Breast Pumps & Nursing Accessories Market Overview:

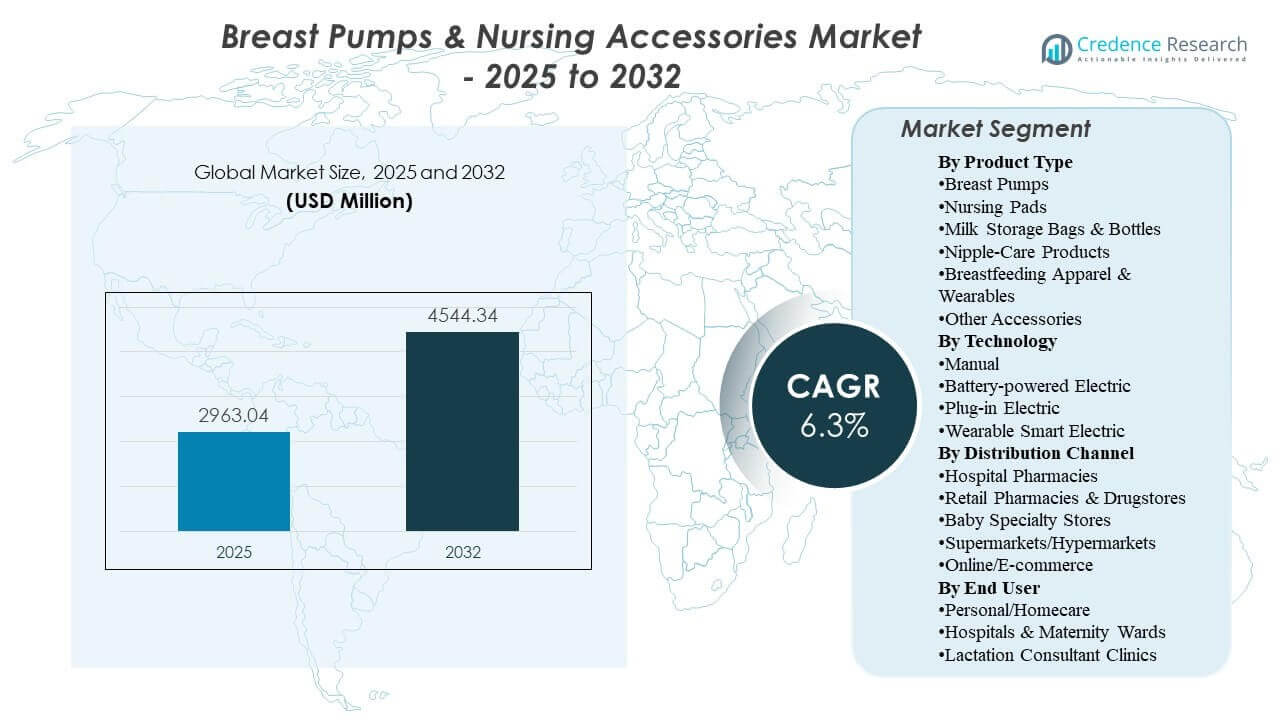

The global Breast Pumps & Nursing Accessories Market size was estimated at USD 2,963.04 million in 2025 and is expected to reach USD 4,544.34 million by 2032, growing at a CAGR of 6.3% from 2025 to 2032. Growth is primarily driven by rising pumping frequency among working mothers and the resulting need for convenient milk expression, storage, and comfort-support products across daily routines. Demand is also supported by product premiumization in hands-free pumping and broader retail and e-commerce availability, which expands access beyond traditional maternity care touchpoints.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Breast Pumps & Nursing Accessories Market Size 2025 |

USD 2,963.04 million |

| Breast Pumps & Nursing Accessories Market, CAGR |

6.3% |

| Breast Pumps & Nursing Accessories Market Size 2032 |

USD 4,544.34 million |

Key Market Trends & Insights

- The market is projected to expand from USD 2,963.04 million (2025) to USD 4,544.34 million (2032) at a 6.3% CAGR (2025–2032).

- Asia Pacific accounted for 33.1% of revenue in 2025, making it the largest regional contributor in the base year.

- North America represented 25.6% of revenue in 2025, supported by high penetration of pumping and accessories usage.

- Breast Pumps held 38.9% share in 2025 within product type, reflecting their central role in the overall category.

- Personal/Homecare accounted for 34.1% share in 2025, highlighting the dominance of at-home usage scenarios.

Segment Analysis

Demand formation is strongly linked to real-world feeding patterns where pumping and storage are used to manage schedule constraints, return-to-work transitions, and shared caregiving routines. As pumping becomes more integrated into everyday life, buyers increasingly evaluate products on comfort, time savings, portability, and ease of cleaning, which raises the importance of accessories such as storage bags, bottles, nipple-care items, and wearable-support apparel. In this context, brand trust and availability across trusted retail and pharmacy channels remain important for first-time mothers and gift purchasers.

Purchase behavior is also shaped by “ecosystem” adoption, where a pump purchase triggers repeat purchases of consumables and add-ons over the lactation period. Product portfolios that offer compatible storage systems, comfort components, and wearable solutions typically drive higher basket size and repeat sales. At the same time, e-commerce discovery and peer recommendations accelerate upgrades and switching, especially in premium hands-free formats that compete on convenience and discretion.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Product Type Insights

Breast Pumps accounted for the largest share of 38.9% in 2025. This leadership reflects the product’s essential role in enabling milk expression when direct breastfeeding is not feasible due to work schedules, medical needs, or lifestyle preferences. Pumps also act as the anchor purchase that drives follow-on demand for storage, hygiene, and comfort accessories, increasing total category spend per user. Continuous innovation around portability and hands-free use further strengthens pump adoption and replacement cycles.

By Technology Insights

Electric pumping solutions remain the preferred choice for frequent users because they reduce effort and shorten session time compared with manual alternatives. Battery-enabled portability supports usage across home, travel, and workplace settings, expanding the addressable user base beyond stationary routines. Wearable smart electric formats are increasingly positioned around discretion and mobility, which can drive premiumization and upgrades. Manual pumps remain relevant for occasional use cases and budget-sensitive buyers, especially as a backup option.

By Distribution Channel Insights

Retail Pharmacies & Drugstores accounted for the largest share of 21.8% in 2025. Pharmacies benefit from strong consumer trust, proximity to postnatal care journeys, and the ability to bundle purchases with other maternity and infant-care essentials. In-store availability supports immediate need purchases, particularly for pads, nipple-care products, and milk storage items. Pharmacy-led assortment and advice-oriented selling also help convert new mothers who seek reassurance on safety, hygiene, and product fit.

By End User Insights

Personal/Homecare accounted for the largest share of 34.1% in 2025. At-home use dominates because feeding schedules and pumping routines are most commonly managed within household settings and require convenient, repeatable workflows. Homecare demand is also reinforced by the need for privacy, comfort, and flexibility, which favors personal ownership of pumps and accessories rather than shared institutional use. Hospitals and maternity wards remain important for early-stage lactation support and clinical-grade equipment needs, while lactation consultant clinics influence purchasing through education and product guidance.

Market Drivers

Increasing integration of pumping into daily routines

Pumping is increasingly used to manage time constraints and enable feeding continuity when direct breastfeeding is disrupted. This expands demand not only for pumps but also for storage and comfort-support accessories that make frequent use easier. As routines become more structured, buyers prioritize products that reduce friction such as easier assembly, quicker cleaning, and reliable storage compatibility. The result is stronger repeat purchasing for consumables and add-on accessories.

- For instance, Medela’s Freestyle Hands-free uses collection cups with only 3 parts, includes 21 mm and 24 mm shield sizes, holds up to 150 ml/5 oz per cup, and delivers about 2 hours of battery life, or roughly eight 15-minute sessions, between charges.

Premiumization toward comfort, portability, and discretion

Demand is shifting toward products that improve comfort and allow hands-free or low-visibility use. Wearable and wearable-support products align with mobility needs and reduce perceived disruption, supporting adoption in working and commuting contexts. Comfort features, better fit options, and improved materials also increase willingness to pay in mid-to-premium tiers. This premiumization effect lifts average selling prices and supports category expansion.

- For instance, Willow Go starts each session with 6 stimulation levels, then shifts to 9 expression levels after 2 minutes, offers 5 oz and 7 oz container options, and is designed so users can walk around, eat dinner, or handle other light activities while pumping.

Channel expansion and broader availability of curated assortments

Wider distribution improves accessibility for first-time and repeat buyers and reduces time-to-purchase for urgent needs. Pharmacy channels play a key role in trusted, advice-adjacent buying behavior, especially for postpartum essentials. Strong assortment availability increases cross-selling between pumps, storage, and nipple-care solutions. Consistent availability across channels supports repeat purchase behavior across the lactation period.

Ecosystem purchasing and repeat consumption of accessories

Pump buyers often become repeat purchasers of storage bags, bottles, pads, and care products due to ongoing daily usage. Compatibility within a brand ecosystem and perceived hygiene advantages can drive stickiness and repeat buying. As usage frequency increases, customers value reliable replenishment and product consistency. This creates a predictable demand base for consumables and recurring accessories.

Breast Pumps & Nursing Accessories Market Challenges

Price sensitivity remains a constraint, especially for premium electric and wearable solutions, where total system cost can limit adoption in budget-constrained households. Even when demand exists, buyers may delay upgrades or choose entry-level alternatives, which can reduce premium mix in some regions. In addition, comfort and fit issues can lead to dissatisfaction and product returns, especially for first-time users who struggle with correct sizing and setup. Managing fit complexity at scale is a continuing execution challenge for brands.

- For instance, Elvie Pump highlights premium technical features such as a battery life of about 2.5 hours or 5–6 pumping sessions, 7 intensity settings, and breast shield options in 21 mm, 24 mm, and 28 mm, illustrating how brands are adding measurable fit and convenience features that can improve usability but also make product selection and setup more complex for new users.

Quality concerns, product durability expectations, and hygiene requirements also create friction, particularly for products requiring frequent cleaning and repeated daily use. Variability in user technique can affect perceived performance, increasing reliance on education and support to avoid churn. Channel competition can intensify discounting and reduce pricing power, especially where comparable products are widely available. Brands must balance promotional activity with long-term trust, safety perception, and customer support.

Market Trends and Opportunities

Wearable and hands-free usage formats continue to reshape product positioning as buyers seek mobility and discreet pumping. This creates opportunities for brands to expand accessory ecosystems such as wearable-support apparel, collection components, and comfort add-ons that complement hands-free routines. Product bundling strategies can increase conversion and improve lifetime value by connecting pumps with storage and care products. Strong ecosystem design also supports differentiation beyond core pump performance.

- For instance, Lansinoh’s wearable breast pump supports this positioning with battery life of up to 8 pumping sessions on a full charge, 8 oz click-tight collection cups, only 3 parts to clean, and four flange sizes included in the box—21 mm, 25 mm, 28 mm, and 30.5 mm—giving the brand a clear platform for fit-related accessories, storage solutions, and comfort-focused add-ons around the core device.

E-commerce is also expanding the addressable market by improving discovery, access to wider assortments, and the ability to compare features and user feedback. Digital content and peer-driven recommendations influence purchase decisions, supporting new customer acquisition and upgrades. Subscription and replenishment models for consumables can reduce churn and stabilize recurring revenue. Brands that align digital merchandising with education and fit guidance are better positioned to reduce returns and improve satisfaction.

Regional Insights

North America

North America accounted for 25.6% of revenue in 2025, supported by high penetration of pumping routines and strong accessory attach rates. Consumer preferences increasingly favor convenience and time efficiency, reinforcing demand for reliable pumping and storage systems. Pharmacy and retail availability supports rapid replenishment for consumables and postpartum essentials. Competitive intensity is high, with differentiation often driven by portfolio breadth and ecosystem compatibility across pumps and accessories.

Europe

Europe represented 23.4% of revenue in 2025, supported by established maternal-care pathways and broad retail and pharmacy access. Demand is influenced by product safety perception, comfort, and standardized routines that favor repeatable accessories usage. Buyers often prioritize predictable performance and ease of cleaning, which supports steady adoption across core categories. Premium wearable solutions are gaining attention in urban markets where discretion and mobility are valued.

Asia Pacific

Asia Pacific led the market with 33.1% share in 2025, reflecting a large addressable population and rising adoption of pumping and accessory ecosystems in urban centers. Expanding middle-income households and growing workforce participation among mothers support increasing usage frequency and cross-category purchasing. E-commerce and modern retail improve accessibility and product discovery, accelerating adoption across tier-1 and tier-2 cities. Brands that balance affordability with convenience features are well-positioned in this region.

Latin America

Latin America accounted for 9.6% of revenue in 2025, with demand concentrated in urban and higher-income segments. Access and affordability continue to influence product mix, with a stronger tilt toward essential items and value-oriented solutions. Retail availability and consumer education play important roles in supporting conversion and repeat purchases. Growth opportunities are tied to improved channel reach and broader availability of trusted brands.

Middle East & Africa

Middle East & Africa contributed 8.3% of revenue in 2025, shaped by uneven purchasing power and varying access to modern retail and maternity care services. Demand tends to be stronger in major cities where awareness, product availability, and private healthcare influence adoption. Practicality and affordability often guide purchasing decisions, supporting steady demand for core accessories and entry-to-mid products. Expanding retail footprints and improved education can broaden category penetration over time.

Competitive Landscape

Competition is centered on portfolio breadth across pumps and accessories, comfort and fit ecosystems, and channel execution across pharmacy, baby retail, and digital platforms. Companies differentiate through product design (hands-free vs conventional), usability (cleaning and assembly), and ecosystem compatibility that increases repeat purchases for storage and care products. Brand trust remains a key purchase driver in postpartum categories, making product safety perception and customer support strategically important. Innovation cycles increasingly focus on convenience features and integrated accessory bundles that improve the end-to-end pumping workflow.

Medela AG is typically positioned around a broad lactation-focused portfolio that spans pumps and supporting accessories designed to improve comfort, consistency, and workflow reliability. Its approach often emphasizes compatibility across components, enabling repeat purchases and easier replenishment of commonly used items. A wide product range can also support multiple price tiers and use cases, from occasional home use to more frequent routines. This ecosystem depth can strengthen retention by reducing switching costs once a user is established in a specific product set.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Medela AG

- Pigeon Corporation

- Koninklijke Philips N.V.

- Ameda, Inc.

- Willow Innovations, Inc.

- Lansinoh Laboratories, Inc.

- Elvie (Chiaro Technology)

- Spectra Baby / Uzin Medicare

- Motif Medical

- Tommee Tippee

- Hygeia Health

- Freemie

- Haakaa

- Momcozy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In January 2026, Lansinoh launched the NaturalWave Double Electric Breast Pump, positioning it as a next-generation power pump designed to help mothers express milk and support milk-supply maintenance through its Flutter Technology.

- In August 2025, Philips launched the Philips Avent Hands-free Electric Breast Pump in India, highlighting features such as Natural Motion Technology, a hospital-strength motor, and SkinSense breast shields to make pumping more comfortable and discreet for mothers.

- In July 2025, Medela launched Magic InBra in Canada, describing it as its most advanced wearable breast pump and emphasizing its ultra-slim design, clinically validated 105 degree breast shields, and hospital-grade performance in a wearable format.

- In January 2025, Momcozy announced the U.S. launch of the Air 1 Ultra-Slim Breast Pump, a wearable model developed with input from maternal health experts and mothers, with features including a transparent top, wireless charging case, app control, and quieter operation.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 2,963.04 million |

| Revenue forecast in 2032 |

USD 4,544.34 million |

| Growth rate (CAGR) |

6.3% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2025–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Product Type Outlook: Breast Pumps, Nursing Pads, Milk Storage Bags & Bottles, Nipple-Care Products, Breastfeeding Apparel & Wearables, Other Accessories;

By Technology Outlook: Manual, Battery-powered Electric, Plug-in Electric, Wearable Smart Electric;

By Distribution Channel Outlook: Hospital Pharmacies, Retail Pharmacies & Drugstores, Baby Specialty Stores, Supermarkets/Hypermarkets, Online/E-commerce;

By End User Outlook: Personal/Homecare, Hospitals & Maternity Wards, Lactation Consultant Clinics |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

Medela AG, Pigeon Corporation, Koninklijke Philips N.V., Ameda, Inc., Willow Innovations, Inc., Lansinoh Laboratories, Inc., Elvie (Chiaro Technology), Spectra Baby / Uzin Medicare, Motif Medical, Tommee Tippee, Hygeia Health, Freemie, Haakaa, Momcozy |

| No. of Pages |

320 |

Segmentation

By Product Type

- Breast Pumps

- Nursing Pads

- Milk Storage Bags & Bottles

- Nipple-Care Products

- Breastfeeding Apparel & Wearables

- Other Accessories

By Technology

- Manual

- Battery-powered Electric

- Plug-in Electric

- Wearable Smart Electric

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies & Drugstores

- Baby Specialty Stores

- Supermarkets/Hypermarkets

- Online/E-commerce

By End User

- Personal/Homecare

- Hospitals & Maternity Wards

- Lactation Consultant Clinics

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa