Bioengineered Protein Drugs Market Overview:

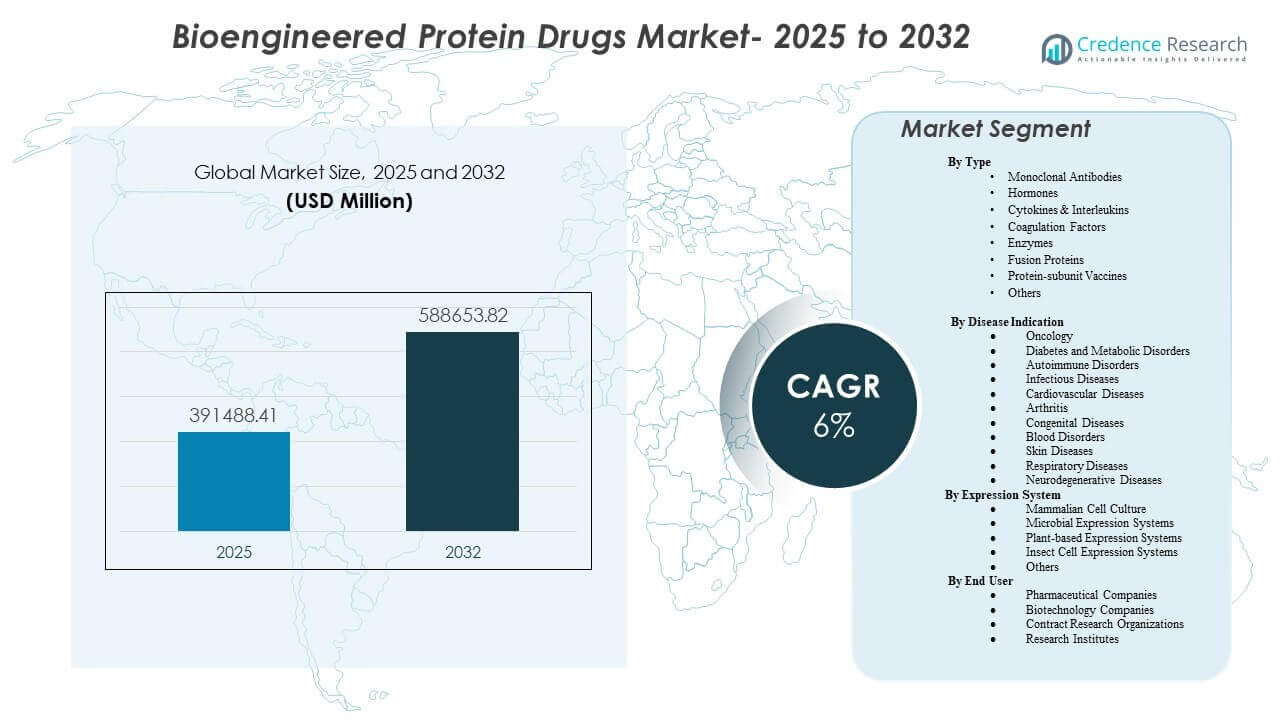

The global Bioengineered Protein Drugs Market size was estimated at USD 391,488.41 million in 2025 and is expected to reach USD 588,653.82 million by 2032, growing at a CAGR of 6% from 2025 to 2032. Demand growth is primarily supported by sustained clinical adoption of engineered biologics across high-burden chronic diseases, supported by deeper pipelines, broader lines of therapy, and continued expansion of specialty-care access. Bioengineered Protein Drugs Market activity remains concentrated in mature healthcare systems while faster uptake in emerging markets is supported by expanding biologics manufacturing capacity and improving reimbursement pathways.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bioengineered Protein Drugs Market Size 2025 |

USD 391,488.41 million |

| Bioengineered Protein Drugs Market, CAGR |

6% |

| Bioengineered Protein Drugs Market Size 2032 |

USD 588,653.82 million |

Key Market Trends & Insights

- North America accounted for 43.70% of Bioengineered Protein Drugs Market revenue in 2025, reflecting continued concentration of biologics usage and spend.

- Monoclonal Antibodies accounted for the largest share of 40.8% in 2025, supported by broad use across oncology and immune-mediated disorders.

- Oncology represented 33.9% of Bioengineered Protein Drugs Market demand in 2025, supported by high biologics penetration across multiple tumor types and combination regimens.

- Mammalian Cell Culture represented 71.2% of Bioengineered Protein Drugs Market production in 2025, reflecting the dominance of complex proteins requiring human-like post-translational modifications.

- Bioengineered Protein Drugs Market is expected to expand at 6% CAGR during 2025–2032, supported by sustained biologics innovation and scaling of manufacturing capacity.

Segment Analysis

Bioengineered Protein Drugs Market performance is shaped by a product mix led by antibody therapeutics, alongside sustained contribution from hormones, cytokines, and advanced protein formats. Commercial performance is strengthened by ongoing label expansions, lifecycle management strategies, and the increasing use of targeted biologics in earlier treatment lines for select indications. Treatment protocols in oncology and immunology continue to favor engineered proteins where clinical differentiation and patient outcomes are clearly established.

Bioengineered Protein Drugs Market manufacturing remains anchored in mammalian expression due to quality requirements for complex molecules, especially monoclonal antibodies and glycosylated proteins. Platform standardization, improved yields, and stronger quality systems support scale and supply continuity for high-volume biologics. Alternative expression systems continue to develop for specific protein classes, but large-scale commercial output remains concentrated in established mammalian platforms.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Bioengineered Protein Drugs Market demand also reflects a widening end-user ecosystem that spans large pharmaceutical companies, innovation-driven biotechnology companies, and service-oriented organizations supporting development and scale-up. Trial execution complexity and expanding portfolios sustain demand for specialized development services and advanced analytics. Research institutes continue to contribute early-stage discovery and translational research that feeds clinical pipelines.

By Type Insights

Monoclonal Antibodies accounted for the largest share of 40.8% in 2025. Leadership is supported by broad clinical utility across multiple disease areas, strong evidence bases, and sustained pipeline productivity across antibody formats. Commercial durability is reinforced by new indications, combination regimens, and improved delivery formats that expand patient reach. Manufacturing maturity and regulatory familiarity also support consistent scale-up and global commercialization for antibody portfolios.

By Disease Indication Insights

Oncology accounted for the largest share of 33.9% in 2025. Oncology leadership is sustained by continuous innovation in targeted biologics, high adoption in specialty care, and expansion of biologics into earlier therapy lines. Clinical practice increasingly relies on engineered proteins for precision mechanisms, improved response rates, and improved management of complex tumor biology. Reimbursement prioritization for high-impact oncology therapies further supports value concentration in oncology treatments.

By Expression System Insights

Mammalian Cell Culture accounted for the largest share of 71.2% in 2025. Dominance is linked to the requirement for human-like glycosylation and complex folding for many therapeutic proteins and antibodies. Established mammalian manufacturing ecosystems support predictable quality, validated processes, and regulatory acceptance at commercial scale. Continuous bioprocess improvements, including process intensification and analytics, further strengthen mammalian system competitiveness for large-scale production.

By End User Insights

Bioengineered Protein Drugs Market adoption is led by pharmaceutical and biotechnology companies that commercialize therapeutic proteins at scale and sustain pipeline investments across disease areas. Contract research organizations support clinical execution, bioanalytical testing, and operational scale for complex biologics programs, particularly for emerging developers. Research institutes contribute translational research and platform science that accelerates early discovery and validation of therapeutic targets. Partnerships across end-user groups continue to shorten development timelines and improve development success rates for advanced protein modalities.

Bioengineered Protein Drugs Market Drivers

Expanding biologics pipelines and continued innovation in protein engineering

Bioengineered Protein Drugs Market growth is supported by ongoing expansion of biologics pipelines across oncology, immunology, and metabolic disease areas. Protein engineering advancements improve binding specificity, half-life, and safety profiles, strengthening clinical differentiation. Next-generation formats, including fusion proteins and multispecific antibodies, expand addressable mechanisms and clinical utility. Wider pipeline activity sustains commercialization flow and reinforces long-term demand for manufacturing capacity.

- For instance, Roche’s Hemlibra, a bispecific antibody engineered to bridge factor IXa and factor X, reduced treated bleeds by 96% with weekly dosing and 97% with every-two-week dosing versus no prophylaxis in the phase III HAVEN 3 study, while 55.6% and 60.0% of patients, respectively, recorded zero treated bleeds.

Rising chronic disease burden and increased specialty-care utilization

Bioengineered Protein Drugs Market demand benefits from sustained prevalence of chronic conditions that require long-term therapy and intensive management. Specialty care pathways increasingly use engineered proteins where targeted mechanisms improve outcomes versus traditional therapies. Earlier diagnosis and broader treatment eligibility increase therapy uptake across major indications. Stronger adherence and long-term use for biologics in chronic care also supports recurring revenue growth.

Manufacturing scale-up and platform standardization

Bioengineered Protein Drugs Market expansion is reinforced by continued investments in production capacity and process optimization. Standardized manufacturing platforms improve comparability, reduce variability, and support reliable commercial supply. Process intensification and improved analytics increase yields and reduce cost per gram for major protein classes. Stable production platforms strengthen launch readiness and enable faster geographic expansion.

Improved market access and broader reimbursement coverage for biologics

Bioengineered Protein Drugs Market growth is supported by improved reimbursement coverage for high-impact biologics across developed and selected emerging healthcare systems. Health technology assessment approaches increasingly evaluate outcomes-based benefits, supporting adoption where clinical value is strong. Expanded payer coverage improves uptake in earlier lines of therapy for select indications. More predictable access frameworks also support investment confidence for developers and manufacturers.

- For instance, in NICE’s appraisal of Sanofi and Regeneron’s dupilumab for uncontrolled COPD, pooled BOREAS and NOTUS data showed an adjusted annualized moderate-or-severe exacerbation rate of 0.79 per year with dupilumab versus 1.16 with placebo over 52 weeks, and the committee highlighted an overall 31% exacerbation reduction as clinically meaningful in the reimbursement review.

Bioengineered Protein Drugs Market Challenges

Bioengineered Protein Drugs Market faces persistent cost pressures driven by complex manufacturing requirements, cold-chain logistics, and stringent quality standards. Pricing scrutiny and reimbursement negotiations can slow uptake in cost-sensitive healthcare systems, particularly for high-cost biologics. Supply disruptions, process deviations, and capacity constraints can create product availability risks for high-demand therapies. Development complexity also increases failure risk in late-stage trials, especially for novel protein formats and multi-target mechanisms.

- For instance, Roche’s Vabysmo (faricimab), the first bispecific antibody approved for the eye, was evaluated in 1,329 patients across the phase III TENAYA and LUCERNE studies; 46% and 45% of patients achieved four-month dosing at year one, rising to 59% and 67% at year two, and patients received a median of 10 injections over two years versus 15 with aflibercept , showing how advanced dual-target protein drugs can improve durability but require complex development and execution.

Bioengineered Protein Drugs Market competition intensifies due to biosimilar entry and increased payer preference for lower-cost alternatives in select therapeutic areas. Differentiation requires sustained evidence generation, formulation innovation, and patient-convenience improvements to defend share. Regulatory expectations for comparability, pharmacovigilance, and post-market commitments increase compliance burden. Fragmented access conditions across regions also create uneven commercialization performance and longer market-entry timelines.

Bioengineered Protein Drugs Market Trends and Opportunities

Bioengineered Protein Drugs Market trends increasingly favor next-generation antibody formats, including multispecific antibodies and engineered Fc variants that improve potency and dosing efficiency. Subcutaneous delivery expansion and device-based administration improve patient convenience and support broader outpatient usage. Digital adherence tools and patient support programs are increasingly integrated to improve persistence in chronic therapies. These developments create opportunities for differentiated products that improve outcomes and reduce total care burden.

Bioengineered Protein Drugs Market opportunities are expanding through manufacturing innovation, including modular facilities, advanced analytics, and process automation that improve efficiency and reduce variability. Alternative expression platforms are gaining interest for specific protein categories where cost, speed, or scalability can improve commercial attractiveness. Partnerships between innovators and manufacturing specialists support faster scale-up and earlier commercialization readiness. Geographic expansion in Asia Pacific also creates opportunity as biologics access improves and local production capacity rises.

- For instance, FUJIFILM Diosynth Biotechnologies’ Holly Springs expansion will add 8 additional 20,000 L mammalian cell-culture bioreactors by 2028 on top of the initial 8 by 20,000 L plan, showing how modular scale-out is being used to strengthen biologics production readiness.

Regional Insights

North America

North America accounted for 43.70% of Bioengineered Protein Drugs Market revenue in 2025. Regional leadership is supported by deep biologics penetration, strong specialty-care infrastructure, and broad payer coverage for high-value therapies. Clinical trial density and early adoption of advanced biologics accelerate uptake of novel protein formats. Manufacturing capacity investments and strong commercialization capabilities further support North America leadership.

Europe

Europe accounted for 22.60% of Bioengineered Protein Drugs Market revenue in 2025. Demand is sustained by structured reimbursement systems, established clinical guidelines for biologics, and broad hospital and specialty-clinic access. Competitive dynamics are shaped by biosimilar penetration and value-based purchasing approaches in multiple markets. Continued innovation and strong clinical adoption in oncology and immunology support ongoing demand.

Asia Pacific

Asia Pacific accounted for 22.30% of Bioengineered Protein Drugs Market revenue in 2025. Regional growth is supported by expanding biologics manufacturing ecosystems, improving access frameworks, and rising diagnosis and treatment rates for chronic diseases. Local capacity expansion supports supply resilience and increases affordability for selected biologics. Increasing investment in clinical research and regulatory modernization also supports faster adoption of protein therapeutics.

Latin America

Latin America accounted for 6.40% of Bioengineered Protein Drugs Market revenue in 2025. Uptake is influenced by public procurement, reimbursement constraints, and access variability across countries. Demand remains concentrated in larger markets and major urban centers with higher specialty-care availability. Biosimilars and tender-based purchasing continue to shape price dynamics and product selection.

Middle East & Africa

Middle East & Africa accounted for 5.00% of Bioengineered Protein Drugs Market revenue in 2025. Regional demand is driven by higher-spend pockets supported by public healthcare investments and expansion of specialty-care capacity. Access variability and affordability constraints remain key adoption barriers in several markets. Improvements in hospital infrastructure and procurement systems can support incremental growth for essential biologics.

Competitive Landscape

Bioengineered Protein Drugs Market competition is defined by portfolio breadth, evidence generation, manufacturing scale, and lifecycle management strategies. Leading participants invest in next-generation antibody and protein formats, strengthen indication expansion pathways, and optimize production to improve reliability and cost structure. Partnerships and licensing deals remain central for accessing novel platforms and accelerating clinical development. Competitive differentiation increasingly depends on dosing convenience, real-world outcomes, and supply consistency for large-volume biologics.

Abbott specialization within Bioengineered Protein Drugs Market activity is typically anchored in adjacent therapeutic and diagnostics ecosystems that support broader biologics adoption and disease management workflows. Strategic positioning focuses on improving care pathways through integrated solutions that complement biologic therapy usage across chronic diseases. Portfolio alignment and operational scale support resilient participation in high-demand therapy categories. Cross-functional investments in clinical evidence and commercialization infrastructure strengthen long-term competitiveness.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott

- AbbVie

- Amgen Inc.

- Bayer AG

- Baxter Healthcare

- Biocon

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd.

- GlaxoSmithKline plc

- Johnson & Johnson

- Merck & Co., Inc.

- Novartis AG

- Novo Nordisk

- Sanofi

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In June 2025, Merck received U.S. FDA approval for ENFLONSIA (clesrovimab-cfor), an extended half-life monoclonal antibody for the prevention of RSV lower respiratory tract disease in infants who are born during or entering their first RSV season, making it a notable new biologic product entry in this market.

- In June 2025, BioNTech and Bristol Myers Squibb entered a global strategic partnership to co-develop and co-commercialize BNT327, a next-generation PD-L1xVEGF-A bispecific antibody candidate for multiple solid tumor types. The companies said the collaboration includes a 50/50 profit-and-loss split and is intended to accelerate the candidate’s development and future commercialization across a broad range of oncology indications.

- In March 2025, Sanofi announced a definitive agreement to acquire DR-0201 from Dren Bio, a targeted bispecific myeloid cell engager that has shown robust B-cell depletion in pre-clinical and early clinical studies, strengthening Sanofi’s position in engineered antibody-based immunology therapies.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 391,488.41 million |

| Revenue forecast in 2032 |

USD 588,653.82 million |

| Growth rate (CAGR) |

6% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Type; By Disease Indication; By Expression System; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Abbott; AbbVie; Amgen Inc.; Bayer AG; Baxter Healthcare; Biocon; Eli Lilly and Company; F. Hoffmann-La Roche Ltd.; GlaxoSmithKline plc; Johnson & Johnson; Merck & Co., Inc.; Novartis AG; Novo Nordisk; Sanofi |

| No. of Pages |

340 |

Segmentation

By Type

- Monoclonal Antibodies

- Hormones

- Cytokines & Interleukins

- Coagulation Factors

- Enzymes

- Fusion Proteins

- Protein-subunit Vaccines

- Others

By Disease Indication

- Oncology

- Diabetes and Metabolic Disorders

- Autoimmune Disorders

- Infectious Diseases

- Cardiovascular Diseases

- Arthritis

- Congenital Diseases

- Blood Disorders

- Skin Diseases

- Respiratory Diseases

- Neurodegenerative Diseases

By Expression System

- Mammalian Cell Culture

- Microbial Expression Systems

- Plant-based Expression Systems

- Insect Cell Expression Systems

- Others

By End User

- Pharmaceutical Companies

- Biotechnology Companies

- Contract Research Organizations

- Research Institutes

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa