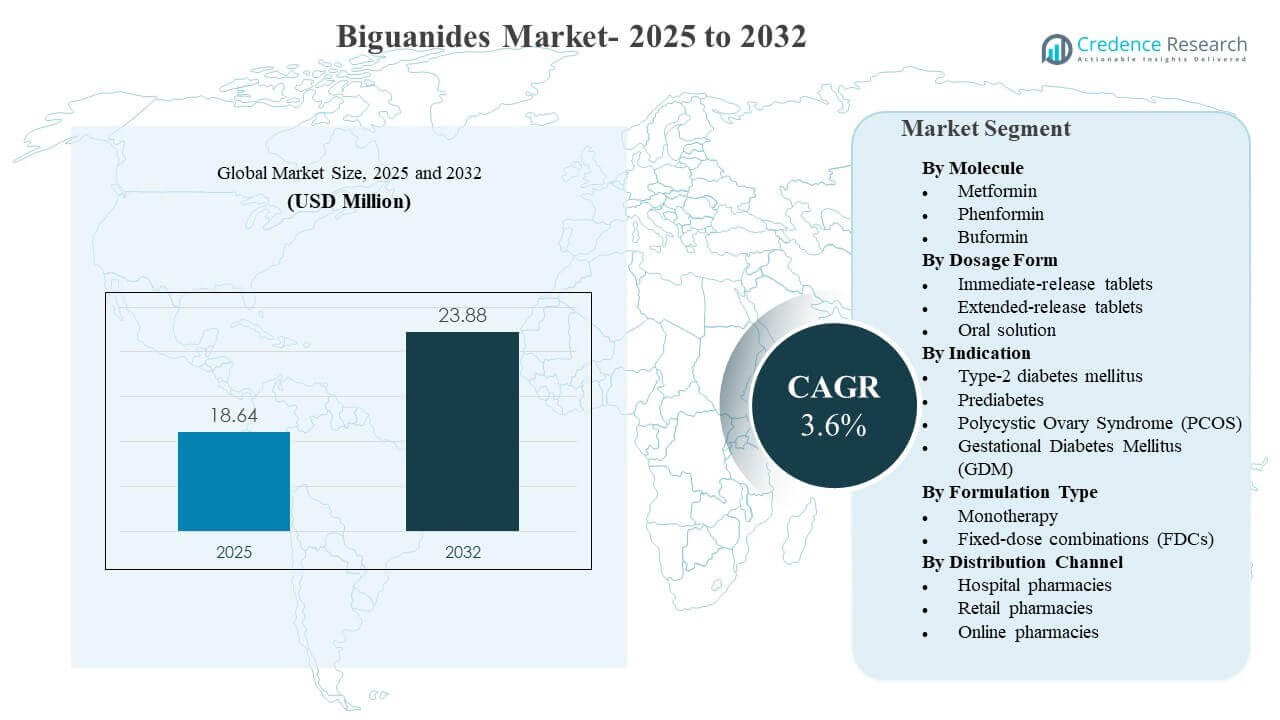

The global Biguanides Market size was estimated at USD 18.64 million in 2025 and is expected to reach USD 23.88 million by 2032, growing at a CAGR of 3.6% from 2025 to 2032. Demand is primarily driven by the sustained role of metformin-based therapy across the type-2 diabetes care pathway, reinforced by wide prescriber familiarity, strong generic availability, and large treated patient pools across both mature and emerging healthcare systems. A steady shift toward extended-release dosing and fixed-dose combinations is also improving adherence and persistence in chronic therapy, and these factors are increasingly shaping manufacturer portfolio strategy and channel mix across major regions.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biguanides Market Size 2025 |

USD 18.64 million |

| Biguanides Market , CAGR |

3.6% |

| Biguanides Market Size 2032 |

USD 23.88 million |

Key Market Trends & Insights

- Metformin accounted for the largest share of 94.3% in 2025, reflecting deep prescriber adoption and broad generic penetration across healthcare systems.

- Immediate-release tablets captured 58.9% share in 2025, supported by low cost per dose and entrenched first-line prescribing practices in primary care.

- Type-2 diabetes mellitus represented 87.8% of demand in 2025, making it the dominant indication for biguanide utilization and refill-driven volumes.

- Monotherapy held 50.7% share in 2025, with continued use as an initial treatment step before intensification into combination regimens.

- Asia Pacific led with a 33.7% revenue share in 2025, anchored by large patient volumes and expanding diagnosis and treatment coverage.

Segment Analysis

Biguanides remain a mature, volume-led therapeutic class where growth is shaped by chronic disease burden and regimen optimization rather than rapid molecule innovation. Prescribing patterns continue to favor metformin as a foundational therapy, and demand stability is reinforced by broad accessibility, high clinician comfort, and long-standing use across the diabetes continuum. In many markets, refill behavior and continuity of care programs sustain baseline consumption, keeping the market resilient even during therapy switching and intensification.

Product strategy is increasingly focused on formulation and regimen convenience. Extended-release dosing is gaining traction for patients seeking simplified schedules and improved gastrointestinal tolerability, and fixed-dose combinations are expanding to improve adherence and enable earlier multi-mechanism control in type-2 diabetes. Distribution dynamics are also shifting as digital pharmacies scale chronic refill fulfillment and home delivery, creating new competitive emphasis on availability, pricing discipline, and supply reliability across channels.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Molecule Insights

Metformin accounted for the largest share of 94.3% in 2025. Leadership is reinforced by its entrenched first-line positioning in routine type-2 diabetes management and its extensive generic manufacturing base that supports affordability and access. High prescriber familiarity and large installed patient populations sustain repeat purchasing behavior across retail and institutional settings. Adjunct demand from insulin-resistance related use cases further supports baseline utilization in select patient groups.

By Dosage Form Insights

Immediate-release tablets accounted for the largest share of 58.9% in 2025. The segment leads due to established prescribing habits, wide availability of low-cost generics, and broad formulary inclusion across public and private reimbursement pathways. Immediate-release formats also remain common for initiation and titration, particularly in price-sensitive settings. High-volume tender procurement in institutional care further supports consistent consumption of immediate-release tablets.

By Indication Insights

Type-2 diabetes mellitus accounted for the largest share of 87.8% in 2025. The indication leads due to the large treated population base and the continued role of metformin-centered regimens across early and ongoing therapy. Routine screening and earlier diagnosis in multiple geographies are increasing the pool of patients eligible for initiation. Chronic refills and stepwise intensification into combination regimens sustain ongoing demand tied to type-2 diabetes care pathways.

By Formulation Type Insights

Monotherapy accounted for the largest share of 50.7% in 2025. The segment remains dominant because metformin is frequently used as an initial therapy step before escalation, particularly where cost containment and simple regimens are prioritized. Monotherapy prescribing is also supported by strong generic supply and broad availability across dosage strengths and pack sizes. Clinical practice patterns that start with single-agent therapy and intensify based on glycemic response keep monotherapy volumes structurally high.

By Distribution Channel Insights

Hospital pharmacies accounted for the largest share of 43.9% in 2025. Leadership is linked to diagnosis and initiation workflows concentrated in hospitals, protocol-driven prescribing in specialist settings, and hospital-led chronic disease programs that influence refill behavior. Institutional procurement and inpatient-to-outpatient transition pathways also support strong hospital channel throughput. In several markets, hospital-connected dispensing networks improve continuity and reinforce hospital share in chronic therapy distribution.

Biguanides Market Drivers

Expanding treated type-2 diabetes population

Rising diagnosis and treatment coverage for type-2 diabetes is the core demand engine for biguanides. Primary care protocols frequently position metformin-based therapy at the start of the treatment pathway, which sustains high initiation volumes. Ongoing refills and long treatment durations amplify recurring demand in both mature and emerging markets. Broader screening and care access also increase therapy continuity, supporting stable purchasing across hospital and retail channels.

- For instance, metformin marketed by multiple originators and generic manufacturers such as Bristol Myers Squibb and Teva was prescribed over 90 million times annually in the U.S. by 2021, more than double the volume recorded in 2004, underscoring its entrenched first-line role in type-2 diabetes management.

Strong generic availability and affordability

A large and competitive manufacturing base has improved product availability and reduced cost barriers for core biguanide therapy. Broad formulary inclusion supports consistent demand across public systems and private insurance models. Price-access balance is particularly important in high-volume regions where therapy affordability influences adherence and persistence. Supply scale also enables large tenders and institutional procurement, reinforcing baseline demand in hospital-connected distribution.

- For instance, large generic producers such as Teva, Sun Pharmaceutical, and Aurobindo Pharma collectively supply metformin hydrochloride to support global volumes that reached roughly 88 thousand tonnes in 2024, enabling sustained participation in large-scale public and institutional tenders worldwide.

Shift toward convenience-focused formulations and combinations

Extended-release dosing and fixed-dose combinations are improving regimen convenience and adherence for chronic users. Once-daily schedules and improved tolerability can reduce discontinuation risk and support therapy persistence. Combination regimens that include metformin enable earlier intensification and simplify multi-drug administration, supporting uptake in patients requiring broader glycemic control. These formulation strategies also enable differentiation beyond commodity generics in select markets.

Channel modernization and refill continuity

Distribution improvements are supporting better therapy continuity across the diabetes care cycle. Retail pharmacy networks remain critical for refills, and online pharmacy growth is expanding convenience and access for chronic medication delivery. Digital prescription workflows and subscription refill models reduce friction in repeat purchases. These channel shifts encourage manufacturers and distributors to strengthen availability, packaging, and inventory planning to protect continuity of supply.

Biguanides Market Challenges

Pricing pressure remains a structural challenge because high generic penetration limits margin expansion for commodity formulations. Competitive tendering, reimbursement controls, and substitution policies can compress realized prices and intensify competition among suppliers. Product differentiation is also constrained because molecule-level innovation is limited, forcing manufacturers to compete through formulation, combinations, or channel access. Maintaining profitability therefore depends on operational efficiency, scale, and stable supply performance.

- For instance, under China’s volume-based procurement (VBP) program, winning generic manufacturers have accepted price cuts often exceeding 90% in centralized tenders, which sharply narrows unit margins but allows high-volume players to sustain profitability through very large contracted volumes and low-cost manufacturing footprints.

Regulatory and quality expectations create ongoing compliance burdens across the manufacturing and distribution chain. Any disruption related to quality deviations, inspection outcomes, or supply interruptions can quickly affect availability in high-volume chronic therapy markets. Inventory risk increases when demand patterns shift toward extended-release or combination formats that require different production planning. Companies must also manage variability in national reimbursement rules and formulary decisions that influence channel mix and pricing.

Biguanides Market Trends and Opportunities

Formulation-led value creation is emerging as a key trend as extended-release dosing gains share and supports patient convenience. Product portfolios are increasingly designed to balance high-volume immediate-release demand with differentiated extended-release offerings that can improve persistence in chronic therapy. Packaging innovations, titration-friendly strengths, and patient-support tools also support adherence and reduce discontinuation risk. These shifts create opportunities for suppliers that can scale quality manufacturing and maintain consistent availability across channels.

Fixed-dose combinations represent a meaningful growth avenue as healthcare systems encourage simplified regimens and earlier intensification. Metformin-based combinations can reduce pill burden and support multi-mechanism control, aligning with real-world adherence needs in long-duration therapy. Online pharmacy expansion further improves access for refill-driven categories and supports predictable demand patterns through subscription and delivery models. Companies that align portfolios to these therapy and channel shifts can strengthen positioning despite pricing pressure.

- For instance, the GIFT study of patients with type 2 diabetes switching from separate metformin plus DPP‑4 inhibitor tablets to a fixed‑dose combination reported significantly greater HbA1c reductions in those with high baseline pill burden, with a 0.4% A1c drop in patients taking 10 or more pills per day compared with 0.1% in those taking fewer than 10 pills, underscoring the clinical value of regimen simplification.

Regional Insights

North America

North America held an estimated 28.1% revenue share in 2025. Revenue contribution is supported by higher penetration of combination regimens, strong refill continuity, and mature pharmacy distribution infrastructure. Institutional protocols and specialist-led diabetes management programs influence initiation and intensification patterns. Market performance is also shaped by payer-driven formulary design and substitution dynamics across brands and generics.

Europe

Europe held an estimated 22.9% revenue share in 2025. The region benefits from broad access to essential diabetes therapy and consistent primary care prescribing. Revenue share is moderated by high generic utilization and price controls across many national health systems. Demand stability remains strong due to chronic refill behavior and large treated populations. Regional variation is influenced by reimbursement rules, tender mechanisms, and country-level prescribing guidelines.

Asia Pacific

Asia Pacific held 33.7% revenue share in 2025. Large patient volumes and rising diagnosis rates are central to regional leadership, supported by improving access to therapy across public and private channels. High generic availability sustains affordability and supports broad uptake. Urbanization and expanding retail pharmacy footprints improve refill convenience. Digital dispensing and delivery models are increasingly influencing channel mix and continuity.

Latin America

Latin America held an estimated 8.6% revenue share in 2025. Growth is influenced by expanding access to chronic therapies, improving diagnosis rates, and increasing pharmacy reach in large urban centers. Pricing sensitivity and uneven reimbursement coverage across countries continue to shape adoption and persistence. Generic availability supports volume growth, but revenue expansion can be constrained by procurement practices. Channel modernization is improving refill continuity in select markets.

Middle East & Africa

Middle East & Africa held an estimated 6.7% revenue share in 2025. Demand is supported by rising metabolic disease burden and improving healthcare access in higher-income markets within the region. Adoption is uneven due to variability in diagnosis rates, reimbursement systems, and supply consistency. Public-sector procurement plays a meaningful role in many countries, affecting price realization and availability. Expansion of private pharmacy networks is improving access for chronic refills.

Competitive Landscape

Competition is shaped by high-volume generic supply, price discipline, and consistent product availability across channels. Differentiation increasingly comes from extended-release formulations, fixed-dose combinations, and supply reliability that supports chronic refill continuity. Companies also compete through regulatory execution, broad dose-strength portfolios, and geographic expansion across tender-driven and retail-led markets. Strategic emphasis is shifting toward portfolio mix optimization to balance commodity volumes with differentiated formats.

Bristol Myers Squibb is typically positioned through lifecycle management and portfolio strategy discipline across established therapeutic categories, with focus on maintaining supply consistency and commercial execution in mature markets. Competitive relevance in the biguanides landscape is linked to disciplined portfolio participation, commercialization capability, and the ability to navigate evolving channel mix and reimbursement dynamics. The company’s strategic approach aligns with maintaining continuity in demand-led therapy categories where prescriber trust and product availability influence ongoing utilization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bristol Myers Squibb

- Takeda Pharmaceutical Company

- Sanofi S.A.

- Merck & Co., Inc.

- Boehringer Ingelheim

- Eli Lilly and Company

- Teva Pharmaceutical Industries Ltd.

- Novo Nordisk A/S

- Pfizer Inc.

- Glenmark Pharmaceuticals Ltd.

- Sun Pharmaceutical Industries Ltd.

- Cipla Ltd.

- Dr. Reddy’s Laboratories Ltd.

- Lupin Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2025, DongKoo Bio & Pharma received South Korean regulatory approval for Sitaflozinmet, a new triple‑combination antidiabetic product that combines metformin hydrochloride (a biguanide) with dapagliflozin and sitagliptin, positioning the company to target patients needing intensified glucose control with a single fixed‑dose tablet and strengthening its presence in the biguanides segment of the diabetes market.

- In January 2025, Zydus Lifesciences secured inclusion of its products Zituvio, Zituvimet, and Zituvimet XR on the CVS Caremark formulary in the United States, effectively expanding patient access to these metformin‑based DPP‑4 inhibitor combination therapies and reinforcing the company’s commercial footprint in biguanide‑containing fixed‑dose combinations within the U.S. diabetes care landscape.

- In December 2024, Lupin finalized the acquisition of Indian marketing rights for Boehringer Ingelheim’s diabetes brands Gibtulio, Gibtulio Met, and AJADUO, which include metformin‑containing combination therapies, thereby broadening Lupin’s biguanide‑anchored antidiabetic portfolio in India and enabling the company to leverage established brands in the highly competitive oral diabetes treatments market.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 18.64 million |

| Revenue forecast in 2032 |

USD 23.88 million |

| Growth rate (CAGR) |

3.6% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Molecule; By Dosage Form; By Indication; By Formulation Type; By Distribution Channel |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Bristol Myers Squibb, Takeda Pharmaceutical Company, Sanofi S.A., Merck & Co., Inc., Boehringer Ingelheim, Eli Lilly and Company, Teva Pharmaceutical Industries Ltd., Novo Nordisk A/S, Pfizer Inc., Glenmark Pharmaceuticals Ltd., Sun Pharmaceutical Industries Ltd., Cipla Ltd., Dr. Reddy’s Laboratories Ltd., Lupin Ltd. |

| No. of Pages |

336 |

Segmentation

By Molecule

- Metformin

- Phenformin

- Buformin

By Dosage Form

- Immediate-release tablets

- Extended-release tablets

- Oral solution

By Indication

- Type-2 diabetes mellitus

- Prediabetes

- Polycystic Ovary Syndrome (PCOS)

- Gestational Diabetes Mellitus (GDM)

By Formulation Type

- Monotherapy

- Fixed-dose combinations (FDCs)

By Distribution Channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa