Bioprocess Analyzers Market

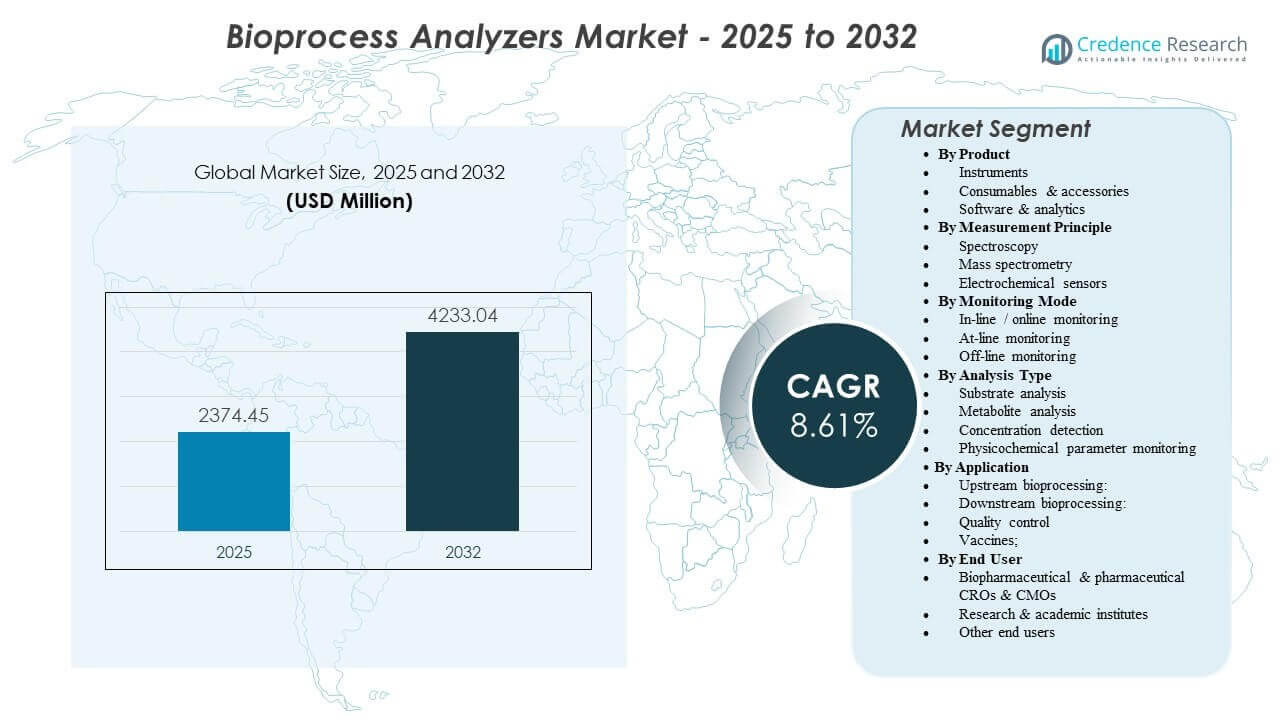

The global Bioprocess Analyzers Market size was estimated at USD 2,374.45 million in 2025 and is expected to reach USD 4,233.04 million by 2032, growing at a CAGR of 8.61% from 2025 to 2032. Expansion of biologics manufacturing capacity and tighter expectations for process control are increasing the need for rapid measurement of critical quality and process parameters across upstream and downstream operations. Demand is also supported by broader adoption of real-time monitoring workflows that reduce batch variability and shorten development-to-scale-up timelines.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bioprocess Analyzers Market Size 2025 |

USD 2,374.45 million |

| Bioprocess Analyzers Market, CAGR |

8.61% |

| Bioprocess Analyzers Market Size 2032 |

USD 4,233.04 million |

Key Market Trends & Insights

- The market is projected to expand from USD 2,374.45 million (2025) to USD 4,233.04 million (2032) at a 8.61% CAGR (2025–2032).

- North America accounted for 40.31% of global revenue in 2025, reflecting high concentration of commercial biomanufacturing sites and analytical infrastructure.

- Instruments held 58.47% share in 2025, supported by installed-base expansion and validation-driven purchasing in regulated manufacturing.

- Raman spectroscopy represented 41.56% share in 2025, reflecting preference for non-destructive, in-line compatible measurement in bioprocess environments.

- Vaccines captured 32.68% share in 2025, driven by high-volume production and stringent in-process control requirements.

Segment Analysis

Bioprocess analyzers are increasingly selected as part of end-to-end control strategies, where measurement hardware and data workflows are deployed together to support faster decision-making and more consistent batches. Buyers prioritize platforms that can scale from process development to manufacturing with repeatable performance, robust calibration routines, and integration into automation and control systems. In parallel, analytics adoption is rising as teams standardize data integrity practices and look to reduce manual interpretation in high-throughput environments.

The market is also shaped by a shift toward continuous and near-continuous monitoring across critical steps, particularly where tighter control windows materially affect yield, product quality, and release readiness. As biomanufacturing footprints expand globally, procurement decisions increasingly weigh lifecycle support, validation documentation, interoperability, and the ability to run multiple assays or parameters with minimal sampling burden.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Insights

Instruments accounted for the largest share of 58.47% in 2025. Instruments lead because regulated manufacturing environments favor validated, repeatable hardware platforms that can be standardized across suites and sites. Expansion of installed bioreactor and purification capacity increases demand for core measurement systems that can support multiple unit operations. Instrument performance requirements around uptime, traceability, and integration with automation systems also reinforce preference for established platforms with proven service coverage.

By Measurement Principle / Technology Insights

Raman spectroscopy accounted for the largest share of 41.56% in 2025. Raman leads due to suitability for in-line deployment, minimal sample preparation, and compatibility with aqueous bioprocess environments where non-destructive measurement is valuable. Teams can build chemometric models during development and transfer them into manufacturing workflows to reduce scale-up risk and improve control. The ability to generate rich spectral fingerprints supports broader monitoring of process dynamics beyond single-analyte measurement.

By Monitoring Mode Insights

In-line and online monitoring is increasingly prioritized where real-time feedback can reduce sampling burden and enable faster corrective actions during critical process steps. At-line workflows remain widely used where speed is needed but integration complexity must be controlled, especially in multiproduct facilities and development settings. Off-line monitoring continues to play a role for confirmatory testing, method development, and use cases where probe placement is impractical or where additional analytical rigor is required for release readiness.

By Analysis Type Insights

Substrate analysis accounted for the largest share of 45.62% in 2025. Substrate monitoring leads because nutrient control is central to productivity and consistency in many upstream processes, particularly in high-density cultures. Tight tracking of key inputs supports stable growth kinetics and reduces variability that can carry into downstream purification and quality attributes. Standardized substrate workflows are also easier to validate and embed into routine operating procedures, supporting high utilization across sites.

By Application Insights

Vaccines accounted for the largest share of 32.68% in 2025. Vaccine production drives sustained analyzer demand due to high lot volumes, strict process control needs, and frequent monitoring of critical parameters across manufacturing stages. Manufacturing lines often require rapid detection and trending to maintain consistency and reduce deviations that affect throughput. The emphasis on robust in-process control and efficient release readiness increases analyzer utilization intensity across both production and quality workflows.

By End User Insights

Biopharmaceutical & pharmaceutical companies accounted for the largest share of 58.74% in 2025. Large biopharma and pharma organizations lead because they operate broad internal development and manufacturing footprints that require standardized monitoring, validation, and documentation practices. Internal process development teams also invest in analyzers to improve scalability and de-risk tech transfer into manufacturing. Multi-site standardization and lifecycle support requirements further favor enterprise deployments within these organizations.

Bioprocess Analyzers Market Drivers

Expansion of biologics manufacturing capacity

Biopharma companies and contractors continue to expand capacity to support growing demand for complex biologics, vaccines, and advanced therapies. Each added suite increases the need for reliable measurement of process parameters and material quality. As facilities scale, organizations seek standardized analyzer platforms to ensure comparability across lines. This raises demand for validated instruments, consistent methods, and integrated data workflows across sites. Capacity additions also increase the number of sampling points and monitoring steps per batch, lifting analyzer utilization rates. Large multi-site networks further prioritize harmonized analytics to support faster tech transfer and consistent batch release decisions.

- For instance, Lonza’s Vacaville site in California has reached a total biologics capacity of 332,000 liters across 19 mammalian bioreactors, requiring site-wide standardization of process analyzers and monitoring workflows to support late-stage and commercial production.

Increased focus on real-time process understanding and control

Manufacturers are tightening control windows to improve yield consistency and reduce deviations. Real-time or near-real-time measurement enables faster intervention when processes drift, reducing batch risk. In-line capable technologies support continuous visibility into critical parameters without heavy manual sampling. These requirements drive adoption of analyzer systems that integrate with control architectures and enable automated trending. Real-time insights also support faster root-cause investigations by linking process shifts to upstream inputs and operating conditions. Over time, this reduces deviation-related downtime and improves overall equipment effectiveness in high-throughput facilities.

- For instance, Thermo Scientific’s MarqMetrix Process Raman Analyzer has been used for in-line monitoring of high-density perfusion cultures at 100–130 million cells per milliliter over a 50‑day continuous bioreactor run, enabling real-time control of glucose, lactate, ammonium, product titer, and cell viability without off-line sampling.

Growth of outsourcing to CROs and CMOs

Outsourcing increases the number of production environments that need flexible analyzer deployments capable of handling multiple client processes. Contractors must demonstrate robust monitoring and documentation to meet customer and regulatory expectations. This supports demand for multi-application analyzer platforms and strong service models. The result is broader buying across mid-sized and large contractors, not only the largest biopharma manufacturers. Multi-client operations also increase the need for rapid changeovers and standardized reporting across programs. As contractors scale, they invest in analyzer platforms that can be qualified once and deployed repeatedly across different molecules and unit operations.

Rising importance of data integrity and compliant analytics workflows

Regulated manufacturing places strong emphasis on traceability, auditability, and consistent reporting. Analyzer platforms that pair instruments with software and analytics help standardize data capture and reduce manual transcription risk. Centralized data workflows also improve comparability across development and manufacturing. These factors increase the strategic value of analyzers as part of compliant operating systems. Organizations also seek stronger governance of metadata, user access, and audit trails to satisfy data integrity expectations. This elevates demand for validated software layers that integrate analyzers with LIMS, MES, and quality management systems.

Bioprocess Analyzers Market Challenges

Bioprocess analyzer deployment can be constrained by integration complexity, particularly when legacy automation systems, heterogeneous instruments, and site-specific workflows must be connected. Validation requirements and change-control processes can extend timelines for installation and method transfer. In multi-product facilities, maintaining consistent performance across varied process conditions adds additional burden to model maintenance and calibration routines. Connectivity limitations and differing site standards can slow harmonization across global manufacturing networks. Operational teams may also face downtime or production scheduling constraints that limit when upgrades and qualification activities can be executed.

- For instance, in an Emerson PAT deployment at a commercial biologics site, integrating multivariate analyzers into an existing DeltaV control system required configuring more than 200 new I/O tags and mapping over 50 real-time PAT parameters into the historian before routine “golden batch” fingerprinting across campaigns became possible.

Cost and skills constraints also influence adoption, especially for advanced measurement technologies that require specialized method development and data interpretation. Organizations may face limited internal expertise for chemometric modeling, instrument qualification, and ongoing lifecycle management. Procurement teams also weigh total cost of ownership, including consumables, service contracts, and training, which can slow upgrades in budget-constrained settings. Budget pressure is amplified when ROI is difficult to quantify across multiple processes with different batch economics. Skills gaps can also create reliance on vendors or consultants, increasing ongoing operating costs and extending troubleshooting cycles.

Bioprocess Analyzers Market Trends and Opportunities

Adoption of integrated hardware–software workflows is accelerating as manufacturers aim to standardize measurement, trending, and compliance reporting across sites. Platforms that support interoperability, centralized analytics, and robust audit trails are gaining preference. This creates opportunities for vendors that can deliver end-to-end solutions with clear validation packages and strong lifecycle support. Vendors that offer scalable architectures and pre-built integration connectors can shorten deployment timelines and reduce IT burden. Standardized workflows also enable faster onboarding of new sites and smoother method transfer from development to manufacturing.

- For instance, chromatography data systems such as Waters Empower and Agilent OpenLab maintain immutable audit logs for every injection and reprocessing event, which can be referenced during method transfer to replicate integration parameters and review histories when deploying analytical methods from development labs into commercial QC environments.

Another opportunity lies in expanding use of real-time monitoring to reduce sampling burden and shorten cycle times in both upstream and downstream steps. In-line sensing and faster at-line workflows are increasingly used to improve responsiveness and reduce batch variability. Vendors that can simplify deployment, improve model transferability, and deliver stable performance across changing process conditions are positioned to capture higher adoption in scaled manufacturing footprints. Real-time monitoring also supports earlier detection of excursions, reducing scrap risk and improving batch success rates. As continuous and hybrid manufacturing grows, demand should rise for sensors and analyzers that can operate reliably over long run times with minimal intervention.

Regional Insights

North America

North America represented 40.31% of market revenue in 2025, supported by high concentration of commercial biologics manufacturing, strong investment in process development, and established adoption of compliant monitoring workflows. Organizations in the region continue to standardize analyzer platforms across suites to improve comparability and reduce deviation risk. Purchasing decisions often prioritize validation readiness, service coverage, and integration into automation and quality systems.

Europe

Europe accounted for 26.88% of revenue in 2025, supported by mature biologics production and strong expectations around quality systems and documentation. Manufacturers emphasize robust measurement routines to maintain consistent product profiles across batches and sites. Demand is reinforced by continued investment in bioprocessing infrastructure and the need for standardized methods across regional networks.

Asia Pacific

Asia Pacific held 22.41% share in 2025, driven by expanding manufacturing footprints and increasing emphasis on scalable, compliant operations across development and production. Facilities often adopt analyzers to improve consistency, raise throughput, and reduce manual sampling constraints. Growing adoption of standardized platforms across new and expanding sites supports sustained demand for both instruments and supporting analytics workflows.

Latin America

Latin America captured 6.43% of revenue in 2025, reflecting a smaller installed manufacturing base but continued efforts to modernize bioprocessing capabilities. Procurement commonly focuses on reliability, serviceability, and cost-effective deployment models. Expanding local production and technology transfer programs can increase analyzer utilization over time, especially where quality and consistency requirements tighten.

Middle East & Africa

Middle East & Africa represented 3.97% of the market in 2025, with demand concentrated in select countries expanding local pharmaceutical and biologics capabilities. Adoption is supported by investment in quality-driven manufacturing and gradual buildout of specialized facilities. Vendors with strong deployment support and training programs are better positioned to capture growth in emerging sites with limited local expertise.

Competitive Landscape

Competition centers on delivering validated instrument performance alongside software and analytics that support compliant data capture, workflow automation, and integration into control systems. Vendors differentiate through measurement breadth, deployment flexibility across unit operations, and service models that reduce downtime and accelerate qualification. Product strategies increasingly emphasize interoperability, standardized method libraries, and scalable platforms that can move from development into manufacturing with consistent outcomes.

Agilent Technologies, Inc. competes through analytical instrumentation strengths and workflow-oriented offerings that support measurement accuracy, repeatability, and data integrity expectations in regulated environments. The company’s positioning benefits from broad lab and process analytics expertise that can be aligned with bioprocess monitoring needs across development and quality workflows. Agilent’s approach typically emphasizes solution consistency, lifecycle support, and compatibility with controlled documentation and reporting requirements in biomanufacturing settings.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies, Inc.

- Danaher Corporation (incl. Cytiva, Beckman Coulter)

- Thermo Fisher Scientific Inc.

- Sartorius AG

- F. Hoffmann-La Roche Ltd. (Roche Diagnostics)

- Merck KGaA (MilliporeSigma)

- Eppendorf SE

- Nova Biomedical

- BD (Becton, Dickinson and Company)

- Bio-Rad Laboratories, Inc.

- Revvity, Inc. (formerly PerkinElmer life sciences)

- Bruker Corporation

- Hamilton Company

- HORIBA, Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In July 2025, Roche CustomBiotech launched the Cedex Lactose Assay for use with its Cedex Bio and Cedex Bio HT Analyzers. Roche said the new assay was designed for precise and reliable lactose measurement in aqueous solutions, supporting tighter bioprocess control in pharmaceutical production and food manufacturing.

- In July 2025, Univercells Technologies partnered with Repligen to bring real-time process analytical technology into scale-X bioreactors. Under the collaboration, Repligen’s MAVEN platform is being integrated for real-time glucose and lactate monitoring, helping reduce manual nutrient testing and improve process data resolution in viral vector and vaccine biomanufacturing.

- In March 2025, Repligen announced the acquisition of 908 Devices’ desktop bioprocessing analytics portfolio, adding four process analytical technology products: MAVERICK, MAVEN, REBEL, and ZipChip. The deal was positioned as a move to strengthen Repligen’s upstream and downstream bioprocess analytics capabilities and expand its workflow coverage for biopharmaceutical customers.

- In December 2024, Eppendorf SE entered a strategic partnership with DataHow AG to advance bioprocess data management. The collaboration integrates DataHow’s AI-enabled DataHowLab solution with Eppendorf’s BioNsight cloud platform so scientists can combine monitoring, analytics, and predictive modeling more effectively in bioprocess development.

Report Scope

| Report Attribute |

Details |

| Market Name |

Bioprocess Analyzers Market |

| Market size value in 2025 |

USD 2,374.45 million |

| Revenue forecast in 2032 |

USD 4,233.04 million by 2032 |

| Growth rate (CAGR) |

8.61% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product: Instruments; Consumables & accessories; Software & analytics.

By Measurement Principle / Technology: Spectroscopy (Raman spectroscopy, Near-infrared (NIR)); Mass spectrometry; Electrochemical sensors.

By Monitoring Mode: In-line / online monitoring; At-line monitoring; Off-line monitoring.

By Analysis Type: Substrate analysis; Metabolite analysis; Concentration detection; Physicochemical parameter monitoring.

By Application: Upstream bioprocessing (Cell culture monitoring; Fermentation monitoring); Downstream bioprocessing (Protein purification / downstream monitoring); Quality control (in-process / release testing); Vaccines; Antibiotics; Recombinant proteins; Biosimilars.

By End User: Biopharmaceutical & pharmaceutical companies; CROs & CMOs / contract manufacturing & research organizations; Research & academic institutes; Other end users. |

| Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Key companies profiled |

Agilent Technologies, Inc.; Danaher Corporation (incl. Cytiva, Beckman Coulter); Thermo Fisher Scientific Inc.; Sartorius AG; F. Hoffmann-La Roche Ltd. (Roche Diagnostics); Merck KGaA (MilliporeSigma); Eppendorf SE; Nova Biomedical; BD (Becton, Dickinson and Company); Bio-Rad Laboratories, Inc.; Revvity, Inc. (formerly PerkinElmer life sciences); Bruker Corporation; Hamilton Company; HORIBA, Ltd. |

| No. of Pages |

340 |

Segmentation

By Product

- Instruments

- Consumables & accessories

- Software & analytics

By Measurement Principle / Technology

- Spectroscopy [Raman spectroscopy, Near-infrared (NIR)]

- Mass spectrometry

- Electrochemical sensors

By Monitoring Mode

- In-line / online monitoring

- At-line monitoring

- Off-line monitoring

By Analysis Type

- Substrate analysis

- Metabolite analysis

- Concentration detection

- Physicochemical parameter monitoring

By Application

- Upstream bioprocessing [Cell culture monitoring; Fermentation monitoring]

- Downstream bioprocessing [Protein purification / downstream monitoring]

- Quality control (in-process / release testing)

- Vaccines

- Antibiotics

- Recombinant proteins

- Biosimilars

By End User

- Biopharmaceutical & pharmaceutical companies

- CROs & CMOs / contract manufacturing & research organizations

- Research & academic institutes

- Other end users

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa