Biopharmaceuticals Market

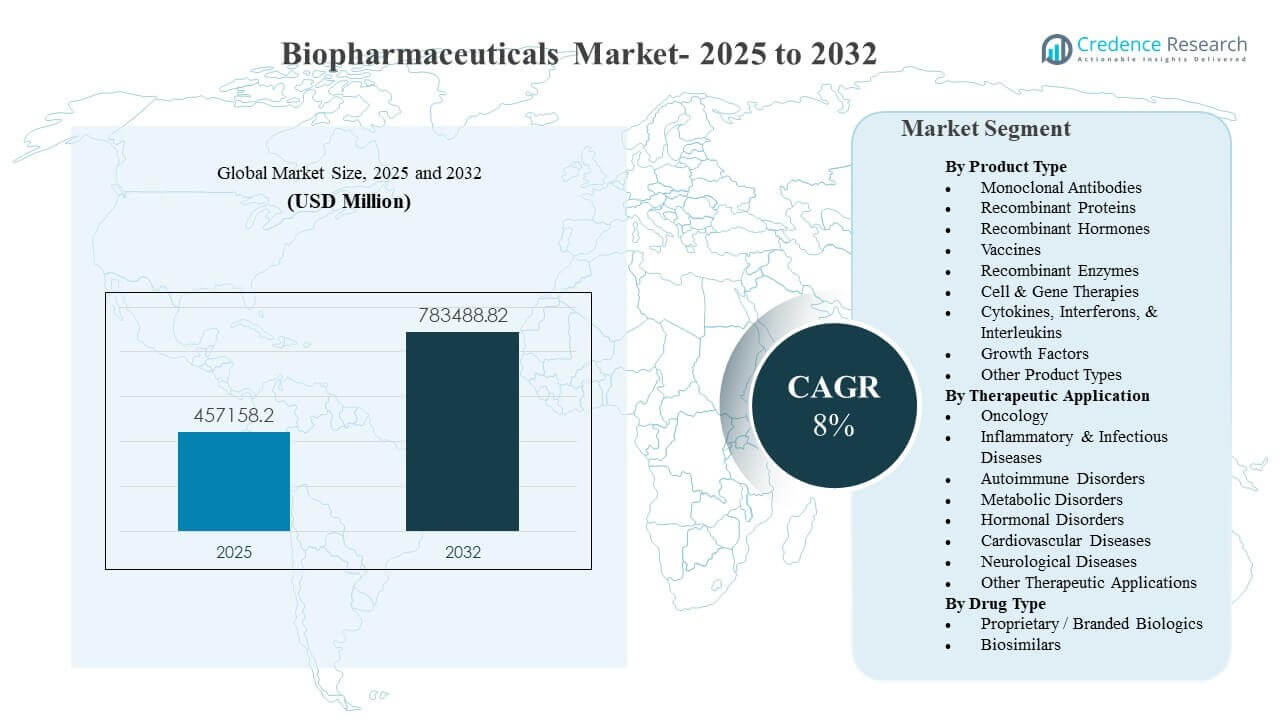

The global Biopharmaceuticals Market size was estimated at USD 457,158.2 million in 2025 and is expected to reach USD 783,488.82 million by 2032, growing at a CAGR of 8% from 2025 to 2032. Growth is primarily driven by sustained demand for targeted and high-efficacy therapies in chronic and specialty indications, supported by continued biologics innovation and broader clinical adoption pathways. Capacity expansion in advanced modalities and improved access in emerging markets continue to add momentum to volume growth across multiple therapeutic categories.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biopharmaceuticals Market Size 2025 |

USD 457,158.2 million |

| Biopharmaceuticals Market, CAGR |

8% |

| Biopharmaceuticals Market Size 2032 |

USD 783,488.82 million |

Key Market Trends & Insights

- The Biopharmaceuticals Market is projected to expand from USD 457,158.2 million in 2025 to USD 783,488.82 million by 2032 at an 8% CAGR (2025–2032).

- North America accounted for an estimated 43.6% share of global revenue in 2025, supported by high biologics utilization and strong specialty reimbursement structures.

- Europe represented an estimated 26.4% share in 2025, underpinned by broad reimbursed access and sizeable treated populations across specialty care.

- Monoclonal Antibodies held the leading product type position at 35.4% share in 2025 due to wide adoption across oncology and immunology pathways.

- Oncology remained the largest therapeutic application at 30.6% share in 2025, reflecting sustained innovation and expanding treatment eligibility across tumor types.

Segment Analysis

Product innovation and clinical preference for targeted mechanisms continue to shape demand across the Biopharmaceuticals Market, with providers and payers favoring therapies that deliver differentiated outcomes in complex disease settings. Manufacturing quality, cold-chain readiness, and scalable supply are increasingly important selection criteria as biologics portfolios broaden and therapy administration expands across more care settings. As treatment pathways become more protocol-driven, providers rely on consistent product performance, reliable availability, and well-supported clinical evidence to guide therapy choices.

Demand patterns also reflect a mix of premium branded biologics and expanding biosimilar adoption in mature markets. Switching policies, tender-based procurement, and formulary optimization are strengthening biosimilars’ role in improving affordability and access, particularly for high-volume categories. At the same time, advanced modalities such as cell and gene therapies are influencing investment priorities, pushing suppliers toward higher-complexity development, specialized manufacturing capabilities, and more robust analytics and release testing.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Monoclonal Antibodies accounted for the largest share of 35.4% in 2025. This leadership is supported by broad applicability across oncology, autoimmune disorders, and inflammatory diseases where targeted binding mechanisms enable strong clinical efficacy. Extensive clinical familiarity and well-established administration pathways improve adoption versus newer modalities with steeper implementation requirements. Continuous antibody innovation, including improved engineering and lifecycle management, helps sustain utilization and supports new indication expansion.

By Therapeutic Application Insights

Oncology accounted for the largest share of 30.6% in 2025. High unmet need and continuous innovation in biologic-based regimens support sustained demand across hematologic and solid tumor settings. Label expansions and combination approaches continue to broaden treated populations and extend therapy durations. Specialized care delivery models and structured treatment protocols further reinforce consistent biologics use in oncology pathways.

By Drug Type Insights

Proprietary / Branded Biologics accounted for the largest share of 76.3% in 2025. Branded biologics maintain revenue leadership through established franchises, differentiated clinical value, and ongoing portfolio upgrades that support premium positioning. Strong physician confidence and stable supply reliability keep branded therapies central in high-acuity and specialty indications. Biosimilars are expanding penetration as more biologics face loss of exclusivity, but branded portfolios continue to dominate where differentiation and lifecycle strategies remain strong.

Biopharmaceuticals Market Drivers

Rising specialty disease burden and protocol-driven biologics adoption

Biopharmaceuticals Market growth is supported by increasing diagnosis and long-term management needs across oncology, autoimmune, metabolic, and neurological conditions. Providers are adopting more targeted therapies as standards of care evolve toward mechanism-specific treatment selection. Protocolization of specialty pathways increases biologics utilization frequency and improves continuity of care. The shift toward measurable outcomes also favors biologics with strong efficacy and durability evidence. In addition, growing use of companion diagnostics and biomarker-led patient selection is improving response rates and reinforcing biologics utilization in specialty pathways.

- For instance, Merck’s KEYTRUDA demonstrates biomarker-led biologics adoption in protocolized specialty care: in the FDA-reviewed KEYNOTE-042 study for first-line NSCLC selected using the PD-L1 IHC 22C3 pharmDx companion diagnostic, median overall survival was 20.0 months versus 12.2 months with chemotherapy in the PD-L1 TPS ≥50% subgroup, and 16.7 months versus 12.1 months in the overall TPS ≥1% population.

Continuous innovation across biologic platforms and advanced modalities

Ongoing innovation in monoclonal antibodies, recombinant proteins, vaccines, and cell and gene therapies expands the clinical utility of biopharmaceuticals. Pipeline progression enables new mechanism-of-action options and supports label expansion into earlier lines of therapy. Platform improvements also enhance manufacturability and consistency, improving commercial scalability. These factors collectively reinforce premium demand and help sustain new product launches across major therapy areas. Moreover, advances in formulation science and delivery systems are helping shift certain biologics toward more convenient administration settings, supporting broader adoption.

Expansion of manufacturing capacity and supply-chain resilience

Biopharmaceuticals Market demand benefits from ongoing investments in manufacturing expansions, process improvements, and quality systems upgrades. Higher capacity supports faster scale-up and reduces supply constraints in high-growth categories. Improved analytics, automation, and quality controls lower deviation risk and strengthen batch reliability. These enhancements increase market confidence and support broader uptake in regions improving access to specialty therapies. Additionally, dual-sourcing strategies and localized fill-finish investments are being used to mitigate geopolitical and logistics-related supply risks.

- For instance, Samsung Biologics announced Plant 5 with 180,000 liters of manufacturing capacity, which will increase the company’s total site capacity to 784,000 liters upon completion, providing a clear example of large-scale biologics manufacturing expansion.

Increasing access through reimbursement expansion and biosimilar-led affordability

Broader insurance coverage, government procurement programs, and payer focus on value-based decision-making are expanding access to biopharmaceutical therapies. Biosimilars are improving affordability and enabling treatment adoption in larger patient cohorts where branded therapy cost is a barrier. Provider education and real-world evidence are supporting switching comfort in mature systems. This combination improves overall utilization volumes and strengthens long-term market expansion. At the same time, stepped-therapy and formulary optimization are increasing volume elasticity, particularly in chronic autoimmune and inflammatory indications.

Biopharmaceuticals Market Challenges

Manufacturing complexity and stringent quality requirements remain major constraints in the Biopharmaceuticals Market. Biologic production is sensitive to process variability, requiring strict controls, validated analytics, and robust release testing to maintain consistency. Capacity is not always flexible across modalities, and specialized facilities can face long lead times to build and qualify. These factors can increase costs and limit rapid response to demand shifts for certain products. Furthermore, workforce shortages in specialized bioprocessing and quality roles can delay tech transfer, validation, and routine production ramp-up.

Pricing pressure and reimbursement scrutiny also influence adoption dynamics, particularly for high-cost biologics and advanced therapies. Payers increasingly evaluate comparative effectiveness and budget impact, which can tighten access criteria and slow uptake in some indications. Tendering and reference pricing can compress margins for mature biologics and accelerate substitution pressure. Companies must balance affordability expectations with sustaining innovation investment and maintaining reliable supply. In addition, variability in national reimbursement timelines and HTA decisions can create uneven launch uptake and delayed patient access across regions.

- For instance, Vertex reported that 53 of 54 evaluable patients with transfusion-dependent beta-thalassaemia treated with its CRISPR-based Casgevy achieved at least 12 consecutive months of transfusion independence, while NICE recommended the therapy specifically for people aged 12 years and over who need regular transfusions and do not have a suitable donor, demonstrating how strong clinical performance can still be paired with tightly defined reimbursement eligibility.

Biopharmaceuticals Market Trends and Opportunities

Biosimilar penetration and competitive tendering are reshaping market access strategies in multiple regions. As more biologics lose exclusivity, biosimilars are expanding their role in improving affordability and increasing treated populations. Companies are responding through portfolio optimization, differentiated service offerings, and improved evidence packages to support market positioning. This trend creates opportunities for manufacturers with strong development capabilities and efficient supply chains. Additionally, interchangeability policies and stronger pharmacovigilance frameworks are improving stakeholder confidence and accelerating biosimilar switching in select markets.

- For instance, Samsung Bioepis and Organon reported that their high-concentration SB5 interchangeability study enrolled 371 patients with moderate to severe plaque psoriasis; after a 13-week lead-in, eligible patients were randomized 1:1, and the trial met all primary pharmacokinetic endpoints, with the 90% confidence interval for AUC ratio at 0.8007 to 1.1115 and for Cmax ratio at 0.8637 to 1.1433, both fully within the predefined 0.80 to 1.25 margin.

Advanced modalities and next-generation biologics are also influencing investment priorities and partnership activity. Cell and gene therapies, engineered antibodies, and improved vaccine platforms require specialized manufacturing and analytics, increasing the strategic importance of technical capabilities. Companies are expanding capacity and building technology partnerships to accelerate development timelines. These moves support long-term opportunities in high-value indications where differentiated outcomes justify adoption. Moreover, modular manufacturing, digital batch release, and AI-enabled process monitoring are emerging as levers to reduce cost of goods and shorten time-to-market for complex biologics.

Regional Insights

North America

North America accounted for 43.6% of the Biopharmaceuticals Market revenue in 2025. High biologics utilization is supported by broad specialty care infrastructure, strong clinical adoption, and a large base of reimbursed patients in chronic and high-acuity indications. The region benefits from deep innovation ecosystems and mature commercialization pathways that support rapid uptake of differentiated therapies. Continued portfolio expansions across oncology, autoimmune, and metabolic categories sustain demand for both established and next-generation biologics.

Europe

Europe represented 26.4% of market revenue in 2025. Regional demand is supported by established reimbursement systems, sizeable treated populations, and strong specialty prescribing across oncology and immunology. Biosimilar-driven affordability initiatives play a meaningful role in expanding access and sustaining volume growth in mature categories. Ongoing investments in manufacturing capabilities and regulatory alignment across key markets support stable supply and consistent adoption.

Asia Pacific

Asia Pacific held 22.6% share in 2025. Growth is supported by expanding access to specialty therapies, improving healthcare coverage, and increasing local manufacturing capabilities across biologics and biosimilars. Larger patient pools and improving diagnostic reach are raising treatment volumes across multiple therapeutic areas. As clinical pathways mature and affordability improves, adoption continues to expand beyond tertiary centers into broader networks.

Latin America

Latin America accounted for 4.8% share in 2025. Market expansion is supported by gradual improvements in access and procurement capacity, particularly in large national health systems and private channels. Adoption remains influenced by pricing sensitivity and variable reimbursement structures across countries. Increased biosimilar availability and targeted public procurement programs are expected to support broader biologics penetration over time.

Middle East & Africa

Middle East & Africa represented 2.6% of revenue in 2025. Demand is concentrated in higher-income markets with stronger specialty infrastructure and expanding access initiatives, while many countries remain constrained by affordability and distribution limitations. Growth is supported by gradual expansion of tertiary care capacity and improving availability of essential biologics. Increased focus on supply-chain reliability and specialty care build-out supports incremental adoption.

Competitive Landscape

Competition in the Biopharmaceuticals Market is shaped by portfolio breadth, differentiated clinical evidence, manufacturing reliability, and lifecycle management capabilities. Leading companies compete through new product launches, label expansions, platform innovation, and strategic partnerships that strengthen development pipelines and manufacturing resilience. Biosimilar competition is increasing in mature therapy areas, driving pricing pressure and raising the importance of operational efficiency and evidence-based positioning. Investment in advanced modalities and supply-chain capabilities is becoming a key differentiator as product complexity increases.

Pfizer Inc. continues to compete through a combination of broad therapeutic coverage, development scale, and commercial execution in high-volume and specialty categories. The company’s approach emphasizes portfolio optimization, targeted innovation, and strategic deal activity to strengthen future pipelines and address large-scale disease areas. Pfizer’s scale supports manufacturing readiness and commercialization reach across major markets. Continued focus on differentiated assets and lifecycle planning helps sustain competitiveness across evolving therapy areas.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Pfizer Inc.

- AbbVie Inc.

- Merck & Co., Inc.

- F. Hoffmann-La Roche Ltd.

- Novartis AG

- Johnson & Johnson Services, Inc.

- Bristol-Myers Squibb Company

- Sanofi

- GSK plc

- AstraZeneca

- Takeda Pharmaceutical Company Limited

- Eli Lilly and Company

- Amgen Inc.

- Biogen

- Novo Nordisk A/S

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is qualitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In December 2025, BioMarin Pharmaceutical agreed to acquire Amicus Therapeutics for $4.8 billion, in a transaction expected to close in the second quarter of 2026, substantially expanding BioMarin’s rare genetic disease portfolio. This deal represented a strategic shift for BioMarin under CEO Alexander Hardy, moving from being a perennial acquisition target to becoming an active acquirer in the rare disease space.

- In January 2026, GlaxoSmithKline (GSK) committed $2.2 billion to acquire RAPT Therapeutics, a clinical-stage biopharmaceutical company focused on inflammatory and immunologic disease drug development. This deal added a differentiated pipeline of oral therapies targeting immune-mediated diseases, complementing GSK’s existing immunology and inflammation portfolio.

- In January 2026, Eli Lilly announced the acquisition of Ventyx Biosciences, a clinical-stage company developing oral therapies for inflammation-mediated diseases, for an aggregate equity value of approximately $1.2 billion. This acquisition strengthened Lilly’s immunology pipeline and added novel oral assets to complement its existing biologics-focused inflammation portfolio.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 457,158.2 million |

| Revenue forecast in 2032 |

USD 783,488.82 million |

| Growth rate (CAGR) |

8% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type, By Therapeutic Application, By Drug Type |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Pfizer Inc., AbbVie Inc., Merck & Co., Inc., F. Hoffmann-La Roche Ltd., Novartis AG, Johnson & Johnson Services, Inc., Bristol-Myers Squibb Company, Sanofi, GSK plc, AstraZeneca, Takeda Pharmaceutical Company Limited, Eli Lilly and Company, Amgen Inc., Biogen, Novo Nordisk A/S companies |

| No.of Pages |

330 |

Segmentation

By Product Type

- Monoclonal Antibodies

- Recombinant Proteins

- Recombinant Hormones

- Vaccines

- Recombinant Enzymes

- Cell & Gene Therapies

- Cytokines, Interferons, & Interleukins

- Growth Factors

- Other Product Types

By Therapeutic Application

- Oncology

- Inflammatory & Infectious Diseases

- Autoimmune Disorders

- Metabolic Disorders

- Hormonal Disorders

- Cardiovascular Diseases

- Neurological Diseases

- Other Therapeutic Applications

By Drug Type

- Proprietary / Branded Biologics

- Biosimilars

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa