Building Integrated Photovoltaic (BIPV) Market Overview:

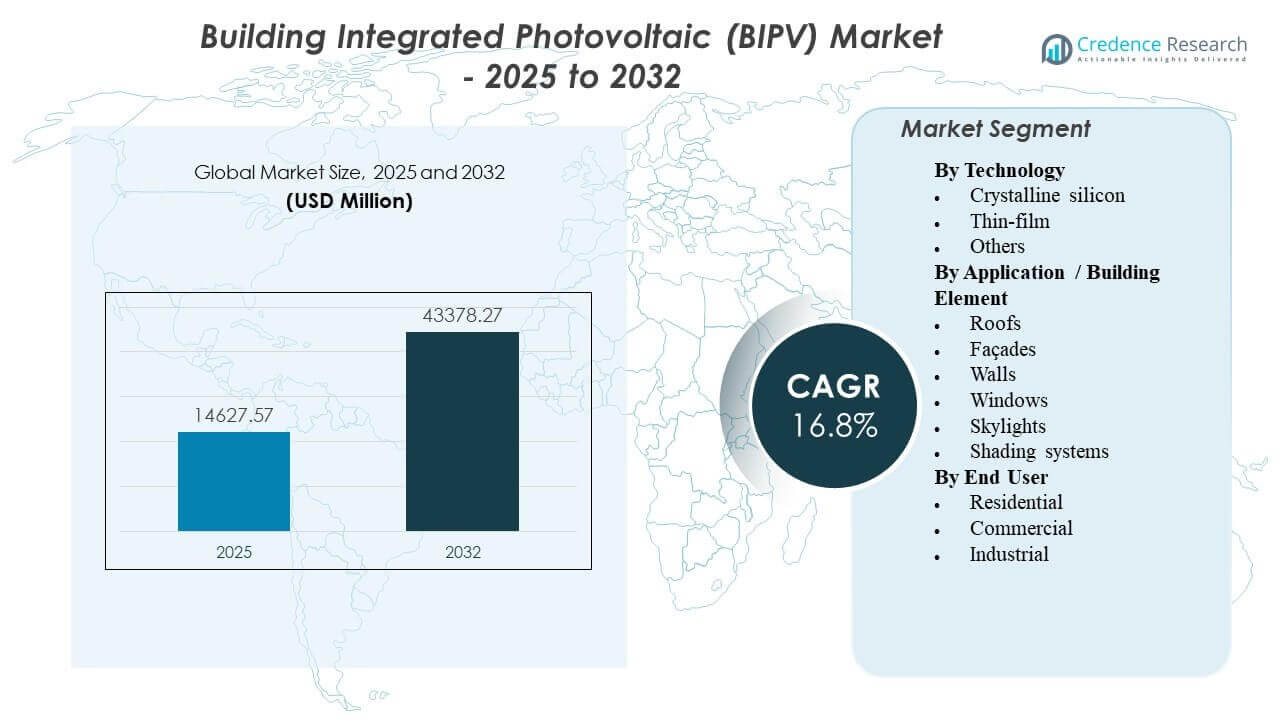

The global Building Integrated Photovoltaic (BIPV) Market size was estimated at USD 14,627.57 million in 2025 and is expected to reach USD 43,378.27 million by 2032, growing at a CAGR of 16.8% from 2025 to 2032. Growth is primarily driven by stricter building energy codes and net-zero building targets that push developers to integrate on-site generation into roofs, façades, and glazing. Demand is also supported by improving product aesthetics and wider availability of integrated solar building materials across premium residential and commercial projects.

| REPORT ATTRIBUTE |

DETAILS |

| Historical Period |

2020-2023 |

| Base Year |

2024 |

| Forecast Period |

2025-2032 |

| Building Integrated Photovoltaic (BIPV) Market Size 2025 |

USD 14,627.57 million |

| Building Integrated Photovoltaic (BIPV) Market, CAGR |

16.8% |

| Building Integrated Photovoltaic (BIPV) Market Size 2032 |

USD 43,378.27 million |

Key Market Trends & Insights

- The Building Integrated Photovoltaic (BIPV) Market is expanding at a CAGR of 8% during 2025–2032.

- Europe accounted for the largest regional share of 9% in 2025, supported by stronger green-building adoption and regulatory pressure for building decarbonization.

- Crystalline silicon remained the leading technology with a share of 9% in 2025, reflecting efficiency-led project selection for building envelopes.

- Roofs represented the largest building-element application with 8% share in 2025, supported by usable surface area and straightforward integration in new builds and retrofits.

- Commercial end users held 1% share in 2025, driven by larger project sizes, ESG-linked procurement, and building performance benchmarking.

Segment Analysis

The Building Integrated Photovoltaic (BIPV) Market is shaped by a shift from add-on rooftop PV toward integrated building-envelope solutions that combine power generation with structural or architectural function. Developers and asset owners increasingly evaluate BIPV as a design-led energy asset that can support compliance with energy-performance standards, reduce operational emissions, and improve building value proposition. Procurement decisions frequently weigh aesthetics, durability, warranty strength, and integration complexity alongside energy yield.

Technology selection is guided by bankability and performance reliability, with most projects prioritizing proven module efficiency and predictable lifecycle output. Roof-led deployments dominate near-term volumes because roof surfaces offer scale and simplified integration, especially for commercial buildings targeting measurable reductions in grid electricity use. End-user adoption remains strongest in commercial buildings, where payback pathways are clearer through larger load profiles, centralized decision-making, and sustainability reporting requirements.

Access crucial information at unmatched prices!

Request your sample report today & start making informed decisions powered by Credence Research Inc.!

Download Sample

By Technology Insights

Crystalline silicon accounted for the largest share of 68.9% in 2025. Crystalline silicon leadership is supported by higher conversion efficiency and mature supply chains that reduce project performance risk. Many building-envelope projects prioritize dependable yield, long service life, and standardized installation ecosystems, which favors crystalline silicon formats. Thin-film solutions remain relevant for design flexibility and lightweight applications, but crystalline silicon remains preferred for yield-focused roof and façade integration.

By Application / Building Element Insights

Roofs accounted for the largest share of 65.8% in 2025. Roof surfaces typically provide the highest usable area and simpler construction pathways compared with façade or glazing elements, supporting broader adoption in both new builds and retrofits. Roof-integrated BIPV also aligns well with self-consumption strategies in commercial buildings that can absorb daytime generation. Façades, windows, skylights, and shading systems grow through architectural differentiation, but these elements commonly require higher engineering coordination and customized specifications.

By End User Insights

Commercial accounted for the largest share of 53.1% in 2025. Commercial adoption benefits from larger project scale, structured capital planning, and stronger pressure to document building-energy performance improvements. Many commercial deployments pair BIPV with energy-management upgrades to demonstrate measurable reductions in operational emissions. Residential demand is supported by premium housing projects and incentive-driven adoption, whereas industrial uptake is more selective and concentrated in sites with suitable envelopes and higher energy intensity.

Building Integrated Photovoltaic (BIPV) Market Drivers

Building decarbonization mandates and energy-performance regulations

Building energy codes and carbon-reduction requirements are pushing developers toward envelope-integrated renewables as part of compliance planning. BIPV supports on-site generation without requiring additional land area, making adoption relevant in dense urban environments. Net-zero and near-zero energy building targets increase the value of integrated solutions that contribute to annual energy balance. Public-sector procurement and green-building certification requirements further reinforce BIPV specification in new projects.

- For instance, the Perpignan Saint-Charles fruit logistics warehouse in France integrated about 97,000 solar shingles over a 7-hectare roof to create an approximately 11 MW BIPV system that generates around 10.7 GWh of electricity per year, directly supporting on-site decarbonization goals under French building energy regulations.

Rising commercial sustainability commitments and ESG-linked investment

Corporate sustainability targets increasingly translate into building-level actions, especially in offices, retail, and institutional buildings. BIPV offers a visible and measurable decarbonization pathway that can strengthen green-lease positioning and tenant preferences. Portfolio owners also use on-site generation to reduce exposure to electricity price volatility and strengthen energy resilience planning. Financing frameworks that favor low-carbon buildings can improve project economics for integrated PV installations.

Advances in PV building materials and improved architectural acceptance

Product innovation across PV glass, façade modules, and lightweight solutions improves design flexibility and reduces aesthetic barriers. Better integration approaches reduce balance-of-system complexity, helping architects specify PV within building envelope packages. Improvements in durability and system warranties support higher confidence among developers and owners. As installed references expand, the market benefits from faster specification cycles and broader familiarity among design and engineering stakeholders.

- For instance, a retrofit project with colored BIPV façade modules documented by IEA PVPS accepted an estimated performance loss of around 35% compared with standard modules in exchange for improved visual quality, demonstrating how new materials balance aesthetics with quantified energy outputs.

Urbanization and growth in new construction and premium retrofits

New construction and deep retrofit activity create natural decision points to adopt integrated envelope materials. BIPV is increasingly considered during roof replacement, façade refurbishment, and glazing upgrades where incremental integration costs can be optimized. Urban density favors solutions that generate electricity without additional footprint beyond the building envelope. Premium residential and commercial projects also use BIPV to differentiate architecture and support energy-performance outcomes.

Building Integrated Photovoltaic (BIPV) Market Challenges

BIPV projects often face higher upfront costs and more complex design coordination than conventional rooftop PV, especially for façade and glazing integration. Building-envelope integration requires alignment across architects, façade contractors, electrical teams, and permitting authorities, which can extend timelines and elevate execution risk. Product standardization remains uneven across geographies, and differences in local codes can add specification friction. These factors can slow adoption when project stakeholders prioritize short-cycle delivery.

- For instance, Onyx Solar’s BIPV glass for the Atlassian headquarters in Sydney integrates 1,800 custom solar glass louvres, each with 28 monocrystalline cells producing 138 Wp per unit for a total of 247 kWp.

Supply-chain and installer readiness can also constrain deployment, particularly for specialized glazing and façade products that require trained partners and tailored installation methods. Performance expectations must be managed because orientation and shading vary widely across building designs, affecting yield predictability. Maintenance planning and warranty alignment across multiple contractors can become complicated without clear responsibility mapping. These issues can limit adoption outside premium projects and highly coordinated commercial builds.

Building Integrated Photovoltaic (BIPV) Market Trends and Opportunities

Integrated solar façades and PV glazing are gaining visibility as architects seek multifunctional building materials that combine aesthetics with energy generation. Transparent and semi-transparent solutions expand addressable surfaces beyond rooftops and support deployment in commercial buildings with large façade areas. Product modularity and customization options improve spec readiness for diverse building designs. These advances create opportunity for solution providers that can offer design support and predictable performance modeling.

- For instance, the Solaire residential tower in New York integrates a façade BIPV array using monocrystalline silicon wafers that achieved an energy payback time of 0.8 years when crediting the cladding it replaces, and 3.8 years under conventional wafer assumptions, demonstrating both architectural integration and quantified lifecycle efficiency.

Partnership-driven go-to-market models are also expanding, with collaboration between PV innovators, façade system providers, and large construction supply chains. Such partnerships improve access to project pipelines and reduce customer acquisition friction in construction-led procurement. Demand is also increasing for integrated solutions bundled with energy-management systems and building-performance analytics. This trend supports higher-value offerings that combine product, integration services, and long-term performance assurance.

Regional Insights

North America

North America accounted for 22.9% of the BIPV market in 2025, supported by stronger uptake in commercial buildings where sustainability targets and energy-resilience planning influence investment decisions. Developers increasingly evaluate envelope-integrated solar during roof replacements and high-performance retrofit cycles, particularly in premium office, retail, and institutional projects. Adoption is reinforced by the growing presence of green-building design firms, energy-service partners, and specialized installers. Overall traction remains strongest in commercial deployments, with selective penetration in higher-income residential segments.

Europe

Europe led the global BIPV market with a 40.9% share in 2025, driven by high green-building penetration and tighter policy pressure to improve building energy performance. Developers more frequently treat building envelopes as energy assets, supporting BIPV integration across roofs and façade systems in both new builds and deep retrofits. A mature ecosystem of architects, façade specialists, and product suppliers improves specification readiness and execution consistency. These conditions sustain broader adoption across commercial buildings and public-sector infrastructure.

Asia Pacific

Asia Pacific represented 26.1% of the market in 2025, supported by high construction activity in major cities and increasing adoption of energy-efficient building designs. Large commercial developments provide substantial roof and façade surface area, improving feasibility for integrated PV deployment. Regional manufacturing depth strengthens product availability across multiple PV formats and building-material configurations, supporting price-performance competitiveness. Growth is further reinforced by smart-city and green-infrastructure programs that prioritize integrated sustainability features.

Latin America

Latin America captured 5.4% of the BIPV market in 2025, reflecting selective adoption concentrated in premium commercial and institutional projects. In many markets, conventional rooftop PV remains the preferred option on cost and simplicity, limiting BIPV adoption outside design-led builds. However, flagship green-building developments and high-irradiance urban corridors support incremental demand for integrated roof and façade solutions. Penetration improves when BIPV is aligned with retrofit cycles and building-material replacement decisions.

Middle East & Africa

Middle East & Africa accounted for 4.7% of the market in 2025, with deployments concentrated in landmark commercial projects and high-visibility developments where aesthetics and sustainability positioning matter. High solar resource supports strong generation potential, but adoption remains constrained by higher solution costs, specialized installation needs, and limited standardization across projects. Market progress depends on deeper ecosystem development among façade contractors, designers, and qualified suppliers. Wider adoption is expected as integrated PV materials become more standardized and procurement becomes easier for mainstream projects.

Competitive Landscape

Competition in the Building Integrated Photovoltaic (BIPV) Market is driven by product differentiation across PV glass, façade-integrated systems, lightweight thin-film formats, and integrated roofing solutions. Market participants compete on efficiency, aesthetics, durability, and integration support for architects and façade contractors. Commercial success often depends on building-code compatibility, warranty strength, and the ability to deliver predictable performance through modeling and installation guidance. Partnerships with construction supply chains and design firms remain critical for scaling deployments.

AGC Inc. is positioned around building-glass capabilities that align with façade and glazing-led BIPV pathways. Product development and collaboration models that integrate PV functionality into architectural glass can reduce adoption barriers for designers seeking energy-generating envelopes. Building-material distribution strength and relationships with façade stakeholders can improve project specification and execution consistency. Such capabilities support participation in design-led commercial projects where performance, aesthetics, and compliance requirements converge.

Shape Your Report to Specific Countries or Regions & Enjoy 30% Off!

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AGC Inc.

- SolarWindow Technologies, Inc.

- Hanergy Mobile Energy Holding Group Limited

- Heliatek GmbH

- Tesla Inc.

- Ascent Solar Technologies, Inc.

- Onyx Solar

- SoliTek UAB

- Mitrex Integrated Solar Technology Inc.

- ML System

- Dyesol

- SolTech Energy

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments

- In October 2025, Mumbai-based Aelius Turbina announced its expansion into manufacturing BIPV products, including solar roof tiles, floor tiles, and facade panels, alongside plans to inaugurate a dedicated BIPV manufacturing facility in January 2026 to support growing demand for integrated solar building materials.

- In June 2025, Kameleon Solar partnered with India-based Nithin Sai Renewables Pvt. Ltd. to expand Kameleon’s BIPV solutions into the Indian market, with the collaboration focused on boosting deployment of integrated solar facades and other architecturally integrated PV products.

- In July 2024, LONGi Green Energy Technology Co. Ltd. formed a strategic partnership with Kingspan to collaborate on integrated BIPV and building-applied PV (BAPV) systems, combining LONGi’s high-efficiency solar technologies with Kingspan’s building envelope expertise to deliver tested solutions for net-zero energy buildings.

Report Scope

| Report Attribute |

Details |

| Market size value in 2025 |

USD 14,627.57 million |

| Revenue forecast in 2032 |

USD 43,378.27 million |

| Growth rate (CAGR) |

16.8% (2025–2032) |

| Base year |

2025 |

| Forecast period |

2026–2032 |

| Quantitative units |

USD million |

| Segments covered |

By Technology Outlook: Crystalline silicon, Thin-film, Others; By Application / Building Element Outlook: Roofs, Façades, Walls, Windows, Skylights, Shading systems; By End User Outlook: Residential, Commercial, Industrial |

| Regional scope |

North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Key companies profiled |

AGC Inc., SolarWindow Technologies, Inc., Hanergy Mobile Energy Holding Group Limited, Heliatek GmbH, Tesla Inc., Ascent Solar Technologies, Inc., Onyx Solar, SoliTek UAB, Mitrex Integrated Solar Technology Inc., ML System, Dyesol, SolTech Energy |

| No. of Pages |

328 |

Segmentation

By Technology

- Crystalline silicon

- Thin-film

- Others

By Application / Building Element

- Roofs

- Façades

- Walls

- Windows

- Skylights

- Shading systems

By End User

- Residential

- Commercial

- Industrial

By Region

- North America

- Europe

- Germany

- France

- U.K.

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- South-east Asia

- Rest of Asia Pacific

- Latin America

- Brazil

- Argentina

- Rest of Latin America

- Middle East & Africa

- GCC Countries

- South Africa

- Rest of the Middle East and Africa