Biological Skin Substitutes Market Overview:

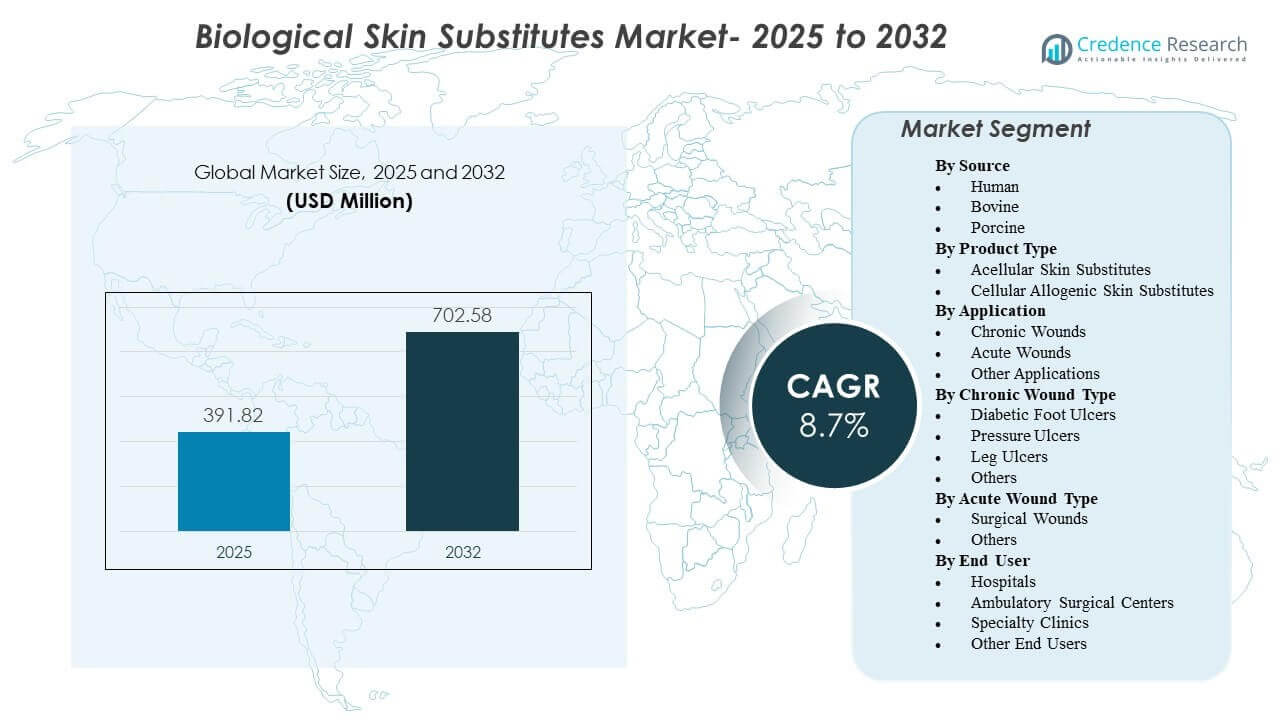

The global Biological Skin Substitutes Market size was estimated at USD 391.82 million in 2025 and is expected to reach USD 702.58 million by 2032, growing at a CAGR of 8.7% from 2025 to 2032. Demand expansion is primarily supported by the rising burden of chronic wounds that require advanced closure support when conventional care pathways fail to deliver predictable healing outcomes. Adoption is also reinforced by increasing use in complex surgical wound management and broader access to specialized wound care capabilities across both inpatient and outpatient settings.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biological Skin Substitutes Market Size 2025 |

USD 391.82 million |

| Biological Skin Substitutes Market, CAGR |

8.7% |

| Biological Skin Substitutes Market Size 2032 |

USD 702.58 million |

Key Market Trends & Insights

- North America represented 40.6% of global revenue in 2025, reflecting strong utilization in advanced wound care pathways.

- Asia Pacific accounted for 31.2% of global revenue in 2025, supported by expanding wound care capacity and rising chronic disease prevalence.

- Europe captured 19.8% of global revenue in 2025, reflecting steady demand in mature clinical and reimbursement environments.

- Acellular Skin Substitutes held the largest product share at 56.1% in 2025, supported by off-the-shelf availability and workflow fit.

- Chronic Wounds represented 58.6% of application revenue in 2025, driven by higher treatment intensity and longer healing cycles.

Segment Analysis

Biological skin substitutes are increasingly positioned as escalation therapies for wounds that stall under standard care, particularly in chronic wound categories where prolonged treatment timelines raise both clinical and economic pressure. Patient complexity continues to rise as comorbidities such as diabetes and vascular disease increase the likelihood of delayed healing and recurrent wound episodes. As a result, wound care teams are prioritizing products with consistent handling characteristics, clearer clinical pathways, and evidence narratives aligned to payer expectations.

Product selection is also influenced by operational fit across care settings. Many providers favor solutions that simplify storage, preparation, and application, especially in high-throughput wound clinics and hospital departments managing a mix of surgical wounds, trauma, and chronic ulcer care. In parallel, purchasing decisions increasingly reflect the total cost of care logic, including fewer complications, fewer re-interventions, and improved closure rates in harder-to-heal wounds.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Source Insights

Human accounted for the largest share of 44.2% in 2025. Human-derived substitutes remain preferred in cases where clinicians prioritize biocompatibility and matrix characteristics that resemble native tissue architecture. Clinical familiarity and established processing approaches also support repeat utilization in complex wound care protocols. However, supply considerations and cost sensitivities sustain ongoing use of bovine and porcine sources in broader wound coverage needs.

By Product Type Insights

Acellular Skin Substitutes accounted for the largest share of 56.1% in 2025. Acellular products align well with routine workflows due to easier handling, storage practicality, and broad applicability across common wound presentations. Off-the-shelf readiness reduces delays in application and supports standardization across facilities. Cellular allogenic products remain important for more challenging wounds where active biologic signaling and regenerative support are prioritized.

By Application Insights

Chronic Wounds accounted for the largest share of 58.6% in 2025. Chronic wounds typically require longer treatment duration, multiple interventions, and closer monitoring, which increases the likelihood of using advanced skin substitutes. Escalation protocols in diabetic foot ulcers, venous leg ulcers, and pressure ulcers often incorporate skin substitutes once progress plateaus under standard care. The chronic wound burden also drives more frequent specialist referrals, strengthening product utilization in dedicated wound care programs.

By Chronic Wound Type Insights

Diabetic foot ulcers, pressure ulcers, and leg ulcers collectively contribute to persistent demand due to recurrence risk and prolonged healing timelines. Diabetic foot ulcers often require advanced closure support because neuropathy and perfusion issues can limit healing momentum. Pressure ulcers remain closely tied to aging populations and long-stay care pathways where prevention failures can lead to complex wounds. Leg ulcers, commonly associated with venous insufficiency, can be difficult to resolve without adjunctive biologic therapies when conservative approaches do not sustain closure.

By Acute Wound Type Insights

Surgical wounds represent a key acute segment because closure quality and complication avoidance are central to post-operative outcomes. Complex surgeries and patients with comorbidities increase the likelihood of delayed healing, dehiscence, or infection risk, which can elevate the use of biologic coverage. Trauma and burn-related acute wounds also support demand where rapid coverage and reduced complication risk are priorities. Product choice is often influenced by operating room workflow constraints and post-acute follow-up capabilities.

By End User Insights

Hospitals accounted for the largest share of 53.4% in 2025. Hospitals manage higher-acuity wound cases, including burns, trauma, and surgical complications, where advanced biologic substitutes are more frequently indicated. Centralized procurement and multidisciplinary wound teams also support standardization of preferred products and protocols. Ambulatory surgical centers and specialty clinics are expanding utilization as more wound care shifts to outpatient settings and same-day pathways increase.

Biological Skin Substitutes Market Drivers

Rising Chronic Wound Burden and Escalation to Advanced Therapies

Biological skin substitutes benefit from increasing prevalence of chronic wounds associated with diabetes, vascular disease, obesity, and aging populations. Chronic wounds frequently require longer treatment timelines and repeated interventions, which raises demand for regenerative adjuncts. Clinical pathways often escalate to skin substitutes when standard care does not deliver adequate healing progression. As chronic wound management becomes more standardized, utilization becomes less episodic and more protocol-driven across care sites.

Workflow Fit and Operational Advantages in Wound Care Delivery

Off-the-shelf availability and consistent handling characteristics support broader adoption across hospital departments and outpatient wound clinics. Facilities increasingly value products that simplify storage, preparation, and application steps, particularly where staffing and throughput pressures exist. Standardized protocols also reduce variability in product choice and reinforce repeat purchasing behavior. Operational fit becomes especially important as wound care expands beyond specialist centers into broader clinical networks.

- For instance, MIMEDX states that EPIFIX is stored at room temperature, has a 5-year shelf life, is compatible with offloading, compression, negative pressure wound therapy, and hyperbaric oxygen therapy, and is processed to preserve 250+ regulatory proteins. Standardized protocols also reduce variability in product choice and reinforce repeat purchasing behavior.

Increasing Procedure Volumes and Complex Surgical Wound Management

Surgical and post-surgical wound complications can require advanced coverage solutions to improve closure outcomes and reduce downstream interventions. Growth in procedures among patients with comorbidities increases the need for wound management solutions that support predictable healing. Biologic substitutes are also used in settings where complications can extend length of stay and elevate costs. These dynamics strengthen the market beyond traditional chronic wound use cases.

- For instance, Kerecis reported in a comparative study of 170 full-thickness biopsy wounds that its Omega3 fish-skin graft achieved a healing hazard ratio of 2.34 versus human amnion membrane and delivered 10% more fully healed wounds by day 28. Biologic substitutes are also used in settings where complications can extend length of stay and elevate costs.

Evidence Expectations and Purchasing Alignment to Value-Based Care

Payers and providers increasingly emphasize clinical evidence, patient outcomes, and total cost of care when evaluating advanced wound products. Facilities align product selection to pathways that support fewer complications, fewer re-applications, and improved closure performance in difficult wounds. This environment favors suppliers that can support formulary decisions with clinical data and education programs. As value-based care expands, procurement decisions increasingly focus on measurable outcomes rather than unit price alone.

Biological Skin Substitutes Market Challenges

Reimbursement complexity and evolving payment mechanisms can create uncertainty for product utilization across outpatient and ambulatory settings. Providers may face variability in coverage criteria, coding alignment, and documentation requirements, which can slow adoption even when clinical demand is clear. Budget scrutiny can also intensify product evaluation cycles, requiring stronger evidence and clearer pathway alignment to secure formulary access. These barriers can disproportionately affect smaller suppliers or newer product entrants.

Clinical heterogeneity across wound types and patient profiles can make outcomes less predictable, creating adoption friction and inconsistent product usage patterns. Differences in wound severity, infection risk, perfusion status, and adherence to follow-up can influence performance, which complicates standardized procurement decisions. Training gaps and inconsistent application techniques can also reduce perceived effectiveness in real-world settings. As a result, suppliers must invest in education, protocol support, and site-level implementation to sustain utilization.

- For instance, KCI (an Acelity company) directly quantified the impact of adherence variability on its iOn PROGRESS™ Remote Therapy Monitoring system for negative pressure wound therapy (NPWT): patients with less than 60% therapy compliance achieved a daily wound volume reduction rate of only 1.42%, whereas patients maintaining 90–100% compliance improved to 2.23% daily wound volume reduction—a 57% performance differential driven entirely by usage consistency, not by any change in the underlying product.

Market Trends and Opportunities

A key trend is the shift toward more structured wound care pathways that define when and how biological substitutes are used after standard care stalls. Protocol-driven escalation supports repeatability and enables facilities to measure outcomes more consistently. This trend creates opportunity for suppliers to embed products into clinical pathways through education, evidence packages, and decision-support tools. Expansion of integrated wound care programs also supports more consistent demand across care networks.

- For instance, Organogenesis developed a real-world evidence package for its Apligraf bilayer living cell therapy, drawing on comparative effectiveness data showing that Apligraf closed venous leg ulcers 52% faster than TheraSkin with a median closure time of 15 weeks versus 31 weeks and 44% faster than Oasis, with a median of 24 weeks versus 43 weeks.

Another trend is the growth of outpatient wound care capacity as more procedures and follow-up shift away from inpatient settings. Specialty clinics and ambulatory centers increasingly manage complex wounds with standardized follow-up schedules and focused expertise. This creates opportunities for products that support streamlined application, predictable handling, and efficient inventory management. Suppliers that align offerings to outpatient workflow constraints and payer documentation needs are positioned to gain incremental share.

Regional Insights

North America

North America led global demand with 40.6% revenue share in 2025, supported by high adoption of advanced wound care products, established clinical pathways, and a broad base of specialized wound care programs. Provider focus on measurable outcomes encourages use of biologic substitutes in difficult-to-heal wounds. Hospital systems and outpatient networks also enable standardized procurement and repeat utilization. The region remains a primary commercialization market for products backed by strong clinical evidence and workflow fit.

Europe

Europe accounted for 19.8% of global revenue in 2025, reflecting steady demand supported by mature clinical practices and broad access to wound care services in many countries. Adoption is shaped by reimbursement structures, evidence requirements, and procurement processes that emphasize cost-effectiveness. Hospitals remain central to complex surgical wound management, while outpatient settings continue to expand specialized wound care. Suppliers often compete through portfolio breadth, clinical validation, and alignment to national procurement pathways.

Asia Pacific

Asia Pacific captured 31.2% revenue share in 2025 and showed strong momentum driven by expanding healthcare infrastructure and rising prevalence of diabetes and other chronic conditions linked to wound incidence. Growth in specialized wound care capacity and improving access to advanced therapies support broader adoption. Hospitals drive early uptake, with specialty clinics increasingly expanding utilization as capabilities mature. Suppliers offering scalable training and cost-aligned product options are better positioned across diverse healthcare systems.

Latin America

Latin America represented 5.3% of global revenue in 2025 and remains smaller in share, but is supported by gradual expansion of specialty wound care and rising awareness of advanced closure solutions. Adoption is influenced by affordability constraints and variability in reimbursement and hospital budgets. Private healthcare networks and urban centers often lead uptake where specialist capabilities are concentrated. Suppliers typically compete through pricing strategies, distributor reach, and targeted clinical education.

Middle East & Africa

Middle East & Africa accounted for 3.1% of global revenue in 2025, with developing demand as advanced wound care access expands in select countries and major urban healthcare hubs. Utilization is shaped by infrastructure differences, payer coverage variability, and supply-chain considerations. Hospitals and specialty centers are key entry points for advanced skin substitutes, particularly in complex surgical and trauma-related wound care. Growth opportunities improve as wound care programs become more structured and clinician training expands.

Competitive Landscape

Competition in the Biological Skin Substitutes Market is shaped by portfolio breadth, clinical evidence positioning, and the ability to support standardized wound care protocols across inpatient and outpatient settings. Suppliers differentiate through product handling characteristics, indication coverage, and education support that improves real-world outcomes. Market participants also compete on procurement alignment, distributor reach, and the ability to demonstrate value through reduced complications and improved closure performance. Strong relationships with wound care teams and health systems help sustain repeat purchasing and formulary positioning.

Organogenesis Inc. remains a prominent participant through focus on advanced wound care solutions and continued emphasis on clinical adoption pathways. Product positioning benefits from alignment to complex wound management needs, particularly where escalation beyond standard care is required. The company approach typically combines clinical education, evidence development, and commercial execution across major care settings. Ongoing engagement with reimbursement and market access dynamics also remains important for sustained utilization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Organogenesis Inc.

- Integra LifeSciences Corporation

- Smith+Nephew

- MIMEDX Group, Inc.

- Vericel Corporation

- Stryker

- 3M

- BioTissue

- Essity Health & Medical

- Tissue Regenix

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In April 2025, AVITA Medical announced the U.S. commercial launch of Cohealyx, a collagen-based dermal matrix designed to support cellular migration and revascularization in full-thickness wounds, and the company said the product was co-developed with Regenity Biosciences.

- In April 2025, LifeNet Health launched Dermacell Porous, a next-generation human acellular dermal matrix processed to retain endogenous growth factors, collagen, and elastin, expanding its regenerative wound solutions portfolio for chronic wound management.

- In July 2025, MiMedx Group entered a collaboration agreement with Vaporox to co-promote and co-market their wound care offerings, while also making an investment in Vaporox and securing certain exclusivity rights tied to possible acquisition discussions.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 391.82 million |

| Revenue forecast in 2032 |

USD 702.58 million |

| Growth rate (CAGR) |

8.7% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Source; By Product Type; By Application; By Chronic Wound Type; By Acute Wound Type; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Organogenesis Inc.; Integra LifeSciences Corporation; Smith+Nephew; MIMEDX Group, Inc.; Vericel Corporation; Stryker; 3M; BioTissue; Essity Health & Medical; Tissue Regenix |

| No.of Pages |

332 |

Segmentation

By Source

By Product Type

- Acellular Skin Substitutes

- Cellular Allogenic Skin Substitutes

By Application

- Chronic Wounds

- Acute Wounds

- Other Applications

By Chronic Wound Type

- Diabetic Foot Ulcers

- Pressure Ulcers

- Leg Ulcers

- Others

By Acute Wound Type

By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Clinics

- Other End Users

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa