Biohazard Bags Market

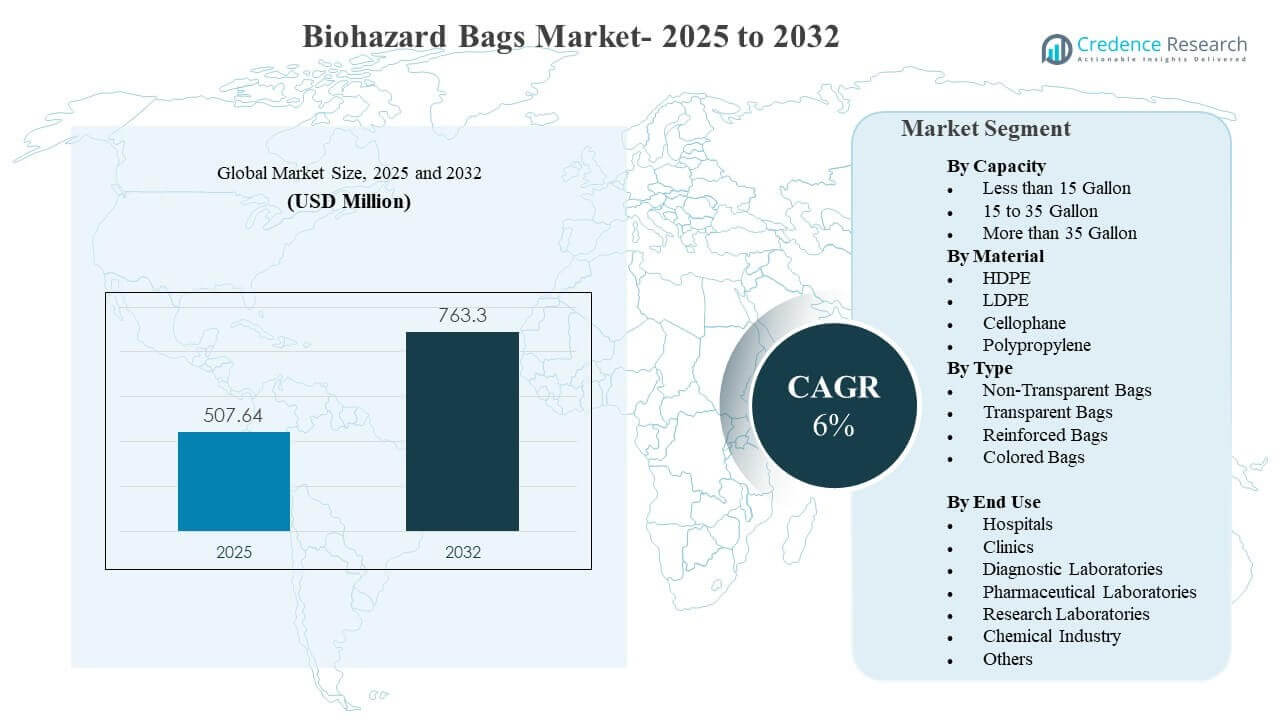

The global Biohazard Bags Market size was estimated at USD 507.64 million in 2025 and is expected to reach USD 763.3 million by 2032, growing at a CAGR of 6% from 2025 to 2032. Growth is primarily driven by stricter biomedical waste segregation and compliance practices across hospitals, clinics, and laboratories, which increases routine procurement of certified containment bags. Expansion of diagnostic testing, outpatient procedures, and laboratory throughput further raises volumes of regulated waste that must be packaged, stored, and transported under controlled protocols.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biohazard Bags Market Size 2025 |

USD 507.64 million |

| Biohazard Bags Market, CAGR |

6% |

| Biohazard Bags Market Size 2032 |

USD 763.3 million |

Key Market Trends & Insights

- The market is projected to expand from USD 507.64 million (2025) to USD 763.3 million (2032) at a 6% CAGR (2025–2032).

- Hospitals accounted for the largest end-use share of 54.1% in 2025, supported by high inpatient throughput and standardized waste workflows.

- More than 35 Gallon bags held the leading capacity share of 47.6% in 2025, reflecting centralized waste collection in high-volume facilities.

- LDPE led the material mix with 41.3% share in 2025, due to its balance of flexibility, tear resistance, and broad compatibility with sealing methods.

- North America represented 37.4% of global revenue in 2025, indicating strong compliance-driven purchasing and mature waste handling systems.

Segment Analysis

Demand for biohazard bags is closely linked to the scale of regulated waste generation in healthcare and laboratory environments, where containment products are purchased repeatedly as consumables. Buyers prioritize consistent thickness, puncture resistance, and secure closure performance because failure risks regulatory non-compliance and exposure incidents. Standardization is common in larger facilities, where procurement teams align bag specifications with internal transport routes, waste carts, and treatment pathways such as autoclaving or off-site processing. As clinical activity expands across diagnostic, outpatient, and research settings, product requirements increasingly emphasize traceability, segregation support, and handling efficiency.

Material selection and bag design are also shaped by how waste is handled from point-of-generation to final disposal. Facilities typically maintain multiple bag types and sizes to support segregation workflows, including color-coded systems and reinforced options for heavier loads or higher tear-risk streams. Laboratory users often require bags compatible with specific handling steps, including controlled storage and sterilization processes, which influences preference for certain polymers and print configurations. Sustainability initiatives are gaining influence in procurement discussions, but performance and compliance remain the primary decision criteria for regulated waste containment.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Capacity Insights

More than 35 Gallon accounted for the largest share of 47.6% in 2025. Large-capacity bags are widely used in hospitals and high-throughput laboratories where waste is consolidated from multiple departments into central collection points. These formats reduce change-out frequency and support operational efficiency during peak clinical and diagnostic activity. They also align with standardized waste cart and bin systems, improving consistency in internal transport and storage workflows.

By Material Insights

LDPE accounted for the largest share of 41.3% in 2025. LDPE is commonly selected for its flexibility and dependable tear resistance, supporting safe handling across routine infectious-waste streams. The material performs well across common sealing and closure methods used in hospitals and labs, which supports purchasing standardization. LDPE also offers a practical balance of performance and cost, making it suitable for high-volume procurement contracts.

By Type Insights

Reinforced and color-coded bag formats are increasingly emphasized in institutional procurement as facilities strengthen segregation discipline and reduce handling risk. Non-transparent bags remain important where privacy and controlled transport are required, especially for regulated streams moved through shared service corridors. Transparent variants support inspection and sorting workflows in laboratory and controlled environments where visual verification can reduce processing errors. Overall, bag type selection is driven by compliance protocols, internal logistics, and the risk profile of the waste stream rather than aesthetics.

By End Use Insights

Hospitals accounted for the largest share of 54.1% in 2025. Hospitals generate the highest volumes of regulated medical waste due to procedure intensity, inpatient occupancy, and round-the-clock operations. Procurement is often centralized, which reinforces consistent specifications and predictable replenishment cycles for biohazard bags. Hospitals also operate multiple waste streams requiring segregation, increasing the number of bag categories stocked and used across departments.

Biohazard Bags Market Drivers

Increasing Regulatory Emphasis on Biomedical Waste Segregation

Regulatory oversight of biomedical waste segregation continues to intensify across both developed and emerging healthcare systems. Facilities are required to separate infectious and hazardous waste streams to reduce exposure risk and ensure compliant treatment and disposal. This creates recurring demand for standardized biohazard bags that meet minimum performance expectations for strength and leakage prevention. As audits and compliance reporting mature, procurement teams increasingly prefer consistent specifications to minimize operational variability and reduce incident risk.

- For instance, Abdos Lifescience’s polypropylene biohazard disposable bags are autoclavable up to 135°C (275°F), are tested to ASTM 1922 and ASTM 1709 standards, and are sold in formats ranging from 12 x 18 inches to 42 x 42 inches, giving healthcare facilities validated performance benchmarks for segregated waste handling.

Rising Diagnostic and Laboratory Throughput

Diagnostic laboratories and research environments generate high volumes of disposable consumables that require controlled containment. Growth in routine diagnostics, preventive screening, and test-panel expansion increases the daily waste load that must be safely packaged. Biohazard bags support workflow continuity because they are integral to point-of-generation disposal practices at benches, sampling stations, and processing areas. As lab networks expand and turnaround expectations tighten, buyers prioritize bag reliability and ease of handling to avoid disruption and rework.

- For instance, Apollo Diagnostics’ Digi-Smart Central Reference Laboratory in Chennai spans 45,000 square feet, integrates five major lab disciplines, cuts sample turnaround time by 60%, and is designed to process more than 100,000 samples per day, directly illustrating how higher-throughput testing environments intensify demand for dependable biohazard waste packaging at the point of generation.

Expansion of Healthcare Infrastructure and Service Access

Hospital expansion, new clinics, and growth in outpatient care broaden the installed base of sites that must comply with regulated waste practices. Larger facilities typically operate structured waste collection routes and centralized storage, which supports higher usage of larger-capacity and reinforced bag formats. As healthcare systems scale, procurement contracts may shift toward higher-volume supply arrangements that secure consistent availability. This increases baseline demand for biohazard bags as routine consumables supporting infection control and safe disposal.

Operational Focus on Safety, Handling Efficiency, and Standardization

Healthcare and laboratory organizations increasingly focus on reducing handling events and minimizing exposure risks through standardized waste workflows. Bag selection is influenced by compatibility with carts, bins, and treatment pathways, including requirements for strength, closure performance, and clear labeling. Standardization reduces training complexity for staff and improves consistency across shifts and departments. This driver supports steady replacement demand and encourages adoption of bag types optimized for internal transport and consolidated collection.

Biohazard Bags Market Challenges

Purchasing decisions remain highly sensitive to compliance risk, which raises expectations for consistent manufacturing quality and performance across lots. Variability in thickness, print quality, or sealing performance can create operational disruption and lead to rejections in centralized procurement systems. At the same time, buyers often face cost pressure and may seek lower-price alternatives, increasing competition among suppliers and complicating long-term contract stability. These factors make quality assurance, traceability, and reliable supply continuity critical for manufacturers.

- For instance, DuPont’s Tyvek® Healthcare Packaging platform is compatible with four commonly used sterilization methods: ethylene oxide, radiation (gamma and electron beam), steam under controlled conditions, and low-temperature oxidative sterilization, which supports more standardized packaging validation across healthcare manufacturing lines.

Logistics and disposal ecosystems differ by country and even by city, which complicates product standardization across multi-site healthcare networks. Facilities may require different bag colors, labeling rules, or handling compatibility based on local regulations and treatment capacity. This increases SKU complexity and can elevate inventory burden for both suppliers and healthcare distributors. As a result, suppliers must balance customization with scalable manufacturing and ensure documentation supports compliance across varied regulatory frameworks.

Biohazard Bags Market Trends and Opportunities

Procurement teams are increasingly prioritizing workflow-fit products that reduce handling time and improve segregation discipline, creating opportunity for differentiated designs such as reinforced formats and clear labeling systems. Facilities also seek bag compatibility with common waste carts, bin liners, and closure solutions to improve operational consistency. As infection-control programs mature, buyers may consolidate suppliers that can deliver consistent performance across multiple sites and support standardized purchasing programs. These shifts favor suppliers with broad portfolios, reliable availability, and established distribution reach.

Sustainability requirements are entering procurement discussions, encouraging exploration of alternative materials, downgauging strategies, and improved material efficiency without compromising performance. However, regulated waste containment still demands strict durability and leak prevention, meaning product innovation must preserve compliance-grade safety. Suppliers that can validate performance while offering improved material efficiency can strengthen their positioning in institutional tenders. Expanded healthcare access in emerging markets also supports long-term volume growth across hospitals, clinics, and diagnostics networks.

- For instance, Revolution Bag states that its can liners contain up to 97% post-consumer recycled content and average 70% PCR, while Berry Global reports that its ProTechnology films can use up to 25% less film by weight than conventional formats without affecting film quality or end-use results, showing how suppliers are pursuing measurable material-efficiency gains while maintaining functional performance expectations.

Regional Insights

North America

North America accounted for 37.4% of the Biohazard Bags Market revenue in 2025, supported by structured biomedical waste handling practices and mature compliance-driven procurement. Hospitals and laboratory networks typically standardize bag specifications, enabling recurring replenishment cycles and stable demand. The region benefits from established medical waste service ecosystems that reinforce routine use of compliant containment products. Demand is further supported by consistent activity across inpatient care, outpatient procedures, and diagnostic testing.

Europe

Europe represented 19.0% of global revenue in 2025, reflecting strong institutional adoption of regulated waste segregation and established healthcare infrastructure. Buyers generally emphasize compliance documentation, performance consistency, and supplier reliability. Waste handling is often integrated into broader environmental and occupational safety practices, reinforcing demand for standardized containment consumables. Product selection tends to align closely with facility-level protocols and local regulatory interpretation.

Asia Pacific

Asia Pacific captured 32.2% of the market in 2025, driven by expanding healthcare capacity, increasing diagnostic penetration, and formalization of waste management practices across large population centers. Growing hospital networks and laboratory services broaden the installed base of compliant waste handling sites. Procurement is increasingly professionalized in major systems, supporting adoption of standardized bag types and sizes. The region also shows strong growth momentum as healthcare access and regulated waste handling requirements expand.

Latin America

Latin America held 6.4% of global revenue in 2025, supported by gradual strengthening of biomedical waste practices in major urban healthcare systems. Demand is often concentrated in higher-capacity hospitals and private diagnostic networks that follow structured procurement. Variability in enforcement and infrastructure can create uneven adoption across geographies, but institutional segments continue to expand. Suppliers with flexible distribution and regionally adapted product offerings are better positioned to capture growth.

Middle East & Africa

The Middle East & Africa accounted for 5.0% of revenue in 2025, with demand largely centered in modern hospitals, diagnostic hubs, and larger research institutions. Growth is supported by healthcare infrastructure investment and increasing use of standardized infection-control practices. Waste management maturity varies across countries, which influences product mix and procurement consistency. Suppliers that can deliver reliable quality and support compliance documentation tend to gain preference in institutional tenders.

Competitive Landscape

Competition in the Biohazard Bags Market is shaped by product performance consistency, portfolio breadth across sizes and materials, and the ability to support compliance-oriented institutional procurement. Suppliers differentiate through manufacturing quality controls, puncture and tear resistance performance, sealing compatibility, and availability across distributor networks. Larger participants often benefit from scale in engineered films, access to healthcare procurement channels, and the ability to offer adjacent containment or waste-management solutions. Contract reliability and fulfillment consistency remain key purchasing criteria, especially for hospitals and laboratory chains.

Thermo Fisher Scientific Inc. is positioned strongly through broad laboratory and healthcare distribution reach and a portfolio that aligns with routine procurement needs in clinical and research environments. The company benefits from established relationships with laboratories and healthcare buyers that prioritize consistent supply and standardized specifications. Its approach typically supports multi-site buyers seeking streamlined procurement across consumables categories. This positioning aligns well with recurring demand dynamics where biohazard bags are purchased as frequent-use containment products.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In September 2025, Medline Industries expanded its product range by launching a new line of eco-friendly, fully biodegradable biohazard bags specifically designed for hospitals and diagnostic laboratories. In response to the growing demand for sustainable healthcare waste management, these bags were engineered to address environmental compliance goals while maintaining safe, leak-proof containment of infectious waste.

- In July 2025, Inteplast Group acquired German plastics manufacturer Perga, marking Inteplast’s first major investment in Europe and adding advanced film products for sheets, bags, and packaging through its Inteplast Engineered Films division.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 507.64 million |

| Revenue forecast in 2032 |

USD 763.3 million |

| Growth rate (CAGR) |

6% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Capacity, By Material, By Type, By End Use |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Thermo Fisher Scientific Inc., SP Bel-Art, International Plastics Inc., Transcendia, Inc., Stericycle, Inc., Daniels Health, Inteplast Group, Merck KGaA, Veolia, Abdos Labtech Private Limited |

| No. of Pages |

328 |

Segmentation

By Capacity

- Less than 15 Gallon

- 15 to 35 Gallon

- More than 35 Gallon

By Material

- HDPE

- LDPE

- Cellophane

- Polypropylene

By Type

- Non-Transparent Bags

- Transparent Bags

- Reinforced Bags

- Colored Bags

By End Use

- Hospitals

- Clinics

- Diagnostic Laboratories

- Pharmaceutical Laboratories

- Research Laboratories

- Chemical Industry

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa