Bladder Cancer Therapeutics & Diagnostics Market Overview:

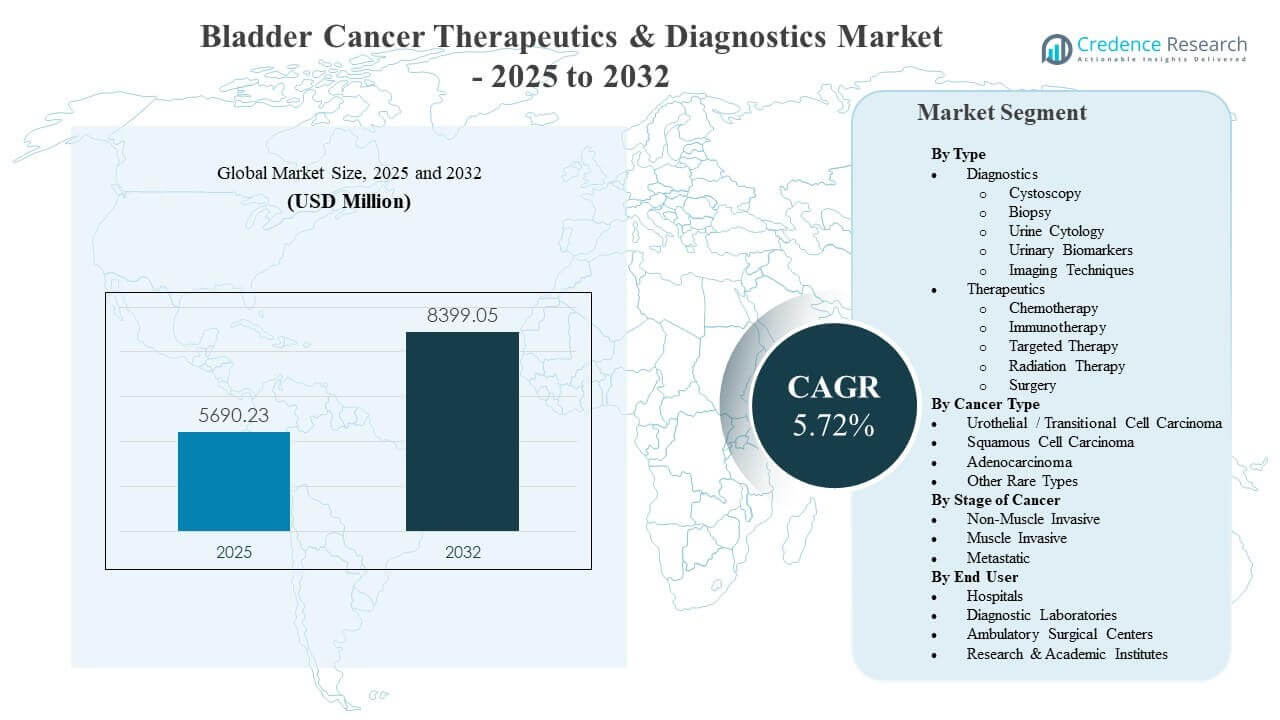

The global Bladder Cancer Therapeutics & Diagnostics Market size was estimated at USD 5690.23 million in 2025 and is expected to reach USD 8399.05 million by 2032, growing at a CAGR of 5.72% from 2025 to 2032. Rising adoption of advanced systemic therapies, supported by stronger survival outcomes and expanded eligibility across disease stages, is a key force shaping demand patterns across oncology care pathways. Bladder cancer surveillance intensity and recurrence risk continue to sustain recurring diagnostic volumes, reinforcing demand for cystoscopy, cytology, and emerging biomarker-based workflows across major healthcare systems.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bladder Cancer Therapeutics & Diagnostics Market Size 2025 |

USD 5690.23 million |

| Bladder Cancer Therapeutics & Diagnostics Market, CAGR |

5.72% |

| Bladder Cancer Therapeutics & Diagnostics Market Size 2032 |

USD 8399.05 million |

Key Market Trends & Insights

- Therapeutics accounted for 61.4% share in 2025, reflecting higher value capture from systemic regimens compared with procedure-led diagnostics.

- Urothelial / transitional cell carcinoma represented 83.3% share in 2025, keeping clinical development and commercialization concentrated in the largest patient pool.

- Hospitals held 54.2% share in 2025, supported by high-acuity procedures, oncology infusion capacity, and multi-disciplinary care delivery.

- North America contributed 42.8% of 2025 revenue, supported by higher oncology spending, faster adoption of novel regimens, and strong specialty care access.

- Asia Pacific is positioned as the fastest-growing region with 10.40% CAGR during 2026–2031, reflecting expanding access, rising diagnosis rates, and broader treatment availability.

Segment Analysis

Bladder Cancer Therapeutics & Diagnostics Market demand is shaped by the combination of intensive surveillance needs and increasing use of advanced systemic therapies. Recurrent monitoring practices keep cystoscopy and urine-based testing volumes elevated, especially in earlier-stage disease where long-term follow-up is common. At the same time, prescribing momentum in advanced settings is being reinforced by stronger outcomes from combination approaches, which is increasing payer and provider willingness to adopt premium-priced regimens.

Commercial growth is increasingly influenced by care setting shifts and workflow efficiency needs. Hospitals remain critical for surgeries, inpatient management, and systemic therapy initiation, but ambulatory environments are expanding their role for procedure-led diagnostics and follow-up care. Diagnostic laboratories are gaining relevance as urinary biomarkers and molecular workflows mature, supporting broader adoption of non-invasive and adjunct decision tools across clinical pathways.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Type Insights

Therapeutics accounted for the largest share of 61.4% in 2025. Therapeutics leads because drug-based care captures higher per-patient revenue across longer treatment durations, particularly in muscle-invasive and metastatic disease pathways. Expanding use of immunotherapy and targeted approaches is strengthening regimen adoption across eligible populations. Greater emphasis on improving outcomes and lowering recurrence risk continues to reinforce investment and utilization across systemic treatment options.

By Cancer Type Insights

Urothelial / Transitional Cell Carcinoma accounted for the largest share of 83.3% in 2025. Urothelial disease dominates because the diagnosed population is substantially larger than other histologies, concentrating clinical trial activity and guideline-backed use in this subtype. Broader availability of immunotherapy and novel combinations is reinforcing treatment intensity in urothelial settings. Commercial focus remains strongest where evidence depth is highest, sustaining leadership for urothelial carcinoma across therapeutics and diagnostics.

By Stage of Cancer Insights

Non-muscle invasive, muscle invasive, and metastatic bladder cancer stages create distinct demand pools across surveillance, procedural diagnostics, and systemic therapy utilization. Non-muscle invasive disease sustains high-frequency monitoring and repeat testing, supporting consistent diagnostic consumption. Muscle invasive disease drives higher intervention intensity and supports adoption of perioperative treatment approaches alongside surgery. Metastatic disease remains a key value driver for systemic therapies, where advanced regimens typically account for a meaningful share of treatment spending.

By End User Insights

Hospitals accounted for the largest share of 54.2% in 2025. Hospitals lead because complex diagnostic workups, surgical procedures, and systemic therapy initiation are frequently centralized in acute-care and tertiary oncology settings. Hospital-based multidisciplinary teams support higher treatment complexity and advanced imaging utilization. Ongoing investment in oncology infrastructure and integrated care pathways continues to strengthen hospital share, even as outpatient care expands for follow-up and routine procedures.

Bladder Cancer Therapeutics & Diagnostics Market Drivers

Expanding adoption of advanced systemic therapies

Bladder Cancer Therapeutics & Diagnostics Market growth is supported by increasing uptake of immunotherapy, targeted therapy, and combination regimens across advanced disease settings. Clinical evidence demonstrating stronger outcomes is encouraging earlier use in treatment sequences and broader patient eligibility. Provider preference is shifting toward regimens that improve survival endpoints and reduce progression risk. Treatment pathway standardization is also improving adoption consistency across leading oncology centers and high-volume health systems.

- For instance, Merck’s pembrolizumab and Bristol Myers Squibb’s nivolumab have demonstrated 24‑month overall survival rates of 72.5% and 75.5%, respectively, and 36‑month overall survival rates of 60.9% and 65.9% as adjuvant therapy in high‑risk muscle‑invasive urothelial carcinoma, supporting earlier use and broader adoption in treatment pathways.

High recurrence rates sustaining long-term surveillance demand

Bladder Cancer Therapeutics & Diagnostics Market demand is reinforced by intensive monitoring protocols, particularly for non-muscle invasive disease. Repeat procedures and follow-up testing remain common due to recurrence risk and the need for ongoing assessment. Surveillance intensity supports steady volumes for cystoscopy and complementary urine-based tests. A larger monitored patient base also supports incremental adoption of adjunct biomarkers that aim to reduce unnecessary procedures and improve risk stratification.

Rising diagnostic innovation and workflow modernization

Bladder Cancer Therapeutics & Diagnostics Market growth is supported by improved imaging quality, enhanced endoscopic visualization, and expanding availability of urinary biomarker tools. Healthcare providers are increasingly focused on workflow efficiency and diagnostic confidence across detection and monitoring stages. Diagnostic laboratories are strengthening capacity for advanced assays, enabling broader use of standardized testing processes. Continued innovation is improving clinical decision support and supporting more personalized care planning.

- For instance, Photocure’s hexaminolevulinate blue‑light cystoscopy has been shown to reduce short‑term recurrence at repeat TURBT from 31.2% with standard white‑light cystoscopy to 11.1% with blue‑light in high‑risk non‑muscle‑invasive bladder cancer, directly improving detection quality and follow‑up workload.

Broader access to oncology care and specialty infrastructure

Bladder Cancer Therapeutics & Diagnostics Market expansion is also linked to wider access to specialist-led oncology services, particularly in fast-growing regions. Growth in urology services, imaging capacity, and oncology infusion infrastructure increases diagnosis and treatment throughput. Policy-driven improvements in reimbursement and cancer program expansion support uptake of standard-of-care diagnostics and therapeutics. Greater awareness and screening practices in risk populations also contribute to rising diagnosis rates and earlier treatment initiation.

Bladder Cancer Therapeutics & Diagnostics Market Challenges

Bladder Cancer Therapeutics & Diagnostics Market growth faces constraints related to affordability and reimbursement variability for advanced regimens and newer diagnostic tools. High therapy costs can limit access in price-sensitive healthcare systems, particularly where reimbursement pathways remain uneven. Diagnostic adoption can also be slowed by clinical workflow disruption and the need for stronger real-world validation. Hospital procurement cycles and payer requirements may delay broader uptake of premium innovations.

- For instance, Merck’s checkpoint inhibitor pembrolizumab, used in advanced bladder cancer, has been associated with incremental cost‑effectiveness ratios reported as high as 122,557–184,000 per quality‑adjusted life year in bladder and other malignancies, which challenges payer acceptance in cost‑sensitive health systems.

Bladder Cancer Therapeutics & Diagnostics Market participants also face challenges tied to clinical complexity and patient heterogeneity across stages and histologies. Variable response rates and tolerability considerations can complicate regimen selection and sequencing. Diagnostic pathways often require invasive confirmation, and non-invasive tools may face adoption barriers if performance thresholds are not consistently demonstrated. Regulatory and evidence-generation timelines can slow commercialization of new biomarker-driven solutions.

Bladder Cancer Therapeutics & Diagnostics Market Trends and Opportunities

Bladder Cancer Therapeutics & Diagnostics Market opportunity is increasing around combination approaches and perioperative use of immunotherapy and targeted regimens. Earlier integration of systemic therapy alongside surgery is expanding the treated population and increasing overall therapy intensity per patient. Continued pipeline advancement supports differentiated positioning across mechanism classes and patient subgroups. Biomarker-driven selection and companion diagnostics offer additional routes to optimize outcomes and improve payer acceptance.

- For instance, phase 2 trials of Janssen’s FGFR inhibitor erdafitinib in previously treated advanced urothelial cancer with FGFR2/3 alterations demonstrated an objective tumor response rate of 40–46%, including complete and partial responses, enabling its positioning as a post‑immunotherapy option in defined genomic subgroups.

Bladder Cancer Therapeutics & Diagnostics Market growth opportunities are also forming around non-invasive testing, longitudinal monitoring, and workflow integration across care settings. Urinary biomarkers and advanced imaging enhancements can support improved recurrence detection and risk stratification. Expanded ambulatory care capacity creates opportunities for streamlined endoscopy, imaging, and follow-up testing models. Regional expansion strategies focused on Asia Pacific and select emerging markets can capture rising diagnosis rates and improving access to specialty care.

Regional Insights

North America

North America accounted for 42.8% of 2025 revenue. Strong oncology spending, higher adoption of advanced therapies, and broad access to specialty urology and cancer centers support regional leadership. Regulatory clarity and payer coverage for standard-of-care regimens help sustain utilization across diagnostics and therapeutics pathways. Ongoing innovation uptake is reinforced by established clinical trial ecosystems and integrated care delivery models.

Europe

Europe accounted for 26.1% of 2025 revenue. Mature healthcare systems and structured reimbursement frameworks support consistent diagnostic volumes and therapy adoption across major markets. Emphasis on evidence-based guidelines supports adoption of validated therapeutic and diagnostic advances. Investment in hospital networks and specialized oncology programs continues to sustain demand across surveillance, imaging, and systemic treatment utilization.

Asia Pacific

Asia Pacific accounted for 23.4% of 2025 revenue. A large patient pool, improving diagnosis rates, and expanding specialty care infrastructure support a rising regional contribution. Asia Pacific is projected to grow at a 10.40% CAGR during 2026–2031, supported by broader access to oncology services and increasing adoption of advanced therapies. Expansion of diagnostic laboratories and imaging capacity is strengthening pathway coverage across urban healthcare hubs.

Latin America

Latin America accounted for 4.9% of 2025 revenue. Regional demand is shaped by uneven access to specialty oncology services and variability in reimbursement coverage for premium therapeutics. Growth is supported by gradual expansion of cancer centers and improvements in diagnostic availability in high-income urban markets. Continued focus on affordability and access remains important for broader adoption.

Middle East & Africa

Middle East & Africa accounted for 2.8% of 2025 revenue. Limited specialist density and variability in care access constrain broad adoption of advanced diagnostics and therapies. Demand remains concentrated in select countries with higher healthcare spending and established oncology infrastructure. Investment in cancer programs and improved referral pathways can support gradual expansion across diagnostics and systemic therapy use.

Competitive Landscape

Bladder Cancer Therapeutics & Diagnostics Market competition is defined by pipeline intensity in immunotherapy, targeted therapy, and combination strategies, alongside continued innovation in diagnostics and biomarker workflows. Companies compete through clinical differentiation, label expansion across stages, and broader adoption support through real-world evidence and pathway integration. Partnerships across pharmaceutical and diagnostics ecosystems are increasingly important to strengthen biomarker-driven positioning and accelerate uptake. Market participants also compete on access strategies, reimbursement support, and regional expansion in high-growth geographies.

Merck & Co., Inc. maintains a strong position through immunotherapy leadership and continued expansion across urothelial and muscle-invasive settings. The company strategy emphasizes clinical evidence generation, combination development, and expanding treatment eligibility across earlier and later stages of bladder cancer care. Continued investment in oncology development supports differentiated positioning against competing checkpoint inhibitors and combination regimens. Integration with evolving diagnostic pathways strengthens treatment selection and supports adoption consistency across major oncology centers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Merck & Co., Inc.

- Bristol-Myers Squibb Company

- F. Hoffmann-La Roche Ltd.

- Johnson & Johnson

- AstraZeneca plc

- Pfizer Inc.

- Novartis AG

- Eli Lilly and Company

- Sanofi

- Thermo Fisher Scientific Inc.

- Siemens Healthineers AG

- Abbott Laboratories

- QIAGEN N.V.

- Illumina, Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In March 2026, Pfizer Inc., together with Merck, announced new late‑stage results for the Padcev plus Keytruda combination in muscle‑invasive bladder cancer showing the regimen cut the risk of disease progression, recurrence, or death by 47% and reduced the risk of death by 35% compared with standard cisplatin‑based chemotherapy, reinforcing the role of this chemo‑free doublet as a practice‑changing bladder cancer therapy.

- In February 2026, Merck & Co., Inc. reported late‑breaking Phase 3 KEYNOTE‑B15/EV‑304 data showing that its immunotherapy Keytruda, combined perioperatively with the antibody‑drug conjugate Padcev for cisplatin‑eligible muscle‑invasive bladder cancer, significantly improved event‑free survival, overall survival, and pathologic complete response versus standard neoadjuvant chemotherapy and surgery, supporting a potential new standard of care in bladder cancer therapeutics.

- In October 2025, F. Hoffmann‑La Roche Ltd. announced positive Phase 3 IMvigor011 results showing that adjuvant Tecentriq, guided by Natera’s Signatera ctDNA assay in patients with ctDNA‑positive muscle‑invasive bladder cancer after cystectomy, reduced the risk of death by 41% and the risk of disease recurrence or death by 36% versus placebo, highlighting a ctDNA‑guided immunotherapy approach that integrates diagnostics and therapeutics in bladder cancer management.

- In January 2025, Pfizer Inc. also reported that its pivotal Phase 3 CREST trial in high‑risk non‑muscle invasive bladder cancer met its primary endpoint, with the investigational PD‑1 inhibitor sasanlimab plus BCG demonstrating a clinically meaningful and statistically significant benefit over BCG alone, marking the first major advance for BCG‑naïve NMIBC in over three decades and expanding Pfizer’s bladder cancer immunotherapy pipeline.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 5690.23 million |

| Revenue forecast in 2032 |

USD 8399.05 million |

| Growth rate (CAGR) |

5.72% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Type, By Cancer Type, By Stage of Cancer, By End User |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Merck & Co., Inc.; Bristol-Myers Squibb Company; F. Hoffmann-La Roche Ltd.; Johnson & Johnson; AstraZeneca plc; Pfizer Inc.; Novartis AG; Eli Lilly and Company; Sanofi; Thermo Fisher Scientific Inc.; Siemens Healthineers AG; Abbott Laboratories; QIAGEN N.V.; Illumina, Inc. |

| No. of Pages |

340 |

Segmentation

By Type

- Diagnostics

- Cystoscopy

- Biopsy

- Urine Cytology

- Urinary Biomarkers

- Imaging Techniques

- Therapeutics

- Chemotherapy

- Immunotherapy

- Targeted Therapy

- Radiation Therapy

- Surgery

By Cancer Type

- Urothelial / Transitional Cell Carcinoma

- Squamous Cell Carcinoma

- Adenocarcinoma

- Other Rare Types

By Stage of Cancer

- Non-Muscle Invasive

- Muscle Invasive

- Metastatic

By End User

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centers

- Research & Academic Institutes

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa