Biosimilars Market Overview:

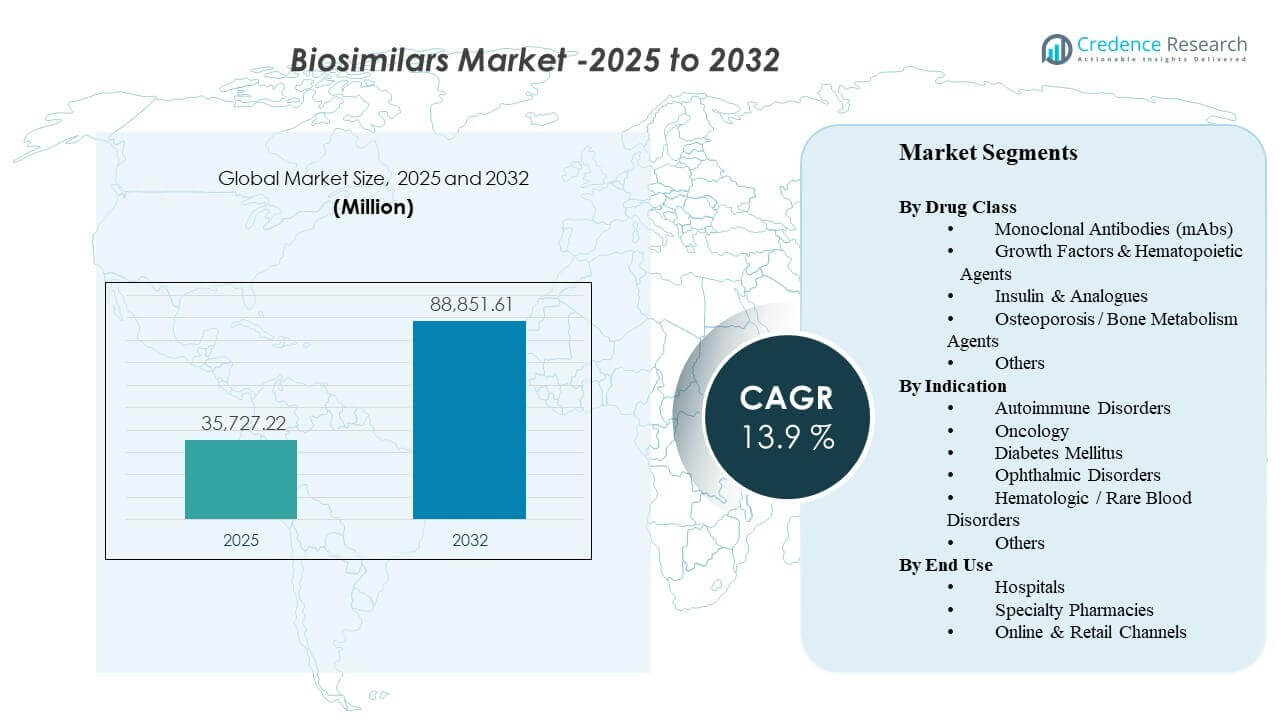

The global Biosimilars Market size was estimated at USD 35,727.22 million in 2025 and is expected to reach USD 88,851.61 million by 2032, growing at a CAGR of 13.9% from 2025 to 2032. Market expansion is primarily driven by widening payer and provider adoption of lower-cost biologic alternatives as high-value originator biologics face patent expiry and intensified price competition. Regulatory frameworks that support comparability-based approvals, along with growing physician confidence in switching for mature molecules, are reinforcing utilization across immunology, oncology, endocrinology, and ophthalmology. In parallel, broader tendering, formulary management, and specialty distribution capabilities are improving real-world access, particularly in markets where hospital procurement and reimbursement policies actively encourage biosimilar uptake.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biosimilars Market Size 2025 |

USD 35,727.22 million |

| Biosimilars Market, CAGR |

13.9% |

| Biosimilars Market Size 2032 |

USD 88,851.61 million |

Key Market Trends & Insights

- North America accounted for 41.3% of 2025 revenue, supported by expanding formulary preference strategies and contracting intensity.

- Europe represented 28.9% of 2025 revenue, reflecting mature tender-driven adoption and structured switching pathways.

- Asia Pacific captured 21.4% of 2025 revenue, aided by rising biologics access and expanding local manufacturing depth.

- Monoclonal Antibodies (mAbs) accounted for the largest drug-class share at 42.8% in 2025 due to high-value immunology and oncology molecules.

- Hospitals led end-use with a 49.2% share in 2025, reflecting infusion-led utilization and centralized procurement.

Segment Analysis

Biosimilar adoption is increasingly shaped by payer-driven access pathways, provider switching confidence, and the total cost of therapy in chronic and specialty care. Competitive intensity is highest where multiple biosimilars reference the same originator and where procurement models allow rapid share shifts through preferred listing and tender awards. Product differentiation is less about clinical performance and more about supply reliability, contracting terms, device usability for self-injectables, and patient support services.

Across applications, demand remains concentrated in chronic, high-burden conditions where biologics represent sustained therapy spend and long treatment durations. Provider confidence improves as post-market experience grows, especially in immunology and oncology settings where treatment protocols and monitoring are standardized. Distribution is also evolving, with specialty pharmacy services and digital ordering improving adherence, reimbursement navigation, and home-based administration support for select molecules.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Drug Class Insights

Monoclonal Antibodies (mAbs) accounted for the largest share of 42.8% in 2025. This leadership reflects the concentration of biosimilar activity around high-revenue immunology and oncology antibodies and the strong economic incentive to shift from originators once multiple alternatives are available. Payer contracting and formulary preference can quickly move volume toward competitively priced mAbs, especially when supported by consistent supply and robust patient support programs. Increasing clinical familiarity with switching in established molecules further sustains mAb adoption in both hospital and outpatient settings.

By Indication Insights

Autoimmune Disorders accounted for the largest share of 36.7% in 2025. High prevalence, chronic treatment duration, and significant biologic spending make autoimmune care the most commercially attractive segment for biosimilar conversion. Treatment algorithms are well-defined and switching is often facilitated through payer policies, preferred products, and physician experience with multiple therapeutic alternatives. As more interchangeable and high-concentration formulations enter the market, switching is becoming operationally easier, strengthening share retention in autoimmune indications.

By End Use Insights

Hospitals accounted for the largest share of 49.2% in 2025. Hospital dominance is supported by infusion-led administration, centralized pharmacy and therapeutics governance, and procurement models that favor rapid uptake once a biosimilar becomes preferred. Standardized protocols and predictable purchasing cycles improve switching execution, particularly for oncology and inpatient biologic use. Hospitals also benefit from scale-driven contracting leverage, enabling them to capture meaningful savings while maintaining consistent patient access.

Biosimilars Market Drivers

Patent Expiries and Cost-Containment Pressure in Biologics

Biosimilars gain traction as major biologic therapies lose exclusivity and health systems prioritize affordability. Payers increasingly use preferred formularies, step edits, and contracting to steer volume toward lower-cost options. Providers respond to clearer coverage signals when clinical outcomes remain comparable under established standards. This dynamic is strongest in high-spend therapeutic classes where even modest price reductions deliver material budget impact. As more reference biologics lose patent protection, the addressable biosimilar pipeline broadens and intensifies competition across multiple therapy areas.

- For instance, Boehringer Ingelheim made its interchangeable adalimumab biosimilar available in the U.S. through two pricing options: branded CYLTEZO at a 5% discount to Humira’s wholesale acquisition cost and unbranded adalimumab-adbm at an 81% discount, giving payers a concrete mechanism to steer volume toward a lower-cost version after loss of exclusivity.

Growing Clinical Confidence and Switching Infrastructure

Accumulated real-world experience and standardized clinical pathways are strengthening confidence in biosimilar use and switching. Provider comfort grows fastest in mature molecules with extensive post-market evidence and stable prescribing patterns. Health systems are also building operational playbooks for transitions, including patient communication, documentation, and monitoring protocols. As switching becomes routine, adoption barriers decline across both hospital and ambulatory care. Education initiatives and clearer guidance on interchangeability and substitution are further reducing hesitation among prescribers and patients.

Procurement, Tendering, and Formulary Levers Accelerating Share Shifts

Institutional purchasing and tender-driven contracting can rapidly reshape market shares once biosimilars are competitively priced. Hospitals and integrated delivery networks often consolidate volume through preferred supplier agreements to maximize savings. These mechanisms reduce fragmentation in purchasing decisions and improve predictability for inventory planning. Over time, repeat tender cycles intensify competition and encourage additional entrants. Winning a single large tender or preferred formulary position can quickly shift volume, making commercial success highly sensitive to access strategy and contracting execution.

- For instance, Celltrion reported that its Remsima IV liquid formulation won national tenders in Norway and Denmark, and that the Norway award alone is expected to secure about 35% of that country’s infliximab IV market through January 2028, showing how a single large tender can shift volume quickly. These mechanisms reduce fragmentation in purchasing decisions and improve predictability for inventory planning.

Expansion of Manufacturing Capacity and Global Commercial Footprints

Scaled biologics manufacturing and broader geographic commercialization support faster availability of biosimilars across regions. Companies are investing in capacity, process optimization, and quality systems to ensure consistent supply at lower cost. Global partnerships and licensing models also help accelerate entry into regulated markets. As portfolios deepen, manufacturers can compete more effectively across multiple molecules and therapeutic areas. Supply resilience and multi-site manufacturing are increasingly important differentiators as buyers prioritize continuity and minimize disruption risk.

Biosimilars Market Challenges

Price erosion can be steep in highly contested molecules, compressing margins and increasing the importance of scale, supply reliability, and contracting capabilities. Complex contracting structures, including rebates and bundled agreements, can reduce the transparency of net pricing and slow switching in some markets. Legal disputes and patent litigation may delay launches, creating uncertainty for pipeline planning and commercialization timing. In addition, stakeholders may face operational friction during transitions, including inventory management, patient communication, and payer authorization requirements.

- For instance, Amgen’s AMJEVITA, the first FDA-approved Humira biosimilar, was approved in 2016 but launched in the U.S. only on January 31, 2023 under patent-settlement timing; by launch, it had accumulated four years of real-world use in more than 300,000 patients across over 60 countries, showing how litigation timing and commercial scale can materially shape rollout execution.

Market fragmentation across countries and healthcare systems creates uneven adoption and complicates global strategy. Differences in interchangeability pathways, substitution rules, tender mechanics, and reimbursement policies produce variable uptake curves by region. Provider hesitancy may persist in sensitive indications or where patient continuity concerns are high. Supply disruptions or limited manufacturing redundancy can also damage confidence and create switching reversals if availability becomes inconsistent.

Biosimilars Market Trends and Opportunities

Interchangeability, high-concentration formulations, and device innovation are becoming more influential in shaping competitive outcomes, especially in self-injectable products. Companies that combine competitive pricing with simplified administration and strong patient support can improve persistence and formulary acceptance. Expansion into new therapeutic areas, including complex specialty segments, is creating additional headroom beyond the earlier oncology- and immunology-heavy adoption base. Digital services that streamline reimbursement and patient engagement are also strengthening value propositions beyond price.

- For instance, Organon and Samsung Bioepis positioned HADLIMA as a self-injectable adalimumab biosimilar in both 40 mg/0.4 mL and 40 mg/0.8 mL presentations, and its PushTouch autoinjector uses a 29-gauge needle, a latex-free needle cover, and a buttonless design that received the Arthritis Foundation’s Ease of Use Certification; the product is also supported by the HADLIMA For You program, including co-pay support.

Emerging-market access programs and localized manufacturing strategies are widening opportunities in Asia Pacific, Latin America, and parts of the Middle East. As biologics utilization grows, biosimilars can become a primary mechanism for improving affordability and expanding coverage. Hospital systems and government payers are increasingly using structured procurement to drive predictable savings. Portfolio strategies that bundle multiple biosimilars may also strengthen negotiating leverage and help accelerate multi-molecule adoption.

Regional Insights

North America

North America accounted for 41.3% of 2025 revenue, supported by strong biologics spending and expanding payer mechanisms to encourage biosimilar use. Formulary preference, contracting, and specialty distribution capabilities are improving access and accelerating switching for selected high-value molecules. Uptake is strongest where multiple competitors exist and where coverage policies are clear and consistently applied. Provider confidence continues to improve as switching becomes operationally routine in large health systems. Competitive dynamics remain intense, with pricing and supply reliability shaping share capture.

Europe

Europe represented 28.9% of 2025 revenue, reflecting established tendering and structured adoption pathways in several countries. Hospital procurement and payer-driven switching policies can produce rapid volume movement once a biosimilar wins preferred status. Competitive pressure is sustained through recurring tender cycles that encourage price competition and portfolio breadth. Adoption tends to be more standardized across institutions where national or regional guidance supports switching. Operational execution remains a key differentiator, particularly around supply continuity and stakeholder engagement.

Asia Pacific

Asia Pacific captured 21.4% of 2025 revenue, supported by expanding biologics access and rising capacity for development and manufacturing. Adoption is accelerating as healthcare systems balance affordability with broader treatment access goals. Local and regional producers increasingly compete with multinational portfolios, expanding choice and improving supply options. Uptake varies by country based on reimbursement structures, procurement models, and prescriber familiarity. Over the forecast period, the region is positioned to gain share as coverage depth and switching infrastructure improve.

Latin America

Latin America accounted for 4.8% of 2025 revenue, with growth shaped by affordability needs and gradual expansion of biologics coverage. Adoption is uneven across countries due to differences in reimbursement, procurement capability, and regulatory pathways. Public tenders can support biosimilar penetration where centralized purchasing is used effectively. Market development also depends on strengthening distribution infrastructure and clinician awareness. As access expands, competitive entry is expected to increase across major molecules.

Middle East & Africa

Middle East and Africa represented 3.6% of 2025 revenue, reflecting smaller biologics access in many markets but growing emphasis on cost-effective specialty care. Uptake is strongest where procurement is centralized and where payer policies actively support biosimilars for budget optimization. Supply consistency and regulatory clarity remain important to building sustained confidence. Local partnerships and regional manufacturing initiatives can improve availability and reduce costs over time. Growth potential is concentrated in markets with expanding insurance coverage and hospital capacity.

Competitive Landscape

Competition in the biosimilars market is defined by portfolio breadth, speed-to-market, supply reliability, and the ability to secure preferred access through contracting and tender participation. Manufacturers increasingly differentiate through device design, high-concentration formulations, and patient support services that improve persistence and reduce administrative burden. Commercial success is shaped by payer engagement, distribution reach into specialty channels, and the capacity to scale manufacturing without disruptions. Companies also use strategic partnerships and licensing models to accelerate entry into regulated markets and broaden geographic footprints.

Pfizer Inc. is focused on leveraging its global commercial infrastructure and scientific capabilities to participate in biosimilar categories where payer demand for affordability is strongest. The company’s approach emphasizes scalable manufacturing access, disciplined portfolio decisions, and channel execution across institutional and specialty settings. Pfizer’s commercialization strength supports contracting depth, which is critical in molecules with multiple competitors. Portfolio management and lifecycle planning remain important as price competition intensifies and switching becomes more standardized.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In a January 2026 update, Biocon Biologics said it will introduce three new oncology biosimilars proposed biosimilars for trastuzumab/hyaluronidase, nivolumab, and pembrolizumab at the 2026 J.P. Morgan Healthcare Conference, expanding its oncology biosimilar portfolio.

- In a December 2025 announcement, Sandoz said it completed the strategic acquisition of Just-Evotec Biologics EU SAS after first signing the agreement on November 4, 2025, a move aimed at strengthening its in-house biosimilars development and manufacturing capabilities.

- In an April 2025 partnership update, Chime Biologics and Polpharma Biologics announced a strategic cooperation agreement to support end-to-end development and commercial manufacturing of a biosimilar product for global markets, including production for a U.S. FDA BLA submission and launches in Europe and other regions.

- In a January 2025 partnership announcement, Teva Pharmaceutical Industries and Samsung Bioepis entered a license, development, and commercialization agreement for EPYSQLI (eculizumab-aagh), Samsung Bioepis’ biosimilar to Soliris, in the U.S., with Samsung Bioepis responsible for development, manufacturing, and supply and Teva handling commercialization

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 35,727.22 million |

| Revenue forecast in 2032 |

USD 88,851.61 million |

| Growth rate (CAGR) |

13.9% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Drug Class Outlook: Monoclonal Antibodies (mAbs), Growth Factors & Hematopoietic Agents, Insulin & Analogues, Osteoporosis / Bone Metabolism Agents, Others; By Indication Outlook: Autoimmune Disorders, Oncology, Diabetes Mellitus, Ophthalmic Disorders, Hematologic / Rare Blood Disorders, Others; By End Use Outlook: Hospitals, Specialty Pharmacies, Online & Retail Channels |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Pfizer Inc., Sandoz Group AG, Amgen Inc., Celltrion Inc., Biocon Biologics Ltd., Samsung Bioepis Co., Ltd., Teva Pharmaceutical Industries Ltd., Viatris Inc. companies |

| No.of Pages |

338 |

Segmentation

By Drug class

- Monoclonal Antibodies (mAbs)

- Growth Factors & Hematopoietic Agents

- Insulin & Analogues

- Osteoporosis / Bone Metabolism Agents

- Others

By Indication

- Autoimmune Disorders

- Oncology

- Diabetes Mellitus

- Ophthalmic Disorders

- Hematologic / Rare Blood Disorders

- Others

By End use

- Hospitals

- Specialty Pharmacies

- Online & Retail Channels

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa