Biotechnology Reagents Market

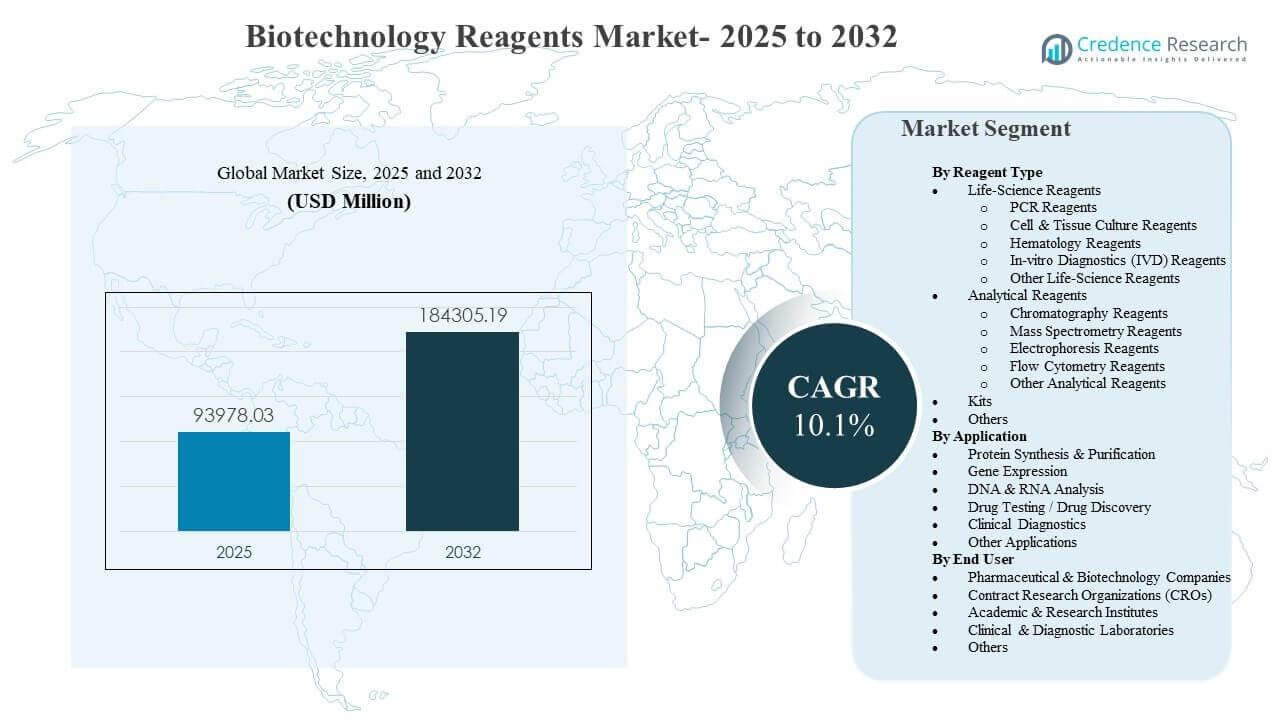

The global Biotechnology Reagents Market size was estimated at USD 93,978.03 million in 2025 and is expected to reach USD 184,305.19 million by 2032, growing at a CAGR of 10.1% from 2025 to 2032. Demand is primarily supported by the expanding intensity of molecular and omics-based workflows across research, bioprocess development, and regulated testing, which increases reagent consumption per study and per sample. Growth is further reinforced by broader lab automation and standardization initiatives that favor validated, workflow-compatible reagents across multi-site operations.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Biotechnology Reagents Market Size 2025 |

USD 93,978.03 million |

| Biotechnology Reagents Market, CAGR |

10.1% |

| Biotechnology Reagents Market Size 2032 |

USD 184,305.19 million |

Key Market Trends & Insights

- The market is projected to expand from USD 93,978.03 million (2025) to USD 184,305.19 million (2032) at a 10.1% CAGR (2025–2032).

- Life-Science Reagents accounted for the largest share of 54.60% in 2025, supported by recurring use across PCR, sequencing, and routine molecular workflows.

- DNA & RNA Analysis represented 30.10% share in 2025, reflecting sustained demand from sequencing, PCR-based testing, and transcriptomics workloads.

- Pharmaceutical & Biotechnology Companies held 43.20% share in 2025, driven by high reagent intensity across discovery, development, and translational pipelines.

- North America captured 38.30% share in 2025, while Asia Pacific reached 26.40% share.

Segment Analysis

The market shows a strong tilt toward high-frequency consumables used in routine molecular biology, genomics, and cell-based workflows, alongside rising demand for standardized, automation-ready formats. Buyers increasingly prefer pre-optimized reagent systems and kits that minimize hands-on time, reduce variability, and improve reproducibility across multiple instruments and sites. In regulated settings, purchasing decisions place a premium on lot-to-lot consistency, documentation, and validation support, which typically favors established suppliers with broad portfolios.

Application demand is increasingly shaped by data-rich workflows such as sequencing, transcriptomics, and multi-omics studies, which lift per-sample reagent consumption and encourage adoption of integrated sample-to-result solutions. Drug discovery and translational programs are also expanding reagent use as biomarker development, screening, and assay development become more iterative and standardized. Across end users, outsourcing and consolidation of lab workflows continue to shift reagent demand toward high-throughput service providers and platform-aligned consumables.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Reagent Type Insights

Life-Science Reagents accounted for the largest share of 54.60% in 2025. This lead is supported by recurring consumption across PCR, nucleic acid preparation, cell culture, and routine molecular workflows that are repeated at high frequency in both research and applied settings. Standardization efforts in laboratories also favor validated, ready-to-use formulations that reduce protocol variability and rework. In parallel, expanding sequencing and cell-based pipelines increase baseline demand for core reagents and compatible kits.

By Application Insights

DNA & RNA Analysis accounted for the largest share of 30.10% in 2025. This dominance reflects sustained utilization in sequencing, amplification, transcriptomics, and nucleic-acid quality control workflows that continue to broaden across research and clinical-adjacent environments. Multi-omics and single-cell studies amplify reagent intensity per experiment, raising total consumption even when sample volumes are constrained. Additionally, greater emphasis on reproducibility and standardized pipelines increases adoption of workflow-consistent chemistries and supporting reagents.

By End User Insights

Pharmaceutical & Biotechnology Companies accounted for the largest share of 43.20% in 2025. Biopharma organizations maintain high reagent consumption across discovery research, process development, analytical testing, and translational studies, often running multiple assays and iterative cycles per candidate. Quality expectations and time-to-decision pressures encourage adoption of trusted reagents with strong documentation and technical support. Growing use of advanced modalities and data-intensive platforms further increases demand for specialized and platform-compatible reagent systems.

Biotechnology Reagents Market Drivers

Expansion of omics-driven research and translational pipelines

Rapid growth in genomics, transcriptomics, and broader multi-omics workflows is increasing reagent use per sample and per study across research and applied settings. Laboratories are running more iterative experiments and larger cohorts, which lifts recurring consumption of preparation, amplification, labeling, and quality-control reagents. In translational programs, biomarker discovery and validation add repeat testing cycles that further increase reagent intensity. As datasets scale, buyers also favor standardized chemistries to improve repeatability across sites and instruments.

- For instance, Illumina’s NovaSeq X Plus platform can generate more than 20,000 whole human genomes per year, substantially increasing consumption of library preparation, amplification, and QC chemistries in large population-scale genomics programs.

Shift toward workflow standardization and automation-ready consumables

Laboratories are prioritizing throughput, reproducibility, and labor efficiency, accelerating adoption of reagents designed for automated workflows. Automation increases sensitivity to reagent consistency and compatibility, leading purchasers toward validated formats and supplier portfolios that reduce integration risk. Standardized protocols across multi-site operations also elevate demand for reliable, lot-consistent reagents that minimize reruns and downtime. Over time, standardized workflows increase switching costs and sustain recurring procurement of platform-aligned consumables.

- For instance, Thermo Fisher Scientific’s Ion Torrent Genexus System automates purification, library preparation, sequencing, and analysis to deliver next-generation sequencing results in as little as 24 hours with a single five-minute reagent setup, pushing demand for pre-filled, automation-validated reagent cartridges.

Rising complexity of assays and demand for higher sensitivity

Modern assays increasingly require high-performance reagents that deliver better specificity, reduced background, and consistent performance across complex samples. This is particularly relevant for low-input workflows, single-cell studies, and advanced analytical testing where failures are expensive and time-sensitive. Higher performance requirements shift demand toward premium reagent systems, optimized kits, and tightly controlled chemistries. As assay complexity grows, technical support, documentation, and validated performance become central to procurement decisions.

Growth in outsourced testing and service-lab throughput

CROs and specialized service laboratories are expanding capacity to meet growing demand for outsourced discovery, screening, and analytical testing. High-throughput service environments rely on standardized reagents and repeatable protocols to ensure predictable turnaround times and data comparability across clients. As outsourcing rises, reagent demand concentrates in larger centralized labs that purchase in volume and prioritize supplier reliability. This channel supports steady, recurring consumption of core reagents, assay kits, and platform-compatible consumables.

Biotechnology Reagents Market Challenges

Supply continuity, lot-to-lot consistency, and quality documentation remain persistent constraints for laboratories operating at scale. Even small performance shifts can trigger re-validation, rework, or reruns, raising both direct costs and time-to-result risk. These pressures are amplified in regulated or clinical-adjacent environments where documentation and traceability requirements are stricter. In addition, long qualification cycles can slow adoption of new reagents even when performance appears superior.

- For instance, laboratories operating under FDA 21 CFR 211.160 must document every change to specifications, sampling plans, and test procedures at the time of performance, with any deviation formally recorded and justified by the quality unit. In addition, long qualification cycles can slow adoption of new reagents even when performance appears superior.

Cost sensitivity and procurement complexity also challenge broader adoption, particularly among academic and budget-constrained institutions. Price pressure often conflicts with the need for validated, high-consistency reagents, creating tradeoffs between unit cost and total cost of ownership. Fragmented instrument platforms can increase compatibility checks and complicate supplier consolidation strategies. Finally, competitive differentiation is difficult in commoditized categories, which can intensify discounting and margin pressure.

Biotechnology Reagents Market Trends and Opportunities

Demand is rising for integrated reagent-and-workflow solutions that reduce hands-on time and improve standardization across instruments, sites, and study designs. Bundled offerings that combine sample prep, assay chemistries, and analytics-ready workflows are increasingly attractive to buyers seeking predictable outcomes. This trend supports opportunities for suppliers that can align reagents tightly with platform ecosystems and provide robust documentation and support. It also encourages portfolio expansion via partnerships and targeted acquisitions.

- For instance, Agilent’s MagnisDx NGS Prep System cut manual hands-on time in an oncology lab from about 2.5 hours to roughly 10–15 minutes while enabling a 72‑hour sample‑to‑result turnaround, illustrating how tightly integrated prep and enrichment workflows can standardize outputs across high‑throughput settings.

Another key opportunity is the scaling of single-cell and multi-omics studies, which typically increase reagent intensity per project and favor optimized chemistries. As laboratories pursue deeper biological resolution, demand grows for sensitive, low-input reagents and standardized kits that reduce variability. Growth in data-rich workflows also creates room for premium pricing where reliability and reproducibility reduce total rerun costs. Suppliers that enable higher throughput and consistent results can capture share as labs scale operations.

Regional Insights

North America (38.30% share in 2025)

North America leads due to its concentration of biopharma R&D, advanced genomics adoption, and strong demand from high-throughput laboratories. A mature ecosystem of instrument platforms and standardized lab workflows supports recurring spend on validated reagents and platform-compatible consumables. The strong presence of CRO networks and centralized testing hubs reinforces volume purchasing and supplier consolidation, while a focus on reproducibility, documentation, and quality systems sustains demand for established reagent portfolios.

Europe (24.90% share in 2025)

Europe remains a major market supported by strong academic research intensity, established biopharma manufacturing, and robust analytical testing capabilities. Laboratories prioritize standardization and validated performance to maintain comparability across multi-site and cross-border collaborations. Steady clinical-adjacent testing and translational research pipelines also drive recurring reagent demand, benefiting suppliers with broad catalogs, deep technical support, and reliable distribution.

Asia Pacific (26.40% share in 2025)

Asia Pacific shows strong scale and momentum driven by expanding biotech manufacturing, growing genomics infrastructure, and increasing laboratory capacity across multiple countries. Wider adoption of sequencing and molecular workflows supports rising consumption of DNA/RNA analysis reagents and associated kits. The region also benefits from outsourcing growth and centralized service labs that prefer standardized workflows, and ongoing improvements in quality systems and automation are expected to increase demand for validated, higher-performance reagents.

Latin America (6.60% share in 2025)

Latin America is a smaller but developing opportunity area as diagnostics networks, research programs, and lab infrastructure continue to expand. Growth is supported by increasing access to molecular methods and gradual improvements in procurement maturity. However, budget constraints and infrastructure variability can limit adoption of premium reagent systems, making reliable performance, training support, and efficient distribution key differentiators for suppliers.

Middle East & Africa (3.80% share in 2025)

The Middle East & Africa market is emerging, supported by gradual expansion of laboratory capacity, public health testing networks, and selected research hubs. Demand is concentrated in centralized laboratories where standardization and training can improve throughput and reproducibility. Constraints include uneven infrastructure and limited access to specialized workflows in some areas, while the strongest opportunities are linked to healthcare modernization and life-sciences investment programs.

Competitive Landscape

Competition is characterized by broad portfolio depth, reliability, and the ability to support end-to-end workflows across molecular biology, diagnostics-adjacent testing, and analytical applications. Suppliers compete on consistency, documentation, technical support, and compatibility with major platform ecosystems, which reduces switching once workflows are standardized. Partnerships, targeted acquisitions, and portfolio integration are commonly used to expand workflow coverage and strengthen positions in faster-growing assay areas. Differentiation is also driven by automation readiness, quality systems, and the ability to scale supply for high-throughput customers.

Merck KGaA is positioned as a diversified life-sciences supplier with strong capabilities across reagents, process solutions, and workflow support that align with biopharma and advanced research demand. The company’s strategy typically emphasizes portfolio breadth, quality systems, and solutions that integrate into standardized laboratory and manufacturing workflows. Expansion into specialized areas that support advanced modalities can strengthen presence in higher-value reagent categories. Its approach supports customer retention where reliability, documentation, and supply continuity are key buying criteria.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Merck KGaA

- Agilent Technologies, Inc.

- Bio-Rad Laboratories, Inc.

- Becton, Dickinson and Company

- Beckman Coulter, Inc. (Danaher)

- bioMérieux SA

- Illumina, Inc.

- Lonza Group

- QIAGEN N.V.

- Promega Corporation

- Abbott Laboratories

- Siemens Healthineers

- Waters Corporation

- Takara Bio Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In July 2025, Bio‑Rad Laboratories, Inc. launched four new Droplet Digital PCR platforms, including the QX Continuum system and QX700 series acquired with its purchase of Stilla Technologies, thereby broadening its ddPCR instruments and associated reagents portfolio.

- In February 2026, Becton, Dickinson and Company (BD) completed the spin‑off and merger of its Biosciences & Diagnostic Solutions business with Waters Corporation, creating a combined entity and marking the final portfolio‑shaping step of BD’s “2025 strategy.”

- In February 2026, bioMérieux SA launched SMARTBIOME, a sequencing‑ and bioinformatics‑based solution designed to help food manufacturers understand and control microbiological spoilage, extending its reagents and molecular microbiology toolkit for industrial applications.

- In March 2026, Agilent Technologies, Inc. entered into a definitive all‑cash agreement valued at about USD 950 million to acquire Biocare Medical, a pathology-focused antibody, reagent, and instrument business, to strengthen its IHC and molecular pathology offering.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 93978.03 million |

| Revenue forecast in 2032 |

USD 184305.19 million |

| Growth rate (CAGR) |

10.1% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Reagent Type; By Application; By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Merck KGaA; Agilent Technologies, Inc.; Bio-Rad Laboratories, Inc.; Becton, Dickinson and Company; Beckman Coulter, Inc. (Danaher); bioMérieux SA; Illumina, Inc.; Lonza Group; QIAGEN N.V.; Promega Corporation; Abbott Laboratories; Siemens Healthineers; Waters Corporation; Takara Bio Inc. |

| No.of Pages |

336 |

Segmentation

By Reagent Type

- Life-Science Reagents

- PCR Reagents

- Cell & Tissue Culture Reagents

- Hematology Reagents

- In-vitro Diagnostics (IVD) Reagents

- Other Life-Science Reagents

- Analytical Reagents

- Chromatography Reagents

- Mass Spectrometry Reagents

- Electrophoresis Reagents

- Flow Cytometry Reagents

- Other Analytical Reagents

- Kits

- Others

By Application

- Protein Synthesis & Purification

- Gene Expression

- DNA & RNA Analysis

- Drug Testing / Drug Discovery

- Clinical Diagnostics

- Other Applications

By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Clinical & Diagnostic Laboratories

- Others

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa