Bovine Blood Plasma Derivatives Market Overview:

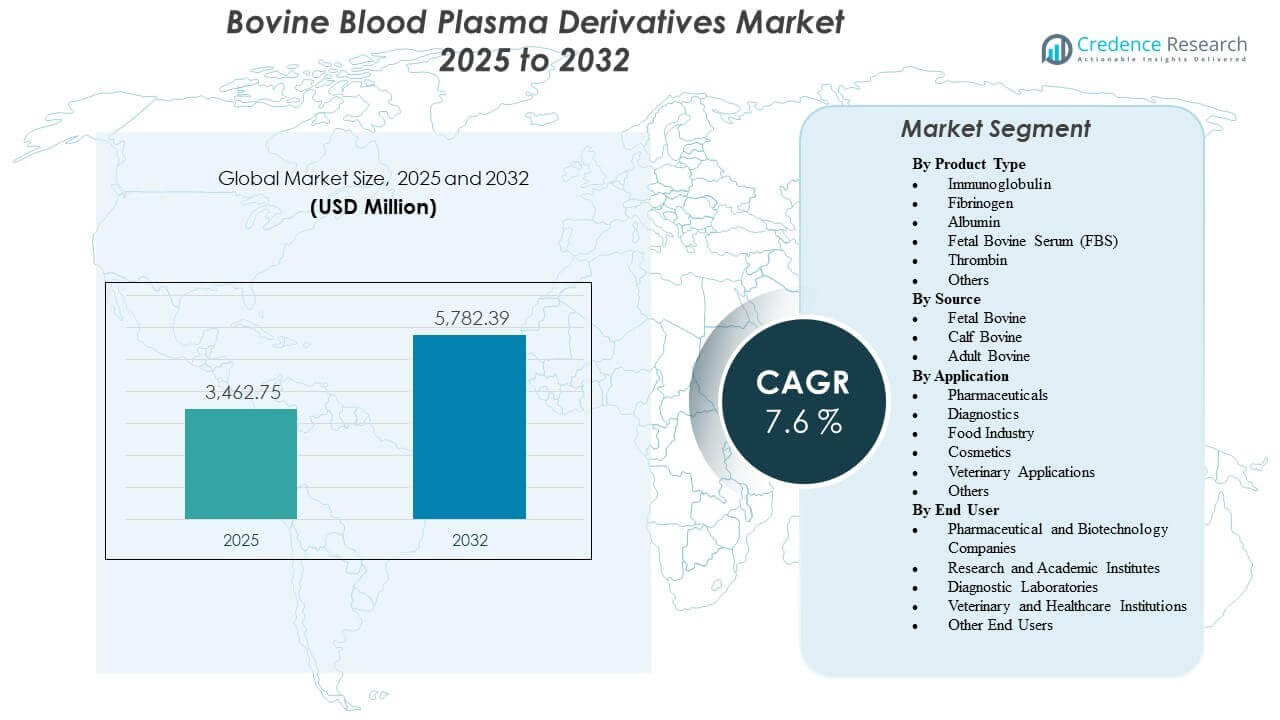

The global Bovine Blood Plasma Derivatives Market size was estimated at USD 3,462.75 million in 2025 and is expected to reach USD 5,782.39 million by 2032, growing at a CAGR of 7.6% from 2025 to 2032. Demand is being driven primarily by sustained biopharmaceutical and life-science activity that requires reliable bovine-derived proteins and sera for development workflows, analytical validation, and specialized manufacturing support. Expansion of diagnostics and research capacity, along with broader adoption of standardized quality controls and traceability requirements, continues to reinforce procurement of qualified plasma derivatives across both regulated and non-regulated use cases.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bovine Blood Plasma Derivatives Market Size 2025 |

USD 3,462.75 million |

| Bovine Blood Plasma Derivatives Market, CAGR |

7.6% |

| Bovine Blood Plasma Derivatives Market Size 2032 |

USD 5,782.39 million |

Key Market Trends & Insights

- The market is projected to expand from USD 3,462.75 million (2025) to USD 5,782.39 million (2032) at a 7.6% CAGR (2025–2032).

- North America accounted for 39.2% of total revenue in 2025, reflecting strong concentration of biopharma and research demand.

- Fetal Bovine Serum (FBS) represented 23.5% share in 2025 within product types, supported by broad cell-culture compatibility and recurring usage.

- Pharmaceuticals accounted for 26.5% share in 2025 by application, underpinned by biologics development and manufacturing support requirements.

- Hospitals & clinics held 28.5% share in 2025 by end user, supported by clinical usage of plasma-derived components and steady institutional procurement.

Segment Analysis

Adoption of bovine blood plasma derivatives remains closely tied to quality-critical workflows where protein functionality, consistency, and traceability are central purchasing criteria. Buyers typically prioritize validated testing profiles, supply continuity, and lot-to-lot performance because downstream variability can disrupt assay reproducibility, cell growth performance, or process comparability. As a result, qualified sourcing and robust screening practices influence vendor selection as strongly as price, especially for regulated or documentation-heavy programs.

Market demand is supported by broad use across biopharma development, diagnostics, and research environments, where multiple derivative types serve distinct roles. Some users are optimizing costs and compliance by segmenting procurement between premium-qualified materials for sensitive applications and standard grades for routine workflows. At the same time, growth in advanced research and complex biologics programs is encouraging deeper specification of inputs, including tighter origin documentation and expanded contamination screening.

By Product Type Insights

Fetal Bovine Serum (FBS) accounted for the largest share of 23.5% in 2025. It leads due to its wide compatibility across mammalian cell lines and its role as a broadly effective growth supplement for research and development workflows. Recurring consumption patterns and the need for reliable performance across assays and cell culture protocols support consistent demand. Supplier differentiation is often strongest in this segment, as buyers value traceability, screening depth, and lot qualification support for sensitive applications.

By Source Insights

Source selection is primarily driven by application sensitivity, desired protein profiles, and documentation requirements rather than a single universally dominant input category. Fetal-derived material is typically preferred for more sensitive cell culture contexts where growth performance and consistency are prioritized, while calf and adult sources can be used where functional requirements differ or cost and availability considerations play a larger role. Import controls, veterinary compliance frameworks, and origin documentation can influence purchasing decisions and shift sourcing preferences over time. Supply continuity and traceability remain core selection criteria across all source categories.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Application Insights

Pharmaceuticals accounted for the largest share of 26.5% in 2025. The segment leads because plasma derivatives and sera support biologics development workflows, analytical comparability, and specialized production or validation needs across drug pipelines. Demand is reinforced by the scale-up of biologics programs and the requirement for consistent inputs during development and manufacturing transitions. Procurement decisions in this segment tend to emphasize documentation strength, quality-system maturity, and long-term supply assurance.

By End User Insights

Hospitals & clinics accounted for the largest share of 28.5% in 2025. This leadership reflects steady institutional procurement and the clinical relevance of certain plasma-derived components in treatment and procedural workflows. Large facilities tend to prefer dependable supply chains and standardized specifications aligned with internal quality and compliance processes. Even where procurement is centralized, demand remains stable due to recurring clinical needs and ongoing replacement cycles.

Bovine Blood Plasma Derivatives Market Drivers

Expansion of biopharmaceutical activity and biologics development

Biopharmaceutical development continues to increase reliance on consistent biological inputs that support reproducible upstream and analytical workflows. Plasma derivatives and sera are used across development pathways where performance consistency reduces experimental variability and helps maintain comparability across stages. As programs progress from research to late-stage development, documentation and quality requirements tighten, reinforcing demand for qualified materials. This dynamic supports both volume growth and premiumization for higher-grade inputs.

- For instance, Cytiva states that its HyClone Characterized FBS is produced using true pool technology to reduce bottle-to-bottle variability, is triple-filtered through sequential 100 nm (0.1 µm) filters, is endotoxin-tested at ≤10EU/mL, and undergoes virus panel testing for each lot under 9 CFR 113.53.

Increased emphasis on quality control, traceability, and standardized specifications

Buyers increasingly require stronger traceability, origin documentation, and contamination screening to reduce risk in sensitive workflows. These expectations influence vendor qualification, contract structuring, and the selection of application-specific grades. Standardization efforts also raise the value of supplier support services such as lot qualification, documentation packages, and testing transparency. Over time, these factors shift purchasing toward suppliers with robust quality systems and reliable supply continuity.

- For instance, Corning reports that its FBS is fully traceable to the abattoir, is triple 0.1 micron sterile filtered to a Sterility Assurance Level of 10^-3, and that every lot must pass USP <71> and EP 2.6.1 sterility testing, test negative for mycoplasma, and meet a gamma-glutamyl transferase authenticity threshold of ≤10IU/L.

Growth in diagnostics, research testing, and laboratory throughput

Laboratory-based activity supports demand across multiple derivative types used for assay development, validation, and routine testing. Higher throughput environments value materials that improve reproducibility and reduce rework caused by variability. As diagnostic development expands across multiple disease areas, broader use of validated reagents and inputs supports steady consumption. This also increases demand for suppliers offering consistent quality and stable availability.

Diversification of end-use demand beyond traditional research workflows

Beyond academic and research institutions, end-use demand is supported by clinical settings, diagnostic labs, veterinary institutions, and industrial users with specialized applications. This diversification increases baseline demand stability because growth is not dependent on a single customer group. It also expands the range of grade requirements, from premium-qualified inputs to cost-optimized options. Vendors that can manage multi-grade portfolios and maintain quality assurance at scale tend to benefit most.

Bovine Blood Plasma Derivatives Market Challenges

Supply-side constraints and compliance complexity remain persistent challenges, particularly for products requiring strict origin documentation and extensive screening. Variability risks, including lot-to-lot performance differences, can create additional qualification time and costs for end users, especially in sensitive cell culture workflows. Logistics constraints, storage requirements, and cold-chain handling can further increase cost and risk for global supply. In addition, procurement teams may face uncertainty when regulations or trade restrictions affect sourcing flexibility.

Competitive pressure also intensifies around quality documentation, validation support, and long-term availability commitments. Buyers often reduce vendor counts to limit variability and simplify qualification, which increases switching friction and raises expectations for supplier performance. The need to maintain consistent specifications while scaling supply can be operationally challenging. Pricing pressure may rise when buyers seek cost optimization for non-critical grades, compressing margins in more commoditized product lines.

- For instance, Merck states that it purchases the same approved cell culture media raw materials from the same qualified suppliers for use across all manufacturing sites, and its harmonized quality framework covers five sites Lenexa, St. Louis-Broadway, Irvine, Darmstadt, and Nantong under ISO 9001:2015 certification.

Market Trends and Opportunities

A key trend is the increasing segmentation of procurement strategies, where organizations adopt tiered sourcing based on application criticality. Higher-grade, tightly qualified materials are increasingly prioritized for regulated or sensitive workflows, while standard grades are reserved for routine use. This creates opportunities for suppliers to expand differentiated portfolios and value-added services such as lot reservation programs, enhanced documentation, and expanded screening profiles. Over time, premium-grade demand can support stronger average selling prices in parts of the market.

- For instance, Thermo Fisher Scientific positions its Gibco MaxSpec FBS as a premium input for sensitive cell culture workflows, with up to 76 quality specification tests and release limits of ≤1 EU/mL endotoxin and ≤15 mg/dL hemoglobin, demonstrating how tighter qualification standards and deeper screening profiles can support differentiated premium-grade sourcing.

Another trend is the steady expansion of bioprocessing capability in developing and emerging hubs, creating new demand pools outside traditional strongholds. Growth in local research infrastructure and diagnostics capacity supports regional consumption and encourages local stocking and distribution partnerships. Suppliers that strengthen regional availability, technical support, and supply assurance can capture incremental growth. Portfolio breadth across derivative types also becomes a competitive advantage as customers prefer fewer suppliers that can meet multiple needs.

Regional Insights

North America

North America held the largest share at 39.2% in 2025, supported by strong concentration of biopharmaceutical development activity, mature research infrastructure, and high laboratory throughput. Demand is reinforced by stringent quality expectations that elevate the value of traceability, screening depth, and supplier validation support. Institutional procurement in clinical and research settings helps stabilize baseline consumption. Buyers frequently prefer established suppliers with strong documentation and supply continuity.

Europe

Europe accounted for 23.6% share in 2025, anchored in established biopharma ecosystems, regulated laboratory environments, and consistent diagnostics activity. Purchasing decisions often emphasize specification consistency and documented quality systems to support reproducibility and compliance. Demand remains steady across research institutes and commercial laboratories that require reliable reagent inputs. Multi-country distribution strength and regional stock availability are important competitive factors.

Asia Pacific

Asia Pacific represented 23.1% share in 2025, supported by expanding biopharma manufacturing capacity, rising research intensity, and broadening diagnostics access. Growth is reinforced by increasing investment in laboratory capabilities and the scaling of development programs that require consistent biological inputs. Buyers are increasingly focusing on quality assurance and stable supply as usage expands. Vendors that improve regional support and local availability are positioned to benefit from sustained demand expansion.

Latin America

Latin America held 8.4% share in 2025, reflecting a smaller but steadily developing base of diagnostics activity, veterinary demand, and applied research usage. Demand is supported by growth in laboratory networks and gradual modernization of testing and research capabilities. Procurement can be more price-sensitive, increasing importance of portfolio flexibility across multiple grades. Supply reliability and distribution coverage remain key requirements for buyers.

Middle East & Africa

The Middle East & Africa accounted for 5.7% share in 2025, supported by gradual expansion of healthcare and laboratory infrastructure and selective growth in research capability. Demand is often concentrated in major urban centers and larger institutional buyers. Import dependency and logistics complexity can shape procurement cycles and supplier selection. Vendors that provide dependable distribution and consistent documentation can strengthen competitiveness in this region.

Competitive Landscape

Competition in the bovine blood plasma derivatives market centers on quality assurance strength, traceability, screening depth, and the ability to deliver consistent lots at scale. Suppliers differentiate through validated testing profiles, documentation packages aligned to regulated workflows, and service models that support qualification and repeatability. Portfolio breadth across derivative types and reliable global distribution are major advantages, particularly for customers seeking vendor consolidation. Long-term relationships are reinforced by switching costs tied to re-qualification and performance comparability requirements.

Thermo Fisher Scientific Inc. is positioned with broad life-science portfolio coverage and distribution capability that supports recurring demand for cell culture and bioprocessing inputs. The company’s approach typically emphasizes standardized product specifications, support for qualification needs, and global availability for multi-site users. Its market relevance benefits from cross-selling across related laboratory consumables and workflow solutions. Strong channel reach and technical support can reinforce customer stickiness in documentation-heavy environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In February 2026, Dyadic Applied BioSolutions and Proliant Health & Biologicals announced the commercial launch of their jointly developed recombinant human albumin product, marking the first commercial sale of a Dyadic-produced recombinant protein.

- In February 2025, Thermo Fisher Scientific Inc. announced a definitive agreement to acquire Solventum’s Purification & Filtration business for about $4.1 billion in cash, a move that strengthens Thermo Fisher’s bioprocessing portfolio and is relevant to plasma-derived and biologics manufacturing workflows.

- In December 2025, Auckland BioSciences Ltd announced its acquisition of Christchurch-based Genesis BioLab, saying the deal would expand its nutraceutical capabilities while building on its existing bioactives business, where animal serum is used in cell-culture and biopharmaceutical manufacturing

- In November 2024, BioWest (France) launched a new high-quality bovine serum specifically designed for large-scale cell culture applications. The serum is derived from clotted whole blood collected aseptically from a fetus via cardiac puncture, in full compliance with European regulations, and was selected for its premium endotoxin levels, hemoglobin profile, and superior cell growth properties, ensuring reliable and reproducible results for biopharmaceutical researchers and manufacturers.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 3,462.75 million |

| Revenue forecast in 2032 |

USD 5,782.39 million |

| Growth rate (CAGR) |

7.6% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2025–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook; By Source Outlook; By Application Outlook; By End User Outlook |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Thermo Fisher Scientific Inc.; Merck KGaA; Proliant Biologicals; LAMPIRE Biological Laboratories, Inc.; Rocky Mountain Biologicals, Inc.; Bovogen Biologicals Pty Ltd; Kraeber & Co GmbH; Atlanta Biologicals, Inc.; Auckland BioSciences Ltd; Cytiva |

| No. of Pages |

330 |

By Segmentation

By Product Type

- Immunoglobulin

- Fibrinogen

- Albumin

- Fetal Bovine Serum (FBS)

- Thrombin

- Others

By Source

- Fetal Bovine

- Calf Bovine

- Adult Bovine

By Application

- Pharmaceuticals

- Diagnostics

- Food Industry

- Cosmetics

- Veterinary Applications

- Others

By End User

- Pharmaceutical and Biotechnology Companies

- Research and Academic Institutes

- Diagnostic Laboratories

- Veterinary and Healthcare Institutions

- Other End Users

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa