Bromelain Products Market Overview:

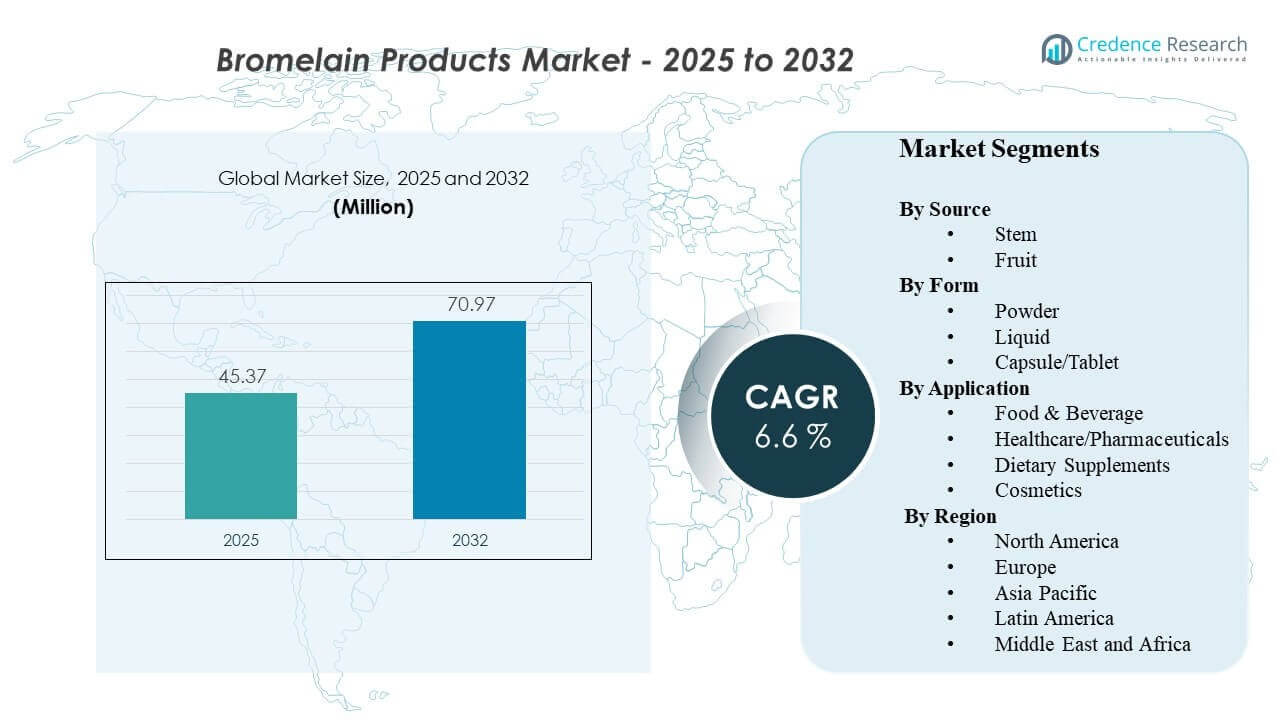

The global Bromelain Products Market size was estimated at USD 45.37 million in 2025 and is expected to reach USD 70.97 million by 2032, growing at a CAGR of 6.6% from 2025 to 2032. Demand is being shaped by wider use of bromelain across wellness and therapeutic positioning, where buyers increasingly evaluate products on activity consistency, traceability of enzyme source, and claims reliability. In parallel, broader adoption in processed food applications and personal care formulations is supporting steady volume pull-through across multiple channels.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2024 |

| Base Year |

2025 |

| Forecast Period |

2026-2032 |

| Bromelain Products Market Size 2025 |

USD 45.37 million |

| Bromelain Products Market, CAGR |

6.6% |

| Bromelain Products Market Size 2032 |

USD 70.97 million |

Key Market Trends & Insights

- The market is projected to expand from USD 45.37 million (2025) to USD 70.97 million (2032) at a 6.6% CAGR (2025–2032).

- Stem-based bromelain is estimated at 58.9% share in 2025, reflecting preference for consistent enzymatic activity and standardized supply.

- Powder form is estimated at 43.6% share in 2025, supported by stability advantages in distribution and storage-sensitive applications.

- North America is estimated at 38.90% share in 2025, underpinned by mature dietary supplement demand and established quality-driven procurement.

- Independent testing referenced in market discussions indicated 75% of select online bromelain supplement listings did not meet potency claims, increasing the importance of verification and compliance-led positioning.

Segment Analysis

The market’s segmentation patterns are influenced by quality expectations and end-use performance requirements. Buyers in regulated or specification-driven channels tend to favor bromelain inputs with reliable activity units, clear origin documentation, and stronger batch-to-batch repeatability. This dynamic supports a sustained tilt toward upstream processing discipline, validated assays, and stable formats that can better retain activity through storage and logistics.

At the same time, consumer-facing demand remains sensitive to trust signals such as third-party testing, transparent labeling, and consistent outcomes. This is especially relevant where bromelain is positioned for wellness benefits, recovery use-cases, or blended formulations. As market participants compete across food, supplement, and personal care applications, differentiated quality systems and fit-for-purpose format selection become central to maintaining price realization and repeat purchases.

By Source Insights

Stem accounted for the largest share of 58.9% in 2025. It leads due to stronger alignment with standardized activity expectations, particularly where buyers require predictable performance in downstream formulations. Stem sourcing is also commonly associated with more consistent enzyme yield characteristics, supporting tighter quality control and more repeatable specifications. In institutional and higher-assurance channels, documented processing controls and validated assays reinforce stem-based preference.

By Form Insights

Powder accounted for the largest share of 43.6% in 2025. It benefits from better shelf stability and easier handling across multi-step supply chains where moisture sensitivity and storage conditions can affect enzyme performance. Powder formats also support scalable packaging, inventory management, and consistent dosing in manufacturing environments. For brands competing on reliability, powders are often easier to standardize and validate compared with more variable liquid activity retention over time.

By Application Insights

Food & beverage usage is supported by bromelain’s proteolytic functionality and processing utility, especially where manufacturers need repeatable performance in ingredient systems. Healthcare/pharmaceutical interest is influenced by structured protocols and the need for higher specification confidence, which elevates the role of validated activity units and quality documentation. Dietary supplements remain demand-rich but increasingly scrutiny-led, with buyers paying closer attention to potency verification and claims substantiation. Cosmetics adoption is supported by enzyme-driven exfoliation positioning and preference for plant-derived actives in formulation trends.

Bromelain Products Market Drivers

Expanding use in supplements and wellness positioning

Bromelain is increasingly incorporated into supplements positioned for digestive support, recovery, and broad wellness routines. As product portfolios expand, brands seek more dependable enzyme inputs to protect repeatability and customer outcomes. This pushes suppliers to strengthen assay validation and documentation to support label claims. Over time, higher quality thresholds can lift value capture even in price-sensitive consumer channels.

- For instance, Pure Encapsulations sells Bromelain 2400 in both 500 mg and 250 mg capsule formats, with a declared potency of 2,400 GDU/g and labeled directions of 1–4 capsules per day for the 500 mg format and 4–8 capsules per day for the 250 mg format, showing how established supplement brands anchor positioning in quantified enzyme activity and controlled dosing formats.

Growth in processed food and ingredient functionality demand

Food processors use bromelain for functional roles where enzymatic action delivers measurable processing outcomes. The market benefits when manufacturers prioritize consistent enzyme activity and formulation compatibility at scale. Supplier capability to offer standardized, stable bromelain formats supports broader adoption across diverse processing environments. These dynamics sustain baseline industrial demand even when consumer channels fluctuate.

- For instance, Enzybel Asia Pacific states that it serves protein processing and food industries through a fully vertically integrated bromelain chain from production to sales and lists five commercial activity grades—1200, 1600, 2000, 2400, and 2500 GDU/g—giving manufacturers a defined potency ladder for scaled food-processing applications.

Increased importance of quality assurance and potency verification

Buyer attention to verified potency is rising due to variability concerns in certain retail and online listings. This strengthens demand for suppliers and brands that can demonstrate robust testing, traceability, and batch documentation. Quality-first positioning becomes a competitive lever for premiumization and institutional penetration. As verification becomes more normalized, under-validated products face higher substitution risk.

Wider adoption in personal care formulations

Cosmetic formulators are incorporating enzymatic actives into products positioned around exfoliation, renewal, and skin feel improvements. Bromelain benefits from plant-derived positioning that aligns with clean-label and naturally-inclined product narratives. Suppliers that provide stability guidance and compatible formats can improve adoption outcomes for formulators. This drives incremental demand beyond traditional supplement use-cases.

Bromelain Products Market Challenges

A key challenge is managing variability in perceived efficacy when products are not standardized to consistent activity units. Differences in sourcing, processing, storage, and labeling practices can contribute to uneven customer outcomes, which can weaken trust and increase churn. As scrutiny on claims grows, brands may face higher compliance and testing requirements, increasing time-to-market and cost burdens.

Another challenge is maintaining activity stability across distribution and storage environments, particularly for formulations exposed to heat, humidity, or long transit times. Enzymes can lose effectiveness if packaging, stabilization, or handling is not optimized. This can create performance gaps between product promise and real-world usage. As a result, suppliers must invest in stronger stabilization and quality systems to protect downstream performance.

- For instance, Green Leaf Extractions specifies its Bromelain 2400 GDU in full and tight containers away from direct heat and light at 24-25°C, states a shelf life of not more than 2 years under those storage conditions, and sets loss on drying at a maximum of 4.0%, demonstrating how measurable storage and moisture-control parameters are built into commercial stability management.

Bromelain Products Market Trends and Opportunities

The market is moving toward clearer standardization of activity labeling and stronger verification practices, which favors suppliers that can consistently demonstrate batch performance. This trend supports differentiation beyond price and increases the value of documented QA systems. Brands with stronger testing narratives can build trust and reduce returns, especially in online channels. Over time, verification-led competition can shift purchasing decisions toward more reliable suppliers.

- For instance, Szymotech Biosolutions lists its Bromelain Br at a minimum activity of 2,400 GDU/g with a stated measurement accuracy of +/-5%, loss on drying capped at 6% w/w, and microbiological limits such as Salmonella absent in 25 g, giving buyers concrete batch-level benchmarks to evaluate supplier reliability.

Another opportunity lies in application-driven product engineering, where suppliers tailor bromelain forms and specifications to end-use needs. This includes stability-focused powders, improved processing controls, and better compatibility guidance for formulators. Suppliers that support customers with technical documentation and usage recommendations can improve retention and increase cross-application adoption. These service layers can raise switching costs and support long-term partnerships.

Regional Insights

North America

North America is estimated at 38.90% share in 2025, supported by mature supplement demand, established specialty retail channels, and stronger buyer emphasis on validation and claims reliability. Purchasers often prioritize consistency, documentation, and product standardization, which supports higher-quality supplier positioning. Competitive intensity is shaped by brand trust and potency verification expectations.

Europe

Europe is estimated at 22.70% share in 2025, reflecting established nutraceutical markets, regulated labeling practices, and steady ingredient procurement for health and wellness products. Buyers often evaluate products on compliance alignment and consistent performance. Suppliers that can support documentation and standardized specifications are better positioned for sustained demand.

Asia Pacific

Asia Pacific is estimated at 24.60% share in 2025, supported by large consumer bases, expanding wellness adoption, and broad manufacturing ecosystems that pull enzyme ingredients into multiple use-cases. Demand is influenced by affordability, availability, and increasing interest in product integrity. Suppliers that balance cost-competitiveness with reliable quality controls can scale faster in this region.

Latin America

Latin America is estimated at 8.40% share in 2025, with demand supported by growing supplement adoption and food processing applications, but constrained by uneven purchasing power and distribution maturity across markets. Buyers may be more price-sensitive, which heightens competition among suppliers. Brands that can maintain acceptable quality while managing cost are advantaged.

Middle East & Africa

Middle East & Africa is estimated at 5.40% share in 2025, reflecting smaller structured demand and variable retail access across countries. Growth is more selective and tied to distribution development and premium wellness uptake in certain sub-markets. Suppliers often need stronger partner networks to improve reach and reliability.

Competitive Landscape

Competition is shaped by product quality validation, source traceability, assay standardization, and the ability to serve multiple end-use channels with consistent performance. Suppliers differentiate through activity-unit consistency, documentation strength, and format options that preserve enzyme stability. Customer retention improves when suppliers provide technical support and reliable batch repeatability, particularly for formulators and specification-driven buyers.

Advanced Enzyme Technologies typically competes by combining enzyme development expertise with scalable manufacturing and broader enzyme portfolio credibility. Its positioning can benefit from process controls, standardized production, and support capabilities for application-specific requirements. As buyers place greater emphasis on verification and repeatable outcomes, suppliers with stronger QA systems and documentation are better placed to defend pricing and expand institutional and formulation-led demand.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

Recent Developments

- In August 2025, Advanced Enzyme Technologies reported an acquisition-related update under Regulation 30, stating that its board had approved a Rs. 10 million investment in Advanced Nutrazyme Private Limited, its existing wholly owned subsidiary.

- In November 2024, Creative Enzymes launched new enzymatic solutions for sustainable leather processing, positioning the products around higher processing efficiency and lower environmental impact. This is a recent product-launch update, although it is not bromelain-specific.

- In an August 2025, Enzybel Pharma 2, an Enzybel-branded business under Natix, entered a partnership with Deebio to help address global pancrelipase shortages through a highly purified, standardized API and a dedicated manufacturing setup.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 45.37 million |

| Revenue forecast in 2032 |

USD 70.97 million |

| Growth rate (CAGR) |

6.6% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026-2032 |

| Quantitative units |

USD million |

| Segments covered |

By Source; By Form; By Application |

| Regional scope |

North America; Europe; Asia Pacific; Latin America; Middle East & Africa |

| Key companies profiled |

Advanced Enzyme Technologies; Biozyme Laboratories; Challenge Bioproducts; Creative Enzymes; Enzybel International; Guangxi Nanning Jiuzhou Group; Hong Mao Biochemicals; Nanning Pangbo Bioengineering |

| No. of Pages |

332 |

Segmentation

By Source

By Form

- Powder

- Liquid

- Capsule/Tablet

By Application

- Food & Beverage

- Healthcare/Pharmaceuticals

- Dietary Supplements

- Cosmetics

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa