| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Bowel Management Systems Market Size 2024 |

USD 1,835.39 million |

| Bowel Management Systems Market, CAGR |

3.98% |

| Bowel Management Systems Market Size 2032 |

USD 2,498.68 million |

Market Overview:

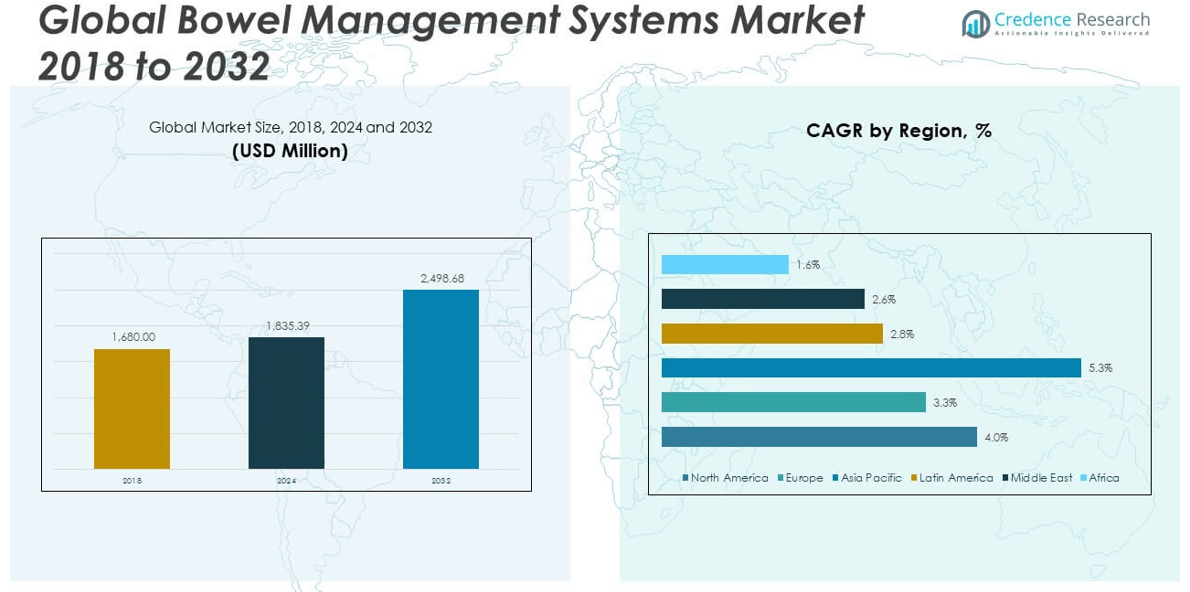

The Bowel Management Systems Market size was valued at USD 1,680.00 million in 2018 to USD 1,835.39 million in 2024 and is anticipated to reach USD 2,498.68 million by 2032, at a CAGR of 3.98% during the forecast period.

The bowel management systems market is primarily driven by the rising prevalence of chronic bowel disorders, including fecal incontinence, constipation, and neurogenic bowel dysfunction, especially among the elderly and pediatric populations. An increasing number of patients suffering from spinal cord injuries, multiple sclerosis, and spina bifida is fueling the demand for advanced bowel care solutions. Additionally, continuous innovation in device design—such as improved rectal catheters, irrigation systems, and nerve modulation devices—enhances patient comfort and clinical efficacy, boosting adoption. The market is further supported by the growing preference for homecare and ambulatory treatment settings, driven by cost-effectiveness and convenience. With patients seeking discreet, non-invasive solutions, companies are focusing on portable, user-friendly products. Furthermore, increasing awareness, supportive reimbursement frameworks, and healthcare reforms in both developed and emerging countries are expanding access to bowel management technologies, reinforcing overall market growth and encouraging early diagnosis and treatment interventions across multiple care environments.

North America holds the largest share of the bowel management systems market, with the United States leading due to a high prevalence of bowel-related conditions, a strong reimbursement infrastructure, and widespread adoption of advanced medical devices. Europe follows closely, driven by its aging population, rising healthcare spending, and robust clinical research landscape. Both regions benefit from favorable regulatory environments and established healthcare networks. However, Asia-Pacific is emerging as the fastest-growing regional market, propelled by rising awareness, improving healthcare infrastructure, and increasing incidence of gastrointestinal disorders. Countries like India, China, and Japan are witnessing rapid adoption due to expanding access to diagnostic tools and treatment options. Government initiatives aimed at promoting chronic disease management further support growth in these areas. Latin America and the Middle East & Africa, although still developing, are gradually witnessing market traction due to increasing healthcare investments, local manufacturing partnerships, and a growing emphasis on patient-centered bowel care solutions.

Market Insights:

- The Bowel Management Systems Market was valued at USD 1,835.39 million in 2024 and is projected to reach USD 2,498.68 million by 2032, growing at a CAGR of 3.98%.

- Increasing prevalence of fecal incontinence, constipation, and neurogenic bowel dysfunction among aging and pediatric populations is driving market demand.

- Continuous innovation in irrigation systems, nerve modulation devices, and rectal catheters is improving comfort, safety, and patient adherence.

- The growing shift toward homecare and outpatient settings is expanding revenue opportunities, especially through portable and user-friendly products.

- Emerging markets in Asia-Pacific and Latin America are showing high growth potential due to better healthcare access, rising awareness, and local manufacturing.

- High device costs and inconsistent reimbursement policies are limiting adoption in cost-sensitive and underinsured regions.

- North America leads the market share, while Asia-Pacific is the fastest-growing region supported by government initiatives and increasing diagnostic access.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

Market Drivers:

Increasing Prevalence of Chronic Bowel Disorders Across Age Groups is Fueling Device Demand

The Bowel Management Systems Market continues to expand due to the rising incidence of chronic bowel disorders such as fecal incontinence, constipation, irritable bowel syndrome, and neurogenic bowel dysfunction. These conditions affect a growing number of individuals, particularly the elderly and those with neurological impairments like spinal cord injuries and multiple sclerosis. The pediatric population, especially children with congenital anomalies such as spina bifida, also requires consistent bowel care solutions. This broad patient base sustains long-term demand for effective and accessible bowel management systems. The healthcare community increasingly recognizes the need for proactive intervention and symptom management. This shift supports the consistent deployment of bowel care solutions across hospitals, rehabilitation centers, and homecare settings.

Product Innovations and Clinical Advancements Are Enhancing System Effectiveness

Device manufacturers are introducing novel bowel management solutions that improve safety, comfort, and usability. The Bowel Management Systems Market benefits from technology upgrades including automated irrigation systems, soft silicone rectal catheters, and neuromodulation therapies. These innovations address patient concerns related to discomfort, leakage, and hygiene, making systems more acceptable for routine use. Companies are also improving product packaging and portability to support at-home application. Regulatory bodies continue to approve new devices backed by positive clinical outcomes, which strengthens provider confidence in recommending them. These advancements support better patient outcomes and align with the medical community’s shift toward personalized care.

- For example, Consure Medical’s Qora Stool Management Kit uses a self-expanding stent that exerts zero radial pressure, eliminating the need for balloon inflation and reducing the risk of mucosal injury

Shift Toward Home-Based and Outpatient Care Is Creating New Revenue Opportunities

There is a growing preference among patients and providers for bowel management solutions that support treatment in home and outpatient settings. The Bowel Management Systems Market is evolving to meet this demand by offering user-friendly products that allow individuals to manage their condition independently or with minimal caregiver assistance. Homecare devices reduce the need for hospital visits, lower long-term healthcare costs, and improve quality of life. This trend also reduces the burden on healthcare systems, particularly in regions facing hospital resource constraints. Manufacturers are focusing on product designs that are simple to use, discreet, and effective outside clinical environments. It helps build patient trust and expands the overall user base.

- For example, Medtronic, its InterStim Micro neuromodulation device used for bowel and bladder control is the smallest rechargeable sacral nerve stimulator on the market at just 2.8 cm³. It offers 20-minute weekly recharging and has shown over 50% reduction in incontinence episodes in 80% of patients within 3 months, based on internal clinical audits

Rising Healthcare Access in Developing Economies Is Expanding the Market Landscape

Emerging economies are becoming important contributors to the growth of the Bowel Management Systems Market. Improved healthcare infrastructure, rising awareness of chronic bowel conditions, and government investments in medical technology access have expanded treatment availability. Public and private initiatives targeting geriatric and pediatric care are helping increase device penetration. Local distribution partnerships and regional manufacturing have made products more affordable and accessible. As medical professionals in these regions adopt modern bowel care protocols, the need for advanced systems continues to rise. It strengthens the market presence of global players while enabling regional firms to develop tailored solutions.

Market Trends:

Adoption of Digital Health Integration is Enhancing Bowel Care Monitoring

The integration of digital technologies with bowel management systems is reshaping clinical and at-home care. Device manufacturers are embedding smart sensors and Bluetooth-enabled modules into irrigation systems and monitoring units. These tools enable real-time data tracking, allowing patients and caregivers to monitor bowel activity and adherence to treatment routines more effectively. Clinicians benefit from remote access to usage reports and alerts, enabling timely interventions without in-person visits. This digital transition aligns with the broader movement toward telehealth and remote patient management. The Bowel Management Systems Market is increasingly incorporating such features to improve user compliance, optimize treatment plans, and reduce complications related to delayed care.

Growing Emphasis on Sustainable and Eco-Friendly Medical Device Design

Sustainability has emerged as a critical focus in medical device manufacturing. In the Bowel Management Systems Market, companies are shifting toward environmentally friendly materials, reducing single-use plastics, and adopting recyclable packaging. Hospitals and home users are demanding products that balance performance with lower environmental impact. Some manufacturers now use biodegradable components in disposable parts of bowel kits and adopt energy-efficient production methods. Regulatory bodies and procurement organizations are also prioritizing sustainability in device selection. It pushes market participants to innovate in ways that support both healthcare outcomes and environmental responsibility.

Increased Use of Bowel Management Systems in Critical Care Settings

Critical care units are witnessing higher deployment of advanced bowel management systems to maintain patient hygiene and prevent infection. Intensive care patients, especially those with reduced mobility or neurological trauma, often require effective fecal containment. Hospitals are standardizing bowel management protocols in ICUs to avoid complications such as pressure injuries and catheter-associated infections. The Bowel Management Systems Market is responding with systems specifically designed for high-dependency environments, featuring secure placement, anti-leak barriers, and minimal skin contact. This trend supports faster recovery and improved patient outcomes. It also aligns with infection control priorities and hospital quality benchmarks.

- For example, the Flexi-Seal™ PROTECT PLUS by ConvaTec is specifically designed for critical care, featuring a self-closing catheter and over-inflation warning system to prevent leakage and mucosal damage

Customizable Product Offerings Are Gaining Preference Among Patients and Providers

The market is witnessing a shift toward customized solutions tailored to patient-specific needs. Manufacturers are offering modular bowel management kits that allow caregivers to choose components based on anatomy, frequency of use, and comfort levels. This approach improves usability and reduces unnecessary cost by avoiding one-size-fits-all solutions. The Bowel Management Systems Market is moving toward flexible product lines that cater to various conditions, from temporary post-surgical care to long-term neurological management. Providers value this adaptability in managing diverse patient populations. It also helps improve patient satisfaction and long-term treatment adherence.

- For instance, ConvaTec’s Flexi-Seal™ product line includes multiple variants PROTECT, SIGNAL, and Fecal Collector each tailored to different patient needs and care environments

Market Challenges Analysis:

High Cost of Advanced Devices and Limited Reimbursement Hamper Broader Accessibility

The high cost of bowel management systems continues to pose a significant challenge, particularly for patients in low- and middle-income regions. Many of the latest solutions, including automated irrigation devices and implantable neuromodulation systems, remain out of reach for underinsured or uninsured individuals. The Bowel Management Systems Market faces resistance from healthcare providers and institutions when reimbursement policies do not adequately cover these devices. Inconsistent coverage across countries and insurance plans further complicates access to standardized care. Hospitals and clinics may delay adoption due to budget constraints or prefer lower-cost alternatives that offer limited efficacy. It affects both patient outcomes and market expansion in cost-sensitive segments.

Stigma and Lack of Awareness Limit Patient Willingness to Seek Early Treatment

Cultural stigma around bowel disorders significantly reduces diagnosis rates and delays treatment initiation. Many patients hesitate to discuss fecal incontinence or chronic bowel dysfunction due to embarrassment, leading to underreporting and poor disease management. The Bowel Management Systems Market struggles to reach its full potential when awareness about available treatments and products remains low. Healthcare providers also face challenges in educating patients about the importance of proactive bowel care. Limited training and discomfort in addressing these topics can lead to underutilization of clinically beneficial systems. It constrains market penetration, particularly in conservative societies and aging populations where such conditions are often normalized or ignored.

Market Opportunities:

Expansion into Emerging Markets Can Unlock Untapped Revenue Potential

Rising healthcare investments in emerging economies present a major opportunity for the Bowel Management Systems Market. Governments in Asia-Pacific, Latin America, and parts of Africa are strengthening healthcare infrastructure and promoting early diagnosis of chronic conditions. These developments create demand for effective bowel care solutions across both public and private healthcare settings. Local manufacturing partnerships and cost-efficient product adaptations can help global players improve accessibility. Training programs for healthcare professionals in these regions can further accelerate product adoption. It allows companies to diversify their revenue streams and reduce reliance on saturated markets.

Development of Pediatric-Specific Solutions Can Address an Underserved Segment

Children with congenital or neurological conditions often require long-term bowel management, yet few products cater specifically to their anatomical and clinical needs. The Bowel Management Systems Market can benefit from investing in pediatric-friendly devices that offer safety, ease of use, and comfort. Tailored product lines supported by caregiver education can improve outcomes and patient adherence. Pediatric hospitals and rehabilitation centers increasingly seek age-appropriate solutions. Collaborations with pediatric specialists and advocacy groups can support product innovation and market entry. It creates a strategic avenue for differentiation and long-term customer retention.

Market Segmentation Analysis:

The Bowel Management Systems Market is segmented by type, patient type, and end use, reflecting diverse clinical needs and care settings.

By type segments, colostomy bags account for a significant share due to their widespread use in post-surgical and chronic conditions. Irrigation systems are gaining traction for their non-invasive approach and suitability in home settings. Nerve modulation devices represent a high-growth segment, driven by innovation and long-term efficacy in treating neurogenic bowel dysfunction. The “others” category includes disposable kits and supportive accessories that contribute to patient hygiene and convenience.

- For example, Coloplast’s SenSura® Mio line is widely used for post-surgical and chronic bowel conditions like colorectal cancer and Crohn’s disease. According to Harvard Health, up to 1 million Americans live with an ostomy, and colostomy bags are essential for managing waste after surgery.

By patient type, the adult segment dominates the Bowel Management Systems Market due to the high prevalence of bowel disorders in aging populations. The pediatric segment is smaller but steadily expanding, especially with increased diagnosis of congenital and neurological conditions.

By end use, home care leads in revenue growth, supported by patient preference for privacy and ease of use. Hospitals remain key users for acute care, while ambulatory surgery centers are integrating systems for pre- and post-operative bowel management.

- For example, ConvaTec’s Flexi-Seal™ PROTECT PLUS are used to prevent infection and skin breakdown in immobilized patients.

Segmentation:

By Type:

- Colostomy Bags

- Irrigation Systems

- Nerve Modulation Devices

- Others

By Patient Type:

By End Use:

- Home Care

- Hospitals

- Ambulatory Surgery Centers

- Others

By Region:

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa

Regional Analysis:

The North America Bowel Management Systems Market size was valued at USD 606.48 million in 2018 to USD 654.49 million in 2024 and is anticipated to reach USD 889.78 million by 2032, at a CAGR of 4.0% during the forecast period. North America holds the largest share in the Bowel Management Systems Market, accounting for approximately 35% of the global market. Strong demand arises from a high prevalence of bowel disorders, advanced healthcare infrastructure, and a favorable reimbursement environment. The United States leads regional growth due to higher per capita health spending, awareness of bowel-related conditions, and access to technologically advanced devices. Hospitals and outpatient centers increasingly adopt neuromodulation therapies and closed-end catheter systems for patients with chronic conditions. It continues to benefit from continuous product innovation, FDA approvals, and rising demand in homecare settings. Market players prioritize North America for early product launches and large-scale clinical trials.

The Europe Bowel Management Systems Market size was valued at USD 495.60 million in 2018 to USD 522.67 million in 2024 and is anticipated to reach USD 676.52 million by 2032, at a CAGR of 3.3% during the forecast period. Europe represents the second-largest regional share, holding approximately 28% of the Bowel Management Systems Market. Countries such as Germany, France, and the U.K. show consistent demand driven by their aging populations and strong public healthcare systems. Clinical adoption of bowel care solutions in rehabilitation settings remains high, especially for stroke and spinal cord injury patients. It benefits from supportive reimbursement policies and rising integration of bowel care in post-acute treatment protocols. European manufacturers are also investing in sustainable and reusable product designs, which gain traction among healthcare providers. Government-backed awareness campaigns continue to reduce stigma around bowel disorders.

The Asia Pacific Bowel Management Systems Market size was valued at USD 396.48 million in 2018 to USD 453.06 million in 2024 and is anticipated to reach USD 682.89 million by 2032, at a CAGR of 5.3% during the forecast period. Asia Pacific holds around 24% of the Bowel Management Systems Market and is the fastest-growing region globally. Increasing incidence of neurogenic and colorectal disorders, expanding healthcare infrastructure, and rising awareness are driving adoption. Countries such as China, India, and Japan are investing in medical device procurement and homecare solutions for chronic conditions. It is witnessing higher demand for affordable and portable systems suited for both clinical and home settings. Growth is further supported by medical training programs and government initiatives targeting geriatric and post-surgical care. Regional distributors and partnerships with global firms are expanding the availability of advanced bowel care devices.

The Latin America Bowel Management Systems Market size was valued at USD 86.02 million in 2018 to USD 92.85 million in 2024 and is anticipated to reach USD 115.11 million by 2032, at a CAGR of 2.8% during the forecast period. Latin America contributes nearly 5% of the global Bowel Management Systems Market. Demand is gradually increasing in Brazil, Mexico, and Argentina, supported by growing access to healthcare services and a rising number of aging patients. Urban healthcare facilities are incorporating bowel management products into post-acute and critical care settings. It continues to face challenges related to affordability and limited awareness in rural regions. Market expansion depends on local partnerships and healthcare reforms aimed at improving chronic disease management. Educational outreach and training initiatives are helping increase product acceptance among both physicians and patients.

The Middle East Bowel Management Systems Market size was valued at USD 59.81 million in 2018 to USD 60.92 million in 2024 and is anticipated to reach USD 74.22 million by 2032, at a CAGR of 2.6% during the forecast period. The Middle East holds close to 3% of the Bowel Management Systems Market, with concentrated demand in countries like the UAE and Saudi Arabia. Private healthcare investments, growth of medical tourism, and advanced hospital infrastructure support market growth in urban centers. It is gaining moderate traction in rehabilitation and elder care facilities, particularly for spinal and neurological disorders. High-end hospitals are adopting modern systems, though penetration remains limited in public-sector institutions. Increasing collaboration between international device companies and regional distributors is expanding market reach. Educational programs and physician awareness are crucial for improving long-term adoption.

The Africa Bowel Management Systems Market size was valued at USD 35.62 million in 2018 to USD 51.40 million in 2024 and is anticipated to reach USD 60.14 million by 2032, at a CAGR of 1.6% during the forecast period. Africa accounts for approximately 2% of the global Bowel Management Systems Market. Most demand is concentrated in South Africa and Egypt, where private hospitals and urban clinics have greater access to medical technologies. Public awareness remains low, and limited reimbursement options hinder broader adoption. It still faces infrastructural and cost-related challenges in rural areas. Donor-funded healthcare programs and nonprofit initiatives play a small but important role in introducing basic bowel care solutions. Market growth remains modest but steady, with future potential tied to policy reforms and improved access to chronic care services.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Key Player Analysis:

- Convatec Inc.

- Becton Dickinson and Company

- ProSys International Ltd

- Suzhou Shenyun Medical Equipment Co., Ltd

- Coloplast Corp

- Consure Medical

- Axonics, Inc.

- SAYCO PTY LTD

- Qufora

- Hollister Incorporated

- Wellspect HealthCare (a Dentsply Sirona Company)

- Welland Medical Limited

Competitive Analysis:

The Bowel Management Systems Market features a competitive landscape dominated by key players such as Coloplast, Medtronic, Convatec Group, B. Braun Melsungen, and Hollister Incorporated. These companies focus on expanding their product portfolios through continuous innovation, clinical trials, and regulatory approvals. The market reflects strong competition in both hospital-based and homecare segments, with companies targeting user-friendly and cost-effective solutions. It also sees rising interest from regional manufacturers aiming to address affordability and local distribution challenges in emerging markets. Strategic partnerships, acquisitions, and regional expansions remain common growth strategies among top-tier players. Competitive differentiation often centers around device comfort, efficacy, infection control features, and digital integration. The Bowel Management Systems Market continues to evolve as companies adapt to patient-centric demands and increasing clinical emphasis on quality-of-life outcomes.

Recent Developments:

- In March 2025, Convatec announced an exclusive global collaboration with the Wound, Ostomy, and Continence Nurses Society™ (WOCN), the world’s largest professional nursing community in this field. The partnership will deliver two free educational initiatives—the Advanced Ostomy Care Program and the Ostomy Care Associates (OCA) Program—to enhance ostomy care knowledge among healthcare professionals, with initial launches in the US, UK, and Ireland.

- In February 2025, BD announced its intent to separate its Biosciences and Diagnostic Solutions business to enhance strategic focus and unlock value for shareholders. This restructuring aims to create a more focused, growth-oriented MedTech company, while also positioning the separated business as a leader in life sciences tools and diagnostics.

- In January 2024, Boston Scientific completed its acquisition of Axonics, Inc.

Boston Scientific expanded its urology and bowel dysfunction portfolio through a definitive acquisition of Axonics, Inc. The transaction, valued at approximately $3.7 billion in equity ($3.4 billion enterprise), included the Axonics R20™ and F15™ sacral neuromodulation systems for treating urinary and fecal incontinence.

- In February 2024, Coloplast launched Peristeen Light, a new transanal irrigation device.

Coloplast introduced Peristeen Light, a hand-held, low-volume irrigation solution designed to support users with bowel disorders. The device features intuitive assembly and a soft flexible catheter to improve comfort and usability

Market Concentration & Characteristics:

The Bowel Management Systems Market is moderately concentrated, with a few global players accounting for a significant share of overall revenue. It is characterized by high entry barriers due to regulatory compliance, product validation requirements, and the need for clinical acceptance. The market prioritizes safety, patient comfort, and ease of use, which drives innovation across product categories. Companies compete on product differentiation, cost efficiency, and distribution reach. It remains driven by both hospital-based procedures and the growing demand for homecare solutions. The market also exhibits a shift toward digital integration and customized offerings, reflecting evolving patient and provider expectations.

Report Coverage:

The research report offers an in-depth analysis based on type, patient type, and end use. It details leading market players, providing an overview of their business, product offerings, investments, revenue streams, and key applications. Additionally, the report includes insights into the competitive environment, SWOT analysis, current market trends, as well as the primary drivers and constraints. Furthermore, it discusses various factors that have driven market expansion in recent years. The report also explores market dynamics, regulatory scenarios, and technological advancements that are shaping the industry. It assesses the impact of external factors and global economic changes on market growth. Lastly, it provides strategic recommendations for new entrants and established companies to navigate the complexities of the market.

Future Outlook:

- Rising global prevalence of neurogenic and chronic bowel disorders will sustain long-term demand.

- Homecare segment is expected to lead growth due to increased adoption of self-administered systems.

- Pediatric-specific product development will open new opportunities in underserved markets.

- Digital health integration and remote monitoring will enhance treatment adherence and outcomes.

- Asia Pacific will continue to register the highest CAGR driven by healthcare expansion and awareness.

- Customizable and modular device designs will gain traction among healthcare providers.

- Strategic partnerships with regional distributors will improve market access in emerging economies.

- Sustainability-focused manufacturing and eco-friendly materials will influence procurement decisions.

- Regulatory approvals for innovative solutions such as neuromodulation devices will boost clinical use.

- Investments in patient education and stigma reduction campaigns will expand the addressable population.