Body Fluid Collection & Diagnostics Market Overview:

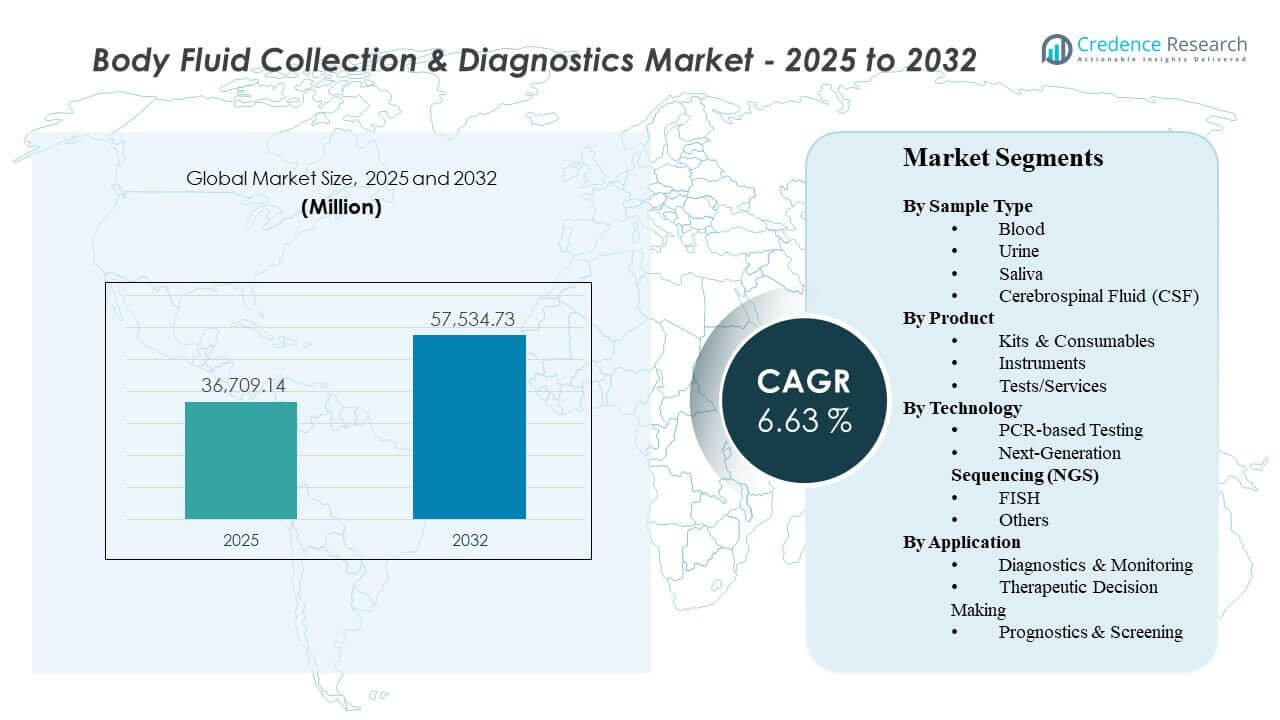

The global Body Fluid Collection & Diagnostics Market size was estimated at USD 36,709.14 million in 2025 and is expected to reach USD 57,534.73 million by 2032, growing at a CAGR of 6.63% from 2025 to 2032. Demand is being reinforced by rising diagnostic test volumes across infectious disease, oncology, and chronic disease monitoring, where repeat testing and faster turnaround requirements increase utilization of standardized collection and testing workflows. North America and Europe continue to anchor revenue through mature lab networks and reimbursement-driven adoption, while Asia Pacific contributes incremental growth through expanding access, capacity build-outs, and broader molecular testing penetration.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Body Fluid Collection & Diagnostics Market Size 2025 |

USD 36,709.14million |

| Body Fluid Collection & Diagnostics Market, CAGR |

6.63% |

| Body Fluid Collection & Diagnostics Market Size 2032 |

USD 57,534.73 million |

Key Market Trends & Insights

- Blood represented 74.9% share (base-year reference) within sample-type usage, reflecting dominant routine testing and monitoring pathways.

- Kits & consumables accounted for 66.8% share (base-year reference), supported by recurring procurement and standardized workflows across labs.

- PCR-based testing held 56.6% share (base-year reference), sustained by speed, scalability, and broad clinical fit for targeted detection.

- Diagnostics & monitoring contributed 42.3% share (base-year reference) as ongoing patient management increases repeat testing frequency.

- Asia Pacific is associated with the fastest regional expansion in referenced outlook tracking, supported by accelerating diagnostic capacity build-outs, broader testing access, and rising adoption of advanced molecular workflows.

Segment Analysis

Body Fluid Collection & Diagnostics Market demand concentrates around high-throughput workflows where sample collection, preparation, and testing must remain reliable, fast, and standardized across clinical settings. Blood-led testing continues to dominate because routine screening, chronic disease monitoring, and broad compatibility with molecular assays keep volumes structurally high. Provider preference for predictable turnaround and fewer pre-analytical errors supports widespread use of standardized consumables and validated protocols.

Technology adoption remains anchored in PCR for targeted detection needs across infectious disease and selected oncology panels, supported by mature instrumentation, clear operating procedures, and consistent performance in routine lab environments. At the same time, sequencing-based approaches expand where comprehensive profiling and biomarker depth is required, particularly in oncology and complex disease characterization. Application mix increasingly reflects a shift toward ongoing monitoring and therapy-aligned decisions, where testing frequency and clinical utility remain tightly linked to care pathways.

Sample Type Insights

Blood accounted for the largest share of 74.9% in 2024. Blood sampling leads because blood supports routine diagnostics across multiple disease areas and is integrated into standardized collection and lab processing pathways. Broad compatibility with molecular assays and biomarker workflows increases clinical utility across both acute and chronic settings. High test repetition for monitoring and follow-up sustains volume, reinforcing blood as the primary sample type in most lab menus.

Product Insights

Kits & Consumables accounted for the largest share of 66.8% in 2024. Kits and consumables lead because recurring purchasing aligns with high testing throughput and routine replenishment cycles in laboratories and hospitals. Pre-validated kits standardize workflows and reduce variability across operators, improving operational efficiency. Supply chain consolidation and preferred-vendor contracting further supports consumables volume concentration across large lab networks.

Technology Insights

PCR-based Testing accounted for the largest share of 56.6% in 2024. PCR adoption remains highest because PCR provides fast turnaround, scalable throughput, and strong fit for targeted detection requirements. Mature installation bases and trained personnel reduce operational friction for PCR deployment across decentralized and centralized labs. Continued demand for reliable routine molecular testing sustains PCR as the primary modality in many diagnostic workflows.

Application Insights

Diagnostics & Monitoring accounted for the largest share of 42.3% in 2024. Diagnostics and monitoring lead because repeated testing is embedded in chronic disease management, treatment response tracking, and follow-up protocols. Clinical pathways favor standardized testing intervals, supporting consistent demand for collection and diagnostic services. Expanding biomarker monitoring and longitudinal patient management further reinforces this application segment.

Body Fluid Collection & Diagnostics Market Drivers

Expansion of routine testing volumes across infectious and chronic diseases

Body Fluid Collection & Diagnostics Market growth is supported by increasing diagnostic utilization across infectious diseases and chronic conditions that require repeated monitoring. Routine testing demand increases the need for standardized collection workflows that reduce pre-analytical variability. Hospitals and laboratories prioritize reliability and throughput to manage growing sample loads. Higher testing frequency strengthens recurring demand for consumables and routine molecular workflows. This also pushes providers to streamline phlebotomy, transport, and sample-processing steps to avoid bottlenecks at peak volumes.

- For instance, Roche reported that its cobas 6800/8800 systems can generate up to 96 results in about 3 hours, with total throughput of 1,440 results per 24 hours on the cobas 6800 and 4,128 results per 24 hours on the cobas 8800, demonstrating how routine high-volume testing depends on standardized and scalable workflows.

Broader adoption of molecular diagnostics in clinical workflows

Clinical pathways increasingly incorporate molecular methods for faster detection, improved sensitivity, and targeted analysis, supporting sustained demand for collection and diagnostic solutions. PCR continues to anchor many routine molecular workflows due to speed and scalability. Expanded molecular testing increases requirements for validated sample preparation and standardized kit-based workflows. The shift toward molecular adoption reinforces investment in instruments, reagents, and workflow optimization. As testing expands beyond reference labs, ease-of-use and interoperability with LIS/LIMS systems become stronger purchasing criteria.

- For instance, Cepheid states that its GeneXpert platform supports more than 20 FDA-cleared or authorized tests, delivers most PCR results in less than 1 hour, and is available in configurations from 2 to 80 modules with LIS and EMR interface capabilities, highlighting why decentralized molecular adoption favors scalable and interoperable systems.

Growth of biomarker-led decision-making and monitoring

Therapeutic decisions and monitoring pathways increasingly depend on biomarkers that require reliable sample collection and validated diagnostics. Oncology and other complex conditions drive greater use of advanced testing approaches where the clinical value of detailed profiling is higher. Biomarker usage supports repeat testing cycles across patient journeys, increasing overall test volumes. This dynamic benefits both consumables-driven workflows and service-based diagnostic offerings. It also increases demand for higher-quality sample integrity controls to ensure comparability across longitudinal results.

Laboratory capacity build-outs and workflow standardization initiatives

Healthcare systems expand laboratory capacity and standardize operating procedures to reduce turnaround time and improve consistency across sites. Consolidated lab networks adopt harmonized kits and protocols to manage quality and procurement efficiency. Standardization reduces operational friction, supports repeatable performance, and improves scale economics. These changes reinforce demand for integrated workflows across collection devices, consumables, instruments, and testing services. In parallel, automation and centralized procurement help reduce unit costs while improving consistency across multi-site lab networks.

Body Fluid Collection & Diagnostics Market Challenges

Body Fluid Collection & Diagnostics Market participants face variability in reimbursement coverage and testing guidelines across geographies and applications, which can slow adoption for newer assays and advanced modalities. Pricing pressure in mature markets increases the need for efficiency, differentiation, and value-based evidence that supports continued utilization. Operational constraints such as workforce shortages and training needs can limit the pace of molecular workflow expansion in some settings.

Quality and consistency risks remain material across pre-analytical steps, where sample handling, transport, and processing variability can influence results and re-test rates. Supply chain disruptions for critical reagents and consumables can create workflow instability and inventory constraints. Data integration challenges across instruments, laboratory information systems, and reporting pipelines can slow full workflow modernization, especially in fragmented provider environments.

- For instance, BD states that its Vacutainer Barricor plasma blood collection tubes are optimally centrifuged at 4,000 RCF for 3 minutes, compared with a minimum of 1,800 RCF for 10 minutes, while Sysmex reports that Caresphere XQC receives IQC data from approximately 13,000 analyzers worldwide and supports peer groups of up to 1,500 analyzers with results available within minutes, illustrating how vendors are using measurable workflow and connectivity gains to address consistency and integration gaps.

Body Fluid Collection & Diagnostics Market Trends and Opportunities

Body Fluid Collection & Diagnostics Market trends include broader adoption of high-sensitivity methods for targeted detection and quantification, alongside gradual scaling of comprehensive profiling approaches where clinical need is strongest. Sequencing-related workflows expand as costs decline and evidence supporting clinical utility grows, especially in oncology and complex disease characterization. Providers increasingly prioritize standardized workflows that reduce variability and improve turnaround time, supporting kit-based adoption and integrated sample-to-result pathways.

Opportunities emerge from expansion of testing access in developing health systems and from the shift toward longitudinal monitoring in chronic and high-risk patient groups. Growth of biomarker-driven care supports demand for both routine and advanced diagnostics tied to treatment selection and response assessment. Partnerships that integrate sample collection, preparation, and analysis within unified workflows can improve adoption by lowering operational complexity and increasing reliability.

- For instance, Natera reports that its Signatera colorectal cancer program has generated data in more than 2,240 patients, showed that Signatera-positive patients had a 35x higher risk of recurrence, and detected relapse 6 months before recurrence, while the company also states that MRD testing and tumor genomic profiling can be performed from a single sample to streamline longitudinal monitoring workflows.

Regional Insights

North America

Body Fluid Collection & Diagnostics Market revenue in North America is estimated at 43.90% share in 2025, supported by mature laboratory networks, broad reimbursement coverage, and high diagnostic utilization. Demand is reinforced by established molecular testing capacity and procurement scale across large provider and lab organizations. Ongoing innovation in assay menus and workflow automation supports continued adoption across hospitals and reference laboratories.

Europe

Europe is estimated at 25.40% share in 2025, reflecting broad access to diagnostic services and established quality standards across clinical laboratories. Adoption remains supported by structured screening and monitoring pathways, alongside steady modernization of molecular and precision diagnostics in major markets. Procurement frameworks and health system cost controls increase emphasis on standardized workflows and demonstrable clinical utility.

Asia Pacific

Asia Pacific is estimated at 23.10% share in 2025, underpinned by expanding access to diagnostic services, capacity build-outs, and rising molecular testing penetration. Growth is supported by increasing healthcare investment, public health initiatives, and broader availability of advanced diagnostics in large population centers. The regional trajectory aligns with faster expansion versus mature markets as infrastructure and testing volume scale.

Latin America

Latin America is estimated at 4.80% share in 2025, with demand driven by improving laboratory access, gradual modernization of diagnostic capacity, and higher testing demand in major urban healthcare hubs. Growth depends on expansion of procurement capacity, strengthened supply chains, and broader adoption of standardized workflows. Public-private initiatives and reference-lab expansion can further increase testing availability over time.

Middle East & Africa

Middle East and Africa is estimated at 2.80% share in 2025, reflecting varied diagnostic infrastructure maturity across countries. Demand growth is supported by investment in hospital networks, national laboratory upgrades, and expanding access to routine diagnostics. Adoption rates are influenced by procurement constraints, workforce capacity, and the pace of laboratory modernization initiatives.

Competitive Landscape

Body Fluid Collection & Diagnostics Market competition is shaped by end-to-end workflow coverage across collection devices, sample preparation, assay development, instruments, and data integration. Companies differentiate through breadth of test menus, workflow standardization, automation support, and installed base expansion strategies that reduce operational complexity for laboratories. Scale advantages in manufacturing and distribution strengthen positioning for recurring consumables demand, while partnerships and platform ecosystems help reinforce customer retention.

Thermo Fisher Scientific Inc. focuses on broad portfolio coverage spanning instruments, reagents, and molecular diagnostic workflows that support high-throughput laboratory needs. Thermo Fisher Scientific Inc. emphasizes standardized kits and scalable platforms that help laboratories maintain consistent performance across sites and operators. Thermo Fisher Scientific Inc. continues to reinforce workflow integration to improve turnaround and operational reliability for routine and molecular testing demand.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In November 2025, F. Hoffmann-La Roche Ltd. expanded its collaboration with Freenome to commercialize Freenome’s blood-based cancer screening technology in international markets, while also deepening R&D work around cfDNA testing and Roche’s SBX sequencing platform

- In July 2025, Thermo Fisher Scientific Inc. introduced LabLink360 and Thermo Scientific MAS Max quality controls at ADLM 2025, with the launch aimed at improving quality assurance and workflow efficiency in clinical and diagnostic laboratories.

- In June 2025, Illumina, Inc. announced a definitive agreement to acquire SomaLogic and related assets for $350 million in cash plus potential milestones, saying the deal would strengthen its proteomics and multiomics strategy for biomarker discovery and disease profiling.

- In January 2025, Bio-Rad Laboratories, Inc. took part in Geneoscopy’s $105 million Series C financing, and the company said Geneoscopy’s ColoSense colorectal cancer screening test is designed for use with Bio-Rad’s QXDx ddPCR platform, making this a notable diagnostics-related partnership and commercialization update.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 36709.14 million |

| Revenue forecast in 2032 |

USD 57534.73 million |

| Growth rate (CAGR) |

6.63% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

Sample Type; Product; Technology; Application |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Thermo Fisher Scientific Inc.; Bio-Rad Laboratories, Inc.; Illumina, Inc.; F. Hoffmann-La Roche Ltd.; QIAGEN N.V.; Becton, Dickinson and Company; Guardant Health, Inc.; Johnson & Johnson |

| No. of Pages |

335 |

Segmentation

Sample Type

- Blood

- Urine

- Saliva

- Cerebrospinal Fluid (CSF)

Product

- Kits & Consumables

- Instruments

- Tests/Services

Technology

- PCR-based Testing

- Next-Generation Sequencing (NGS)

- Fluorescence in situ hybridization (FISH)

- Others

Application

- Diagnostics & Monitoring

- Therapeutic Decision Making

- Prognostics & Screening

Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa